ASYMMETRY® Observations are Mike Shell’s observations of investor behavior causing directional price trends, global macro, tactical ETF trading, momentum stock trading, hedging, volatility trading, and risk management that creates asymmetric investment returns. An asymmetric return profile is a risk/reward profile with a positive asymmetry between profit and loss. Mike Shell is the founder of Shell Capital Management, LLC and the portfolio manager of ASYMMETRY® Global Tactical

Macroeconomics is a branch of economics dealing with the performance, structure, behavior, and decision-making of an economy as a whole.

Macroeconomics is the part of economics focused on the big picture: analyzing economic phenomena such as interest rates, growth, unemployment, and inflation. Macro is in contrast with microeconomics, the study of the behavior of individual markets, workers, households, and firms. Macroeconomic phenomena are the product of all the microeconomic activity in an economy.

Global is related to, or involving, the whole world, not just one country or state.

Global Macroeconomics, or Global Macro, then, is looking at the whole world for trends and behavior of big picture trends.

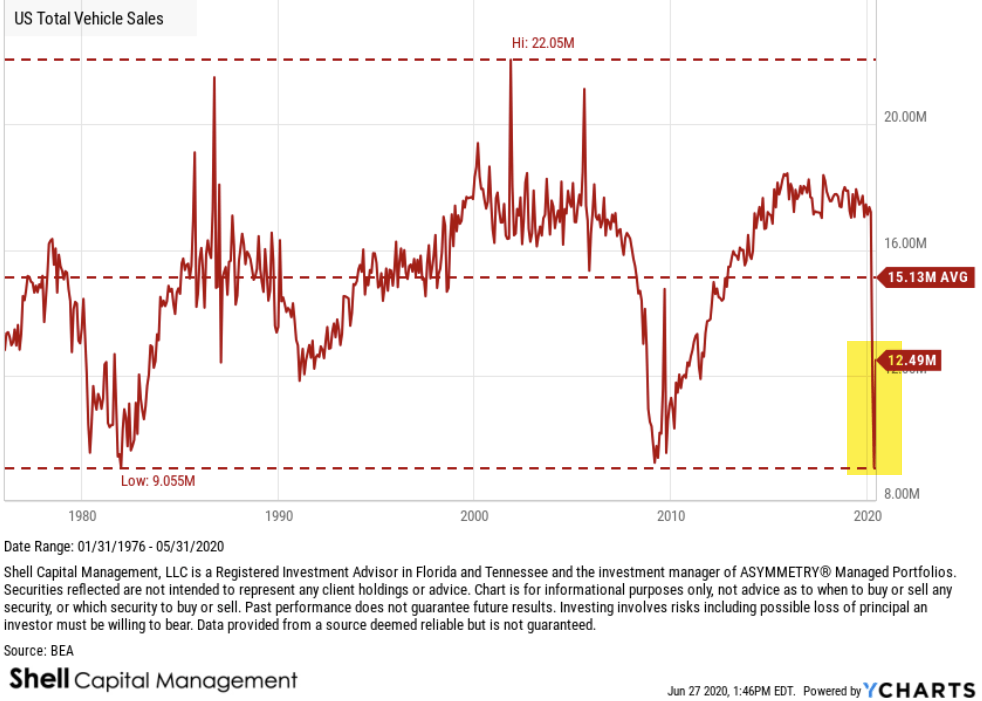

US Total Vehicle Sales measures the total number of auto, light truck, and heavy truck sales in the US and helps gauge how consumers are spending their discretionary income. In the chart, we can visually see the trends in car and truck sales going back 43 years.

US Total Vehicle Sales bottomed at prior lows, and is now trending back up.

