ASYMMETRY® Observations are Mike Shell’s observations of investor behavior causing directional price trends, global macro, tactical ETF trading, momentum stock trading, hedging, volatility trading, and risk management that creates asymmetric investment returns. An asymmetric return profile is a risk/reward profile with a positive asymmetry between profit and loss. Mike Shell is the founder of Shell Capital Management, LLC and the portfolio manager of ASYMMETRY® Global Tactical

There was enough buying climaxes in stocks this week to signal a short term top in the stock market.

This week 596 stocks printed a buying climax, which is the most since Feb 2018.

A buying climax is when a stock trends up to a 52 week high, then closes the week with a loss, which is a sign of distribution shifting from strong to weak hands.

A buying (or selling) climax is the result of surge in supply and demand.

The key theory of a buying climax is the exhaustion of demand as the last buyers enter the market.

The final surge of buying typically leads to p

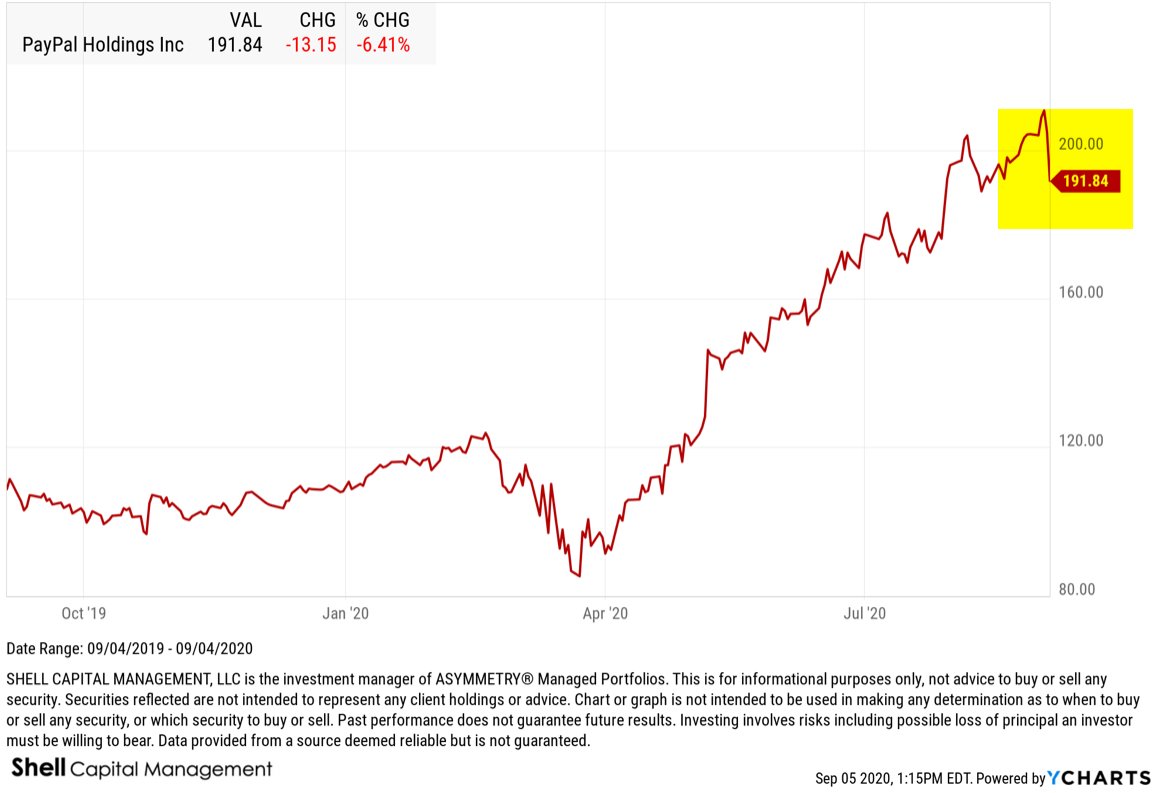

For example, PayPal printed a buying climax this week. Shares of PYPL trended up to a new 52 week high, then closed down on the week. It’s a sign of distribution, as shares of shifting from strong holders to weak. Stocks like PayPal have benefited from people staying at home and buying things online. It was a leading stock with strong relative strength, until now.

