Category Archives: Sector Trends

Oops a whipsaw

I tend to focus on risk management in these occasional observations I share.

My focus is on risk management because that’s my edge.

If I can direct and control my possibility of loss through tactical trading decisions, then I’m left to focus on the upside of profits.

I pinned that on my wall twenty years ago when I was testing asymmetric trading systems for asymmetric risk/reward and asymmetric investment returns.

As I intensely studied the mathematical expectation of trading systems, I concluded the downside drawdown is the part I have the potential to control.

If a position is trending down, I can exit, and reduce my exposure to zero.

I could also use exchange-traded options for defined risk. ie. if I buy a call option for $5 that’s all I can lose if the position doesn’t become profitable.

I could instead place a stop loss exit $5 below the entry price for a similar effect, but the position could gap down $10, and the loss would be larger than the limited call option would have been.

These are the kind of portfolio management decisions we get to choose from as investment portfolio managers.

I discuss this more in How is trend following with a stop loss optionality similar to a call option?

Our issue at hand today is the trendline whipsaw of the stock market index.

In Stock Market Resumes Downtrend I shared the observation the U.S. stock market as measured by the S&P 500 stock index, has trended down from a lower high.

Here’s the chart:

I went on to point out the stock index wasn’t yet oversold, and the number of stocks in the 500 in an uptrend was trending down.

Trend lines aren’t magic; they’re just a general trend guide.

I wasn’t seeing heavy selling pressure, so I thought “we’ll see.”

Here’s an update. See below for the context of the numbers.

- The downtrend line for the S&P 500 is now negated as the stock market has reversed back up and the index easily trended above the trendline and broke out to the upside. This will likely drive some to call the bear market over and suggest a new bull market has begun.

- Momentum, as measured by 14-day relative strength, indicates the SPX isn’t yet overbought at 62, and I’d only consider it so above 80. Read: there’s still room to run if it wants. There will be little resistance from velocity moving too far too fast.

- The percent of SPX 500 stocks trending above their 200-day moving averages is at 67%, so 33% of the stocks could still trend up, and 67% isn’t a level I consider resistance. That is, if it were at 80% it would indicate most stocks have already trended up, so the desire to buy may be getting exhausted.

- The average true range of the past 15 days shows a visual representation that realized volatility is declining. In fact, realized vol has declined to the August 2022 level.

I’ll stop there to keep this succinct.

The bottom line is the stock market was trending down, and it’s now reversed back up into a notable uptrend.

I started with observations of risk management because no indicator is ever perfect, they’ll all imperfect.

When every new moment is unique, and we’ve never been “here” before, anything can happen.

The best we can do is define the direction of the trend and follow it, until it reaches an extreme, or reverses down.

Ironically, as the realized volatility is now as low as it was in August 2022, that’s also when I shared Whipsaw and warned I have a hunch we’re going to hear the word “whipsaw” a lot in the coming months.

For the past year, we’ve survived and thrived through a prolonged bear market that may be much longer and deeper if the U.S. economy enters a recession.

Only time will tell if the U.S. is in a recession, or if we’ll instead see the soft landing our friends at Goldman Sachs expect.

But for now, the U.S. equities trend is back up again, and the Fed’s interest rate decision next week will likely be the driver of what happens next.

I expect 2023 to be a very challenging year for macro economics, and it’ll be fun to watch.

At Shell Capital, we just want to repeat another profitable year like last year, or better.

Mike Shell is the founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Managed Portfolios. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as investment advice to buy or sell any security. This information does not suggest in any way that any graph, chart, or formula offered can solely guide an investor as to which securities to buy or sell, or when to buy or sell them. Securities reflected are not intended to represent any client holdings or recommendations made by the firm. In the event any past specific recommendations are referred to inadvertently, a list of all recommendations made by the company within at least the prior one-year period may be furnished upon request. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities on the list. Any opinions expressed may change as subsequent conditions change. Please do not make any investment decisions based on such information, as it is not advice and is subject to change without notice. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but are not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect the position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

U.S. Sector Trend, Momentum, and Breadth Through October 2022

Our objective is asymmetric risk/reward for asymmetric investment returns; we are unconstrained as to strategy or market.

A skillful trend follower wants to catch a trend early in its stage and capitalize on it until it ends, so if we want to identify them early, we must necessarily focus on short-term trends to see if they can become longer-term trends and asymmetric profits.

With that said, in the month of October 2022, eight of the eleven sectors tracked by S&P sector indices are in the green, and three are in the red.

To read the complete observation, see U.S. Sector Trend, Momentum, and Breadth Through October 2022

The stock market trend is being tested

The stock market is now reaching its first short-term higher probability of a countertrend pullback.

The S&P 500 stock index tapped its 200-day average and reached a short-term overbought level based on relative strength and volatility and is now stalling.

The S&P 500 Equal Weight, which gives an equal weighting to all 500 stocks instead of more exposure to the largest companies based on capitalization, crossed above its 200-day average but was reaching an overbought level at the same time.

So, it’s not surprising to see these market proxies roll over at this level.

Two weeks ago I pointed out in The stock market is at an inflection point the S&P 500 was stalling as if there is resistance at this price level, and there’s a lot of potential supply for those in a loss trap, and it was getting overbought as measured by the relative strength index. The index trended up a few more percent before pulling back today.

I don’t normally trade the S&P 500 index, I just use it as a proxy for the overall stock market.

For portfolio management, I get more granular into the sectors inside, and the stocks.

I also include global markets like commodities, bonds, and other alternatives, to provide a global unconstrained opportunity set to find potentially profitable trends.

Trend systems just want to be fed some trends, so the system can extract the parts it wants from the parts it doesn’t want. It’s best to provide a wide range of uncorrelated price trends for trend systems to create a unique return stream from them.

From the broad index like the S&P 500 it’s useful to look inside to see the percentage of stocks that are trending above their 50-day and 200-day averages to gauge the strength of participation in the uptrend.

The percent of S&P 500 stocks trending above the 50-day average has quickly trended up to the red zone.

The breadth thrusts we’ve seen are typical of a new uptrend — unless* it’s a prolonged bear market. *IF this is the early stage of a prolonged bear market that is likely accompanied by a recession, then we’ll see many swings like this as it unfolds along the way.

However, once most stocks are already in uptrends, the enthusiasm to buy may have run out, so I consider the level above 80% to be a higher risk zone. If we are looking for a lower risk entry, it’s below 30%. A strong breadth thrust like this is bullish when it starts and is typical off the lows after stocks have already trended down as much as they have.

At this point, despite the S&P 500 being down 1.5% today, it appears to be a normal pullback from overbought levels. Our relative strength index signals the index was moving up with such velocity it was a little too far, too fast, which is good in the longer term but increased the odds of a retrench in the short term.

I reduced exposure earlier this week, and the price action next week will determine if we reduce further or buy the dip at lower prices.

In the big picture, we’re strolling into the seasonally weakest month for the stock market after a big rally and no shortage of risks to the short-term uptrend, so it’s essential to determine an exit, hedge, or reduce exposure.

On the positive side, the recent decline in volatility and new uptrends suggest systematic trend-following investment programs could provide inflows of several billion dollars a day in stocks for the next few months if it continues.

While everyone else is trying to figure out what’s going to happen next with inflation, rates, and other global macro issues, we focus on keeping our hard-earned capital invested in the direction of the trend.

If the trends change, so will we.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Managed Portfolios. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as investment advice to buy or sell any security. This information does not suggest in any way that any graph, chart, or formula offered can solely guide an investor as to which securities to buy or sell, or when to buy or sell them. Securities reflected are not intended to represent any client holdings or recommendations made by the firm. In the event any past specific recommendations are referred to inadvertently, a list of all recommendations made by the company within at least the prior one-year period may be furnished upon request. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities on the list. Any opinions expressed may change as subsequent conditions change. Please do not make any investment decisions based on such information, as it is not advice and is subject to change without notice. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but are not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect the position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

The stock market is at an inflection point

The S&P 500 is stalling as if there is resistance at this price level, and there’s a lot of potential supply for those in a loss trap.

