ASYMMETRY® Observations are Mike Shell’s observations of investor behavior causing directional price trends, global macro, tactical ETF trading, momentum stock trading, hedging, volatility trading, and risk management that creates asymmetric investment returns. An asymmetric return profile is a risk/reward profile with a positive asymmetry between profit and loss. Mike Shell is the founder of Shell Capital Management, LLC and the portfolio manager of ASYMMETRY® Global Tactical

Bridgewater Associates, Inc.Co-CIO Karen Karniol-Tambour joins Positive Sum CEO Patrick O’Shaughnessy at the 2023 Sohn Investment Conference. Below is the interview she says the market is very asymmetric right now because of the asymmetry between the upside vs. the downside, and I agree.

I’ll summarize:

If the economy enters a recession, it’s very bad for stocks, and this time the Fed is unlikely to immediately respond by lowering rates since inflation is a problem. So, the downside risk is large. It’s already priced-in to the stock market, so it won’t be a big surprise. Not a lot of upside potential.

If the economy doesn’t enter a recession, the Fed will be in a tough decision point, because inflation is unlikely to come down without a recession. If the Fed doesn’t ease like it’s already price-in, the market is going to be disappointed.

It’s asymmetric because the downside potential is greater than the upside.

The interview:

Patrick O’Shaughnessy:

What do you think that prevailing valuations, let’s say, just on like the big asset classes tell us about what the market thinks is going on? Like, what does it seem like is in prices right now, if you will, as you look at S&P 500 you know, multiples or something very basic like that?

Bridgewater Co-CIO Karen Karniol-Tambour:

WellI think the stock market is telling you that there’s going to be a modest economic slowdown, a pretty contained economic slowdown, nothing like you know a significant recession or anything like that, With that slowdown alone, the Federal Reserve is going to find that sufficient to go ease from you know, 5% to 3% extremely quickly, and that its going to do that despite where inflation is today because inflation is going to go back to totally reasonable levels that they want very very quickly. You see that kind of across stock and bond pricing you know bond pricing is telling you in places to be fine we’re not there’s no inflation from anything like resembling long term and the Fed’s about to ease pretty significantly without a significant slowdown.

Where that sort of leaves you is if the market I believe is asymmetric it’s very asymmetric because it you actually get an economic slowdown; that’s obviously very bad for stocks. I don’t have to tell you that that would be you know pretty bad for stocks. But there’s really not much of a recession priced into them it would be pretty bad. Usually the way you get out of that (as I was saying) is that every time there’s a slowdown the Central Bank just comes and eases right away. Now, not only will it be much harder for them to ease because inflation’s been more a problem. Tension is there, but that easing is already priced in and so even if they do kind of bite the bullet and say “I’m not going to worry about inflation” and ease, it’s already in the market prices it’s not going to surprise the market so much.

Then, on the other hand, if the market doesn’t slow, if the economy doesn’t slow so much, if we don’t get that kind of recession if the equity prices are right that you’re not going to get a big recession and the fed’s going to be a tough spot because I don’t really see why inflation’s going to come down with no recession. You have a very very strong labor market if nothing slows and so if they don’t ease like it’s already price they’re going to be disappointing. So, every day once we hit summer the Federal Reserve doesn’t pivot and ease that’s effectively a tightening relative to what’s priced in that’s also disappointing.

That’s a lot of room for disappointment that can happen whether the economy is strong or weak.

Patrick O’Shaughnessy:

That’s all sort of like what I’ll call you know relatively near to intermediate term future how do you think about portfolio positioning in light of that general view when you know like you for a long time it’s paid to just be long risk and have a very simple portfolio because of everything you’ve discussed. How’s that different today like how would you how do you think about positioning against this asymmetric setup that you described

Karen Karniol-Tambour:

I think it’s one of the toughest times to be an investor in many years because you know as you’re saying risk assets has been so good and I think risk assets are about as unattractive as we’ve seen a very long time and they’ve and that’s we’re seeing that come to fruition they don’t just bounce back you don’t just get kind of automatic rallies no matter what so it’s a hard time to be an investor I think as an investor you have to think about diversification in a different way diversification just wasn’t that important because the one asset people hold “equities” was just the strongest outperformer and the different places investors can kind of look they can look at geographically so they can look at geographies that have less of this tension places like Japan or China where you’re in a different situation you’re not about to hit a big Central Bank tension Japanese Central Bankers are pretty excited about getting higher inflation they’ve won for a long time and it’s far from, you know, out of control.

She basically suggests U.S. stocks are overrated and Japan stocks, Emerging Markets stocks, and Gold, are underrated.

For me, and everyone else even if they don’t realize it, the price trend is the final arbiter.

For more than two decades, I’ve focused my efforts on developing systems to identify trends early in their stage to capitalize on trends as they continue and exit a trend if it reverses.

It all started in business school, where I earned a Bachelor of Applied Science degree in advanced accounting. It was “advanced” because I took the extra advanced classes above a typical accounting major required to sit for the CPA exam in Tennessee. It basically results in a master’s in accounting, but not really, but it’s just the same 150 credit hours.

I rarely speak of my formal college simply because I haven’t considered it a source of edge for investment management.

But maybe it has.

In some conversations recently, people have asked about my background and how I got started as an investment manager and founder of an investment firm. After further review, I’ve come to realize the knowledge I have of financial statements, and the vast details and fundamental information that make them up, is what drove me to observe very little of it really drives the market price in an auction market.

That’s something I’ve always believed, but it occurred to me during business school.

To be succinct; I very quickly discovered undervalued stocks are trading at a cheap multiple of earnings for a reason, and that’s more likely to continue than to reverse.

I didn’t have a lot of capital to play with, and it was hard earned capital. I worked as a Sheriffs’ Officer full time through college fully time, so it took me a few extra years to complete. I wasn’t about to lose too much of what I had in the stock market, so I aimed to cut my losses short early on.

I’ve focused on cutting my losses short ever since, so now I have about 25 years experience as a tactical trader with an emphasis on the one thing I believe I can best limit or control; the downside of my losers.

When I focus on limiting the downside of loss, I am left to enjoy the upside of gains.

But we can’t do that with fundamentals and valuation. Risk can only be directed, limited, managed, and controlled, by focusing on the price trend.

The price trend is more likely to continue than to reverse, as evidenced even by vast academic studies of momentum.

Because a price trend is more likely to continue than to reverse, it’s essential to realize if you attempt to buy stocks that are in downtrends, you’ll likely experience more downtrend.

So, buying what you perceive are “undervalued” stocks is like catching a falling knife they say.

I’d rather wait for the knife to fall, stab the ground or someone’s foot, then pick it up safely.

Knives a dangerous, and up close, even more dangerous than a gun, so govern yourself accordingly.

Nevertheless, the valuation of stocks and overall valuation of the market by and large can be useful to observe at the extremes in valuation.

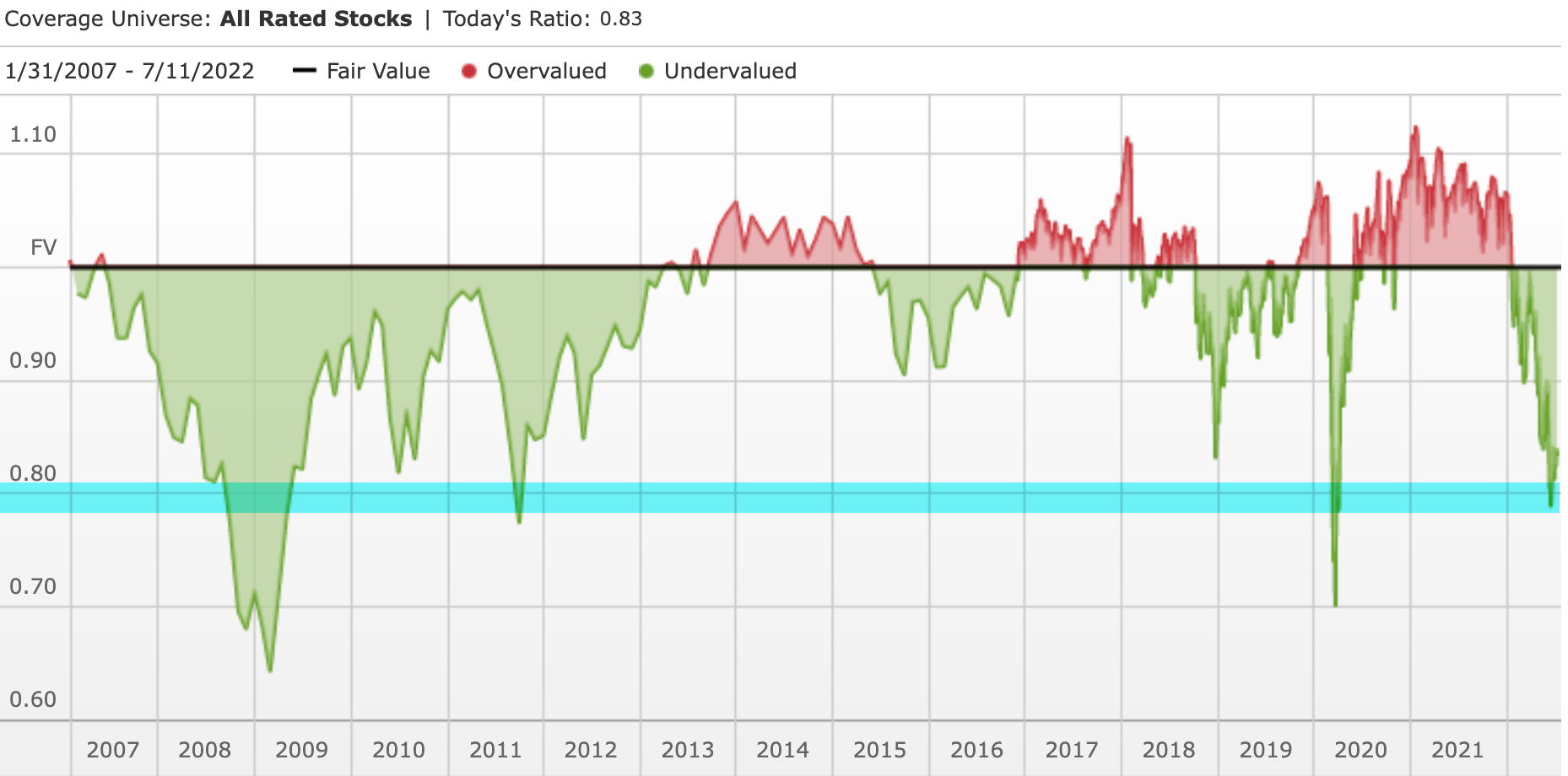

The chart below tells the story based on Morningstar’s fair value estimates for individual stocks.

The chart shows the ratio price to fair value for the median stock in Morningstar’s selected coverage universe over time.

A ratio above 1.00 indicates that the stock’s price is higher than Morningstar’s estimate of its fair value.

The further the price/fair value ratio rises above 1.00, the more the median stock is overvalued.

A ratio below 1.00 indicates that the stock’s price is lower than our estimate of its fair value.

The further it moves below 1.00, the more the median stock is undervalued.