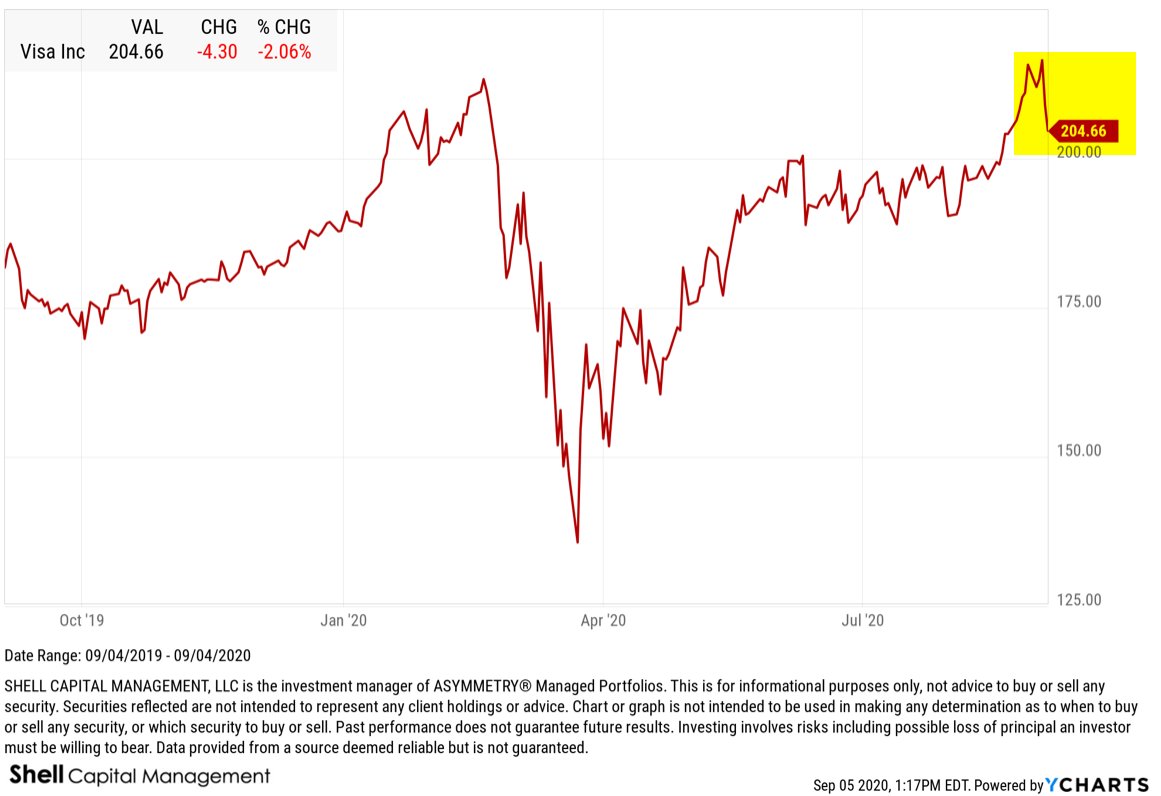

Visa (V) is another example of a BUYING CLIMAX. Visa has been a leading stock with strong momentum and earnings growth, but it trended to a new high, then closed down.

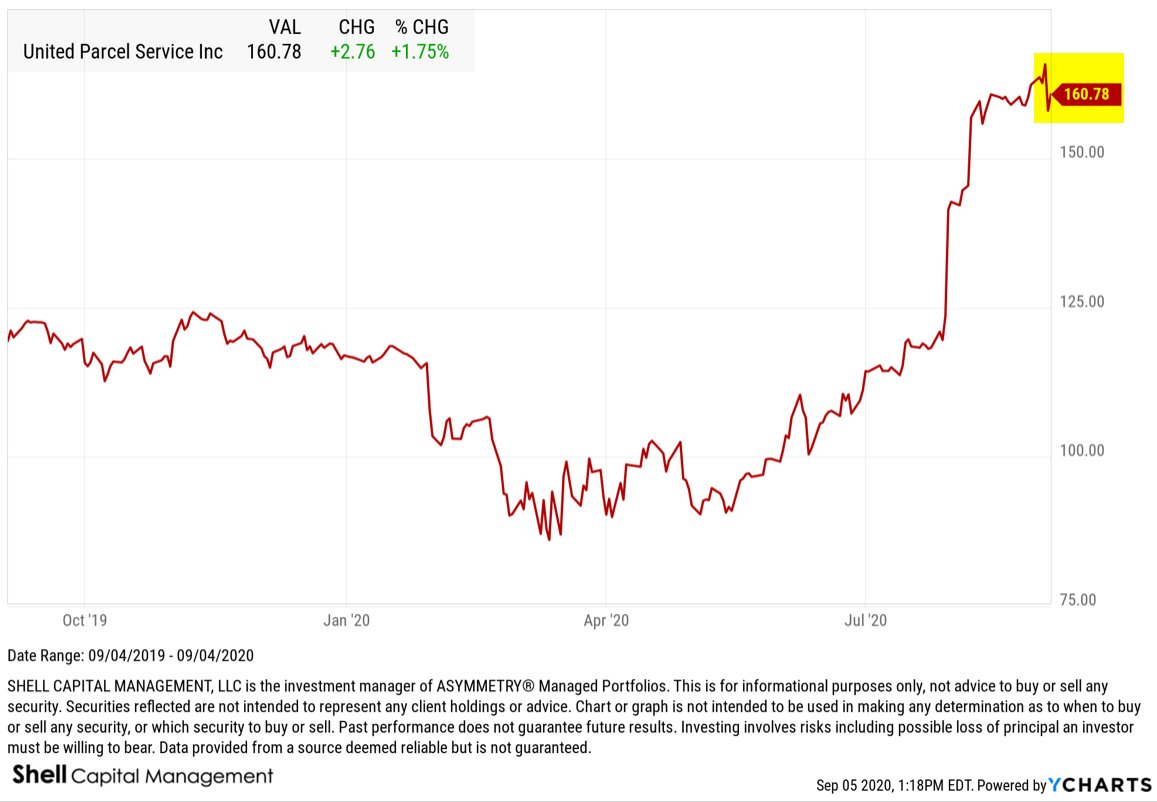

UPS is another example of a BUYING CLIMAX from a leading stock as it printed a new 52 week high, but closed down this week. Not as strong of an example as above, but a buying climax nonetheless.