It’s also getting overbought as measured by the relative strength index.

The yellow horizontal highlight denotes the price range with the most volume, which you can see in the Volume by Price bars on the right which show the volume at each price level that could be support or resistence.

At the current price level, you can see the yellow highlighted area is the price range of the highest volume of the past three months.

In February, the SPY declined and found support, or buying demand, at this level. Afterward, it trended up before trending down to this level again and once again was met with enough buying enthusiasm to hold it for several days, then the support failed and the S&P 500 Index ETF declined.

At that point, those who bought earlier at higher prices around the price level or higher carried a loss.

In May the stock market trended up against but selling pressure dominated and the index once again trended sideways for several days of indecision before finally breaking down in a waterfall decline for several days.

The stock market finally got oversold again and investor sentiment was extremely bearish, and it’s since climbed a wall or worry.

Now the price has trended up to this price level again that has been both support and resistance in the past three months and it seems to be stalling.

Today started off strong, up 1% or more, only to fade by the end of the day.

The stock market is at an inflection point.

If the stock market gets enough buying demand to keep prices trending up this bear market could be over sooner than later. However, with the Federal Reserve increasing interest rates because the annual inflation rate in the US has accelerated to 9.1% and economic growth is slowing, if the US is in a recession, as noted in “Bear Markets with an Economic Recession Last Longer and are More Severe” bear markets typically last much longer and trend down more.

Investors should be cautious this may not be over yet, and far from it.

We’ll see, and probably sooner than later.

The inflation report this week may be a market mover.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Managed Portfolios. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as investment advice to buy or sell any security. This information does not suggest in any way that any graph, chart, or formula offered can solely guide an investor as to which securities to buy or sell, or when to buy or sell them. Securities reflected are not intended to represent any client holdings or recommendations made by the firm. In the event any past specific recommendations are referred to inadvertently, a list of all recommendations made by the company within at least the prior one-year period may be furnished upon request. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities on the list. Any opinions expressed may change as subsequent conditions change. Please do not make any investment decisions based on such information, as it is not advice and is subject to change without notice. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but are not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect the position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Every new price trend begins with a countertrend

Every new price trend begins with a countertrend, and that’s true for uptrends that roll over into downtrends and downtrends that reverse into uptrends, so trend following starts with a countertrend.

Technology-weighted Nasdaq 100 changed the short-term trend, breaking out above its 50-day average, now in a short-term uptrend.

Past performance is never a guarantee of future performance, but if the Nasdaq uptrend follows through, it’ll need to trend up more than 12% to trade above the longer-term 200-day average.

Nasdaq meets first overhead supply as potential resistant around 13,000.

All the areas above current prices are the hurdle of a trend trying to recover from losses.

Why?

Because many investors and traders may be trapped in losses around those prior lows and highs, the price levels attracted much historical trading.

Many tactical traders mistakenly claim resistance “is” at these levels, but we don’t know if there is resistance to further prices trending up until the price range is reached.

If a price trend reaches a level and reverses back, then we know there was “resistance” to that price level, which means there was selling pressure once the price got to that higher level.

Only time will tell if that is the case here, but we’ll be watching to see if new uptrends are met with selling prior price levels of interest, then we’ll know how much trouble these trends will have trending up into areas investors may have wished they had sold before taking on heavy losses.

To see what I mean, the Nasdaq 100 index was down -33% year to date a few weeks ago, and after a series of higher lows and higher highs (an uptrend) it’s still down -25%.

If you were invested in the Nasdaq type investment this year, or a portfolio of similar stocks, you’ve been in a loss trap.

As prices trend back up, trapped holders may start to tap out, although others may hold on until they get back to breakeven.

This is the kind of price action we’ll observe unfold from here to see which market dynamics are more dominant.

Overhead supply of shares wanting to be sold becoming at least some pressure as resistance is why price trends look so rough and volatile after a downtrend.

At every level the trend reaches, other investors and traders are deciding to buy, hold, or sell.

It’s what makes a market.

For now, we have an uptrend in enough of the high-growth stocks as measured by the Nasdaq 100 index to clear the 50-day average, so no resistance there.

Every new price trends begin with a countertrend and a follow-through.

Let’s see how it goes from here.

Giddy up!

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Managed Portfolios. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as investment advice to buy or sell any security. This information does not suggest in any way that any graph, chart, or formula offered can solely guide an investor as to which securities to buy or sell, or when to buy or sell them. Securities reflected are not intended to represent any client holdings or recommendations made by the firm. In the event any past specific recommendations are referred to inadvertently, a list of all recommendations made by the company within at least the prior one-year period may be furnished upon request. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities on the list. Any opinions expressed may change as subsequent conditions change. Please do not make any investment decisions based on such information, as it is not advice and is subject to change without notice. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but are not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect the position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Inflation is Declining According to this Trend Analysis of Commodities

In economics, inflation is an increase in the prices of goods and services in an economy.

When the general price level rises, each unit of currency buys fewer goods and services; consequently, inflation corresponds to a reduction in the purchasing power of money.

You may not see the value of your money change online like you do with your investment fund values changing daily, but it’s changing.

Inflation is a real risk for everyone, but it’s worse for people who have their money earning a low rate of interest at a bank or another low-yield fixed asset.

If someone believes they are being a “conservative investor” by investing money in an interest-bearing bank account, it’s only because the bank statement doesn’t show the real value of money after inflation.

The latest inflation report shows U.S. Inflation is 9%, three times higher than the long-term average of 3.25%, so if someone is only earning 3% on a CD, the value of their money is 6% less than it was.

That is, they “lost” 6% of buying power.

But that’s not the main point of this observation, it’s just one of many reasons the trend in prices is important.

The US Inflation Rate is the percentage a chosen basket of goods and services purchased in the US increases in price over a year. Inflation is one of the metrics used by the US Federal Reserve to gauge the health of the economy. Since 2012, the Federal Reserve has targeted a 2% inflation rate for the US economy and may make changes to monetary policy if inflation is not within that range. A notable time for inflation was the early 1980’s during the recession. Inflation rates went as high as 14.93%, causing the Federal Reserve led by Paul Volcker to take dramatic actions.

As an investment manager applying trend systems to global markets, I see it much more granular. I’m applying computerized trend systems to a wide range of global currencies, commodities, stocks, and bond markets, so I see the directional trend changes and shifts in momentum. Although I’ve automated the process of monitoring all these global markets, I still like to review the pictures as charts to see what is going on.

I ranked the S&P GSCI Indices by short-term momentum to see which are trending up the most, so we’ll start there.

I think it’s well known that many commodities markets had been trending up this year, but as we’ll see, many of these markets are now in downtrends.

I’ll share these trends in a way that makes it obvious that commodities aren’t just tradable markets, but they impact all of us, and commodities are interconnected. For example, the price of soybeans impacts livestock.

The S&P GSCI Feeder Cattle Index provides investors with a reliable and publicly available benchmark for investment performance in the feeder cattle market. S&P GSCI Feeder Cattle Index is in an uptrend as defined by above the 50 and 200-day moving averages. In fact, in the lower two frames, I include the percent above or below the 50 and 200-day average, and Feeder Cattle is about 5% above its 50-day average and 8% above its 200-day average price.

Feeder Cattle is the strongest uptrend over the past three months. It only gets worse from here.

S&P GSCI All Cattle Index is a broader basket of cattle, and it too is in an uptrend after breaking out of a multi-month base.

Live Cattle represented by S&P GSCI Live Cattle Index looks very similar, and is an uptrend, but not an all-time new high as it’s still below the February high.

