I have long said that many indexes are a black box. If we don’t know what will be added or deleted from the index in advance, the rules driving the changes must be a black box. I especially believe the Dow Jones Industrial Average is a Black Box.

I’ve also said most of the indexes are simply systematic investment strategies that apply some rules-based strategy and most of them are quantitative. That isn’t the case with all indices, however, since some of the additions and deletions (buys and sells) in the index are decided by a committee. However, even the committee uses some quantitative rules-based method to some degree.

But, it’s still people, making decisions, deciding which stocks to add or remove. As such, there is both a degree of quantitative rules-based system and some elements of discretionary decision-making. To be sure, read their notices of index changes.

S&P Dow Jones Indices recently announced their quarterly rebalance for S&P and Dow Jones equity indices scheduled to take effect prior to the open Monday, March 23, 2020, are being postponed.

Specifically, they said:

S&P DJI made this decision following thorough consideration of how best to support our clients and govern our indices during this period of extreme global market volatility, market-wide circuit breaker events and exchange closures.

Below is a summary of the changes that will impact certain indices.

-

The majority of quarterly shares outstanding and investable weight factor (IWF) updates are postponed.

-

Membership changes (i.e., adds/drops) for select indices will be postponed.

-

Capping constraints that enable consistency with certain diversification requirements will be applied by the end of March.

This is an example of what I call Man + Machine. As most of the S&P Dow Jones Indices is systematic, applying a rules-based strategy for adding and deleting stocks in the index much like the manager of a fund does, this action is the result of the discretionary overlay of people making active decisions.

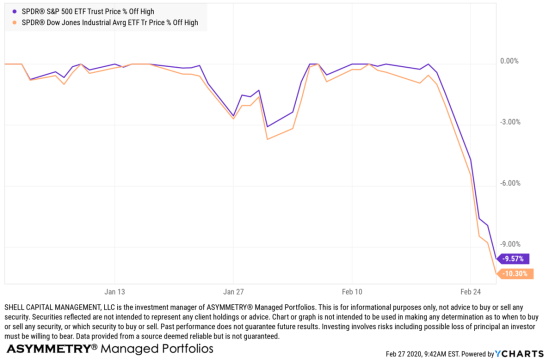

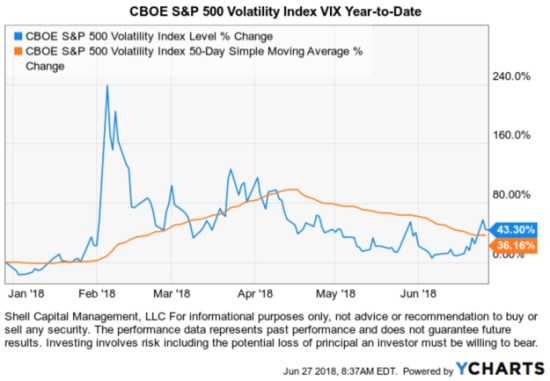

The recent volatility across global markets is one of the most extreme volatility expansions we’ve ever seen before as prices are spreading out everywhere. No index company is more known than S&P Dow Jones Indices, and even they have made a big discretionary active decision in response to changing market conditions.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor in Florida, Tennessee, and Texas. Shell Capital is focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. I observe the charts and graphs to visually see what is going on with price trends and volatility, it is not intended to be used in making any determination as to when to buy or sell any security, or which security to buy or sell. Instead, these are observations of the data as a visual representation of what is going on with the trend and its volatility for situational awareness. I do not necessarily make any buy or sell decisions based on it. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.