As stocks like UPS have benefited from the stay at home climate of rising deliveries, it’s obviously driven by companies like Amazon (AMZN), which happens to be another BUYING CLIMAX example.

Amazon trended to a new high, then closed down this week.

Costco (COST) is another example of a big winning stock that printed a new high during the recent euphoria for stocks that closed down this weak to print a buying climax.

Nvidia has been one of the most explosive momentum stocks this year. NVDA printed a new high, then closed -12% off its high this week.

The list of 596 stocks that printed a Buying Climax includes most of the recent leading momentum technology stocks like Apple, Adobe, Microsoft, but also financials like asset manager BlackRock.

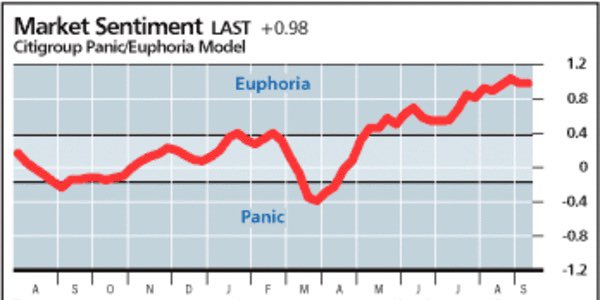

The bottom line is: we’ve seen a period of euphoria, as measured by investor sentiment indicators like the Citigroup Panic/Euphoria Model, and now we’re seeing some blow off tops shift to buying climaxes.

These quantitative indicators have a long history of signaling a shift in supply and demand, which suggests the risk level is elevated for the stock market.

We typically see a buying climax at the end of a bull market cycle.

Investors confidence the trend will continue results in complacency as to market risk. Their confidence the uptrend will continue drives them to ignore the risk of loss, so they don’t manage their risk or hedge exposure to loss.

Complacent investors believe the current trend isn’t going to reverse anytime soon, so they get caught off guard when it does.

Once they start taking on heavy losses, they may panic sell, adding to the selling pressure that pushes prices down even lower.

Risk averse investors should prepare themselves for an increasing probably of a downtrend in stocks.

This may be just a warning shot across the bow of what may be more selling pressure to come.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Technical analysis is the study of financial market price trends.

What’s funny is that technical analysis has evolved into now being called quantitative analysis.

Technical analysis has long been a method of much debate, until the academics determined that past price performance may have an impact on future performance.

I’ve been a chartist and technician for over twenty years now, and I make no bones about it.

I’m also called an independent thinker, because I don’t care what others think of it. I do me, and you do you.

Academics previously didn’t think the study and measurement of past price trends had any edge to be gained. It’s probably because Eugene Fama said “markets are efficient.” So, if it comes from the ivy tower of university, it must be true?

It isn’t.

The efficient-market hypothesis is a hypothesis in financial economics that states that asset prices reflect all available information.

If markets are efficient, then all known information is already factored into prices, and so there is no way to “beat” the market because there are no undervalued or overvalued securities available.

That’s far from reality.

If the markets reflect all known information, and are efficient, then how could we explain a -34% decline in the S&P 500? and a -37% decline in the Dow Jones Industrial Average in just three weeks?

No, that’s gotta be an under-reaction or an overreaction, or both at different times.

It’s the under-reaction and overreaction to new information that causes prices to drift, or trend, directionally over time rather than just always spiking up or down. It’s always what drives momentum, which is know even accepted by academics who didn’t want to believe that past performance had any impact on the current or future price.

I know, it was a silly proposition. Who wouldn’t look at the past price history for perspective of its historical direction, momentum, and volatility.

I was attracted to charting early on in my career. As I earned an advanced accounting degree, including all the advanced accounting courses on top of the standard ones, which would qualify me for the CPA exam in Tennessee. I don’t know about other states, but Tennessee required 150 credit hours and at least five advanced accounting classes on top of the core accounting degree. It is basically a Master’s degree, since I think a B.S. is about 124 hours.

Anyway, I did it, and the more I learned accounting, the more I realized it wasn’t of much use in an auction market.

In theory, the price of a stock trades at some multiple of earnings and such. If it were so simple, we could easily determine with high probability what a stock should trade at, and it would be accurate.

But it isn’t.

I say that anything other than the price trend itself has the potential to lead you astray from its reality.

That includes fundamental valuation measures.

I know accounting and finance about as well as anyone, and as a student who was trading stocks, it didn’t take long to realize the above statement. If a stock is undervalued, there’s a reason the market doesn’t like it. You may not know the reason yet, but some large institutional investors may.

I prefer to follow the big money that moves the price trend. They aren’t always right, either, but all the really matters is the direction they drive the price.

Does it really matter why?

or who?

So I’m a realist. I’ve got a lot of stereotypes I guess.

As I show you the following charts, I like to also include what may be wrong about them. For example, I’m about to show you the price trend of the S&P 500 index, which includes in it about 500 stocks. So, when we look at the index price trend, we have to realize what it represents. If we make a judgment based on the trend of an index, we’re doing it with an understanding there are about 500 different company stocks moving around inside it that have an impact on the outcome.

It isn’t perfect, but neither is fundamental analysis.