Here’s where the weakness in these commodities trends begins. The S&P GSCI Gas Oil Index is in an intermediate-term uptrend; It’s 20% above the 200-day average. But the recent decline pushed it 6% below the 50-day average. The Gas & Oil index is in a primary uptrend, but short-term pullback. Longer-term trends begin with a shorter-term trend, so we’ll see how it trends from here.

Heating oil is represented by the S&P GSCI Heating Oil Index. Like gas and oil, it’s in a primary uptrend, but a short-term downtrend.

Now we’re getting into commodities with a negative price momentum over the past 3 months.

S&P GSCI Sugar Index is in a non-trending, volatile period over the past year, and it’s right at the 50 and 200-day average.

The S&P GSCI Livestock Index, a sub-index of the S&P GSCI, provides investors with a reliable and publicly available benchmark for investment performance in the livestock commodity market. Livestock is another market that’s lost its upward momentum over the past three months, and one to watch for a breakout.

S&P GSCI Natural Gas Index is in a primary uptrend, but recent downtrend in the short term. It tapped its 200-day average and is trending back up, but nearly 7% below where it was three months ago.

I ranked these trends by three-month momentum, so all of the commodities up to this point were outperforming the broad commodity index we know as S&P GSCI Total Return Index. My three-month momentum ranking is completely arbitrary, but it signaled many of these trends had changed recently.

The S&P GSCI Total Return Index is in a primary uptrend as defined by a level above its 200-day average, but it’s in a downtrend since it peaked in June.

S&P GSCI Total Return Index is what many global macro asset managers managing global macro hedge funds use as a benchmark for commodities, so the rest of these trends are more granular looking inside this broader index made up of these other indices.

S&P GSCI Energy Index is in a primary uptrend but has declined materially over the past month.

S&P GSCI Unleaded Gasoline Index is a big one that impacts Americans and our personal economy. S&P GSCI Unleaded Gasoline Index is in a primary uptrend but has corrected a lot these past five weeks. Once again, we see a commodity trend tapping the 200-day moving average, so a breakout below it will signal a changing primary trend.

Coffee is in a downtrend. S&P GSCI Coffee Index is below the 50 and 200 average, signaling it’s in both a short-term and intermediate-term downtrend. This may help explain why Latin American countries like Brazil’s stock index is down, too. Latin America makes a lot of the world’s coffee.

Unless you’re a long/short commodity trader like a CTA trend follower who aims to capitalize on these downtrends as much as the uptrends, this is one of the rare times downtrends are something to cheer on.

S&P GSCI Crude Oil Index is in a short-term downtrend, but a primary uptrend.

Meanwhile, S&P GSCI Cocoa Index is in a downtrend across both time frames.

Hey Crude, as in Brent Crude. We have a downtrend in S&P GSCI Brent Crude Index over the short run after a volatile non-trending period.

An interesting Intermarket analysis this year has been the trend in Gold. Gold is seen by many market participants as a store of value and a safe haven, but S&P GSCI Gold Index is in a downtrend after a sharp uptrend around March. You can probably see how applying multiple time frames can be useful in observing these trends.

By and large, the metals like precision metals are in downtrends.

S&P GSCI Platinum Index is in a downtrend.

Soft commodities, or softs, are commodities such as coffee, cocoa, sugar, corn, wheat, soybean, fruit and livestock. The term generally refers to commodities that are grown, rather than mined. You can see how some of the commodity markets tracked by indices are very granular focused on one single market trend, and others are a basket of commodities within a sector.

S&P GSCI Softs Index has shifted from a quiet uptrend to a volatile downtrend.

A biofuel is any fuel that is derived from biomass, that is, plant or algae material or animal waste.

After an uptrend breakout around March, S&P GSCI Biofuel Index has trended back to the same level it started.

Some of the most common products produced with soybeans are tofu, soy milk, soy sauce, and soy flour. Approximately 85% of soybeans grown around the world are used to make vegetable oils that are either sold to consumers or used commercially according to The Spruce Eats. The USDA says “Just over 70 percent of the soybeans grown in the United States are used for animal feed, with poultry being the number one livestock sector consuming soybeans, followed by hogs, dairy, beef and aquaculture.”

You can probably see how interconnected all this stuff is.

S&P GSCI Soybeans Index is in a downtrend after an uptrend started at the beginning of this year. Hopefully, this lower animal feed cost will help lower the prices of the livestock that are in uptrends.

Lead is still widely used for car batteries, pigments, ammunition, cable sheathing, weights for lifting, weight belts for diving, lead crystal glass, radiation protection and in some solders, according to RSC.org.

S&P GSCI Lead Index is in a downtrend, so I guess we’ll eventually see the price of ammo and car batteries decline, too. Overall, lead has been a non-trending volatile market the past year, but it’s now more decisively in a dowtrend.

Lean Hog is a type of hog (pork) futures contract that can be used to hedge and to speculate on pork prices.

S&P GSCI Lean Hogs Index has trended into a downtrend, so your bacon price may improve.

Palladium is one of a number of metals starting to be used in the fuel cells to power things like cars and buses as well as in jewelry and in dental fillings and crowns.

S&P GSCI Palladium Index is in a downtrend.

Grains are used around the world and are also called cereals, and are the most important staple food. According to NatGeo, humans get an average of 48 percent of their calories, or food energy, from grains. Grains are also used to feed livestock and to manufacture some cooking oils, fuels, cosmetics, and alcohols.

S&P GSCI Grains Index is in a downtrend after it broke up with momentum going into this year. If you like to eat and drink alcohol, this is great news as it seems the prices should drift back to where they were.

Wheat is used for white bread, pastries, pasta, and pizza, so this downtrend in S&P GSCI Wheat Index is a welcome change.

Dr. Copper is market lingo for the base metal that is reputed to have a “Ph. D. in economics” because of its ability to predict turning points in the global economy.

S&P GSCI Copper Index is in a strong downtrend, so if its reputation holds true, the Ph. D. in economics suggests a global economic slowdown is ahead.

The Royal Society of Chemistry says aluminum is used in a huge variety of products including cans, foils, kitchen utensils, window frames, beer kegs and airplane parts.

If the trend in S&P GSCI Aluminum Index is a guide, the price of your next beer keg or airplane should drift lower. Aluminum is in a downtrend.

Industrial Metal alloys are known for their strength, durability, and corrosion resistance, so engineers, architects, and others in the industrial field use these alloys to construct buildings, wires, pipes, bridges, machines, and much more according to Wieland.

S&P GSCI Industrial Metals Index shows industrial metals are in a downtrend with great momentum.

Industrial metals are down so much I’ll show a two-year chart to see the price is back to 2020 levels.

Last but not least is cotton. I think we all know what cotton is used for. The price of clothes should see some decline with S&P GSCI Cotton Index in such a downtrend.

What we’ve observed is many commodity markets were in uptrends, but have more recently trended down. Not all of these necessarily impact the Consumer Price Index, but we certainly use most if not all of them one way or another.

Commodities are real “stuff”, and the prices of much of this stuff are no longer as elevated as it was. If this flows into lowering prices of the stuff we buy, then we’ll see inflation fall from here.

If inflation trends down from here, it’ll be positive for stocks and bonds and may result in the Federal Reserve pausing its aggressive interest rate hikes.

Now you know why we aren’t long commodities at this point.

Investor sentiment (about stocks) is so negative right now, that any slight improvement in inflation may spark an uptrend, then the extremely bearish positioning may drive short covering to keep the trend going a while.

Let’s see how it all unfolds.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Managed Portfolios. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as investment advice to buy or sell any security. This information does not suggest in any way that any graph, chart, or formula offered can solely guide an investor as to which securities to buy or sell, or when to buy or sell them. Securities reflected are not intended to represent any client holdings or recommendations made by the firm. In the event any past specific recommendations are referred to inadvertently, a list of all recommendations made by the company within at least the prior one-year period may be furnished upon request. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities on the list. Any opinions expressed may change as subsequent conditions change. Please do not make any investment decisions based on such information, as it is not advice and is subject to change without notice. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but are not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect the position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Are Growth Sectors Technology, Consumer Cyclicals, and Communication Services more Undervalued than Value?