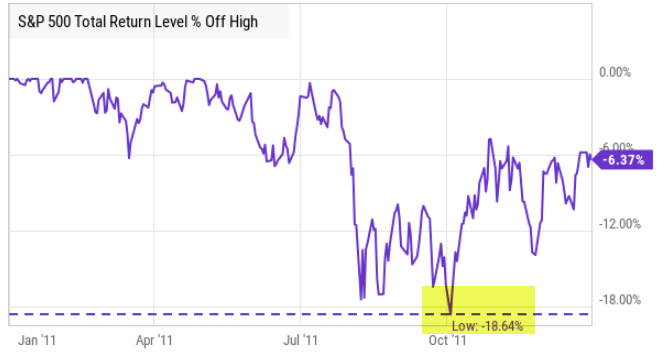

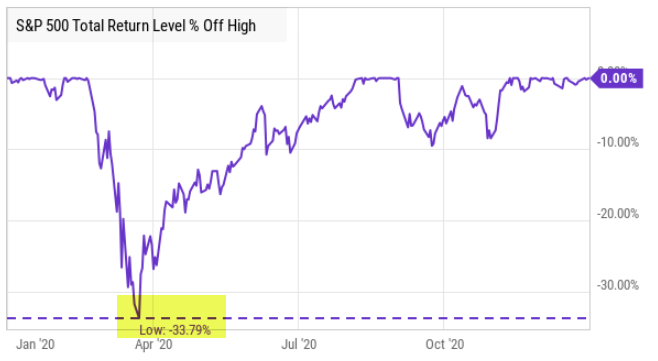

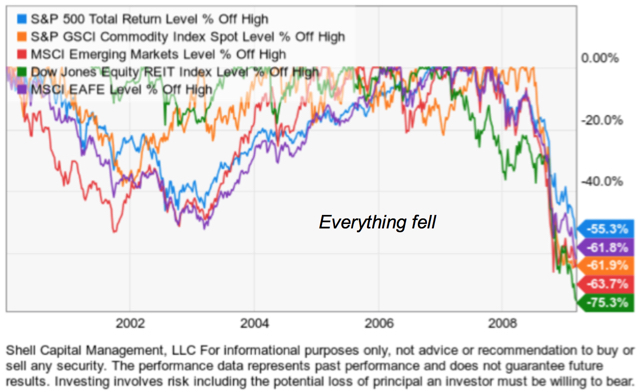

It shows stocks are as undervalued as they were at the low in 2011, nearly as undervalued stocks were March 2020, but not as undervalued as stocks reached in the 2008 stock market crash when the S&P 500 lost -56% from October 2007 to March 2009.

If I were to overall a drawdown chart of the stock index it would mirror the undervalued readings in the chart.

As prices fall, stocks become more undervalued by this measure.

My observation is by and large stocks are relatively undervalued, but they can get much more undervalued if they haven’t yet reached a low enough point to attract institutional buying demand.

To be sure, in 2011 when stocks were as undervalued as Morningstar suggests they are now, the stock index had declined about -19%, similar to the current drawdown of -23%.

The waterfall decline in stock prices March 2020 was -34%, although it recovered quickly in a v-shaped reversal, so it didn’t get as much attention as the current bear market which is down 10% less, but has lasted for seven months without a quick recovery.

Time allows the losses to sink in for those who are holding their stocks.

This time the average stock is down much more than the stock indexes, too, so if you’re holding the weakest stocks your drawdown is worse than the index.

In that case, you’re probably wondering how low it can go.

If stock prices haven’t yet be driven down to a low enough level to attract big institutional capital to buy these lower prices, stocks can certainly trend down a lot lower from here.

For example, in the 2007 – 2009 bear market known as the 2008 Financial Crisis, one I successfully operated through as a tactical trader and risk manager, the stock index dropped -56% over 16 grueling months.

The infamous 2008 crash included many swings up and down on its way to printing a -56% decline from its high in October 2007.

That’s how bad it could get.

It’s also largely the cause of the situation the U.S. finds itself in today.

Since the 2008 Global Financial Crisis, the U.S. Treasury and Federal Reserve Open Market Committee have provided unprecedented support for the equity market and the bond market.

Passive investors and asset allocators have been provided a windfall from the Fed and Treasury, but it’s time to pay the debt.

For passive investors, they’ve been hammered with large losses this year and risk losing more if stock and bond prices keep trending down.

Stocks are already undervalued, but they can get much more undervalued.

Even worse, as my experience tactically operating through many declines like this since the 1990s reflects, are the paranna bites along with the shark bites.

The shark bite is from a passive asset allocator holding on through a prolonged deep bear market in stock prices as they fall -20%, -30%, -40%, -50% or more.

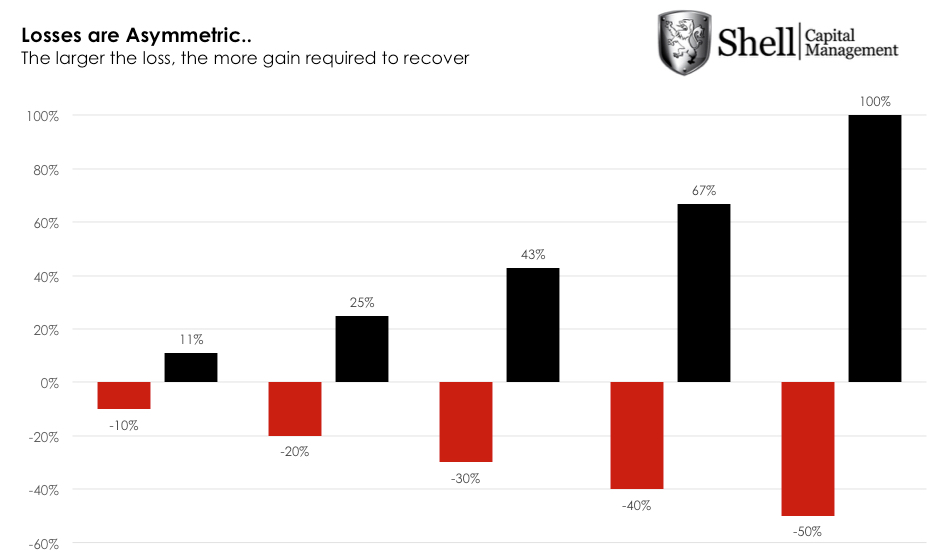

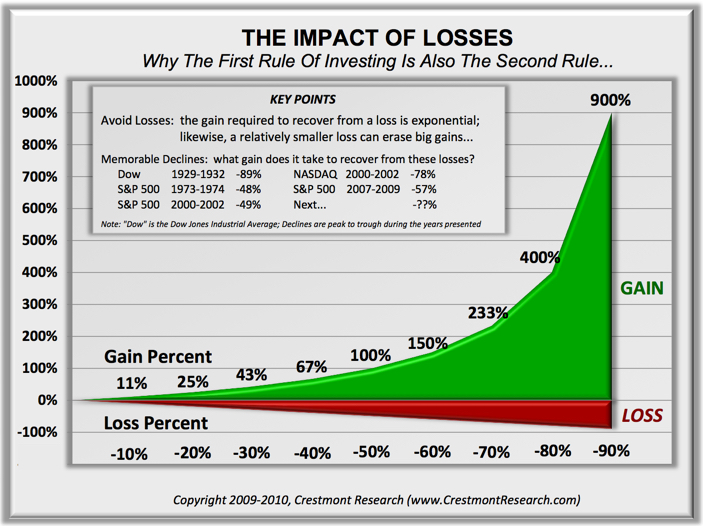

Because losses are so asymemtric and geometically compound aginast you, these capital losses become harder and harder to recover from.

If you lose -50%, it takes a 100% gain to get it back.

Stock market trends are asymmetric; they trend up much lower than they crash down, so that larger gain needed often takes longer, too.

So your emotional capital is at risk.

When you’re down a lot, you’re thinking and decision-making becomes cloudy and stressed because you[‘re under pressure like a pressure cooker.

You don’t know how low it can go.

If you are a buy and hold asset allocator, your loss is unlimited, as there is not point in which you would exit but zero.

Zero may be unlikely, but -50% or more isn’t, as evidenced by history.

And you’ve not been here before.

You’ve not seen this before.

The Fed has never stretched its open market operations this far before.

We just don’t know what’s going to happen next.

But, I’m prepared to tactically execute through whatever unfolds.

I’m having a great year relatively speaking. I’ve been positive most of the year and haven’t ventured far below our all-time new high.

Times like these are when my skillset is designed to show an edge.

Like many tactical investment managers like trend followers, hedge funds, global macro, I too had a period of relative underperformance of the long-only stock indexes. I held my ground but learned some new tricks during the many swings the past decade, and sharpened my countertrend axe to chip away some of the bad parts we don’t want.

But relative outperformance has never been my objective, especially not against a stock index for stock fund that’s fully invested in stocks all the time.

My objective has always been absolute return, not relative return.

My absolute return objective is what drives me to actively manage risk for drawdown control.

Like a good doctor, I aim to first do no harm… as best I can as a risk taker.

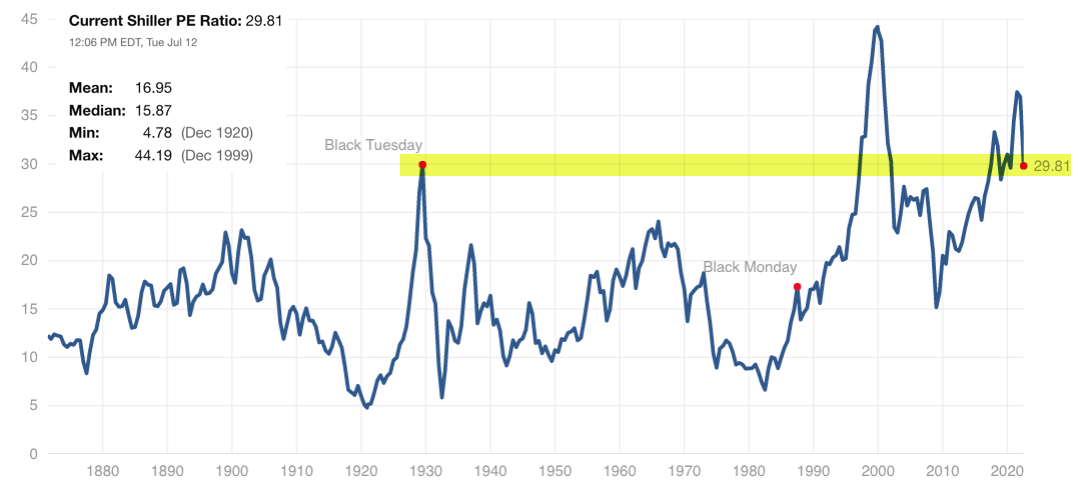

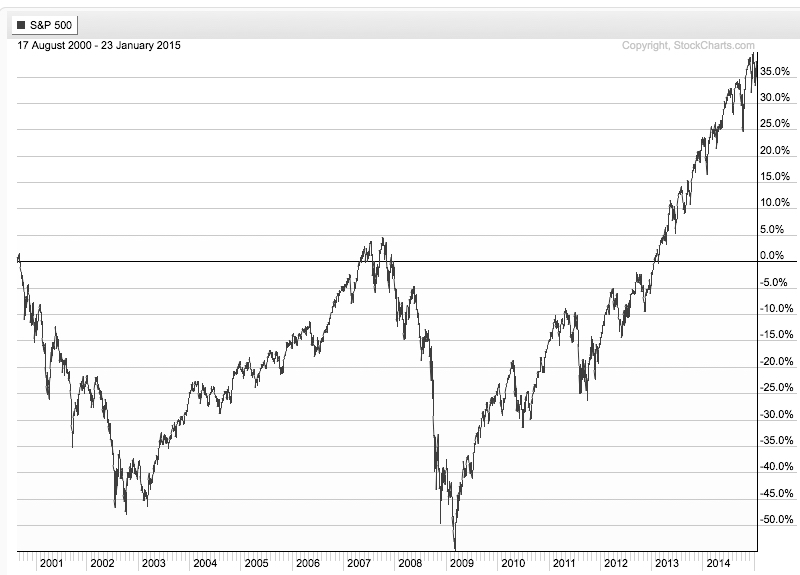

Looking at the Shiller PE ratio for the S&P 500, a long-term observation, the U.S. stock market is still grossly overvalued.