Here we go. What we have here is the popular stock index rubbing up on the top end of a range that represents the prior (February) high.

Technicians, or technical analysts, call this area “resistance”, but I disagree.

I call it potential resistance.

You see, it isn’t resistance until it is.

Resistance is an area on the chart where selling pressure overwhelms buying pressure enough to drive the price lower. A resistance level is identified by a previous price high or peak on price trend chart as I did above.

However, if resistance is where selling overwhelms buying, that hasn’t happened yet. So, it can’t yet be “resistance.”

All analysis requires some common sense and plain critical thinking.

Now, here is the problem. People always want to know of a catalyst that could cause a prevailing price trend to change.

People love a good story.

The reason I believe we’ll see some resistance here, if we’re going to, is because of my momentum measures are signaling the trend is entering the upper end of its range.

The last time the S&P 500 got into this zone was the first week of June.

The S&P 500 declined about -7% afterward.

So, if we’re going to see some pull back, I expect it will come soon.

Afterwards, we’ll then see if it eventually trends back up to a new all time high, or if it instead reverses down into more of a downtrend.

This is how it works. It’s a Bayesian probability, where we update the possibilities as we go.

At each new stage of a trend, the expected value changes.

Let’s see how it unfolds from here.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

People tend to overreact and under-react to new information.

We observe it in the global capital markets more frequently than anywhere, and with immediate feedback.

So, those of us who are adept at identifying and monitoring directional trends in global markets have an advantage in researching trends of all kinds if our quantitative trend methods are robust, and our qualitative judgment and decision-making process is repeatable.

Intellectual skills that are associated with acquiring reliable information about nature are parts of the scientific process. Scientists of all kinds need skills like: communicating, observing, classifying, measuring, predicting, inferring, and researching.

Science isn’t just science, there’s also some art to it. I believe the first skills are more art, such as communicating, observing, classifying.

Many say investing and investment management is both art and a science. Some believe investment management is more art than science, others believe it’s more science than art. Quants try to make it more scientific than artistic.

I do a combination. I am Man + Machine.

The way I look at trends and how time series interact with each other is a robust process that may be applied to anything.

I don’t read articles in Bloomberg or The Wall Street Journal to hear the opinions of others to decide what I believe for myself. When I was a young rookie I did read a lot at first, as we all do, then learned the hard way to focus my efforts on my own original research and thinking.

I do best when I do my own work, as an independent thinker.

So, over the decades as a professional researcher, I first inspect the data to observe any trends and then make sense of it afterward. Sometimes my intention is for predictive analytics, other times it’s just prescriptive. predictive and prescriptive analytics. Predictive analytics provides us with the raw information for making informed decisions, while prescriptive analytics provides us with data-backed, evidence-based decision points that we can weigh against one another.

The scientific method is an empirical method of acquiring knowledge through careful observation, and applying rigorous skepticism about what is observed, realizing how cognitive assumptions and bias can distort how one interprets the observation.

Descriptive Analytics, applying data aggregation and data mining to provide observations andinsight into the past to answer:

“What has happened?”

Predictive Analytics, applying statistical models and probabilistic forecasting methods to understand the future and answer:

“What could happen?”

Prescriptive Analytics, applying simulation and testing algorithms to advise on possible outcomes and answer:

“What should we do?”

The Scientific Method and experimenting is a systematic approach to problem-solving and decision-making.

An algorithm may look something like this:

Problem —> Hypothesis —-> Prediction —-> Test Predictions —> Evaluation

We all have biases. All industries have biases. Sometimes these biases gave blindspots. Our biases that can narrow our vision and influence behavior and beliefs. It’s why in asset management, we often consult with researchers outside the industry to help avoid blind spots from industry bias. For example, the personal financial planning profession has a tendency to blindly say “balance your risks and rewards” and “balance your portfolios”, which is about the silliest things I’ve ever heard.

If you balance your risk and reward, you get symmetry on your statement.

If we want asymmetry, we have to skew the risk and reward positively.

It’s essential to identify blind spots, own them without being defensive, and adjust our behavior to avoid it.

MY OBSERVATIONS OF COVID 19

I have an advantage, because I observe COVID 19 trends and rates of change as it is, without any bias as to beliefs about the disease and such. That is, I’m just purely looking at the data we collect and feed into our systems for observation.

It’s like this:

I focus on; what has changed?

I look for extremes in levels, like new high or low breakouts.

I also monitor the rates of change. Fast breakouts are more likely to form an ongoing trend than slow.