Growth sectors like technology, consumer cyclical, and communications have seen the brunt of the selling this year, and growth is now more “undervalued” than value sectors per CFRA.

According to CFRA: Stocks are ranked in accordance with the following ranking methodologies. Qualitative STARS recommendations are determined and assigned by equity analysts, with 5 being the highest rating.

But as stated in Fundamental Valuation: Is the Stock Market Cheap or Expensive? undervalued stocks can get much more undervalued (prices fall more) in a recessionary bear market.

Risk management is essential in bear markets.

For example, the S&P 500 is down about -23% so far and needs a 30% gain to get back to the prior high.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Managed Portfolios. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as investment advice to buy or sell any security. This information does not suggest in any way that any graph, chart, or formula offered can solely guide an investor as to which securities to buy or sell, or when to buy or sell them. Securities reflected are not intended to represent any client holdings or recommendations made by the firm. In the event any past specific recommendations are referred to inadvertently, a list of all recommendations made by the company within at least the prior one-year period may be furnished upon request. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities on the list. Any opinions expressed may change as subsequent conditions change. Please do not make any investment decisions based on such information, as it is not advice and is subject to change without notice. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but are not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect the position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Following the Trend of Inflation and Risk of Bonds

In How We’ll Know if a Recession is Imminent I said if the 10-2 Year Treasury Yield Spread crosses below zero, and the yield curve becomes inverted, that’s what will signal a recession is probably imminent, but a recession may not be identified until 6 – 24 months later.

We can’t wait until a recession is called to manage our investment risks; the stock market has historically been the leading indicator, declining well in advance.

After U. S. inflation was reported today that inflation accelerated last month to a 7.5% annual rate to a 40-year high, U.S. Treasury Yields trended up to 2%.

Since the 10-2 Year Treasury Yield Spread is the difference between the 2 year U. S. Treasury and the 10 year U. S. Treasury, the spread will tighten as the shorter-term interest rate converges with the longer-term rate.

Recently both yields have been increasing, but the 10-2 Year Treasury Yield Spread is still falling.

The U.S. inflation momentum is driven by rising price trends for autos, household furniture, appliances, as well as for other long-lasting goods we buy.

For example, here is the U. S. Consumer Price Index for used cars and trucks.

It is well known certain consumer prices have been trending up since the pandemic, so the question for the second-level thinker is whether or not these rising inflation trends are already reflected in the prices of stocks and bonds.

So far this year, 2022 has started off with stock markets trending down.

For example, the S&P 500 declined nearly -10% in the few weeks before retracing about half the loss over the past two weeks.

Longer downtrends often retrace about half of their decline before turning down again, so we’ll soon see if this is the early stage of a deeper decline for stocks or a continuation of the primary uptrend.

The Nasdaq 100, which is weighted heavier in large-cap growth stocks and the technology sector, has reacted to more selling pressure down -14% before retracing some of the decline.

Emerging country stocks as measured by the MSCI Emerging Markets Index have finally shown some relative strength against U. S. stocks.

The MSCI Emerging Markets Index trended up at first, then only declined about -3%, and is now positive YTD.

Rising interest rates have a direct negative impact on bond prices, and that is especially true for longer-term bonds.

For example, the ICE U.S. Treasury 20+ Year Bond Index shows the bond price is down over -6% already in 2022.

If you buy and hold bonds, you’re going to learn the risks of bonds and bond funds in a rising rate regime.

Many investors today haven’t invested long enough to have experienced the possible losses that can be driven by this kind of rising inflation, rising interest rates, regime.

Investing involves risks you must be willing to bear, and if you aren’t willing and able to take the risk, you may consider reducing or hedging your risks.

For information about our proactive investment management, active risk management, hedging your risks, and ASYMMETRY® Managed Portfolios, contact us.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Managed Portfolios. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Please do not make any investment decisions based on such information, as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but are not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Breadth of the Stock Market Indicates Internal Weakness and a Stealth Bear Market

I focus most of my attention on my own positions or those on my lists for portfolio management.

Nothing is more telling than what the stocks on my lists that meet certain fundamental earnings growth and technical criteria are doing.

Nothing is more important than the trend, momentum, and volatility of our actual positions.

However, it doesn’t mean we don’t also observe all the other stocks, bonds, commodities, and currencies for signs of strength or weakness.

Even though it may not impact my exposures or drive any change in our positions, I still enjoy taking the time to see what “the market” is doing, overall, in the big picture. That’s what I mostly share here, for informational purposes only.

Below is a chart of the percent of U. S. stocks trending about the 50-day moving average, an intermediate-term trend signal.

A few observations of asymmetry are:

- Only 30% of stocks are trending above the 50 day moving average.

- As we can see in the charge giong back 20 years, its at the low end of its historical range.

- In signficant stock market declines, it gets much worse. For example, in March 2020, more than 90% of stocks were in downtrends, the worst in two decades, including 2008.

- About 8 times this Market Breadth indicator stopped at this level before trending back up, as stocks trended back up.

- About 13 times this Market Breadth indicator didn’t stop here at this level, but instead kept trending loweer as stocks trended lower.

Overall, my observation from this asymmetry (imbalance) is many stocks have already entered downtrends.

Overall, stock market participation started showing weakness after the May 2020 advance, then improved into late 2010 before reaching a peak, and it’s been trending down since.

We may start to hear some call it a “Stealth Bear Market,” a phrase used to describe stock market conditions when the overall indexes are by and large trending higher, but many stocks are trending lower.

A “Stealth Bear Market” may define a trend like this because the S&P 500 stock index has been trending up, as the percent of stocks participating in the uptrend has declined.

Regardless of what we call it, the bottom line is most stocks are already in downtrends, so we’ve been stalking to see when they start trending back up again.

I think it’s essential to actively manage risk and adapt to changing market trends. If you need help, contact us. We manage accounts titled in your own name at an independent custodian of Goldman Sachs.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information, as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but are not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