The S&P 500 was the second-highest most expensive valuation in 140 years, and even after the decline this year, the stock index is still twice the valuation of Black Monday in October 1987 and

only down to its extremely overvalued level it was on Black Monday Oct. 19, 1987, when the Dow Jones Industrial Average fell -22% in a single day and just now down to the valuation level the stock index was on Black Tuesday in the 1929 crash.

If you believe in fundamental valuation as a gauge and a guide, anything can happen, so please govern yourself accordingly.

If you need help or have questions, contact us here.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Managed Portfolios. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as investment advice to buy or sell any security. This information does not suggest in any way that any graph, chart, or formula offered can solely guide an investor as to which securities to buy or sell, or when to buy or sell them. Securities reflected are not intended to represent any client holdings or recommendations made by the firm. In the event any past specific recommendations are referred to inadvertently, a list of all recommendations made by the company within at least the prior one-year period may be furnished upon request. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities on the list. Any opinions expressed may change as subsequent conditions change. Please do not make any investment decisions based on such information, as it is not advice and is subject to change without notice. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but are not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect the position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Today was just a reversal of Friday’s late-day surge.

The stock market is even more washed out.

With the Federal Reserve lowering interest rates and buying back bonds, the long term US Treasury Index reversed back up.

The stock indexes are down to their 2018 lows and if the selling doesn’t dry up, we may see a mean reversion of the last 10 years. It wouldn’t be surprising for many reasons, especially when we see it happens to be the area of trouble in 2015-16. Keep in mind, the Fed has been a key return driver for the last several years. It doesn’t seem to be working anymore.

I’m a risk manager, risk-taker, so I increase and decrease exposure to asymmetric risk/reward as conditions change over time. When I see signs of the selling pressure drying up or buying enthusiasm overwhelming the selling pressure, I’ll be looking to buy stocks again.

That is all.

Let me know if we can help.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor in Florida, Tennessee, and Texas. Shell Capital is focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. I observe the charts and graphs to visually see what is going on with price trends and volatility, it is not intended to be used in making any determination as to when to buy or sell any security, or which security to buy or sell. Instead, these are observations of the data as a visual representation of what is going on with the trend and its volatility for situational awareness. I do not necessarily make any buy or sell decisions based on it. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

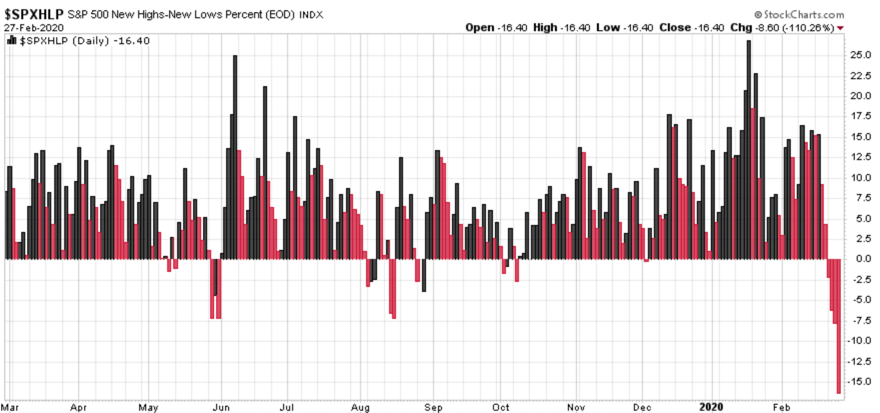

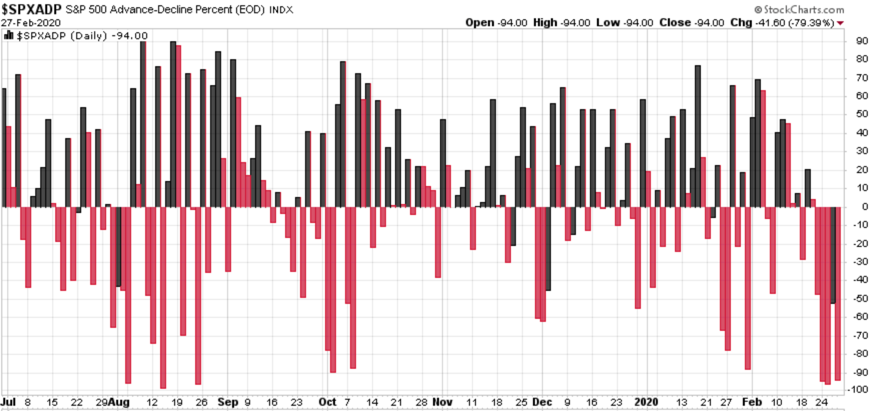

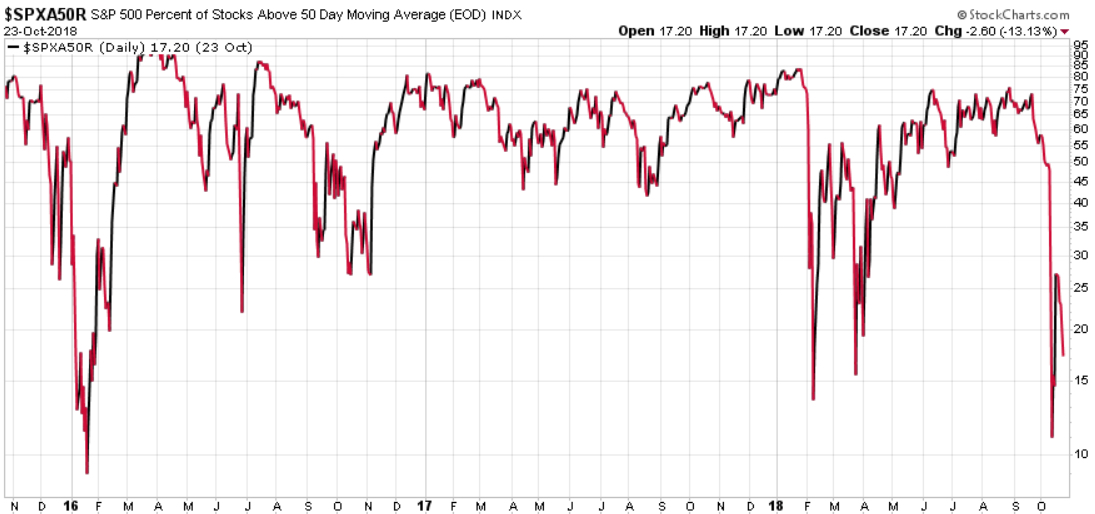

After yesterday’s continued selling pressure, only 7% of the S&P 500 stocks remain in uptrends as measured by the 50-day moving average.

As most stocks are participating in the downtrend, this breadth measure is about as low as it was in December 2018.

In case you are wondering, here are some of the few stocks in the index that are still above their trend line. I don’t consider this a buy list and we don’t own any of them directly.

Another sign of a strong desire to sell is the new highs-new lows as a percentage. It’s as low as it’s been the past year, as new lows are dominating.

As expected, a chart of advance – declining stocks as a percentage is at the low end of its range and about as low as it can get as declining stocks are dominant.

When investors are panic selling, prices can always trend lower, but this data shows mathematically prices have reached an extreme level on the downside that now appears to be an overreaction. We should be close to seeing this panic selling dry up as selling becomes exhausted and these lower prices attract buyers. After that, we’ll see if any countertrend back up continues, or eventually reverses back down. As I’ve said recently, given this bull market is very aged and we’ve seen the longest economic expansion in history, I believe the years ahead will require tactical trading and risk management.

I hope this helps!

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor in Florida, Tennessee, and Texas focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. I observe the charts and graphs to visually see what is going on with price trends and volatility, it is not intended to be used in making any determination as to when to buy or sell any security, or which security to buy or sell. Instead, these are observations of the data as a visual representation of what is going on with the trend and its volatility for situational awareness. I do not necessarily make any buy or sell decisions based on it. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

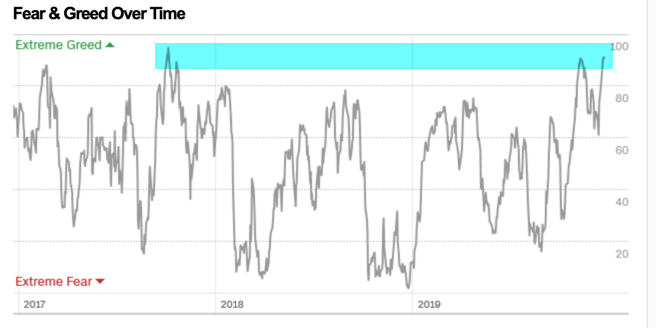

“Someday in the future, stock investors will be giddy again and completely forget about how they feel right now.”

Sure enough, that’s what happened. Individual investors as gauged by the AAII Investor Sentiment Survey capitulated a year ago and have since then oscillated their enthusiasm for stocks sharply as a result of the stock price action. In the chart below we see the stock index with the bullish investor sentiment below it. Investor sentiment clearly oscillates up and down as investors swing from fear and greed, but right now they are bullish.

I also note the bullish sentiment evaporated during every market dip this year. The stock market has memory because its investors do so after such a fall a year ago investors were quick to react (emotionally at least) to every sign of another drop.

It looks like we’re ringing in the new year with high optimism in the stock market.

The Fear & Greed Index, which includes seven different investor sentiment indicators, is dialed up to the “Extreme Greed” level again as people are probably hopeful recent gainst will continue.

The last time this fear and greed gauge was this high was the end of 2017.

The stock market has gained even more in 2019 than it did in 2017, but this year follows a waterfall decline.

After a strong year like 2019, I suggest investors prepare for what could be the opposite in the period ahead.

Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

When multiple statements are given which contradict one another.

These may be given together or may be separated in time. Sometimes the contradictions are rather subtle and are difficult to spot. At other times, they are obvious. If you have enough authority, then you may be able to carry this off.

Mike Shell and Shell Capital Management, LLC is a registered investment advisor and provides investment advice and portfolio management exclusively to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and are not specific advice, research, or buy or sell recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information provided is deemed reliable, but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. Use of this website is subject to its terms and conditions.

Mike Shell and Shell Capital Management, LLC is a registered investment advisor and provides investment advice and portfolio management exclusively to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and are not specific advice, research, or buy or sell recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information provided is deemed reliable, but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. Use of this website is subject to its terms and conditions.

In the last observation I shared about the stock market, “The stock market trends up with momentum,” we saw the stock market reverse back up with strong momentum. The S&P 500 stock index had declined about -7% from its high, then reversed back up 3%. I discussed how investor behavior and sentiment drives market prices. Many investor sentiment measures signaled investor fear seemed to be in control, driving down prices. Volatility had spiked and then started to settle back down. Many individual stocks in the S&P 500 had declined enough to signal shorter-term downtrends, but then they reversed up. I closed by saying:

In summary, today was a strong upward momentum day for the stock market and most stocks participated in the uptrend. After sharp declines like we’ve seen this month, the stock market sometimes reverses up like this into an uptrend only to reverse back down to test the low. After the test, we then find out if it breaks down or breaks out.