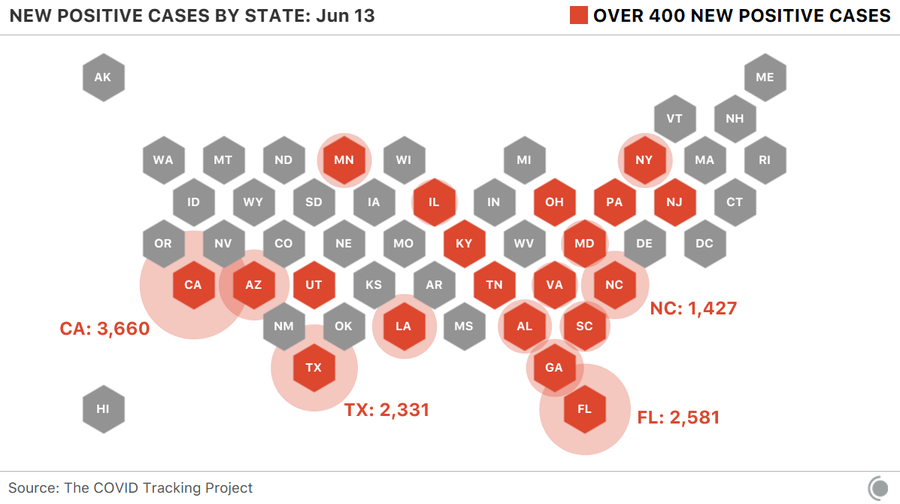

FLORIDA COVID 19 UPDATE

As COVID 19 and the mass quarantine strategy for suppressing the spread has become a political debate lately, so some of you may perceive what you are about to read that way.

Don’t.

I have no political bias about this whatsoever. My personal preference is to get past this virus as quickly as possible with as little human suffering as possible. Ignoring the data and facts doesn’t get us there. Exaggerating the data and facts doesn’t either. So, I suggest you try to see the trends for what they are, as I am.

My home state of Florida is now, unfortunately, trending in the wrong direction. I pointed it out with some fellow money manager friends last week of a potential breakout in the trend and it has since trended higher for a meaningful and material breakout. No one wants businesses to open and get back to normal more than me, but what is, is. The cases per day is in a strong uptrend. The prior high was 1575 on April 3rd and 1601 on May 16th. Yesterday was 2581. I hope to see this trend down.

NEW UPTREND IN FLORIDA CASES NOT DRIVEN BY NEW TESTING

The first hypothesis we think of is, well, maybe the uptrend in driven by an increase in testing. Naturally, increasing the absolute testing also should increase the number of positive tests. That isn’t the case. The high in testing was May 20th in Florida. The testing per day remains materially below that level according to the most recent data.

Keep in mind, the lower line is tests administered per day, so there is a lag between testing and the classification of a positive case. In fact, there are natural lags in all of this data. For example, I don’t expect to see the results of the protests until a week or two afterward to account for the lag in showing symptoms, going to get tested, and getting the test results. If there is any increase in the protesting areas, we’ll hear about it next week or later.

FLORIDA COVID 19 HOSPITALIZATIONS AT AN ALL TIME HIGH

Not much to add here. It is what it is.

I can try to make it seem better with a logarithmic based chart, which draws the chart in a way that two equal percent changes are plotted as the same vertical distance on the scale. It visually normalizes the rate of change. The good news is the rate of change overall is slowing. The bad news is this could look like an S-curve later, which would be typical of a spread.

By the way, here is the log chart of the new cases per day. We normally use a logarithmic chart scale for long term charts to normalize the data especially if I’m comparing it to something else where relative strength (rate of change) is measured. But here, we still see a breakout in rate of change. So, it’s a material breakout in my opinion, but I hope it breaks down.

Unfortunately, three of the new uptrends are in states were we have clients; Florida, California, and Texas. Next up is Texas.

TEXAS COVID 19 UPTREND

New cases in Texas is trending up to all time highs. I think Houston, Texas is now at risk of another stay-at-home order.

CALIFORNIA COVID 19 TREND

California new cases per day has trended up to the all time high again. It doesn’t seem to be in direct result of more testing per day, either.

ARIZONA COVID 19 CASES AT NEW HIGH

Arizona is at a high in new daily cases reported, but also in tests per day. The trouble in Arizona is the material new uptrend in hospitalizations.

The momentum in hospitalizations in Arizona is a real problem, and I’m using a logarithmic scale below, but it doesn’t help.

So, we are seeing new hospitalization highs in Texas, Arizona, and North Carolina. We’re showing Louisiana here as well for context, since it had an early COVID-19 outbreak.

We saw 3 states report more than 2,000 cases yesterday: California, Florida, and Texas. A picture speaks a thousand words.

COVID HAS HIT THE NORTH MUCH HARDER THAN THE SOUTH

But the South is now seeing a surge in cases…

And it doesn’t seem to be an increase in testing.

Can hospitalizations keep falling if cases are rising?

Because hospitalizations are rising rapidly in some Southern states.

I expect we’ll be hearing a lot about these new high breakouts in Arizona, Florida, Texas, and California. All of which, by the way, are the hottest and most humid states in the U.S., so much for the heat and humidity killing the virus.

What we have here is, a a notable uptrend across the South. I hope to see it fade, but based on what I’m seeing, it’s more likely to continue. Only time will tell.

If you are at risk, I recommend remaining cautious, wearing the dang mask, and treating this virus with respect.

Join 520 other subscribers

Speaking of the scientific method used for decision-making.

If you want to get as technical as possible, here’s some homework for the wannabe scientists and armchair mathematicians who really want to get into the maths of the matter. The virus has sparked a lot of important debates around the globe among though leaders. As researchers, we argue and debate our beliefs in hopes to gain new knowledge. One of the most heated public debates has been Taleb and Ioannidis.

