In the last observation I shared about the stock market, “The stock market trends up with momentum,” we saw the stock market reverse back up with strong momentum. The S&P 500 stock index had declined about -7% from its high, then reversed back up 3%. I discussed how investor behavior and sentiment drives market prices. Many investor sentiment measures signaled investor fear seemed to be in control, driving down prices. Volatility had spiked and then started to settle back down. Many individual stocks in the S&P 500 had declined enough to signal shorter-term downtrends, but then they reversed up. I closed by saying:

In summary, today was a strong upward momentum day for the stock market and most stocks participated in the uptrend. After sharp declines like we’ve seen this month, the stock market sometimes reverses up like this into an uptrend only to reverse back down to test the low. After the test, we then find out if it breaks down or breaks out.

One day doesn’t make a trend, but for those who are in risk taker mode with stocks, so far, so good.

The part I bolded with italics has turned out to be the situation this time.

Below is a year to date price trend of the S&P 500 stock index. As of today, my observation “the stock market sometimes reverses up like this into an uptrend only to reverse back down to test the low” is what we are seeing now.

I’ve always believed investment management is about probability and possibilities, it’s never a sure thing. The only certainty is uncertainty, so all we can do is stack the odds in our favor. As I said before, “After the test, we then find out if it breaks down or breaks out.”

The positive news is, investor sentiment measures are reaching levels that often precede short-term trend reversals back up.

The bad news is if the current trend becomes a bigger downtrend these indicators will just stay at extremes as long as they want. We have to actively manage our exposure to loss if we want to avoid large losses, like those -20% or more that are harder to overcome.

Down -10% is one thing, down -20% is another. Any investor should be willing to bear -10% because they will see them many times over the years. Only the most passive buy and hold investors are willing to bear the big losses, which I define as -20% or more.

Nevertheless, I see some good news and bad, so here it is. I’ll share my observations of the weight of the evidence by looking at relatively simple market indicators. I don’t necessarily make my tactical decisions based on this, but it is instead “market analysis” to get an idea of what is going on. Observations like this are intended to view the conditions of the markets.

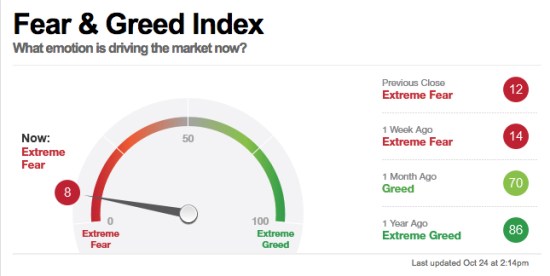

Fear is the dominant driver.

The Fear & Greed Index tracks seven indicators of investor sentiment. When I included it a week ago, it was at 15, which is still in the “Extreme Fear” zone. The theory is, the weighting of these seven indicators of investor sentiment signals when fear or greed is driving the market. Clearly, fear is the dominant driver right now.

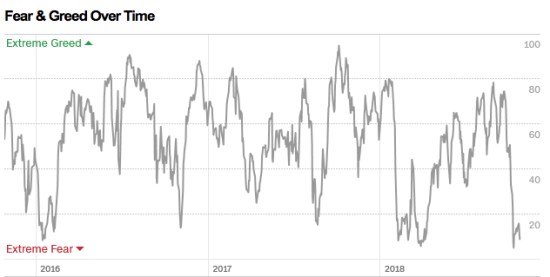

At this point, we can see investor sentiment by this measure has now reached the low level of its historical range. In this chart, we can see how investor sentiment oscillates between fear and greed over time in cycles much like the stock market cycles up and down.

I believe investor behavior is both a driver of price trends, but investors also respond to price trends.

- After prices rise, investors get more optimistic as they extrapolate the recent gains into the future expecting the gains to continue.

- After prices fall, investors fear losing more money as they extrapolate the recent losses into the future expecting them to get worse.

Investor sentiment and price trends can overreact to the upside and downside and the herd of investors seems to get it wrong when they reach an extreme. We observe when these kinds of indicators reach extremes, these cycles are more likely to reverse. It is never a sure thing, but the probabilities increase the possibility of a reversal. But, since there is always a chance of a trend continuing longer in time and more in magnitude, it is certainly uncertain. Since there is always a chance of a bad outcome, I have my limits on our exposure to risk with predetermined exits or a hedge.