One day doesn’t make a trend, but for those who are in risk taker mode with stocks, so far, so good.

The part I bolded with italics has turned out to be the situation this time.

Below is a year to date price trend of the S&P 500 stock index. As of today, my observation “the stock market sometimes reverses up like this into an uptrend only to reverse back down to test the low” is what we are seeing now.

I’ve always believed investment management is about probability and possibilities, it’s never a sure thing. The only certainty is uncertainty, so all we can do is stack the odds in our favor. As I said before, “After the test, we then find out if it breaks down or breaks out.”

The positive news is, investor sentiment measures are reaching levels that often precede short-term trend reversals back up.

The bad news is if the current trend becomes a bigger downtrend these indicators will just stay at extremes as long as they want. We have to actively manage our exposure to loss if we want to avoid large losses, like those -20% or more that are harder to overcome.

Down -10% is one thing, down -20% is another. Any investor should be willing to bear -10% because they will see them many times over the years. Only the most passive buy and hold investors are willing to bear the big losses, which I define as -20% or more.

Nevertheless, I see some good news and bad, so here it is. I’ll share my observations of the weight of the evidence by looking at relatively simple market indicators. I don’t necessarily make my tactical decisions based on this, but it is instead “market analysis” to get an idea of what is going on. Observations like this are intended to view the conditions of the markets.

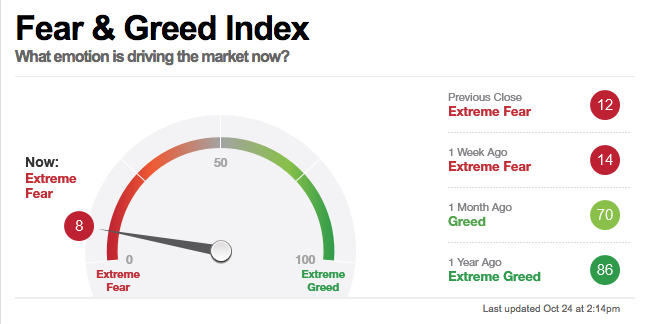

Fear is the dominant driver.

The Fear & Greed Index tracks seven indicators of investor sentiment. When I included it a week ago, it was at 15, which is still in the “Extreme Fear” zone. The theory is, the weighting of these seven indicators of investor sentiment signals when fear or greed is driving the market. Clearly, fear is the dominant driver right now.

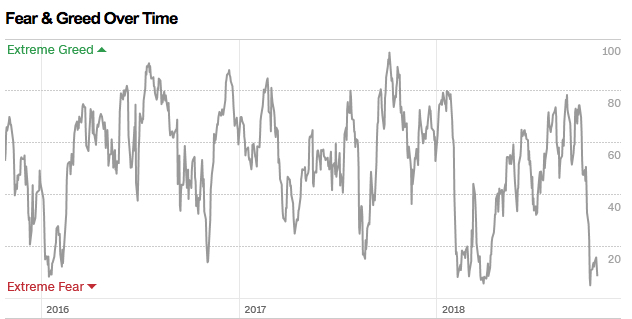

At this point, we can see investor sentiment by this measure has now reached the low level of its historical range. In this chart, we can see how investor sentiment oscillates between fear and greed over time in cycles much like the stock market cycles up and down.

I believe investor behavior is both a driver of price trends, but investors also respond to price trends.

After prices rise, investors get more optimistic as they extrapolate the recent gains into the future expecting the gains to continue.

After prices fall, investors fear losing more money as they extrapolate the recent losses into the future expecting them to get worse.

Investor sentiment and price trends can overreact to the upside and downside and the herd of investors seems to get it wrong when they reach an extreme. We observe when these kinds of indicators reach extremes, these cycles are more likely to reverse. It is never a sure thing, but the probabilities increase the possibility of a reversal. But, since there is always a chance of a trend continuing longer in time and more in magnitude, it is certainly uncertain. Since there is always a chance of a bad outcome, I have my limits on our exposure to risk with predetermined exits or a hedge.

Speaking of a hedge.

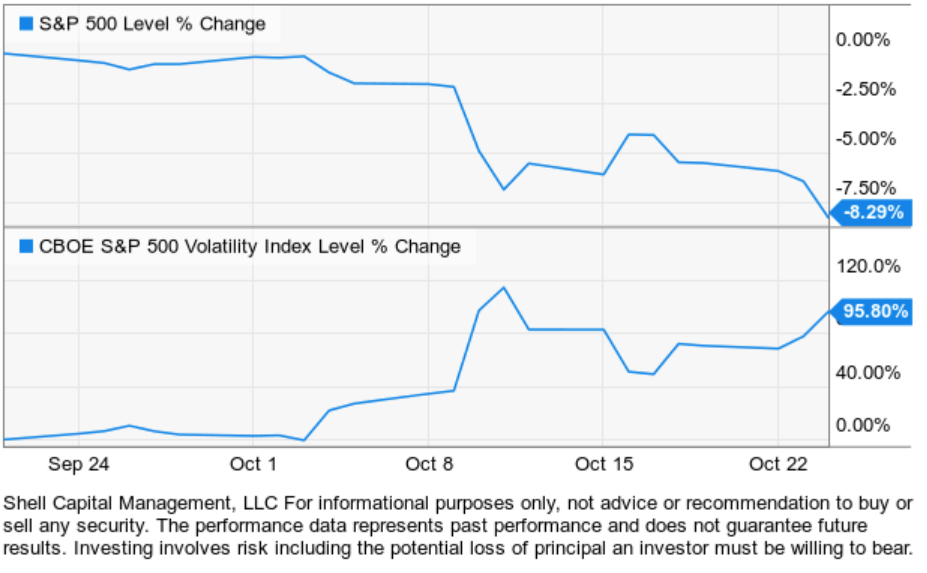

I started pointing out my observation several weeks ago of a potential volatility expansion. If you want to read about it, most of the past few weeks observations have included comments about the VIX volatility index. Over the past few days, we’ve observed a continuation in the volatility expansion.

Implied volatility has expanded nearly 100% over in the past 30 days.

As a tactical portfolio manager, my first focus is risk management. When I believe I have defined my risk of loss, I become willing to shift from risk manager to risk taker. I share that because I want to point out the potential for hedging with volatility. Rather than a detailed exhaustive rigorous 50-page paper, I’m going to keep it succinct.

My day job isn’t to write or talk about the markets. I’m a professional portfolio manager, so my priority is to make trading and investment decisions as a tactical investment manager. I’m a risk manager and risk taker. If I never take any risk, I wouldn’t have any to manage. The observations I share here are just educational, for those who want to follow along and get an idea of how I see things. I hope you find it helpful or at least interesting. It’s always fun when it starts new conversations.

To keep the concept of hedging short and to the point for my purpose today, I’ll just share a simple chart of the price trend of the stock index and the volatility index over the past 30 days. The stock index has declined -8.3% as the implied volatility index expanded over 95%. You can probably see the potential for a hedge. However, it isn’t so simple, because these are just indexes and we can’t buy or sell the VIX index.

The purpose of a hedge is to shift the risk of loss from one thing to another. The surest way to reduce the possibility of loss is to simply sell to reduce exposure in the thing that is the risk. That’s what I do most of the time. For example, when I observed a potential volatility expansion, I reduced my exposure to positions that had the possibility of loss due to increased volatility. Once prices fall and volatility contracts, maybe we increase exposure again to shift back to risk-taking. If we take no risk at all, we would have no potential for a capital gain. So, tactical portfolio management is about increasing and decreasing exposure to the possibility of gain and loss. If we do it well, we create the kind of asymmetric risk/reward I aim for.

So, any hedging we may do is really just shifting from one risk to another, hoping to offset the original risk. Keep in mind, as I see it, a risk is the possibility of loss. I’ll share more on hedging soon. I have some observations about hedging and hedge systems you may find interesting.

Most stocks are participating in the downtrend. Below is an updated chart of the percent of the stocks in the S&P 500 that are above their 50-day moving average. If you want to know more about what it is, read the last observations. The simple observation here is that most stocks are declining.

Much like how we saw investor sentiment cycle and swing up and down, we also see this breadth indicator oscillate from higher risk levels to lower risk levels.

After most stocks are already in uptrends, I believe the risk is higher that we’ll see it reverse.

After most stocks have already declined into downtrends, it increases the possibility that selling pressure may be getting closer to exhaustion.

The good news is, at some point selling pressure does get exhausted as those who want to sell have sold and prices reach a low enough level to bring in new buying demand.

That’s what stock investors are waiting for now.

These are my observations. I don’t have a crystal ball, nor does anyone. I just predetermine my risk levels in advance and monitor, direct, and control risk through my exits/hedging how much I’m willing to risk, or not. We’ll just have to see how it all unfolds in the days and weeks ahead.

Only time will tell if this is the early stage of a bigger deeper downtrend or just another correction within the primary trend.

I hope you find my observations interesting and informative.

The observations shared on this website are for general information only and are not specific advice, research, or buy or sell recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. Use of this website is subject to its terms and conditions.

Much of the observations I shared last week are continuing to be more apparent this week. So, in case you missed it, this may be a good time to read them.

I discussed how earnings season can drive a volatility expansion in stocks, especially high growth momentum stocks. The stock market leaders can become priced for perfection, so we never know how investors will react to their earnings reports. To achieve asymmetric returns from momentum stocks, we need a higher magnitude of positive reactions than adverse reactions over time. On a quarterly basis, it can be tricky. The gains and losses as much as 20% or more in the most leading momentum stocks like Facebook ($FB), Google ($GOOGL), Twitter ($TWTR), Grub ($GRUB), and NetFlix ($NFLX) have since provided a few examples.

In Front-running S&P 500 Resistance I shared an observation that many market technicians incorrectly say support and resistance appear before it actually does. We won’t know if resistance to a price breakout exists until the price actually does pause and reverse. I suggested the S&P 500 may indeed pause and reverse, but not because the index drives the 500 stocks in it, but instead because my momentum indicators suggested the $SPY was reaching a short-term overbought range “So, a pause or reversal, at least some, temporarily, would be reasonable.” As of today, the S&P 500 has paused and reversed a little. We’ll see if it turns down or reserves back up to continue an uptrend.

In Asymmetry of Loss: Why Manage Risk? I showed a simple table of how losses compound exponentially. When losses become greater than -20%, it becomes more exponential as the gains required to recover the loss are more and more asymmetric. This simple concept is essential and a cornerstone to understanding portfolio risk management. Buy and hold type passive investors who hold a fixed allocation of stocks and bonds are always fully exposed to market risk. When the market falls and they lose -20%, -30%, -50% or more of their capital, they then face hoping (and needing) the market to go back up 25%, 43%, or 100% or more just to get back to where they were. This can take years of valuable time. Or, it could take a lifetime, or longer. Just because the markets have rebounded after being down for four or five years from their prior highs doesn’t guarantee they will next time. Past performance is no guarantee of future results.