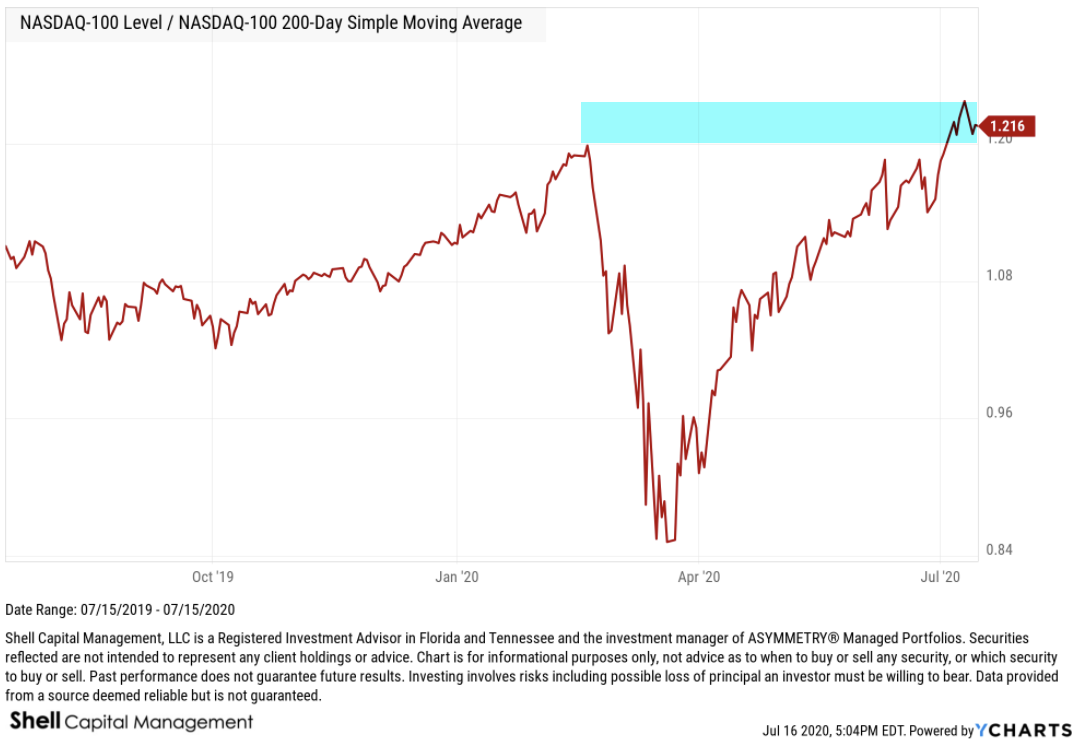

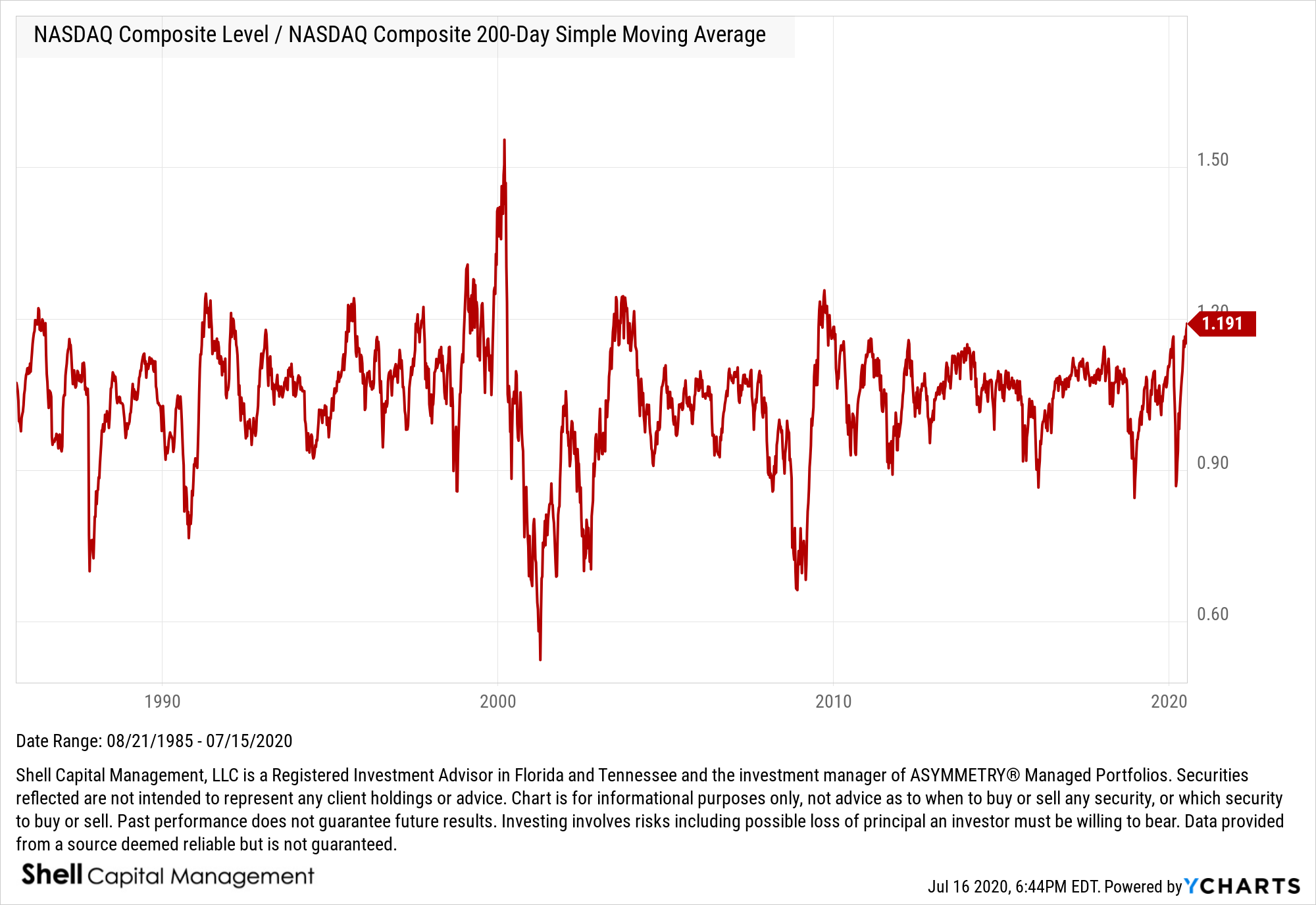

A lot of talk about the NASDAQ being 21% above its 200 day moving average

There’s a lot of talk about the NASDAQ being 21% above its 200 day moving average, so… here’s my 2 cents on the matter.

Yes indeed, the NASDAQ is over 21% above its 200 day moving average. So, if the 200 SMA is your exit, you’d endure a 21% drawdown waiting to sell. I’ve got a ratio chart for it, too. The 1.216 = 21.6% variation. Also note, it’s higher than it was in February.

At a ratio of 1.20 it was high in February, since 1.20 = the level of the NASDAQ was 20% higher than its own 200 day SMA. How high is that?

It’s a decade high!

So, yeah, the NASDAQ seems stretched…

Like the CBOE Put/Call Ratio I shared in Here’s what the equity options put call ratio is telling us, and what it isn’t, the % above a moving average is another indication of sentiment.

When it’s as high as it is now, the market very enthusiastic.

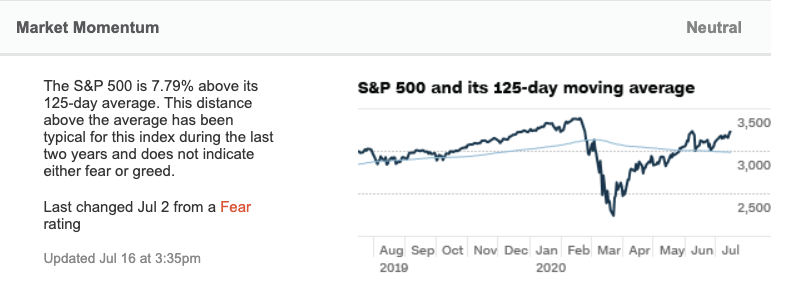

For example, the Fear & Greed Index calls it market momentum and uses the 125 on the S&P 500 as a measure of investor sentiment.