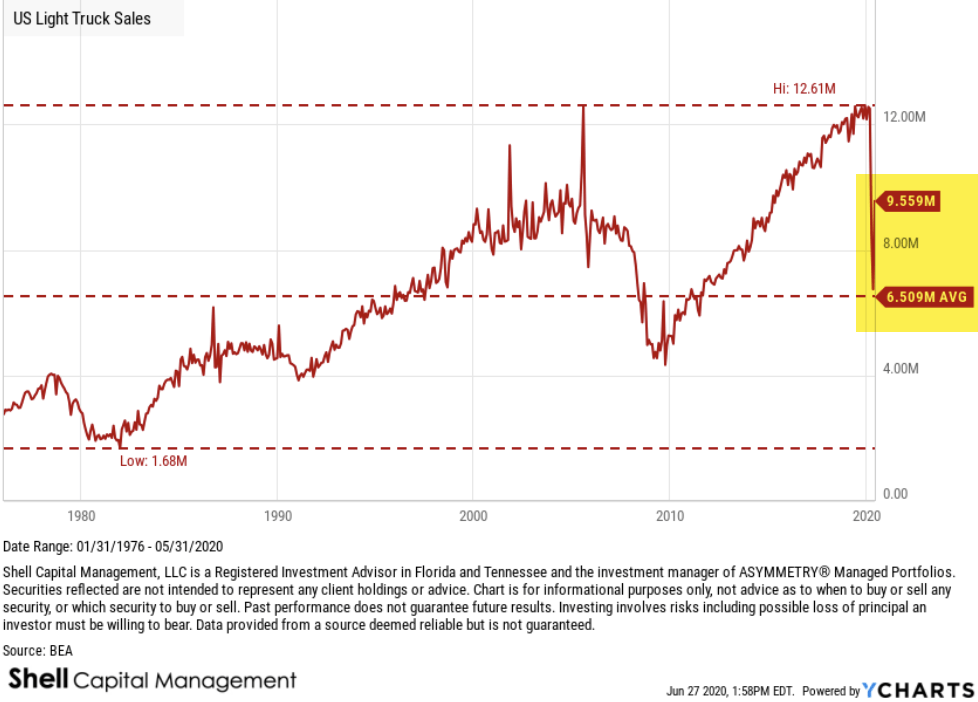

US Light Truck Sales is part of total sales and at a current level of 9.6 million, it’s up from 6.7 million last month and down from 12.57 million one year ago.

US Light Truck Sales has been in an overall uptrend the past four decades, and it reverted to the long term average, but is recovering. US Light Truck Sales is up 41.68% from last month, and -23.96% from one year ago.

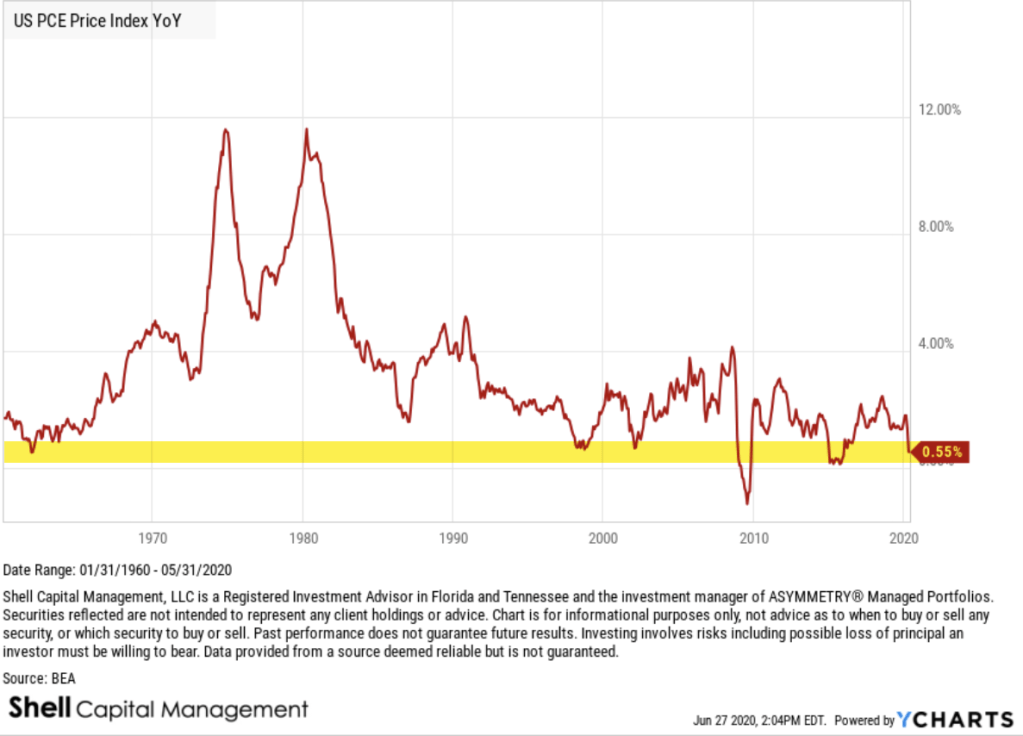

Personal Consumption Expenditures Price Index (PCE) is a measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services. The PCE price index is known for capturing inflation (or deflation) across a wide range of consumer expenses and reflecting changes in consumer behavior. The PCE price index, released each month in the Personal Income and Outlays report, reflects changes in the prices of goods and services purchased by consumers in the United States. Quarterly and annual data are included in the GDP release.