In Trend following applied to stocks, the message was short and sweet: gains are produced by being invested in stocks or markets that are trending up and losses are created by stocks trending against us. Investors prefer to be in rising stocks and out of falling stocks. But, as I showed in Earnings season is tricky for momentum growth stocks the trick is giving the big trends enough room to unfold. In fact, applying trend following and momentum methods to stocks is also tricky. It’s a skill that goes beyond just looking at a chart and it’s not just a quantitative model.

About two weeks ago, the measures of investor sentiment showed a lot of optimism about future stocks prices, so we shouldn’t have been surprised to see some stocks fall. When a lot of enthusiasm is already priced in, investors can respond with disappointment when their stocks don’t live up to high expectations.

Much of the momentum and trend following in stocks is driven by an overreaction to the upside that can be accompanied by an overreaction to the downside. A robust portfolio management system factors these things in.

You can follow ASYMMETRY® Observations by click on on “Get Updates by Email” on the top right or follow us on Twitter.

The observations shared in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results.

Momentum stocks are stocks that show high upside momentum in their price trend. Momentum stocks are trending not only regarding their absolute price gains but also relative strength vs. other stocks or the stock market index.

Momentum stocks are usually high growth stocks. Since momentum stocks are the strongest trending stocks, their trends are often driven by growth in sales and earnings. Growth stocks are companies that are growing earnings at a rate significantly above average. Growth stocks have high increases in earnings per share quarter over quarter, year over year, and may not pay dividends since these companies usually reinvest their strong earnings to accelerate growth.

Now that we have defined what I mean by “momentum stocks,” we can take a look at some examples of momentum stocks and their characteristics like how their prices trend.

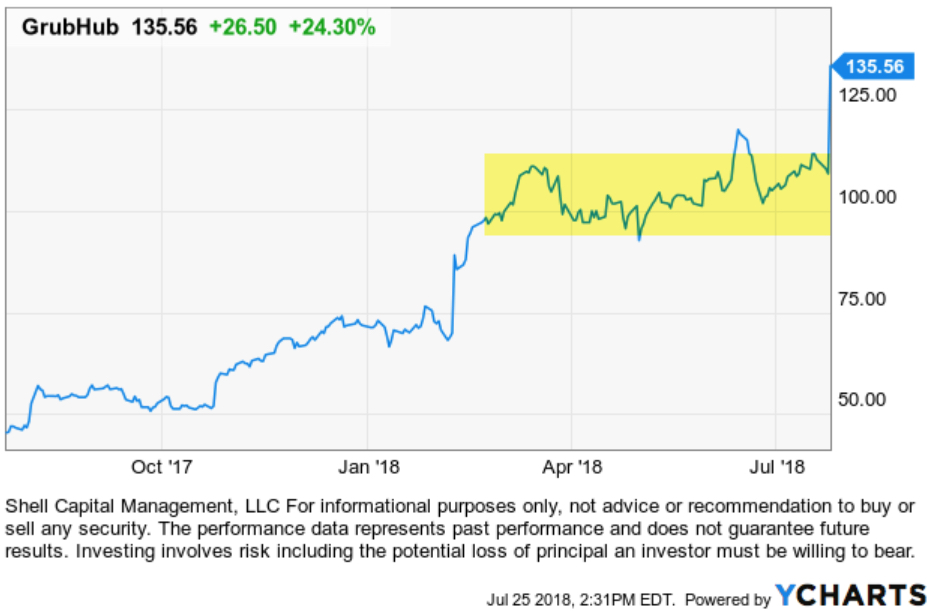

Grubhub Inc. ($GRUB) is an online and mobile food-ordering company that connects diners with local restaurants. GrubHub is a great example today of a high momentum growth stock. GrubHub stock has gained 24% today after smashing Wall Street’s expectations. Earnings grew 92% to 50 cents a share, marking the fifth quarter in a row of accelerating EPS growth. Revenue soared 51% to $239.7 million, a quarterly best.

Before today, GrubHub stock was in a positive trend that developed a flat base since April (highlighted on the chart). GRUB had already gained 60% year to date, but after such as explosive uptrend in momentum, it trended sideways for a while.

It is earnings season, which can be tricky for the highest momentum stocks. Once a stock has already made a big move, it could already have a lot of good news expectations priced in. That concerns some momentum stock traders. In fact, I know some momentum stock traders who exit their stocks before their quarterly earnings announcements. If they had exited GrubHub, they would have missed today’s continuation of its momentum. However, they would avoid the downside of those that trend in the other direction.

I’ve been trading momentum stocks for over two decades. Over the years I’ve observed different regimes of how they act regarding trend strength and volatility. There are periods of volatility expansion and contraction and other periods when momentum is much stronger.

Volatility is how quickly and how far the price spreads out. When price trends are volatile, it’s harder to stick with them because they can move against us. We like upside volatility, but smart investors are loss averse enough to dislike downside volatility that leads to drawdowns. To understand why the smart money is loss averse, read: “Asymmetry of Loss: Why Manage Risk?“.

Strong upward trending stocks are sometimes accompanied by volatility. That’s to be expected because momentum is a kind of volatility expansion. Upward momentum, the kind we like, is an upward expansion in the range of the price – volatility.

That’s good vol.

But, strong trending momentum stocks necessarily may include some bad volatility, too. Bad volatility is the kind investors don’t like – it’s when the price drops, especially if it’s a sharp decline.

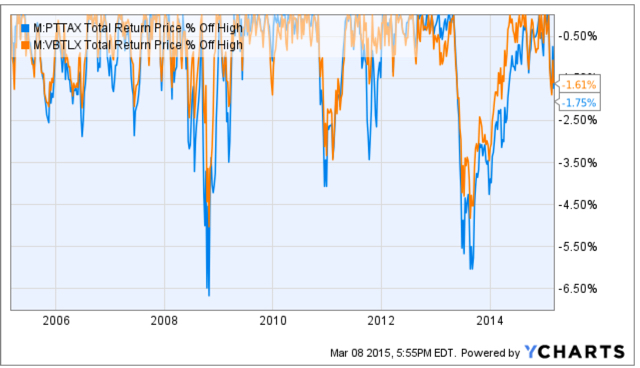

I mentioned GrubHub had gained 60% YTD. I like to point out, observe, and understand asymmetries. The asymmetry is the good and the bad, the positive and the negative, I prefer to skew them positively. What I call the Asymmetry® Ratio is a chart of the upside total return vs. the chart of the downside % off high. To achieve the gain for GrubHub, investors would have had to endure its price declines to get it. For GrubHub, the stock has declined -10% to -15% many times over the past year. It has spent much of the time off its high. To have realized all of the gains, investors had to be willing to experience the drawdowns.

I point this out because yesterday I wrote “Asymmetry of Loss: Why Manage Risk?” where I discussed the mathematical basis behind the need for me to actively manage the downside risk. To achieve the significant gain, we often have to endure at least some of the drawdowns along the way. The trick is how much, and for me, that depends on many system factors.

Earnings season, when companies are reporting their quarterly earnings, is especially tricky for high momentum stocks because stocks that may be “priced for perfection” may be even more volatile than normal. Accelerating profit growth is attractive to investment managers and institutional investors because increasing profit growth means a company is doing something right and delivering exceptional value to customers. I’m more focused on the direction of the price trend – I like positive momentum. But, earnings are a driver of the price trend for stocks.

Earnings can trend in the other direction, too, or things can happen to cause concern. This information is released in quarterly reports.

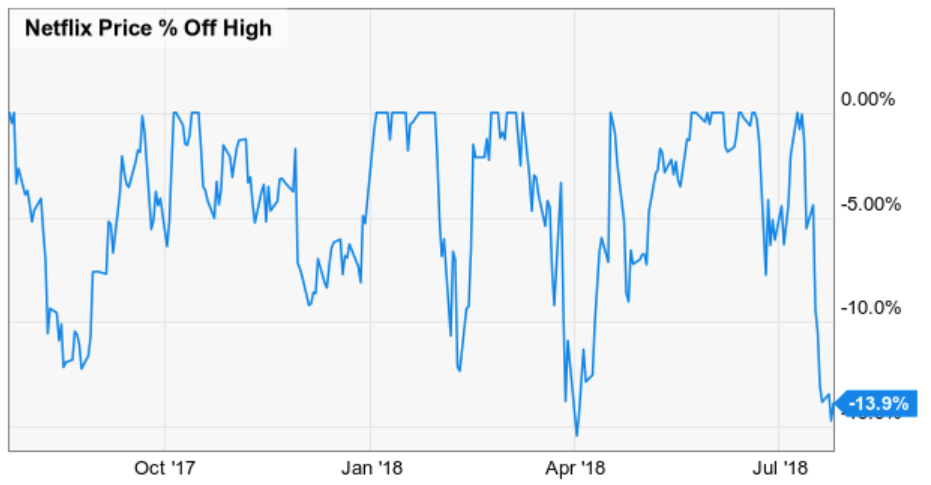

Another example of a momentum stock is NetFlix. By my measures, GrubHub is a leading stock in its sector and NetFlix (NFLX) is the leader in its industry group, too, based on its positive momentum and earnings growth. As we see in the chart below, NFLX has gained 88% year to date. That’s astonishing momentum considering the broad stock market measured by the S&P 500 has gained around 5%, and its Consumer Services Sector ETF has gained 11%.

However, NetFlix stock regularly declines as much as -15% as a regular part of its trend. It has fallen over -10% five times in the past year on its way to making huge gains. The latest reason for the decline was information that was released during its quarterly earnings announcement. The stock dropped sharply afterward.

But, as we see in the chart, it’s still within its normal decline that has happened five times the past year.

While some of my other momentum stock trader friends may exit their stocks during the earnings season, I instead focus more on the price trend itself. I predefine my risk in every position, so I determine how much I’ll allow a stock to trend to the downside before I exit. When a stock trends down too far, it’s no longer in a positive trend with the side of momentum we want. To cut losses short, I exit before the damage gets too large.

How much is too much?

A hint is in the above charts.

If we want to experience a positive trend of a momentum stock, we necessarily have to give it enough room to let it do what it does. When it trends beyond that, it’s time to exit and move on. We can always re-enter it again it if trends back to the right side.

Sure, earnings season can be tricky, but for me, it’s designed into my system. I’m looking for positive Asymmetry® – an asymmetric risk/reward. What we’ve seen above are stocks that may decline as much as -15% as a normal part of their trend when they fall, but have gained over 50% over the same period.

You can probably see how I may be able to create a potentially positive asymmetric risk/reward payoff from such a trend.

You can follow ASYMMETRY® Observations by click on on “Get Updates by Email” on the top right or follow us on Twitter.

The observations shared in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results.

“The essence of portfolio management is the management of risks, not the management of returns.” —Benjamin Graham

Why actively manage investment risk?

Why not just buy and hold markets and ride through their large drawdowns?

Losses are asymmetric and loss compounds exponentially.

The larger the loss, the more gain is required to recover the loss to get back to breakeven.

The negative asymmetry of loss starts quickly, losses more than -20% decline start to compound against you exponentially and with a greater magnitude the larger the loss is allowed to grow.

If your investment portfolio experiences a -20% loss, it needs a 25% gain to get back the breakeven value it was before the loss.

At the -30% loss level, you need a 43% gain to get it back.

Diversification is often used as an attempt to manage risk by allocating capital across different markets and assets.

Diversification and asset allocation alone doesn’t achieve the kind of risk management needed to avoid these large declines in value. Global markets can fall together, providing no protection from loss.

For example, global markets all fell during the last two bear markets 2000-2003 and 2007-2009.

