The popular U. S. stock indexes closed in the red for the year Monday, erasing their big starting gains in January. As I mentioned many times; quick gains can be lost even faster. The financial news has mostly been quoting the Dow Jones Industrial Average because it had gained the most year-to-date. It had gained over 7% in January, but lost that gain, and then some, in two days. After just a few days, the Dow Jones dropped -14% in the futures market and -8% on a closing basis. That was enough to wipe out recent gains and mark the index down nearly -2% for the year.

I discussed the market risk in our portfolio commentary for our investment management clients, and we were positioned for it. I also explained it in In remembrance of euphoria: Whatever happened to Stuart and Mr. P? and In the final stages of a bull market. So, it should have been no surprise.

But, when I looked at the asset class performance table, I saw some interesting divergence. Large Cap Growth is still outperforming Small Value. As most of the U.S. equity asset classes were in the red, Large Growth remained positive on the year. I thought I would share a look as to why.

I am a tactical portfolio manager, so my focus is on finding trends and shifting to the trends I want and avoiding those I don’t. That’s a lot different than “asset allocation.” Financial advisors who create asset allocation models for their investment clients normally allocate into funds in the asset class style box. This is also typical with 401(k) plans. They offer funds that provide broad exposure to an asset class style box, rather than the individual stock market sectors I prefer to focus on. So, we often hear style box asset classes quoted like “Large Growth is beating Small Value” or “Large Caps ard leading Small Caps.”

According to Morningstar:

The Morningstar Style Box is a nine-square grid that provides a graphical representation of the “investment style” of stocks and mutual funds. For stocks and stock funds, it classifies securities according to market capitalization (the vertical axis) and growth and value factors (the horizontal axis).

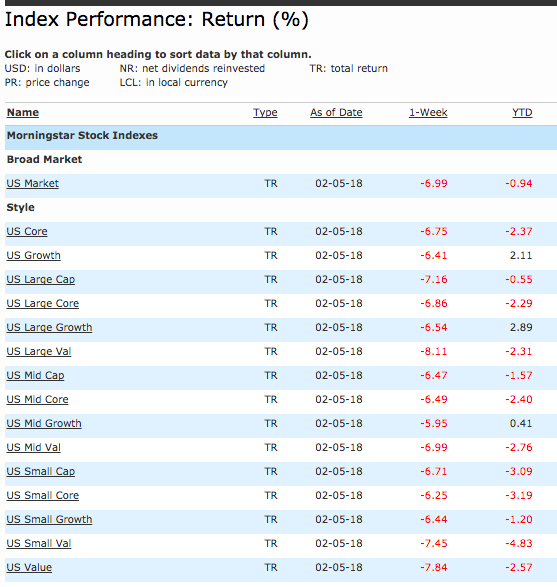

Below is a recent performance for the equity markets. As you see, U.S. Large Growth was leading with a 2.89% gain year-to-date, Small Value was down -4.83%. When we observe such a divergence, it makes us curious what is causing it.

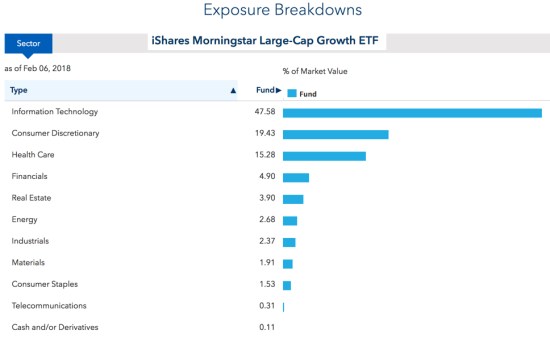

To understand what is driving the return, we take a look inside to see “what is different.” Below is the sector exposure breakdown of Large-Cap Growth. We can understand the sector exposure of the iShares Morningstar Large-Cap Growth ETF. Clearly, the big standout is heavy exposure to Information Technology. The other two larger exposures are Consumer Discretionary and Health Care.

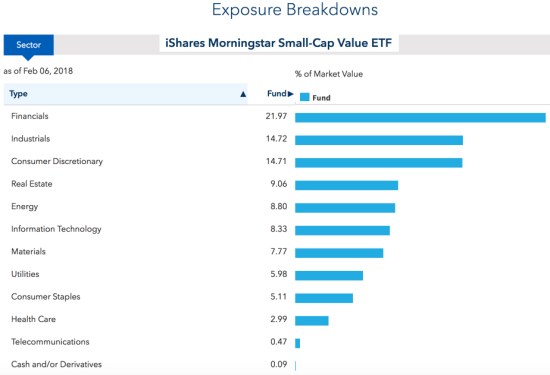

Next, we observe the sector exposure of the Small Value asset class. We can see the sector exposure in the holdings of iShares Morningstar Small-Cap Value ETF.

The Small Value index has 22% exposure to Financials since many financial sector stocks are smaller companies. The other top sector exposures are Industrials, Consumer Discretionary, Real Estate, and Energy.

What is different?

Clearly, the single largest difference is that Large Growth is very heavily exposed to the trend in Technology sector. Technology is 50% of Large Growth while it’s only 8% of Small Value. On the other hand, Financials is only 5% of Large Growth but its the largest exposure in Small Value at 22% of the index.

Stock market asset class returns are driven by their sector exposure. Recently, the Tech sector has been one of the mightiest trends, so it’s helped Large Growth also appear more dominant over equity styles that hold less of it. I would preferably look inside and find out what return driver is causing the difference, then get exposure to that trend in momentum.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

You can follow ASYMMETRY® Observations by click on on “Get Updates by Email” on the top right or follow us on Twitter.

Investment results are probabilistic, never a sure thing. Past performance is no guarantee of future results.

You must be logged in to post a comment.