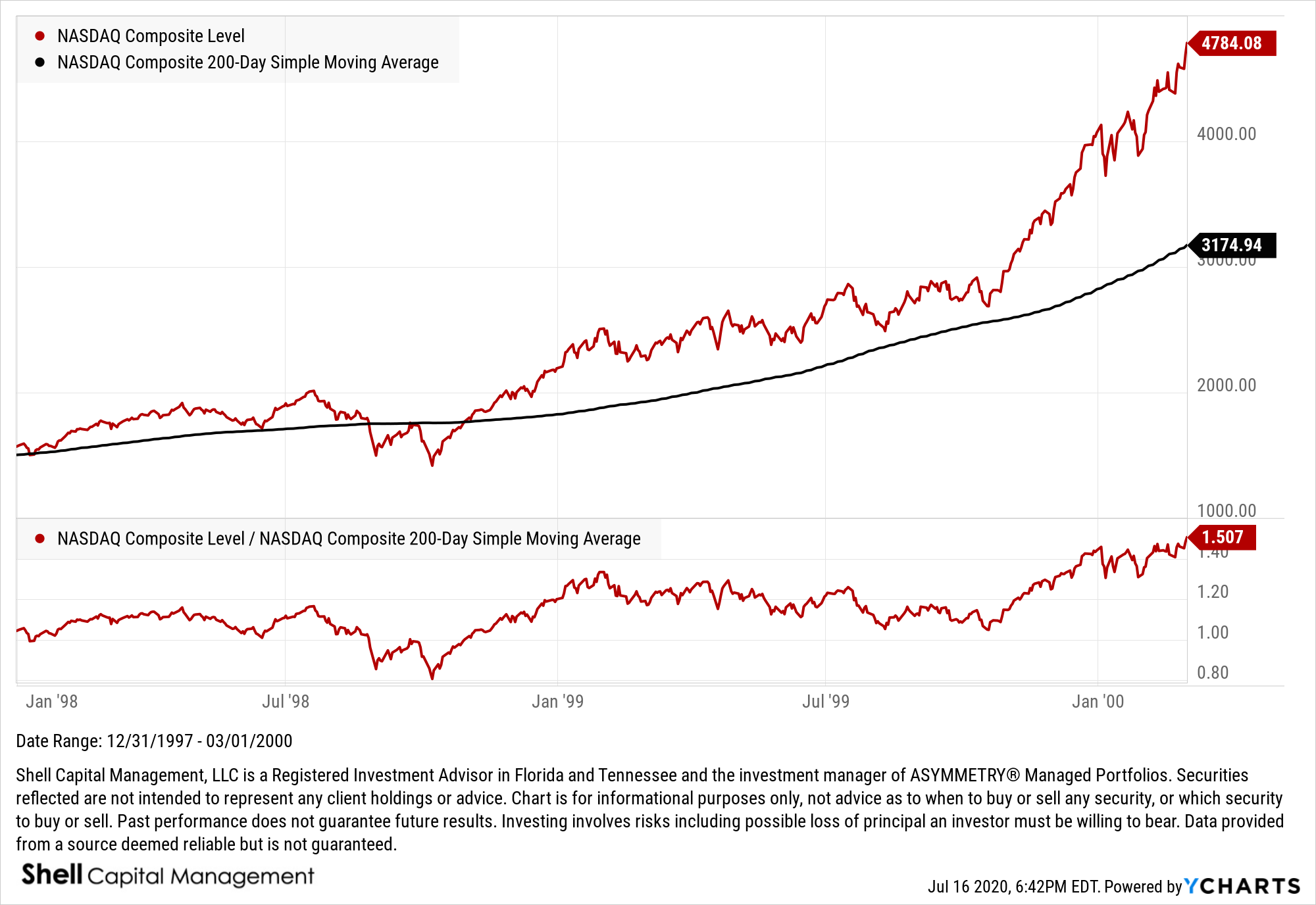

Chatting with some friends on Twitter, someone asked about the relative comparison to the 2000 stock market bubble.

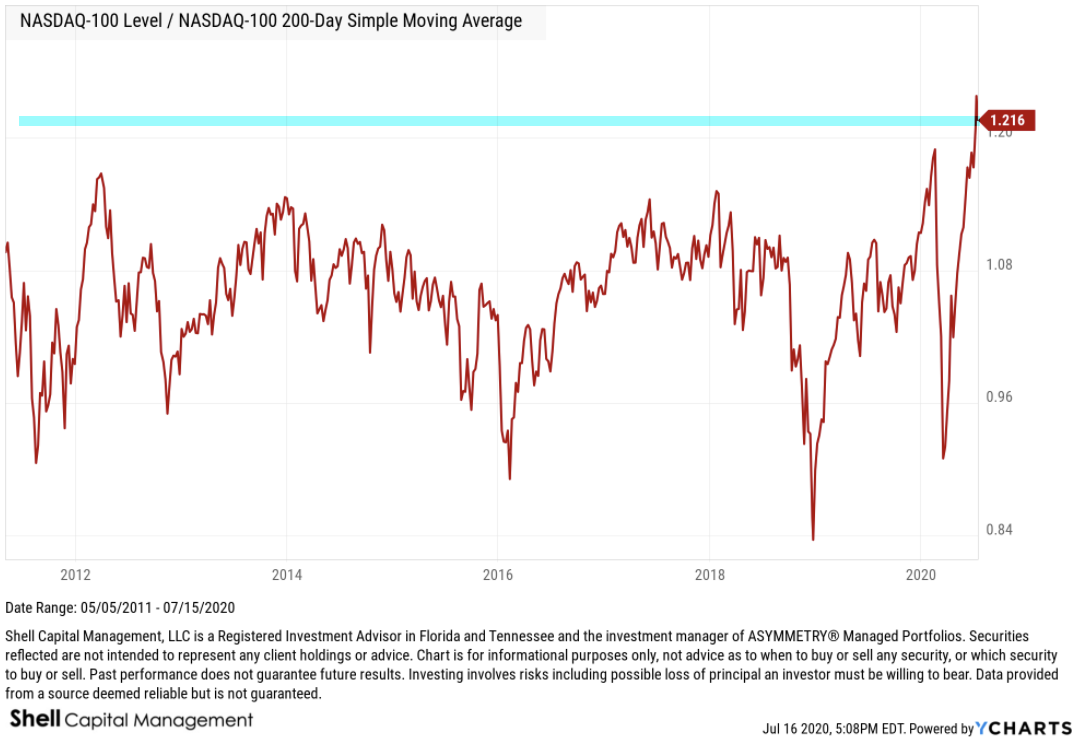

The current period is no comparison to 1999-2000 when the NASDAQ was 50% above its 200 day SMA.

Here is the ratio between the NASDAQ and its own 200-day moving average back to 1985. The relative ratio level the NASDAQ got in 1999 was the highest ever seen.

Interestingly, I first started observing to get trading signals from relative strength ratio charts in the late 90s, and by the time 1999-2000 rolled around, I was comparing not only stocks to other stocks and their sector index, but also a cross section of global markets. For example, stocks vs. bonds, etc.

The NASDAQ was all the craze around 1999, and I had a t-shirt that said “NASDAQ; the world puts its stock in us.”

With technology leading with momentum, the tech heavy nas is seeing some popularity again.

Don’t miss out, get the email:

Join 520 other subscribers

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Should we care the S&P 500 closed above its 200-day simple moving average?

As the U.S. unemployment rate in April 2020 was 14.7%, the highest since the Great Depression, the U.S. stock market is trending up.

And May’s unemployment number may be higher when it’s announced on June 5.

The stock market is said to be a discounting mechanism. The largest stock market investors who drive price trends don’t look back, they look forward.

It’s an auction market and operates on the proposition that investors and traders gaze into the future and discounts all known information about the present moment and expectations for what’s expected to happen next. So, when unexpected events happen, the market takes into account this new information very rapidly.

It certainly seems to be happening now.

Either the market is factoring in a quick recovery, or something else is driving it up.

The Efficient Markets Hypothesis (EMH) is based on the theory that the stock market is a very efficient discounting system, so it factors in expectations of the future. The Efficient Markets Hypothesis suggests the stock market generally moves in the same direction as the economy.

Yeah, I know. If there ever was a time that sounds silly it’s now. Well, and every other market crash and bubble. I’ve seen my fair share of those in the past two decades.

One of the most interesting paradoxes in investment management is the market discounts everything is also the first premise of Technical Analysis.

The three premises on which the technical approach is based:

- Market action discounts everything.

- Prices move in trends.

- History repeats itself.

That both the Efficient Markets Hypothesis and Technical Analysis is based on the belief the market discounts everything known and expected about the future is logically self-contradictory, because EMH doesn’t believe prices move in trends. EMH certainly doesn’t believe Technical Analysis, including trend identification systems for trend following and pattern recognition, is useful. Yet, trend systems and pattern recognition are some of the very strategies that I’ve seen to achieve asymmetric risk-reward.