It didn’t matter if you had a global allocation portfolio diversified between U.S. stocks, international stocks, commodities, and real estate REITs.

Diversification can fail when you need it most, so there is a regulatory disclosure required: Diversification does not assure a profit or protect against loss.

This is why active risk management to limit downside loss is essential for investment management.

I actively manage loss by knowing the absolute point I’ll exit each individual position and managing my risk level at the portfolio level.

Active risk management, as I use it, applies tactics and systems to actively and dynamically decrease or increase exposure to the potential for loss.

My risk management systems are asymmetric risk management systems. Asymmetric risk management intends to manage risk with the objective of a positive asymmetric risk/reward.

My asymmetric risk management systems are designed to cut losses short, but also protects and manages positions with a profit.

After markets trend up for a while without any significant interruption, investors may become complacent and forget the large damage losses can cause to their capital and their confidence. When investors lose confidence in the markets, they tap-out when their losses are allowed to grow to large.

I prefer to stop the loss before it gets too large. How much is too large depends on the client, but also the math. As seen here, I have a mathematical basis for believing I should actively manage investment risk.

It’s why I’ve been doing it for two decades. Because I understood the math, I knew I had to do it over twenty years ago and developed the systems and tactics that proved to be robust in the devastating bear markets I’ve executed through since then.

You can follow ASYMMETRY® Observations by click on on “Get Updates by Email” on the top right or follow us on Twitter.

The observations shared in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results.

Christi Shell was recently asked by ETF.com “Does your firm use active ETFs”.

Her answer from the interview:

Our portfolio manager, Mike Shell, doesn’t currently include active ETFs in our universe of tradeable ETFs, but that doesn’t mean he’d never include them. He tactically shifts between ETFs, based on investor behavioral measures and supply/demand. So our portfolio management style itself is the active management; we are, essentially, actively managing beta.

We use ETFs to gain specific exposure to a return stream such as a sector, country, commodity or currency. With an index ETF, we pretty much know what we’re going to get inside the ETF. (Of course, indexes are reconstituted by a committee of people, so we don’t know in advance what they’ll do. However, an index follows some general rules systematically.)

Therefore, if we discover an ETF we believe has a strategy and return stream that we want access to, then we would add it, whether it’s active or not.

Christi Shell is Managing Director and Certified Wealth Strategist® at Shell Capital Management LLC. Christi has 27 years in financial services ranging from bank management to wealth management giving her a unique skill set and experience to help clients get what they want.

Sometimes the stock market is trending so strongly that the rising tide lifts all boats. No matter what stocks or stock fund you invest in, it goes up. That was the case much of 2017.

Then, there are periods when we see more divergence.

When we observe more divergence, it means stocks, sectors, size, or style has become uncorrelated and are trending apart from each other.

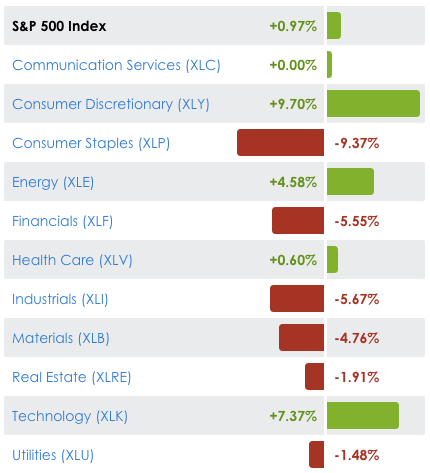

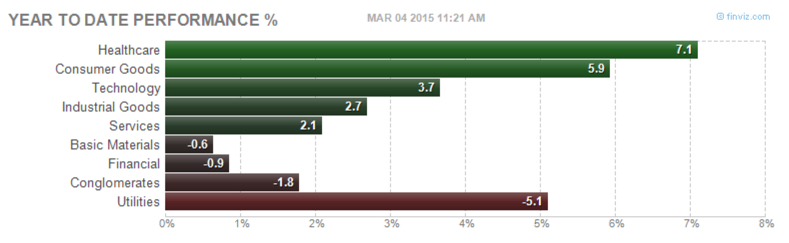

I pointed out in Sector Trends are Driving Equity Returns; there is a notable divergence in sector performance, and that is driving divergence in size and style. Growth stocks have been outperformance value, and it’s driven by strong momentum in Technology and Consumer Discretionary sectors.

When specific sectors are showing stronger relative momentum, we can either focus more on those sectors rather than broad stock index exposure. Or, we can look inside the industry to find the leading individual stocks.

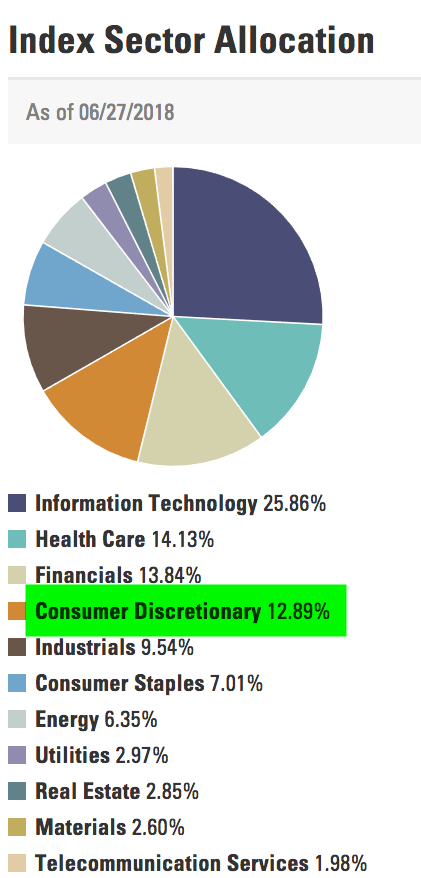

For example, Consumer Discretionary includes industries like automobiles and components, consumer durables, apparel, hotels, restaurants, leisure, media, and retailing are primarily represented in this group. The Index includes Amazon, Home Depot, Walt Disney, and Comcast. Consumer Discretionary is the momentum leader having trended up 9.7% so far this year as the S&P 500 has only gained just under 1%.

If we take a look inside the sector, we see the leaders are diverging farther away from the sector ETF and far beyond the stock market index.

In fact, all the sectors 80 stock holdings are positive in 2018.

The Consumer Discretionary sector is about 13% of the S&P 500. As you can see, if these top four or five sectors in the S&P 500 aren’t trending up it is a drag on the broad stock index.

So, Is it a stock pickers market?

When we see more divergence, it seems to be a better market for “stock pickers” to separate the winners from the losers.

Another way to measure participation in the market is through quantitative breadth indicators. Breadth indicators are a measure of trend direction “participation” of the stocks. For example, the percent of the S&P 500 stocks above or below a moving average is an indication of the momentum of participation.

Below is the percent of stocks above their 50 day moving average tells us how many stocks are trending above their moving average (an uptrend). Right now, the participation is symmetrical; 52% of the stocks in the S&P 500 are in a positive trend as defined by the 50 day moving average. We can also see where that level stands relative to the stock market lows in February and April and the all-time high in January when over 85% of stocks were in an uptrend. By this measure, only half are trending up on a shorter term basis.

The 200-day moving average looks back nearly a year to define the direction of a trend, so it takes a greater move in momentum to get the price above or below it. At this point, the participation is symmetrical; 55% of stocks are above their 200-day moving average and by this time frame, it hasn’t recovered as well from the lows. The percent of stocks above their 200-day moving average is materially below the 85% of stocks that were participating in the uptrend last year. That is, 30% fewer stocks are in longer trend uptrends.

In the above charts, I only showed a one-year look back of the trend. Next, we’ll take a step back to view the current level relative to the past three years.

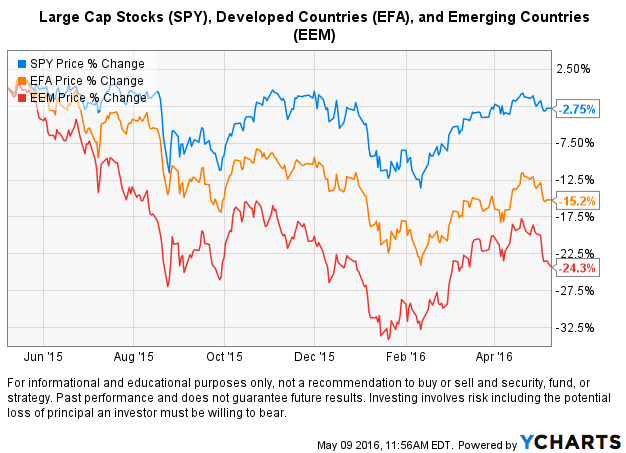

The percent of stocks above their 50 day moving average is still at the upper range of the past three years. The significant stock market declines in August-September 2015 and December-January hammered the stocks down to a very washed out point. During those market declines, the participation was very asymmetric: 90% of the stocks were in downtrends and only about 10% remained in shorter-term uptrends.

The percent of stocks above their 200 day moving average also shows a much more asymmetrical situation during the declines in 2015 and 2016 when the stock index dropped around -15% or more. Only 20% of stocks remained in a positive trend.

Is it a stock pickers market?

Only about half of the stocks in the index are in uptrends, so the other half isn’t. So, if we avoid the half that are in downtrends and only maintains exposure to stocks in uptrends and the trends continue, we can create alpha.

But, keep in mind, that doesn’t necessarily mean we should have any exposure at all in the S&P 500 stock index because happens to have the highest sector exposure in the leading sectors.

But, for those who want to engage in “stock picking”, the timing has a higher probability now to diverge from the stock index than last year because so fewer stocks are in uptrends and more are in downtrends.

For individual stocks traders willing to look inside the box, this is a good thing.

You can follow ASYMMETRY® Observations by click on on “Get Updates by Email” on the top right or follow us on Twitter.

The observations shared in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results.

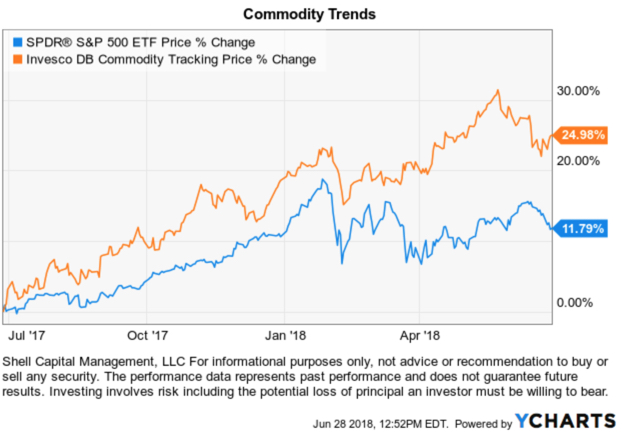

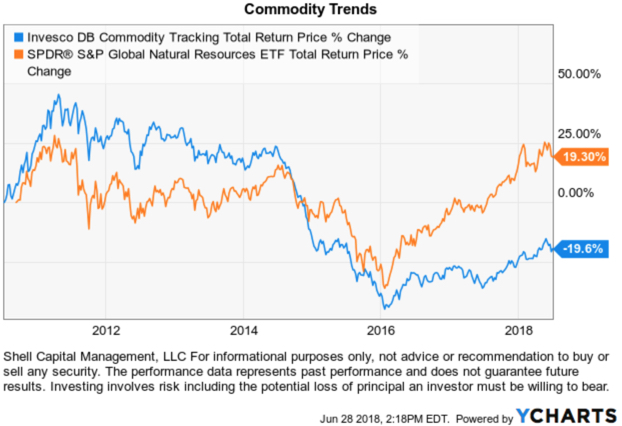

Commodities are trending with better momentum than stocks over the past year.