Personal Consumption Expenditures Price Index (PCE) Year over Year is is at 0.55%, compared to and 1.38% last year (a decline of 60%) and is materially lower than the long term average of 3.25%.

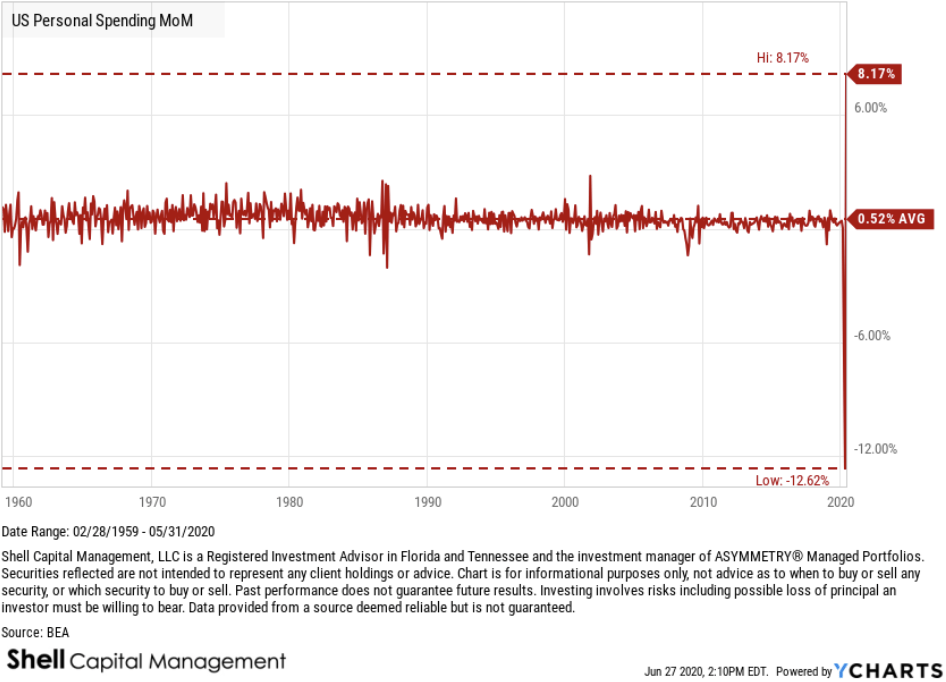

US Personal Spending Month over Month is at 8.17%, compared to -12.62% last month and 0.44% last year. US Personal Spending is now higher than the long term average of 0.52%. The chart shows this data was historically more stable, but we’ve observe some extreme outlier trends this year never seen in the last 60 years.