I consider most trend identification systems to be pattern recognition. Pattern recognition is the systematic recognition of patterns in data. For example, the first action in trading breakouts is to identify current price trend patterns along with potential support and resistance levels in order to signal entry and exit points.

So, here we are. The S&P 500 is now trading above its 200 day moving average again after trending below it on February 27th.

It has been shocking to most that the stock index is now only down about -10% from its February high after a -36% waterfall decline over just 23 trading sessions.

It the fastest waterfall we’ve seen of this magnitude, so maybe we shouldn’t be surprised to see it swing back up to recover 2/3rds of the decline.

But no, it’s not a surprise. I tactically traded through the last two most radical bear markets since the Great Depression and they both included many swings up and down along the way.

The swings are the danger.

If you wait too long and enter after prices have already trended up sharply, you may get invested in stocks just in time for the next trend down.

The same goes for the downside. If you wait until your losses are so large they become intolerable and tap out at the lows, you risk missing out on the price trend recovery like we just saw.

At what point do you feel good about geting back in?

After prices have trended back up as they have now? The S&P 500 is above the 200 day moving average, so it’s a sign of an uptrend.

Is this the time to buy?

Or, do you feel better about investing in stocks after the price trend falls more?

What if it doesn’t?

These are tactical trading decisions. Most investors are not good at it, but some of us are better.

The market is people who trade and invest in the market. People are always looking forward, gazing into the future that doesn’t yet exist, so prices are always adjusting according to people’s beliefs about what’s going to happen next. This includes all signals. All signals are necessarily predictions of the future.

As the SPX is now trending above its 200-day average, trend followers who use the SMA will buy here. We may indeed see some buying interest come in because of it. Only time will tell if its enough buying pressure to drive prices up more. I’ve been operating trend systems for decision-making for over two decades and I don’t know of any money manager who actually trades off a 200-day moving average signal, except one. I’m going to save it for another observation, but until then, I’ll simply share this.

The S&P Trend Allocator Index is designed to track the performance of a systematic trend-following strategy allocating between the S&P 500 and cash, based on price trends. If the S&P 500 is observed to be in a positive trend, then the index is allocated to the S&P 500, otherwise, it is allocated to cash.

Here is the S&P Trend Allocator Index relative to the S&P 500 stock index which is fully invested, all the time.

Oops.

Prior to the waterfall decline, the S&P 500 was trending 11% higher than its 200 day moving average. So, it was going to have at least a -11% drawdown with perfect execution. That’s a nice thing about it. It’s a predefined exit, so at the February high, you knew if the stock market falls, you’ll lose at least -11% before you exit. When we know our defined risk, we can decide to accept it, or not. If you were trading off the 200 SMA and believed a -11% drawdown was unacceptable, you could have raised your stop above it.

But then, if you sold earlier, how would you know when to get back in?

Ok, I just wanted to drive home the point: tactical trading decisions aren’t easy. No indicator works perfectly.

I don’t use the 200 SMA, but the S&P Trend Allocator index does. However, you may notice it didn’t sell at the price trend break below the 200 SMA. Instead, it sold later, and down much more. The S&P Trend Allocator Index sold later because it waits until five days after a crossover to sell. I marked on the chart the point on the price trend it actually sold.

S&P Trend Allocator Index Construction

“At the close of each business day, a trend signal is calculated based on the closing value of the S&P 500 Total Return Index (the “Allocation Indicator Index”) compared to its prior 200-day Simple Moving Average (SMA). The SMA is defined as the average of the last 200 closing values of the S&P 500 Total Return index. The trend signal is positive if the last five consecutive closing values of the S&P 500 Total Return index are equal to or greater than the SMA. The trend is negative if the last five consecutive closing index values are below the SMA. The trend signal does not change from its current status until there have been five consecutive days of index values indicating a signal change.”

I’m not going to get any deeper on this right now, but I will in a later observation, but the drawdown in the S&P Trend Allocator Index was about -27%.

Keep in mind; an index does not include any transaction cost or fees and may not be invested indirectly. If we were applying this trend following method with real money, there would have been transition costs, fund fees, advisory fees, and slippage to account for which would have negatively impacted the return profile. With that said…

Should we care that the S&P 500 is above its 200-day simple moving average?

Since the index was operated in real-time, above is the total return relative to its S&P 500 stock index which is fully invested in stocks all the time.

Here is the drawdowns for a complete picture of its risk-reward profile.

As you see, the S&P Trend Allocator applying the 200-day moving average to the S&P 500 had a drawdown of -27% vs. the -34% drawdown of the S&P 500.

So, the risk management method of the S&P Trend Allocator provided a drawdown control edge of about 7% relative to the fully invested stock index that is exposed to the risk and reward of the stocks all the time.

However, the total return is materially less at this point. Although the S&P Trend Allocator 200 day SMA exit signal exits with a lag and then reenters with a lag, it has participated in most of the stock market drawdowns and then misses out on the early part of its gains off the lows when the rate of change is highest.

It will take a larger downtrend for the 200 day SMA to show its value. The magnitude of the March decline was tremendous, but it happened so fast the lag was exposed as a risk to the strategy.

Now, just imagine how the risk/reward profile will be impacted if it enters the stock market right now, and then the market trends down again. This is one of the risks to be aware of with any trend-following or tactical trading system or method.

No investment strategy is ever perfect, but we gain an edge when we are aware of their weaknesses. I have spent more time trying to break my systems and methods to discover weaknesses than I did creating them.

Join 520 other subscribers

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Panic selling drove a waterfall decline and washout for the stock market

Growing up in East Tennessee and the Great Smoky Mountains, I observed a lot of waterfalls.

Wiki says a fall of water is an area where water flows over a vertical drop or a series of steep declines in the course of a stream or river.

According to National Geographic, a waterfall is a river or other body of water’s steep fall over a rocky ledge into a plunge pool below. Waterfalls are also called cascades. The process of erosion, the wearing away of earth, plays an essential part in the formation of waterfalls.

What we have witnessed in the global equity markets is a waterfall decline, the question now is if the plunge pool has developed.

An overhang in a waterfall can sometimes protrude out enough to form a base, or even drive the water to flow upward for a while, but the waterfall isn’t over until the plunge pool develops.

An overhang in a waterfall can sometimes protrude out enough to form a base, or even drive the water to flow upward for a while, but the waterfall isn’t over until the plunge pool develops.

Using the S&P 500 stock index as a proxy, it’s pretty clear there wasn’t much of an overhang along the way. For example, in the middle of this 3-year chart, we see how the decline in late 2018 played out. It had a lot of overhangs as the stock market was swinging up and down for several weeks. Now, compare that to this time…

What we have here is panic selling.

Investors tend to underreact and overreact to new information.

Underreaction: Trends begin to drift in a direction as people initially underreact to change, so the price trend unfolds gradually.

Overreaction: Sometimes, investors overreact to new information, so the price is driven too far, too fast. When the market overreacts, prices overshoot too high, or too low.

At the bottom of a waterfall is a plunge pool, where the water settles. What does the plunge pool look like as it develops? It’s a floor that has enough support the water stays were it is.

The trouble is, in the market, we don’t physically see the rock bottom. Unlike in physical science, an exchange market is a social science because it’s human behavior. Don’t think this is humans? Maybe it’s the computer algorithms? They are created and operated by humans.

I apply quantitative tools to get a read on how extreme investor sentiment is.

In analyzing market trends and price action, we can see what is going on with market internals, such as breadth. The NYSE Bullish Percent was developed by Abe Cohen was the first breadth indicator. Abe Cohen was an early pioneer of Point & Figure charting and created the NYSE BP in the mid-1950s. The NYSE Bullish Percent is a market risk barometer that measures the percent of stocks listed on the New York Stock Exchange that have a Point & Figure buy signal, so they making higher highs, so they are in uptrends. The NYSE Bullish Percent is washed out. It hasn’t been this low since the waterfall decline in October 2008.

