Volatility Targeting

What is volatility targeting?

Volatility targeting definition is a volatile system or model that applies a measure of volatility to determine the position size or asset allocation of an investment portfolio.

Volatility targeting means the investment manager will increase or decrease the amount of exposure or leverage to ensure the volatility of the portfolio is close to the target level of volatility.

Volatility targeting signals when volatility goes up, the portfolio manager will scale down the portfolio exposure to volatility. When the volatility measure goes down, the portfolio manager will increase the exposure to the market or positions to march the targeted exposure.

Volatility targeting applies a range of measures of volatility. Some investment managers may use some time frame of historical standard deviation as a measure of realized volatility. Others may use an average true range. Some asset managers may use implied volatility from options prices of some combination of them all.

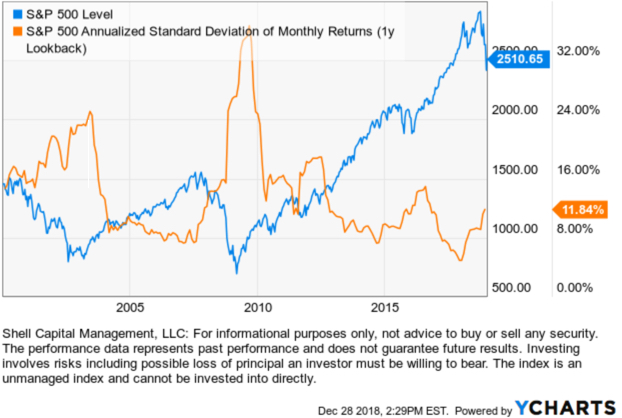

The risk of volatility targeting is it may overweight a market like stocks after they’ve trended up just before they trend down. After the market falls, the volatility targeting may then underweight exposure to stocks and overweight exposure to other markets like bonds or cash just in time for stocks to trend up again. For example, the chart below shows this risk of volatility targeting.

You must be logged in to post a comment.