A commodity is a raw material or primary agricultural product that can be bought and sold, such as copper or coffee. A commodity is a basic good used in commerce that are usually used as inputs in the production of other goods or services.

Soft commodities are goods that are grown, such as wheat, or rice.

Hard commodities are mined. Examples include gold, helium, and oil.

Energy commodities include electricity, gas, coal, and oil. Electricity has the particular characteristic that it is usually uneconomical to store, and must, therefore, be consumed as soon as it is processed.

The Commodity Trend

At first glance, we see in the chart commodities ETF Invesco DB Commodity Index Tracking ETF has trended meaningfully above the popular S&P 500 index of U. S. stocks. The relative outperformance is clear over this one-year time frame. Commodities, as measured by this ETF, are in an absolute positive trend and registering relative momentum.

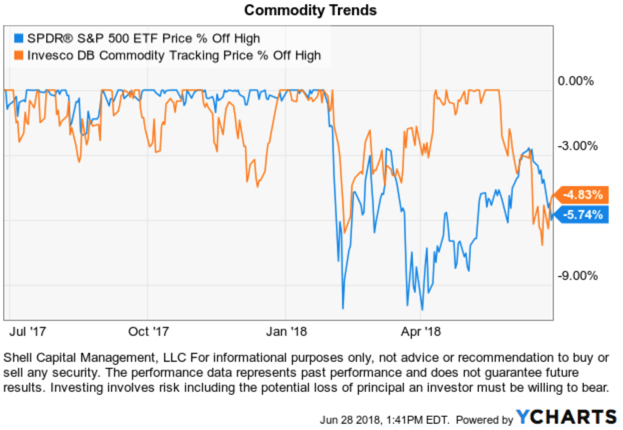

Examining a price trend is incomplete without also considering its downside. On the downside, I look at the % off high drawdowns over the period. We see that commodities were more volatile than stocks before 2018 with four dips around -4%. Since the stock market -10% decline that started in February, commodities declined, too, but not as much as U. S. stocks.

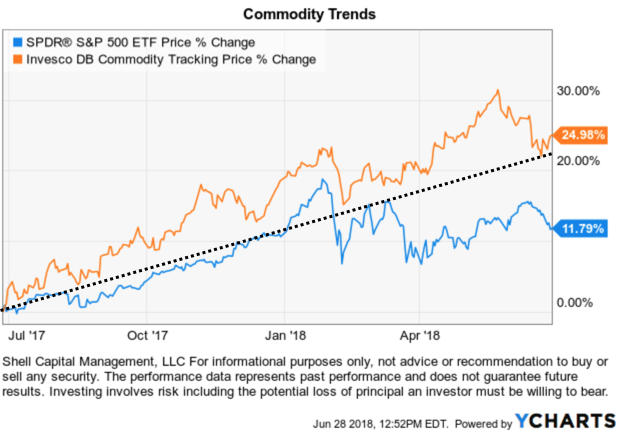

Looking back at the trend chart, I added a simple trend line to show that communities are trending directionally better than the popular U. S. stock index. So, my quantitative Global Tactical Rotation® system that ranks an unconstrained global universe of markets including bonds, stocks, commodities, currencies, and other alternatives like real estate signaled this trend has been generating asymmetric risk/return.

What is the that Invesco DB Commodity Index Tracking ETF? (the bold emphasis is mine)

The Invesco DB Commodity Index Tracking Fund seeks to track changes, whether positive or negative, in the level of the DBIQ Optimum Yield Diversified Commodity Index Excess Return™ (DBIQ Opt Yield Diversified Comm Index ER) plus the interest income from the Fund’s holdings of primarily US Treasury securities and money market income less the Fund’s expenses. The Fund is designed for investors who want a cost-effective and convenient way to invest in commodity futures. The Index is a rules-based index composed of futures contracts on 14 of the most heavily traded and important physical commodities in the world. The Fund and the Index are rebalanced and reconstituted annually in November.

This Fund is not suitable for all investors due to the speculative nature of an investment based upon the Fund’s trading which takes place in very volatile markets. Because an investment in futures contracts is volatile, such frequency in the movement in market prices of the underlying futures contracts could cause large losses. Please see “Risk and Other Information” and the Prospectus for additional risk disclosures. Source: Invesco

The challenge for some investors, however, is that Invesco DB Commodity Index Tracking ETF generates a K-1 tax form for tax reporting. That isn’t a terrible issue, but it means instead of receiving the typical 1099 investors receive a K-1. Some investors aren’t familiar with a K-1, and they can obtain them later than a 1099.

Then, there may be other investors who simply prefer not to own futures for the reason in the second paragraph of the above discription: “Because an investment in futures contracts is volatile, such frequency in the movement in market prices of the underlying futures contracts could cause large losses.” In reality, all investments have risk and stocks can have just as much risk of “large losses” as commodity futures, but it’s a matter of investor preference and perception.

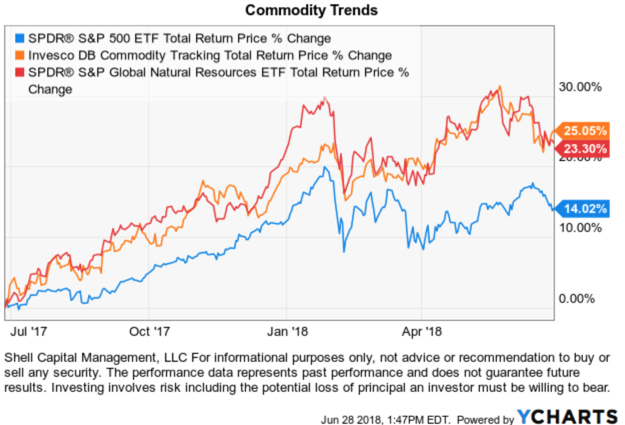

Since we have a wide range of investor types who invest in my ASYMMETRY® Investment Program I could gain my exposure to commodities in other ways. For example, the SPDR® S&P® Global Natural Resources ETF often has a similar return stream as ETFs like DBC that track a commodity futures index, except is actually invests in individual stocks instead.

The SPDR® S&P® Global Natural Resources ETF seeks to provide investment results that, before fees and expenses, correspond generally to the total return performance of the S&P® Global Natural Resources Index (the “Index”)

Seeks to provide exposure to a number of the largest market cap securities in three natural resources sectors – agriculture, energy, and metals and mining

Maximum weight of each sub-index is capped at one-third of the total weight of the Index

Below we see the price trend of this ETF of global natural resources stocks has been highly correlated to an ETF of commodities futures.

In fact, as we step the time frame out to the common inspection date of each ETF in 2011, the SPDR® S&P® Global Natural Resources ETF has actually outperformed Invesco DB Commodity Index Tracking ETF overall in terms of relative momentum.

The bottom line is, commodities “stuff” is trending up over the past two years and when the price of “stuff” is rising, that is called “inflation”. Commodities and global natural resources have been in a downtrend for so long it shouldn’t be a surprise to see this trend reverse up. Only time will tell if it will continue, but if we want exposure to it, we can predefine our risk by deciding at what price I would exit if it doesn’t, and let the trend unfold.Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.You can follow ASYMMETRY® Observations by click on on “Get Updates by Email” on the top right or follow us on Twitter.The observations shared in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results.Buying and Selling ETFsETFs are flexible and easy to trade. Investors buy and sell them like stocks, typically through a brokerage account. Investors can also employ traditional stock trading techniques; including stop orders, limit orders, margin purchases, and short sales using ETFs. They are listed on major US Stock Exchanges.

ETFs are subject to risk similar to those of stocks including those regarding short-selling and margin account maintenance. Ordinary brokerage commissions apply. In general, ETFs can be expected to move up or down in value with the value of the applicable index. Although ETF shares may be bought and sold on the exchange through any brokerage account, ETF shares are not individually redeemable from the Fund. Investors may acquire ETFs and tender them for redemption through the Fund in Creation Unit Aggregations only. Please see the prospectus for more details. After-tax returns are calculated based on NAV using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on the investor’s tax situation and may differ from those shown. The after-tax returns shown are not relevant to investors who hold their fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. Performance of an index is not illustrative of any particular investment. It is not possible to invest directly in an index. As with all stocks, you may be required to deposit more money or securities into your margin account if the equity, including the amount attributable to your ETF shares, declines. Unless otherwise noted all information contained herein is that of the SPDR S&P Global Natural Resources ETF. S&P – In net total return indices, the dividends are reinvested after the deduction of withholding tax. Tax rates are applied at the country level or at the index level.

After yesterdays 1.1% gain for the S&P 500, it is back in positive territory for the year. It’s been a very volatile start for 2018 with an abnormally strong trend in U.S. stocks late 2017 continued in January only to be wiped out in February. Below is a visual representation, showing the period November 2017 to the low last month. I point that out to show how quickly a trend can change and prior gains of 12% in just a three-month time frame and be erased in a -10% decline over 9 days. Most of the decline was in two days over that period.

With that said, as the broad stock market is lagging in its third month of the year so far, two sectors are leading. Consumer Discretionary (XLY) and Technology (XLK). At Shell Capital, we monitor global market trends at the broad market level like the S&P 500 which is diversified across 500 stocks that are a part of 10 sectors. These sectors are tradable via ETFs. We can quickly get broad exposure to the overall stock market, or we can get more granular and get exposure to a sector in a low-cost structure with Sector ETFs. I also monitor the individual stocks inside the sector ETF. When the overall market is in a positive trend, most of the stocks in a sector should be trending up. But, when the overall market has struggled to trend up, like this year-to-date, fewer stocks are trending up inside a sector.

The popular narrative becomes “it’s a stock pickers market.”

I don’t say that myself, I just observe when it is “a stock pickers market” naturally through my daily quantitative research. Here are some examples of my observation.

I pointed out yesterday in Buying demand dominated selling pressure in the stock market that only 32% of the 500 stocks in the S&P 500 are above their 50-day moving average. After yesterdays stock market gain, the participation increased to 40%. The 50-day moving average is a short-term trend indicator, so if 60% of the stocks are below that trend line, we can infer “most stocks are in short-term downtrends.” As of yesterdays close, only 203 (40%) of the S&P 500 are above their 50-day moving average, which means 297 are below it. You can probably see if the price trend continues up, we should see more and more stocks participate in the trend. In fact, if we don’t see more stocks participate, it necessarily means only a few stocks are driving the broad index trend up. I would consider that “a stock pickers market.” Of course, the trick is to see this in advance, or early enough in the stage to capitalize on it. We don’t have to know in advance what’s going to happen next, and we don’t, we just need to observe it soon enough to capture some positive asymmetry (P>L).

