In Growth Stocks have Stronger Momentum than Value in 2018 I explained the divergence between the return of the two styles of Growth and Value. I suggest the real return driver between size and style is primarily the index or ETF sector exposure. To be sure, we’ll take a look inside.

As I said before, the reason I care about such divergence is when return streams spread out and become distinctive, we have more opportunity to carve out the parts we want from the piece I don’t. When a difference between price trends is present, it provides more opportunity to capture the positive trend and avoid the negative trend if it continues.

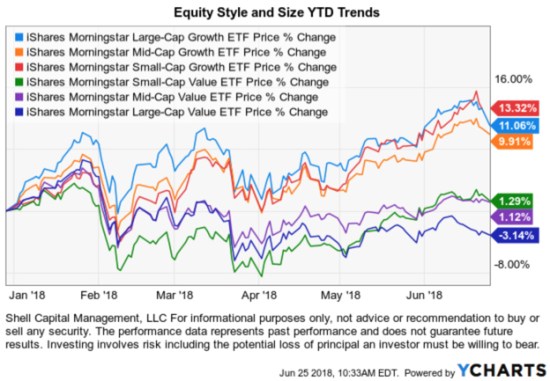

Continuing with the prior observation, I am going to use the same Morningstar size and style ETFs.

Recall the year-to-date price trends are distinctive. Large, mid, and small growth is notably exhibiting positive momentum over large, mid, and small value.

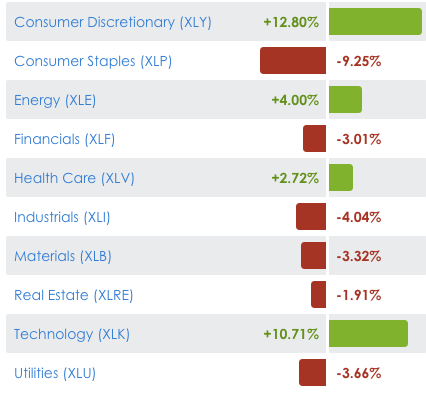

To understand how these factors interact, let’s look at their sector exposure. But first, let’s determine the sector relative momentum leaders and laggards for 2018.

The leaders are Consumer Discretionary (stocks like Netflix $NFLX and Amazon $AMZN), Information Technology (Nvidia $NVDA and Google $GOOG). In third place is Energy and then Healthcare. The laggards are Consumer Staples, Industrials, Materials, and Utilities, which are actually down for the year. Clearly, exposure to Consumer Discretionary and Information Technolgy and avoiding most of the rest would lead to more positive asymmetry.

Below we see strongest momentum Large Growth is heavily weighted (41%) in Technology. The second highest sector weight is Consumer Discretionary, and then Healthcare is third. Large-Cap Growth is the leader just because it has the most exposure in the top sectors.

On the other hand, Large Value, which is down -3% YTD, has its main exposure in the lagging Financial and Consumer Staples sectors.

Dropping down to the Mid-Cap Growth style and size, similar to Large-Cap Growth, we see Information Technology and Healthcare are half of the ETFs exposure.

We are starting to see a trend here. Much like Large-Cap Value, the Mid-Cap Value has top holdings in Financials, Consumer Discretionary, and Utilities sectors.

Can you guess the top sectors of Small-Cap Growth? Like both Large and Mid Growth, Small-Cap Growth top sector exposures are Information Technology, Healthcare, and Consumer Discretionary.

And to no surprise, the Financial sector 26% of Small-Cap Value.

So, Information Technology, Healthcare, and most Consumer Discretionary tend to be more growth-oriented sectors. Financials, Consumer Staples, Utilities, Real Estate, that is, the higher yielding dividend paying types, tend to be classified as Value. Each sector has both Growth and Value stocks within them, but on average, some sectors tend to include more Growth stocks or more Value stocks.

Value stocks are generally defined as shares of undervalued companies with lower prospects for growth.

A growth stock has higher earnings per share and often trade at a higher multiple since the expectation of future earnings is high. Growth stocks usually don’t pay a dividend, as the company would prefer to reinvest retained earnings back into the company to grow.

The Information Technology sector includes companies that are engaged in the creation, storage, and exchange of digital information. The Information Technology sector offers potential exposure to growth with the emergence of cloud computing, mobile computing, and big data.

Another Growth sector is Consumer Discretionary sector manufactures things or provides services that people want but don’t necessarily need, such as high-definition televisions, new cars, and family vacations. Consumer Discretionary sector performance is closely tied to the strength of the overall economy. Consumer Discretionary tends to perform well at the beginning of a recovery when interest rates are low but can lag during economic slowdowns

The Health Care sector is a Growth sector involved in the production and delivery of medicine and health care-related goods and services. Healthcare companies typically have more stable demand, so they are less sensitive to the economic cycle, though it tends to perform best in the later stages of the economic cycle.

It turns out, the three primary Growth sectors that tend to best strongest at the late stage of an economic cycle have been the recent leaders.

Consumer Staples sector consists of companies that provide goods and services that people use on a daily basis, like food, clothing, or other personal products.

The Financial sector is businesses such as banking and brokerage, mortgage finance, and insurance which are sensitive to changes in the economy and interest rates. They tent to perform best at the beginning of a business cycle.

This is why I prefer to focus my U. S. equity exposure on sectors and maybe the strongest momentum stocks within those sectors. Many traditional asset allocations use style and size to get their exposure to the stock market, but as a tactical portfolio manager, I prefer to get more specific into the trending sectors and their individual stocks.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

You can follow ASYMMETRY® Observations by click on on “Get Updates by Email” on the top right or follow us on Twitter.

The observations shared in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results.

Pingback: Trend Analysis of the Stock Market « ASYMMETRY® Observations

Pingback: Is it a stock pickers market? « ASYMMETRY® Observations

Pingback: The week in review « ASYMMETRY® Observations

Pingback: 2nd Quarter 2018 Global Investment Markets Review « ASYMMETRY® Observations