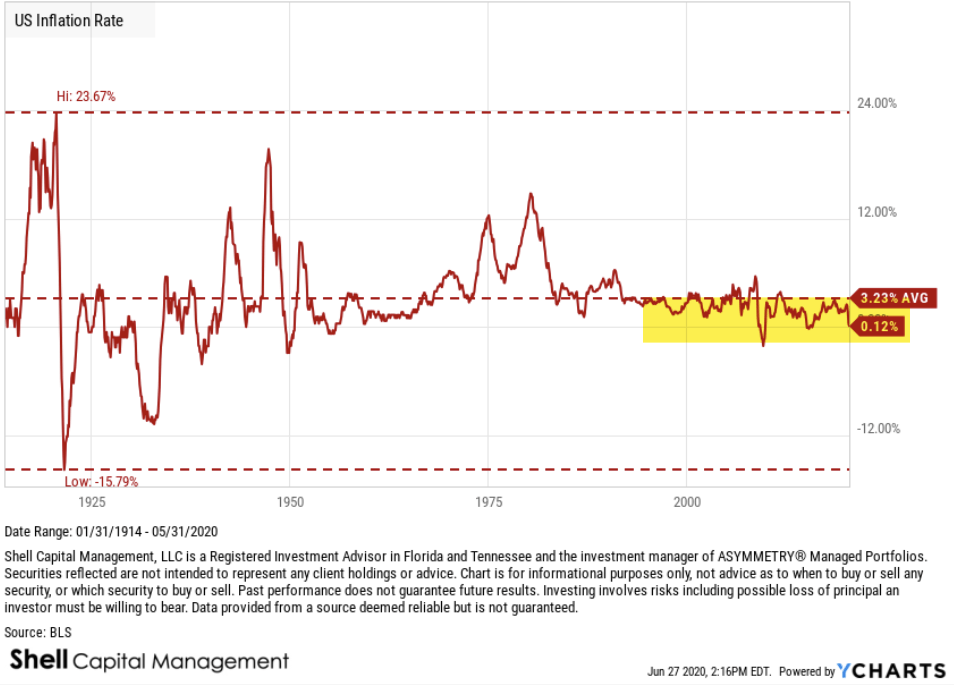

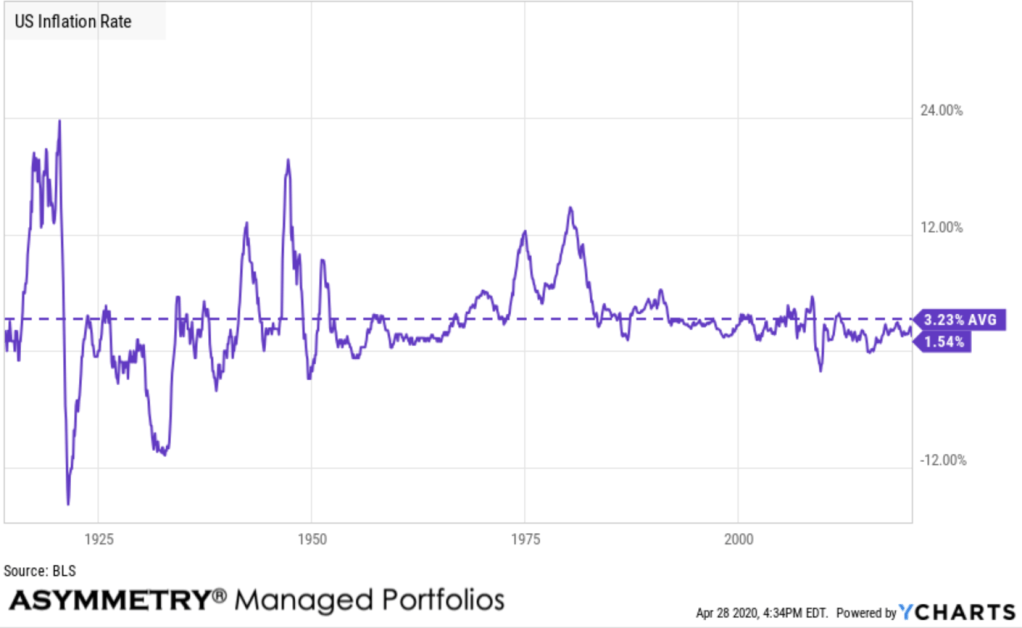

The US Inflation Rate is the percentage in which a chosen basket of goods and services purchased in the US increases in price over a year. Inflation is one of the metrics used by the US Federal Reserve to gauge the health of the economy. Since 2012, the Federal Reserve has targeted a 2% inflation rate for the US economy and may make changes to monetary policy if inflation is not within that range. A notable time for inflation was the early 1980’s during the recession. Inflation rates went as high as 14.93%, causing the Federal Reserve led by Paul Volcker to take dramatic actions.

US Inflation Rate is at 0.12%, compared to 0.33% last month and 1.79% last year. This is disinflation, which is a decrease in the rate of inflation. Disinflation is a slowdown in the rate of increase of the general price level of goods and services in a nation’s gross domestic product over time. Inflation has mostly trended below the long term average of 3.23% for years, but is extremely low at 0.12%. We could be a risk of deflation, which occurs when the inflation rate falls below 0%.

