In the final stages of a bull market, we normally see a parabolic move to the upside, a final blowoff that gets in the last investors. Buying demand is the response of investor euphoria like I pointed out last week.

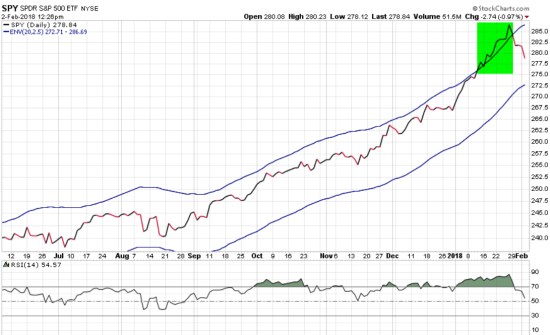

An indication of a parabolic move is seen in price channels and confirmed with momentum oscillators. Only time will tell if this is it, but in the chart, I highlight the S&P 500 stock index broke out above an upper moving average channel.

Price trends usually peak with volatile swings up and down before a larger leg down. Some swing tighter than others, but there is normally a period of “indecision” that precedes an intermediate trend change or drawdown. A drawdown is a decline in the value of an investment or market below its all-time high. Below is the period leading up to the -15% drawdown in the stock index late 2015 – 2016. In the green box, I show the price trend entered a period of swings up and down before breaking an upward trend, drifting more sideways, then a-15% decline.

Next is the swings in the S&P 500 entered into what became a -18% decline in 2011. My point here is that larger legs down don’t necessarily happen all at once, there are indecisive swings that eventually fall apart.

The top in 2007 presented much larger swings and of course ended up declining -56% over nearly two years afterward. I believe these swings up and down before a larger trend unfolds is indecision among traders and investors. Again, my point here is that larger legs down don’t necessarily happen all at once, we instead observe indecisive swings that eventually fall apart.

Lastly, here is the 1999 – 2000 peak that also presented wings like the previous peaks. The stock market trend broke above a simple channel a few times before entering a -50% bear market.

The current trend just recently stretched above the channel and at the same time, was very overbought for months as measured by the momentum oscillators. This happened at the same time bullish investor sentiment measures was reaching record highs and volatility at historical lows. However, as seen in observations above, the U.S. stock market could just now be entering into a phase of swings up and down that could last for months or years, or it could fall apart sooner. Either way, I make this point for situational awareness.

As a portfolio manager, I don’t need to know for sure what’s going to happen next. I just know what I’ll do next as trends unfold.

Only time will tell if this is the early stages of an end of an aged bull market or just an interruption of a euphoric “melt up”. We don’t need to know when a major top is in. It doesn’t require an ON/OFF switch. When a big bear market does come, it will be made up of many swings up and down along the way over many months. People will crave to be in, out, in out, in, out, as it all unfolds. Adaptability is essential: the consistent willingness and ability to alter attitudes, thoughts, and behaviors to appropriately respond to actual or anticipated change in the environment.

Clearly, it’s the swings we have to be prepared for… if we want to avoid a loss trap. In a loss trap, investors get caught in a loss and have a hard time getting out. When they lose more than they can afford or more than their risk tolerance, they are prone to tap out after large declines. To avoid the loss trap, know your risk tolerance and actively manage risk within that tolerance.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

Investment results are probabilistic, never a sure thing.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

The observations shared on this website are for general information only and are not specific advice, research, or buy or sell recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. Use of this website is subject to its terms and conditions.

Pingback: Asset Class Returns are Driven by Sector Exposure « ASYMMETRY® Observations