The International Journal of Forecasting (IJF) is organizing a special section devoted to “Epidemics and forecasting with focus on COVID-19”. Based on their blog posts, John P. Ioannidis and Nassim N. Taleb will be given the opportunity to think of each other’s arguments about the COVID data and how to use it. Consequently, they will both be invited to write a full paper to better detail their views and why they think the opposite side’s views may not be adequate under the current circumstances. These opinion papers will then appear in the IJF, after scientific review by their peers. IJF should reserve the right to publish a closure based on this debate. This debate will not only allow us to better understand the points of view of the two great scientists but be also left as a guide for how to deal with future pandemics.

Nassim N. Taleb believes that all efforts and resources should be directed to halt its spread and reduce the number of infected and deaths without any concern about forecasting its future course as the uncertainty of doing so cannot be measured and the risks involved are highly asymmetric. See “On single point forecasts for fat tailed variable by Nassim Nicholas Taleb.”

John P. Ioannidis, on the other hand, claims that more reliable information is needed to make multiple billion-dollar decisions and that forecasting has failed us by being too pessimistic about the future growth of the pandemic and by exaggerating its negative effects. See “Forecasting for COVID-19 has failed”

Both of their observations are well worth a read.

In addition to the equity markets entering a higher risk level of a drawdown and volatility expansion, we now have a renewed risk of the scary COVID narrative driving more fear.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Surgeon General Jerome Adams said Sunday that this week could be the nation’s “hardest and saddest” thus far. “This is going to be our Pearl Harbor moment, our 9/11 moment, only it’s not going to be localized,” Adams said.

As a US Marine Corps Veteran myself, of course, calling this a WAR is in no way minimizing a real combat zone our great nations warriors have endured for generations. But this IS a WAR in my option, it’s just a very different kind of WAR against an invisible enemy. It’s a kind of asymmetric warfare, as opposed to the traditional combat threats. We are under attack right here in our own communities and it’s our turn to do the fighting, but the way we attack it isn’t the same as how it attacks us. The good news is, fighting and winning this WAR is relatively simple.

In US we have 12,844 deaths from coronavirus and 396,223 confirmed cases. The entire east coast is now red on the map from Coronavirus COVID-19 Cases Tracker by the Center for Systems Science and Engineering (CSSE) at Johns Hopkins University (JHU).

In Quantitative Technical Analysis of the Coronavirus COVID – 19 Trend I said I expect to see the speed of new Coronavirus COVID – 19 cases to increase exponentially, I’m going to start sharing my observations on it from the lens of a “quant” and a technical chartist. I was planning to have already shared some observations, but I found some issues in the state level data that have now been resolved. Of course, all of the data we are reviewing is deemed to be reliable but none of it is guaranteed. I believe it’s clear the US and the world were not well prepared for a pandemic of this magnitude, which is disappointing considering leaders like George W. Bush and Bill Gates warned of it years ago.

I’m concerned many American’s will become overwhelmed at the sheer speed of the growth of coronavirus in the next week. Although I’m seeing some evidence the rate of change has slowed as a result of “social distancing” and such, it’s still spreading very fast as expected. The key is to realize it is expected, so don’t be too alarmed. I’m going to share some charts for a visual of what is going on with the trend and rate of change. I’ll also share how we are combating it here at the Shell compound. If you haven’t already, I encourage your to read my prior observation Quantitative Technical Analysis of the Coronavirus COVID – 19 Trend since I”m not going to repeat myself here.

I’m taking a top down Global Macro approach to looking at the trends and momentum, just as I review price trends of global capital markets.

As you will see the data source noted in the charts, we are pulling in world and US data from Johns Hopkins Center for Systems Science and Engineering and for state level data from The COVID Tracking Project. I’ve also been monitoring other data sources such as the model referenced in a White House press briefing as the “Chris Murray Model,” which is IHME’s COVID-19 projections show demand for hospital services in each state. The demand for these services is expected to exceed capacity soon, so we’ll take a look at it. I’ve been in touch with quantitative analyst, data scientist, etc. all over the country discussing some of this so it’s been nice to see such solidarity as we enter the early stages of this battle. But, this WAR isn’t just going on here in the United States, it’s a pandemic all over the world and humans are all fighting it.

World Coronavirus Cases: 1.381 million for Apr 07 2020

Coronavirus (COVID-19) is a global pandemic that originated in Wuhan, China in 2019. The virus sparked a global economic slowdown because of various countries including China, Italy, and Iran having more than 1000 deaths within the first few months of the virus emerging. The virus also caused many countries to provide fiscal and monetary stimulus. For example, in the United States, the Federal Reserve conducted two surprise rates cuts to lower the Federal Funds rate to nearly 0%. Additionally, parts of the world implemented a complete lockdown of cities to prevent the spread of the virus. The Coronavirus pandemic eclipsed 10,000 cases on February 1, 2020, and 100,000 cases on March 6, 2020.

World Coronavirus Cases is at a current level of 1.381 million, up from 1.345M yesterday. This is a change of 2.67% from yesterday. I’m drawing the charts with a logarithmic scale to illustrate the trend as percentage moves for spacing, rather than number of cases, so a log scale emphasizes the rate of change in a way that linear scales do not.

Unfortunately, in the US, we are leading the world in the number of cases.

The rate of change and trend in China, where it originated, has supposedly slowed down. Here is China’s reported total cases and deaths.

If China is reporting their data accurately, we can see the cases reported per day and deaths per day have trended down the past few weeks.