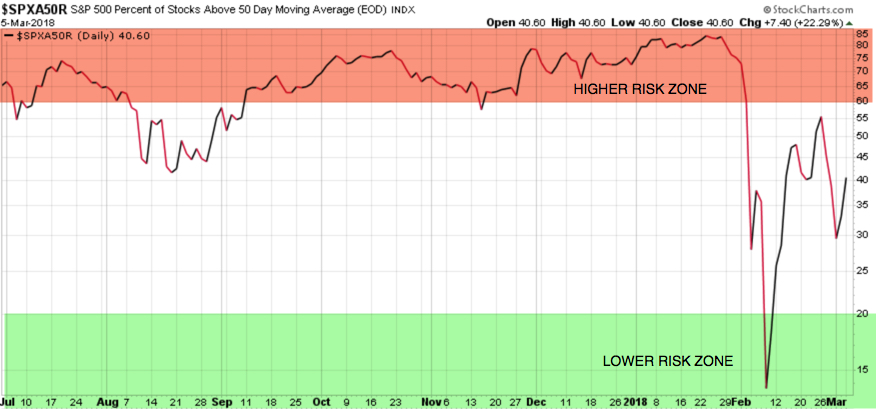

I like a visual representation, so here is the chart of the S&P 500 Percent of Stocks Above 50 Day Moving Average. I colored the top part of the chart red and labeled it “Higher Risk Zone” and the lower part green with the label “Lower Risk Zone”. The observation is when 80% of stocks are already trending positive that momentum is a good thing, but as a skilled risk manager, I begin to prepare for change. After most stocks are already trending up, the stock market has been trending up, so a skilled risk manager prepares for a countertrend reversal that is inevitable at some point. As I shared in my observation near the low, Stock Market Analysis of the S&P 500 when nearly all the stocks were already in negative trends as a skilled risk-taker, I look for that to reverse, too.

This is only a small glimpse at what I look at for illustration purposes to make the point how I can quantify a “stock pickers market.” After 83% of stocks were already in downtrends I shifted from a risk manager stance to risk-taker mode looking. That is, shifting from a reversal down in January after prices had already trended up to an extreme, to preparing for the decline to end after the stock index quickly dropped -10% and my many indicators were signaling me when and where to pay attention. I shared this to represent that I was not surprised to see certain stocks lead a trend direction when so many had shifted from positive trends to negative trends in a short-term time frame.

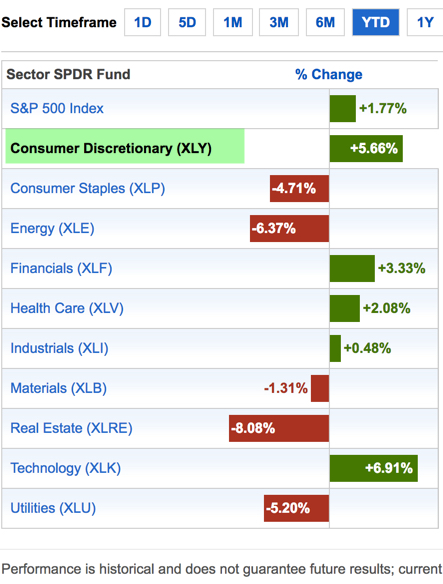

This leads me to my main point, which is very simple. A simple way to observe a “stock pickers market” is to see that certain stocks are leading the trend. Because so may stocks were in short-term downtrends, it isn’t a surprise to see a few strong relative strength leaders inside a sector. For example, in the Sector ETF performance table below, two leading sectors are Consumer Discretionary (XLY) and Technology (XLK). They are up about 6-7% as the broad stock index is up 1.77%. Let’s see what is driving their stronger relative momentum.

Looking inside the Sector for the Leading Stocks

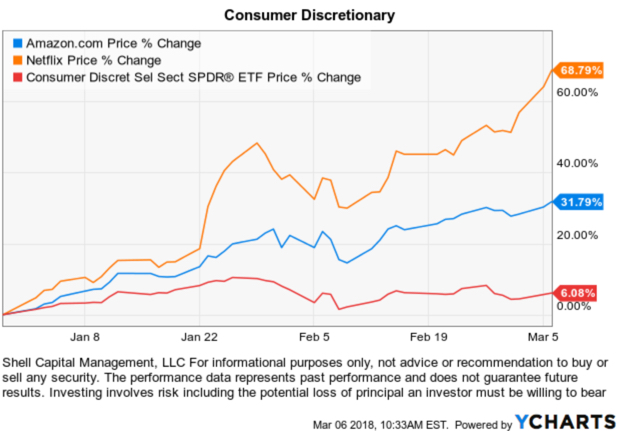

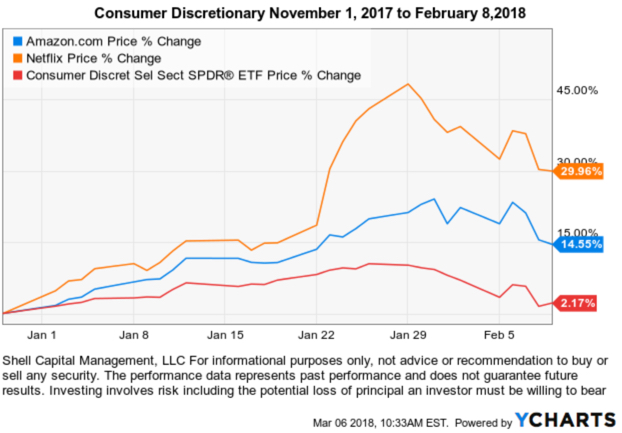

Reviewing the holdings of the Consumer Discretionary $XLY ETF, Amazon.com Inc $AMZN is 20.69% of the Consumer Discretionary Sector and has gained +30.28% for the year. A 20% weighting of a stock that has gained 30% results in a 6% contribution to the portfolio return. That is, this one large position has contributed 100% of the sectors return year-to-date. There are 84 stocks in the ETF. This doesn’t mean the other 83 stocks are flat with no price change. Instead, some of them were also positive for the year and some are negative. So far this year, they have offset each other. Some stocks in the sector have gained more than Amazon, but it makes the simple example because it’s exposure is the largest at 20%. Netflix $NFLX, for example, is the sector ETFs biggest gainer up 64%, but it’s 4.63% of the portfolio. However, because it’s gain is so strong this year its contribution at the portfolio level is still significant at 3% of the 5.66% YTD gain in the sector ETF. That is an extreme example. Why is it extreme? Let’s look at price charts of the year-to-date price trend, then the drawdown, which expresses the ASYMMETRY® ratio. The ASYMMETRY® ratio is a ratio between profit and loss, upside vs. downside, or drawdown vs. total return.

First, we observe the price trend for 2018 of the Consumer Discretionary Sector ETF $XLY, Netflix $NFLX, and Amazon $AMZN. The divergence is clear. But, you may notice they all had a drawdown a few weeks ago. All to often I see the upside presented, but not enough about the path we would have to endure to achieve it. To get a complete picture of asymmetric reward to risk, we want to see the drawdown, too, so we understand the ASYMMETRY® ratio.

Those are some big impressive short-term gains in those stocks. Clearly, this past performance may not be an indication of future results. Too bad we can’t just know for sure in advance which is going to trend up with such velocity. We can’t catch every trend, but if we look in the right way we may find some. In order to take a position in them, we’d have to be willing to experience some downside risk, too. As a portfolio manager, I decide how much my risk is in my positions and at the portfolio level by predefining when I’ll exit a losing position. But, to understand how much downside is possible in stocks like this and the sector ETF, I can examine the historical drawdown. We’ve seen a drawdown in the stock market already this year. Below we see the Consumer Sector ETF drawdown was about -8% a few weeks ago. Amazon wasn’t more, even though it’s gain is much more than the sector. That’s what I’m calling positive asymmetry and good looking asymmetric reward to risk in regard to the trend dynamics. Netflix declined -13%, but its gain is much higher. This is what leading stocks are supposed to look like. They have their risk and they could decline a lot more than the market if investors lose their enthusiasm for them, but we can manage that risk with our exit and drawdown controls.

I often say that it doesn’t matter how much the return is if the risk and volatility are so high you tap out before it is achieved. To better understand that, I want to show two more charts of these stocks. Below is what the YTD price change looked like at the February low. If investors watch their holdings closely and have emotional reactions, you can see how this would be viewed as “I was up 45% and now only 30%.” Many investors (and professional advisors) have difficulty holding on to strong trends when they experience every move.

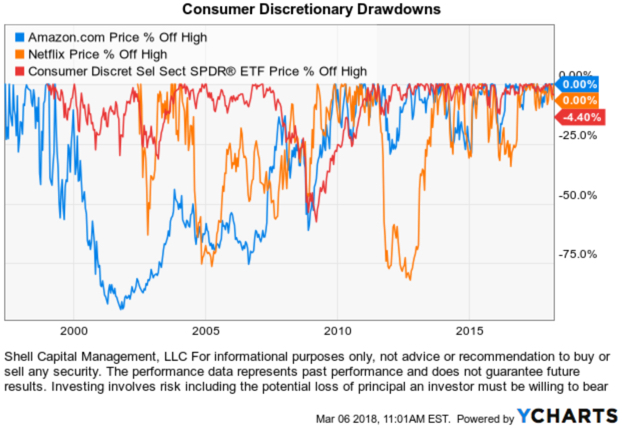

One more chart to illustrate how it doesn’t matter how much the return is if the risk and volatility are so high you tap out before it is achieved. I don’t believe we can just buy and hold and reach our objective of asymmetric reward to risk. I believe risk must be managed, directed and controlled. To make the point, below are the historical drawdowns that have been -60% to -90% in these three. It doesn’t matter how much the return is if the risk and volatility are so high you tap out before it is achieved! To extract positive asymmetric reward to risk, we must necessarily do something different than buy and hold.

This may make you wonder: Why buy a sector ETF if you can buy the strongest stocks?

The divergence isn’t normally this wide. In a trending market, more of the other stocks would normally be participating in a trend. This is why I first explained that in an upward trending market we normally see the majority of stocks eventually trending together. When that is true, the sector ETF provides good exposure and limits the selection risk of just one or two stocks. Make no mistake, individual stocks are riskier. Individual stocks are more subject to negative news like disappointing earnings reports, negative product outlook, or key executives leaving the company, etc. So, individual stocks are more volatile and subject to trend in much wider swings both up and down. But for me, I apply the same risk management systems to predefine my risk at the point of entry drawdown controls as the trend unfolds in the stock, up or down.

Yes, it’s been a “stock pickers market” so far and that trend may continue. It just means that fewer stocks are leading the way for now and in a healthy trend more stocks will participate if the short-term uptrend continues to make higher highs and higher lows. As a tactical portfolio manager, my focus is on what seems to offer the positive ASYMMETRY® of a positive asymmetric reward to risk.

The trend has changed for U.S. stocks since I shared my last observation. On January 27th I pointed out in The U.S. Stock Market Trend that the directional trend for the popular S&P 500® U.S. large cap stock index was still up, though it declined more than -10% twice over the past year. At that point, it had made a slightly lower high but held a higher low. Since then, theS&P 500® declined to a lower low.

First, let’s clearly define a trend in simple terms. A trend is following a general course of direction. Trend is a direction that something is moving, developing, evolving, or changing. A trend is a directional drift, one way or another. I like to call them directional trends. There is an infinite number of trends depending on the time frame. If you watch market movements daily you would probably respond to each day’s gain or loss thinking the trend was up or down based on what it just did that day. The professional traders who execute my trades for me probably consider every second a trend because they want to execute the buy or sell at the best price. As a tactical position trader, I look at multiple time frames from months to years rather than seconds or a single day. So, trends can be up over one time frame and down over another.

As we observe the direction of “the trend”, let’s consider the most basic definitions over some specific time frame.

Higher highs and higher lows is an uptrend.

Lower lows and lower highs is a downtrend.

If there is no meaningful price break above or below those prior levels, it’s non-trending.