The challenge with countertrends is they can also trend farther than you would ever believe is possible. It’s because markets don’t follow a normal distribution. Instead, market trends have fat tails, meaning some gains and losses exceed an otherwise normal distribution, as we see in physical science. As such, the overreactions can overshoot and just keep overshooting. We never know for sure when a trend has stopped. What we can do, however, is apply quantitative tools to gauge and guide. I use these as a guide and barometer for overall market risk.

The percent of the S&P 500 stocks above the 50-day moving average is washed out to 1%. In fact, only 7 of the 505 stocks in the S&P 500 are in a short term uptrend. While in a big bear market such as 2008-09, these conditions can continue for a long time, historically, this lower level of risk eventually offers the potential for asymmetric risk/reward. That is, the possibility for reward is greater than the risk it takes the achieve it. Or, the magnitude for a reward is greater than the downside risk, which can be predetermined with options or an exit (i.e., stop-loss.)

A material change that has occurred the past week is the percent of S&P 500 stocks above their 200 day moving average, or longer-term uptrends have washed out. Only 5% of the stocks are in uptrends now, so 95% of them are in long term downtrends. That doesn’t sound good, but when it reaches an extreme, it suggests to me the selling pressure is intense and could eventually dry up.

This is about as oversold the stock market gets, both internally looking at the individual stocks and the indexes. Sure, it can get more oversold and stay there for as long as sellers have the desire to sell, but it has reached the point the odds of a short term reversal is increasing the lower it goes.

Yesterday I asked: where do you think we are in the cycle of market emotions?

Clearly, when stock indexes drop 8-10% in a single day after already well off their highs, it is driven by emotional panic.

The US Investor Sentiment poll from AAII is released on a few day’s time lag, but Bearish % of those polled is another measure up to 2008-09 levels.

To no surprise, the Fear & Greed Index was penned all the way back to 1 after yesterday’s close.

What we have here is a washout. A washout is an event or period that is spoiled by constant or heavy rain. We may see more rain, but it’s a washout nonetheless. A washout in the stock market is when prices have been flooding down so hard, so broad, it seems like a washout of rain.

As you can imagine, with a waterfall, heavy rains increase the volume and speed of water flow. A washout pushes the river to its limits.

The desire to sell has been overwhelming any buying interest that remains for a few weeks now. This has been the fastest decline in US stock market history. I guess we shouldn’t be so surprised if we believe a trend stretched far in one direction is more prone to snap back harder and faster. That’s what we’ve seen here.

This is the end of the longest bear market in US history, and it has indeed ended with a bang. That also means this is the beginning of a bear market. What we don’t know in advance is how long it will last or how low it will go. If we knew it would be -50%, we could simply sell short and profit from the fall. If we knew this was “the bottom,” we could use leverage to maximize gains on the upside. But, none of us know the outcome in advance, not the biggest banks, not the largest asset managers, and neither you nor I. The edge I do have is accepting this reality and embracing it to the point I drove me to create risk management systems to limit the downside when I’m wrong and focus on the things I can control. I’ve operated tactically through periods like this many times before in the last two decades, so I’ll just do what I do, which means I’ll execute many entries and exits until we find the trend. In conditions like we’ve seen this year, they’ll be countertrends. Once trends do develop, they’ll be trend following.

What I’ve typically seen in past bear markets is many cycles up and down along the way. That isn’t what we’ve seen this time, so far. This reminds me more of September 11, 2001, after the World Trade Center was attacked. The difference is, the S&P 500 was already down about -17%, and since the planes hit the World Trade Center in New York, the NYSE was closed. The New York Stock Exchange remained closed until the following Monday. This was the third time in history that the NYSE experienced prolonged closure, the first time being in the early months of World War I[2][3] and the second being March 1933 during the Great Depression.

It may not play out this way this time, but countertrends should be expected. Here is what the stock market did after the exchange opened after September 11. The SPX dropped -12% quickly, but then investors become patriotic, and it recovered a few weeks later. Of course, this happened inside a bear market that started in 2000 and didn’t end until 2003.

Is this so different than 9/11? Of course, it is. Every new moment is always different. But, we’ve experienced these things before. I was much more of a rookie 20 years ago when I walked into my investment firm office to see the planes hit. It was an incredibly emotional and panicked time in American history. At the time, it wasn’t just the one attack, we wondered what would be next. It was the Pentagon, and another plane was hijacked. We didn’t know what to expect, it was uncertain. When would we be attacked again? Where? Would it wipe us out?

We didn’t know.

Portfolio managers and tactical traders must be here, now, in the present moment, not dwelling on the recent past, there will be time for that later when things are calm and quiet. But even then, we can’t do anything in the past, we can only do it now.

I hope this helps.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor in Florida, Tennessee, and Texas. Shell Capital is focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. I observe the charts and graphs to visually see what is going on with price trends and volatility, it is not intended to be used in making any determination as to when to buy or sell any security, or which security to buy or sell. Instead, these are observations of the data as a visual representation of what is going on with the trend and its volatility for situational awareness. I do not necessarily make any buy or sell decisions based on it. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Employment, Coronavirus, it’s just the market, doing what it does…

It seems most people probably believe the news drives the stock market.

I can see why, since the news headlines want to tell a story.

We like a great story. We want to hear the narrative. We definitely want to believe we know the causation of things going on around us.

Do you believe the news drives stock price trends?

“Coronavirus Live Updates: Trump Praises China’s Response to Outbreak as Death Toll Passes 600“ – New York Times

The Coronavirus outbreak in Wuhan China has grown exponentially as asymmetric uncertainties usually do. According to Worldometer, there are now 31,535 of which 4,826 (15%) in critical condition 638 deaths and 1,778 have recovered.

The Coronavirus outbreak only started less than a month ago, but its rate is exponential.

This is not the kind of asymmetry we want to observe. I hope a cure is found soon to save these human lives.

How has the stock market reacted?

The S&P 500 gained over 3% the past 5 days anyway…

It’s just the market… doing what it does…

This morning, in the U.S. we get great news on employment data.

The US Unemployment Rate measures the percentage of total employees in the United States that are a part of the labor force but are without a job. It’s one of the most widely followed indicators of the health of the US labor market and the US economy as a whole. Historically, the US Unemployment Rate reached as high as 10.80% in 1982 during a notable recessionary period.

The low Unemployment Rate has been a bright spot for the U.S. economy since unemployment trended up sharply in 2008 and peaked at 10.10% in November 2009, the highest level since ’82. A picture is worth a thousand words, so here the trend. from January 2007 to November 2009 as Unemployment Rate increased sharply from 4.4% to 10.10% in about two years.

Looking at the US Unemployment Rate in the bigger picture, below are the trends and cycles going back over sixty years. US Unemployment Rate is at 3.60%, compared to 3.50% last month and 4.00% last year. This is lower than the long term average of 5.73%. The last recession was the second-highest unemployment and it has recovered even smoother than before.

The headlines today:

“January adds a much stronger-than-expected 225,000 jobs, with a boost from warm weather” – CNBC

The stock indexes are down over -0.50% anyway…

I say: It’s just the market, doing what it does…

I believe investors underreact and overreact to new information “news.”

An overreaction is when price trends become overbought or oversold driven by psychological and investor sentiment reasons rather than fundamentals. It’s why we see crashes and bubbles, over short term and long term periods.

An underreaction is when investors initially underreact to new information such as earnings announcements, which leads to a predictable price drift. In other words, underreaction drives price trends!

Prices drift up or down over time when investors underreact to information.

Prices overshoot, trade up or down too far, too fast, when investors overreact to information.

This why my focus is on the direction of price trends, along with volatility, investor sentiment, and multiple time frame momentum.

My directional trend following systems are designed to catch the trends that drift from underreaction.

My countertrend systems signaled by momentum, extreme investor sentiment, and volatility analysis, are engineered to capitalize on overreactions.