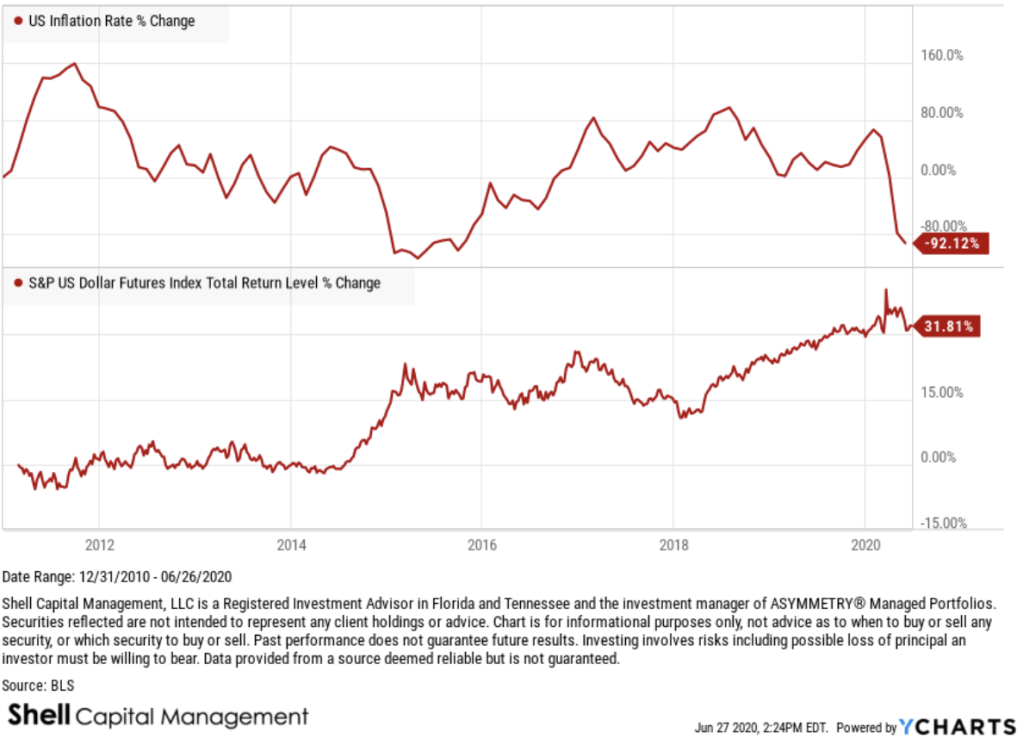

Inflation reduces the value of a currency over time, but sudden deflation increases it. As inflation is declining, the US Dollar is trending up.