When we compare data and directional trends, it’s sometimes useful to view a relative comparison to see who trends compare across countries, in this case. Below is the death rate of the world relative to China. The current death rate at the world level is 5.67% while China’s reported death rate has stabilized at 4% for weeks. We shouldn’t be alarmed by the death rate of other counties and around the world, however, since different countries have varying ages of population and health care. I expect to see some divergence.

The United STATES of America

Let’s look at the states. Keep in mind the data isn’t perfect. Since the Centers for Disease Control and Prevention hasn’t yet begun publicly releasing the number of people who have been tested, The COVID Tracking Project is pulling data from state health departments, which can vary in the way they report tests and infections. This COVID Tracking Project was launched out of The Atlantic to fill a major gap in publicly available COVID-19 testing data. Johns Hopkins University maintains a comprehensive case count, but no governmental or institutional source is publishing complete testing data—including not just identified cases, but how many people have been tested, and where. Without this data, we can’t make informed decisions or accurately communicate risks.

Which states have seen the most cases of coronavirus?

Here are the relative trends of New York, New Jersey, and Michigan on a log scale. Notice the rate of change is slowing.

I drew some trends lines to see the slope changing around April 1st in New York.

I put the New York number of tests administered, hospitalizations, and death rate on one chart.

New York is expected to reach its peak resource use tomorrow. I’m going to keep this observation high level and brief without getting into too much weeds, but the next image is from IHME’s COVID-19 projections. They show demand for hospital services in each state. The demand for these services is expected to exceed capacity. Tomorrow, New York is expected to have a hospital bed shortage of 12,476 beds and a shortage of 5,946 ICU beds. IHME predicts 5,664 ventilators will be needed. Keep in mind, this is their educated guess, so their projections may not prove accurate, but we’ll find out soon.

The numbers for All beds needed and All beds available include ICU beds.

All beds available is the total number of hospital beds available for COVID patients minus the average historical bed use.

ICU beds available is the total number of ICU beds available for COVID patients minus the average historical ICU bed use.

Invasive ventilators needed does not account for the number of ventilators available (ventilator capacity data are not available at this time).

Taking a closer look at the bell shaped curve in the chart, notice there is a colored range around the dotted lines. It’s like the cone of uncertainly we see late summer for hurricanes here in Florida. It shows a range of possible outcomes.

Uncertainty is the range of values that is likely to include the correct projected estimate for a given data category. Larger uncertainty intervals can result from limited data availability, small studies, and conflicting data, while smaller uncertainty intervals can result from extensive data availability, large studies, and data that are consistent across sources. The model presented in this tool has a 95% uncertainty interval and is represented by the shaded area(s) on each chart. The range of outcomes is necessarily wide because of the asymmetric uncertainty. The truth is; we just don’t have a lot of data and information yet, so we make the best of what we do have.

A major concern is the shortage of hospital beds and ventilators, so it’s essential to fight this WAR by simply staying at home and distancing from others for a while. We have clients in New York, so I hope everyone is hunkered down to slow the spread.

Next up is my current home state of Florida. I included all of the data expect the death rate and I see a lot of uptrends.

The death rates are around 2% to 4% at this point. I included the US, New York, and Florida.

Going back to hospital resource use, here is the projections for the US. The country is expected to reach peak resource use a week from now. According to the projections, there will be a significant shortage of beds and ventilators. I don’t want to be alarming, this simply tells us the best way to fight this WAR is to avoid it. We don’t want to be the one needing a ICU bed or ventilator, so we have a choice to avoid it by distancing.

I’m most concerned about Florida. Not because I live in Tampa Bay, but because we have an older population of retirees across the state. I also see evidence of strong infections in Miami-Dade, thanks to spring breakers from New York.

In Florida, we were issued a stay at home order on April 3rd and non-essential services are closed. Florida is expected to reach peak resource use two weeks from today on April 21st, later than most of the country. The good news is, if their projections are accurate, we don’t have as much of a shortage probability here. I supposed Gods waiting room has more beds and such. But we are expected to have a shortage of ventilators.

The possibility band for Florida, however, is tall, which means it could be much higher.

Since we’re looking at Florida, this brings me to another data source I’ve been monitoring. As I discussed in more detail in my last post on COVID – 19, one of the most interesting data I’ve seen is the U.S. health map from Kinsa smart thermometers. The Cumulative Atypical Illness map shows the amount of cumulative unexpected illness, expressed as additional share of the population affected by influenza-like illness, above the expected values.

This is how much influenza-like illness above the normal expected levels they have detected since March 1st. The hot spots are the northeast, Michigan, and south Florida. But, we’re now seeing more red ares all over.

When someone who is using a Kinsa smart thermometer with their phone to track the data, it shows up as atypical when their fever is above what is expected.

The time series chart allows us to compare Kinsa’s observations of the influenza-like illness level in the U.S., in orange and red, against where we’d expect them to be, in blue, and see how that relationship has changed over the past few weeks. The red zone were I drew the arrow below was an early warning of what is likely to be Coronavirus.

The good news is the observed data has trended below expected now and we attribute it to social distancing.

Inder Singh is the founder & CEO of Kinsa. Kinsa’s mission is to create a real-time map of human health to track — and curb — the spread of infectious illnesses Inder wrote an article on Medium last week titled “Your Sacrifices are Saving Lives” showing how their research finds social distancing is working. If you need to see the evidence, I encourage you to read it.