Speaking of a hedge.

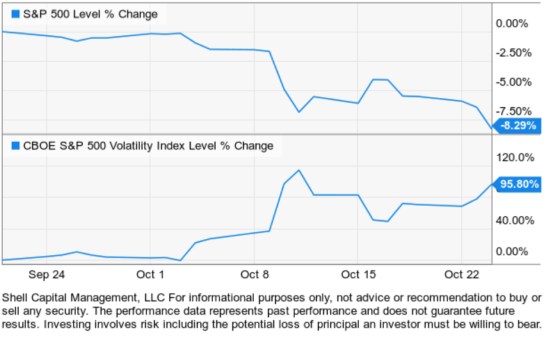

I started pointing out my observation several weeks ago of a potential volatility expansion. If you want to read about it, most of the past few weeks observations have included comments about the VIX volatility index. Over the past few days, we’ve observed a continuation in the volatility expansion.

Implied volatility has expanded nearly 100% over in the past 30 days.

As a tactical portfolio manager, my first focus is risk management. When I believe I have defined my risk of loss, I become willing to shift from risk manager to risk taker. I share that because I want to point out the potential for hedging with volatility. Rather than a detailed exhaustive rigorous 50-page paper, I’m going to keep it succinct.

My day job isn’t to write or talk about the markets. I’m a professional portfolio manager, so my priority is to make trading and investment decisions as a tactical investment manager. I’m a risk manager and risk taker. If I never take any risk, I wouldn’t have any to manage. The observations I share here are just educational, for those who want to follow along and get an idea of how I see things. I hope you find it helpful or at least interesting. It’s always fun when it starts new conversations.

To keep the concept of hedging short and to the point for my purpose today, I’ll just share a simple chart of the price trend of the stock index and the volatility index over the past 30 days. The stock index has declined -8.3% as the implied volatility index expanded over 95%. You can probably see the potential for a hedge. However, it isn’t so simple, because these are just indexes and we can’t buy or sell the VIX index.

The purpose of a hedge is to shift the risk of loss from one thing to another. The surest way to reduce the possibility of loss is to simply sell to reduce exposure in the thing that is the risk. That’s what I do most of the time. For example, when I observed a potential volatility expansion, I reduced my exposure to positions that had the possibility of loss due to increased volatility. Once prices fall and volatility contracts, maybe we increase exposure again to shift back to risk-taking. If we take no risk at all, we would have no potential for a capital gain. So, tactical portfolio management is about increasing and decreasing exposure to the possibility of gain and loss. If we do it well, we create the kind of asymmetric risk/reward I aim for.

So, any hedging we may do is really just shifting from one risk to another, hoping to offset the original risk. Keep in mind, as I see it, a risk is the possibility of loss. I’ll share more on hedging soon. I have some observations about hedging and hedge systems you may find interesting.

Most stocks are participating in the downtrend. Below is an updated chart of the percent of the stocks in the S&P 500 that are above their 50-day moving average. If you want to know more about what it is, read the last observations. The simple observation here is that most stocks are declining.

Much like how we saw investor sentiment cycle and swing up and down, we also see this breadth indicator oscillate from higher risk levels to lower risk levels.

- After most stocks are already in uptrends, I believe the risk is higher that we’ll see it reverse.

- After most stocks have already declined into downtrends, it increases the possibility that selling pressure may be getting closer to exhaustion.

The good news is, at some point selling pressure does get exhausted as those who want to sell have sold and prices reach a low enough level to bring in new buying demand.

That’s what stock investors are waiting for now.

These are my observations. I don’t have a crystal ball, nor does anyone. I just predetermine my risk levels in advance and monitor, direct, and control risk through my exits/hedging how much I’m willing to risk, or not. We’ll just have to see how it all unfolds in the days and weeks ahead.

Only time will tell if this is the early stage of a bigger deeper downtrend or just another correction within the primary trend.

I hope you find my observations interesting and informative.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

The observations shared on this website are for general information only and are not specific advice, research, or buy or sell recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. Use of this website is subject to its terms and conditions.

Pingback: To Know Where You’re Going, Look at Where You’ve Been: The 2018 Year in Review « ASYMMETRY® Observations