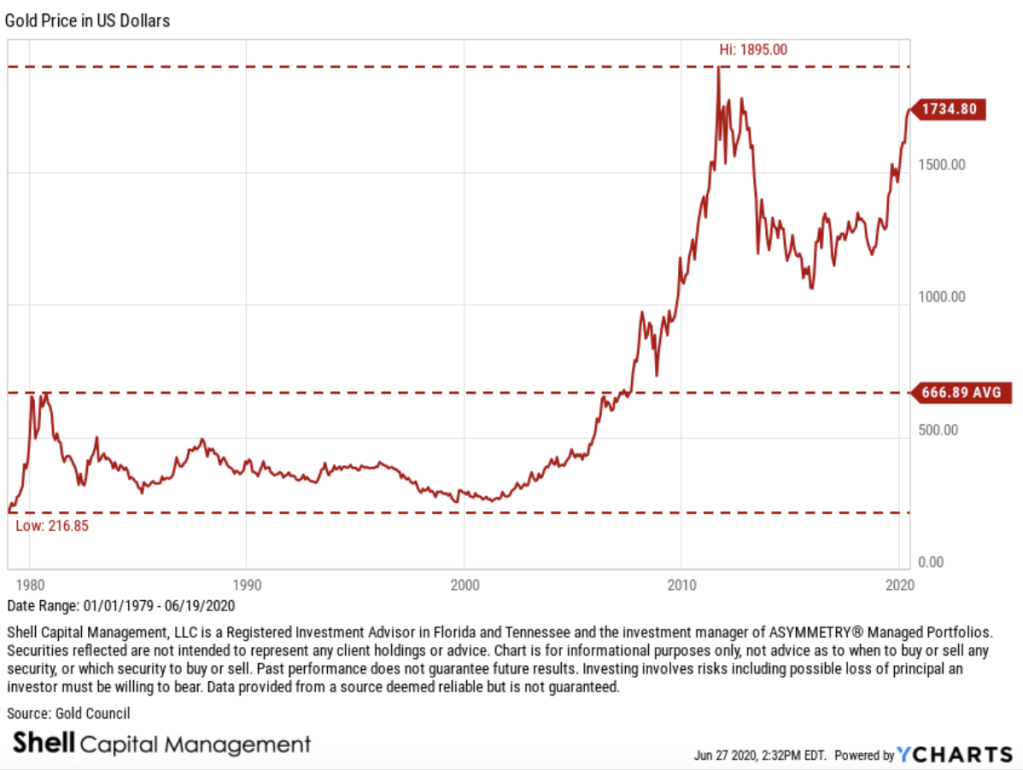

When we think of macroeconomics trends like inflation and the US Dollar, we also think of gold. Here is Gold, priced in US Dollars. The Gold Price in US Dollars measures the cost in US Dollars for a Troy Ounce of gold. Gold can be seen as a “safe haven” investment since it is a tangible investment. Gold is also believed to be a hedge against inflation, which is why it reached as high as $1,895 per troy ounce in 2011 when inflation trended higher.

Gold is in an uptrend.

Inflation and interest rates are the primary return driver of stocks and bonds as well as some commodities and currencies.