I don’t like what I’m seeing here in Florida. Take a look at how high the atypical illness trend was recently. The slope was high and steep. At its peak on March 18th, the atypical illness detected was about 7 and the expected range was 2.5, it was about 300% higher that expected. This data tends to be a week or two ahead of new cases.

Miami-Dade, Broward, Palm Beach County, Duval, and Orange county look similar.

So, the Coronavirus is just getting ramped up and will spread more in the coming days and weeks. It’s probably going to be alarming to many, especially the deaths.

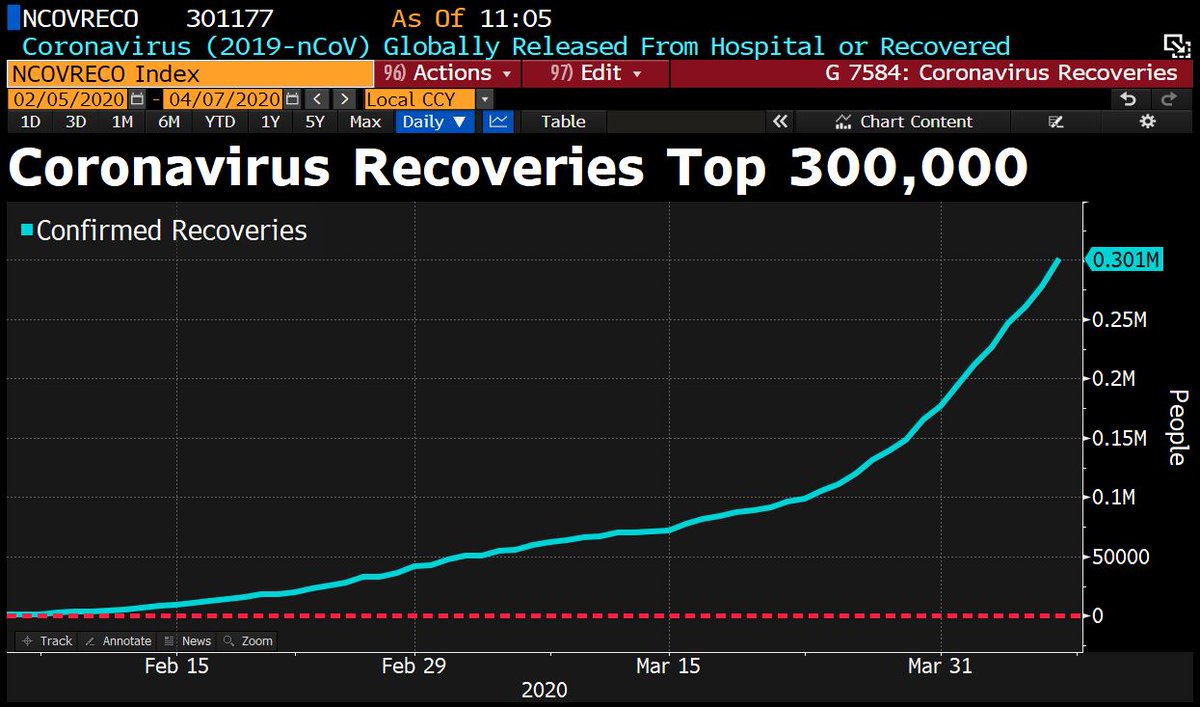

Some good news is 300,000 have recovered.

WE ARE AT WAR

If you want to win this WAR, it’s a matter of distancing and treating everything like it’s infected. Just like the markets, people initially underreact, then they panic because they underreacted, then they overreact.

It reminds me of Maslow’s Hierarchy of Needs as we are all focused on the bottom two right now, no matter who you are or how much money we have. Health, air, water, employment, and personal security are top of mind.

Are we wining the WAR?

David Ingles at Bloomberg shared this chart and points out one ratio to watch is recoveries to infections. A rising trend is good, a declining trend is bad.

OUR BATTLE PLAN

Here is what we are doing at Camp Shell.

We had already started stocking extra bottled water and food, which we would have done anyway in preparations for hurricane season.

It’s mainly been business as usual for us. The only thing different is we aren’t going out to eat with friends or the grocery store. I haven’t left in a car in two weeks, but we still do our daily walk with the dog and cycle for exercise.

We have gloves, masks, and even suits if necessary.

We’ve stopped bringing the mail and packages in through the front door and instead take them into the garage. We put on gloves to handle them and open them. We open all mail and packages at the trash can in the garage and then wipe it all down with spray and then clean off our rubber gloves. We treat it like it’s infected with a deadly virus. Better safe than sorry. We throw away the mail after anything important is scanned using our iPhone and the Dropbox scanner. Nothing comes in without being wiped down. When we need groceries, we order it online from Publix and they deliver. We handle the groceries the same – nothing enters Camp Shell without being wiped down.

It’s very simple.

If we do this and keep social distancing in the days and weeks ahead, we’ll likely avoid the enemy and win the WAR.

This is a relatively easy WAR to win if you want to win it. As with any combat situation, find the weak link and make is strong.

I hope you are taking this seriously and doing the same.

WE WILL WIN THIS.

It reminds me of US Marine Recon: Swift, Silent, and Deadly.

SEMPER FI

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.