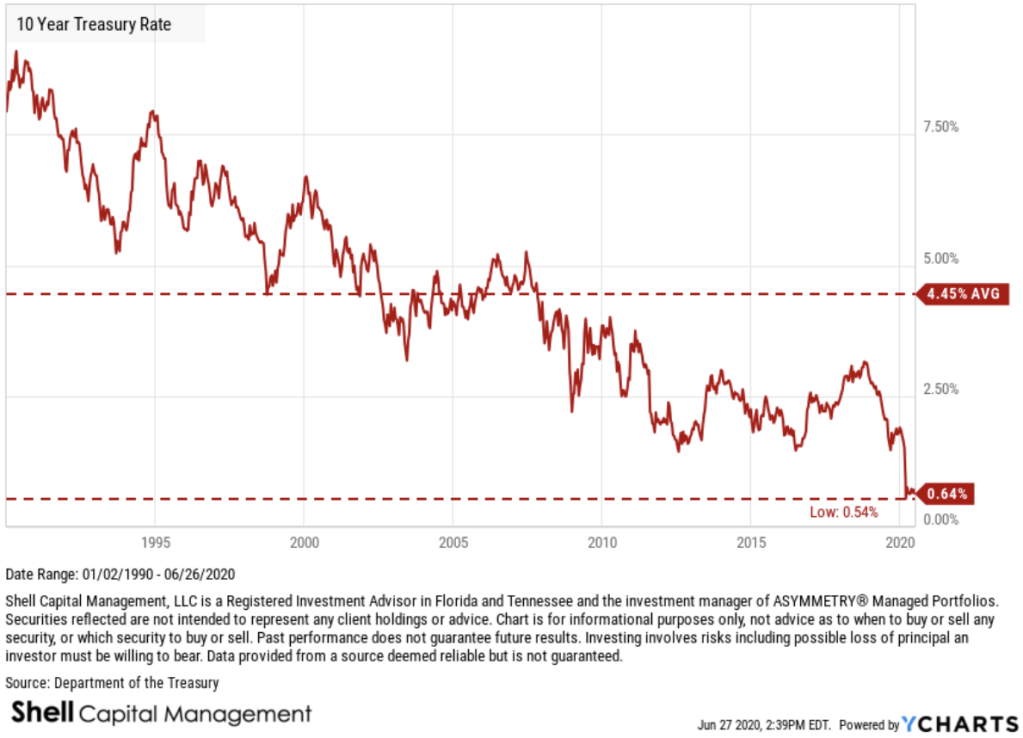

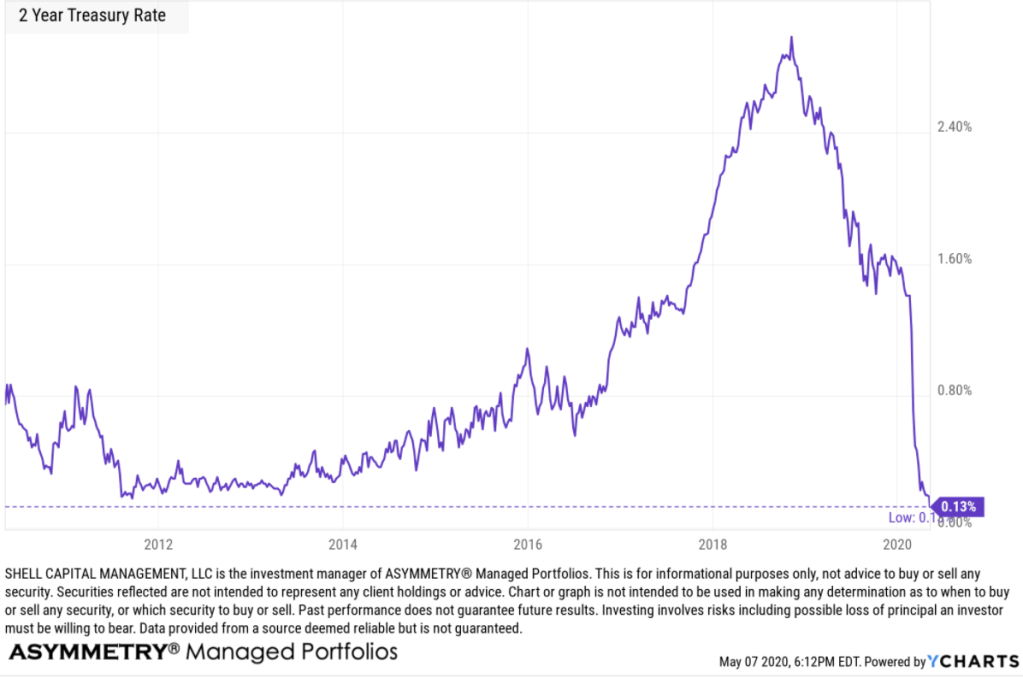

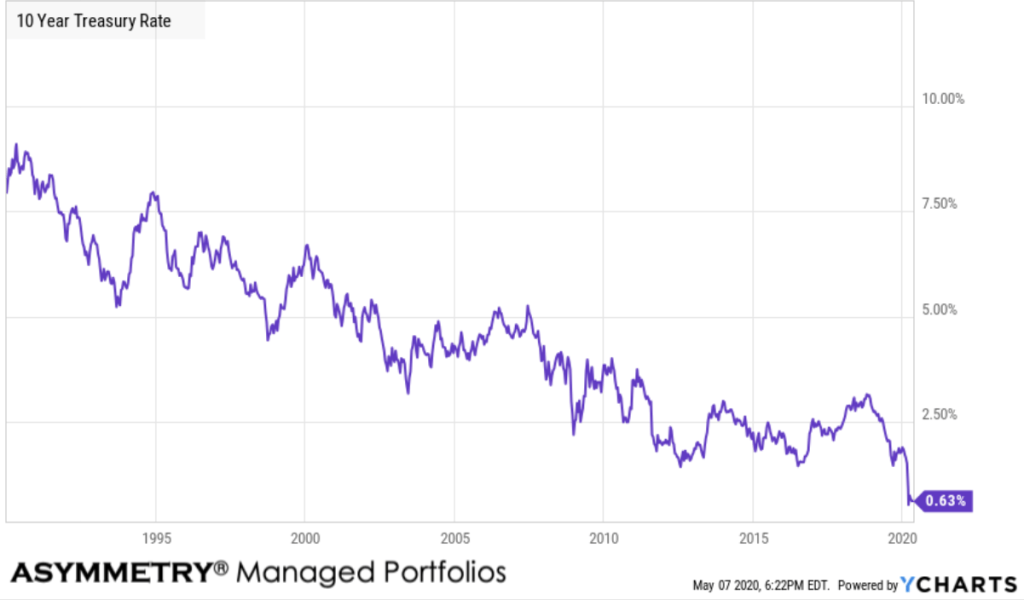

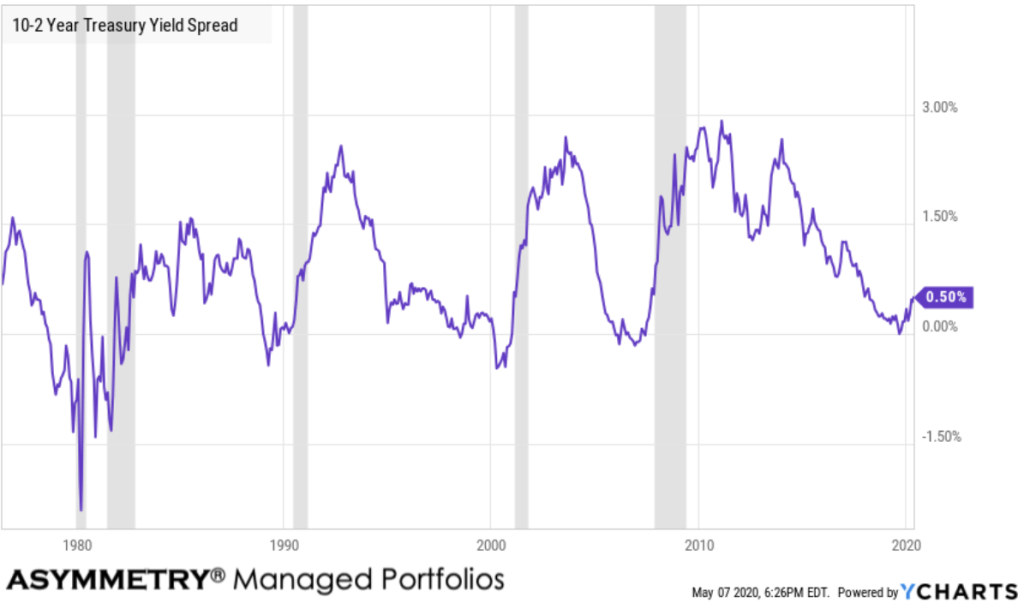

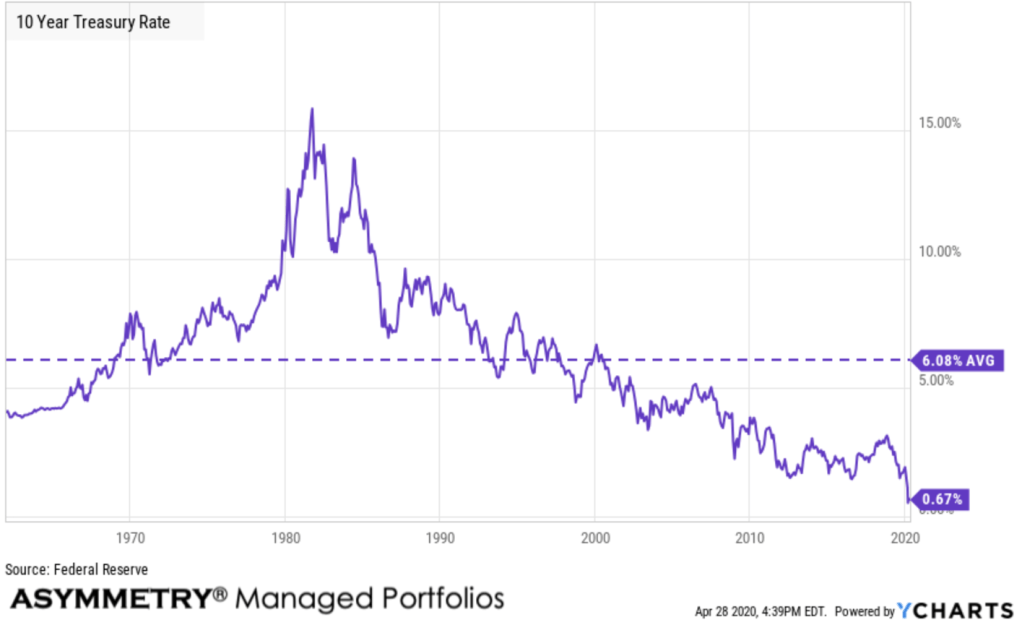

The 10 Year Treasury Rate is the yield earned by investing in a US government issued treasury security that has a maturity of 10 years. The 10 year treasury yield is the longer end of the yield curve. Many analysts use the 10 year yield as the “risk free” rate when valuing the markets or an individual security. Historically, the 10 Year treasury rate reached as high as 15.84% in 1981 as the Fed raised benchmark rates in an effort to contain inflation.

10 Year Treasury Rate is the lowest it has been the past 30 years, currently at 0.64%, compared to 2.01% last year, and is significantly lower than the long term average of 4.45%.

We all know that past performance is no guarantee of future results, and the bond market expected return is a fine example. One thing that is essential for investors to understand is the long term bond returnswill not repeat their pastperformanceover the long term.

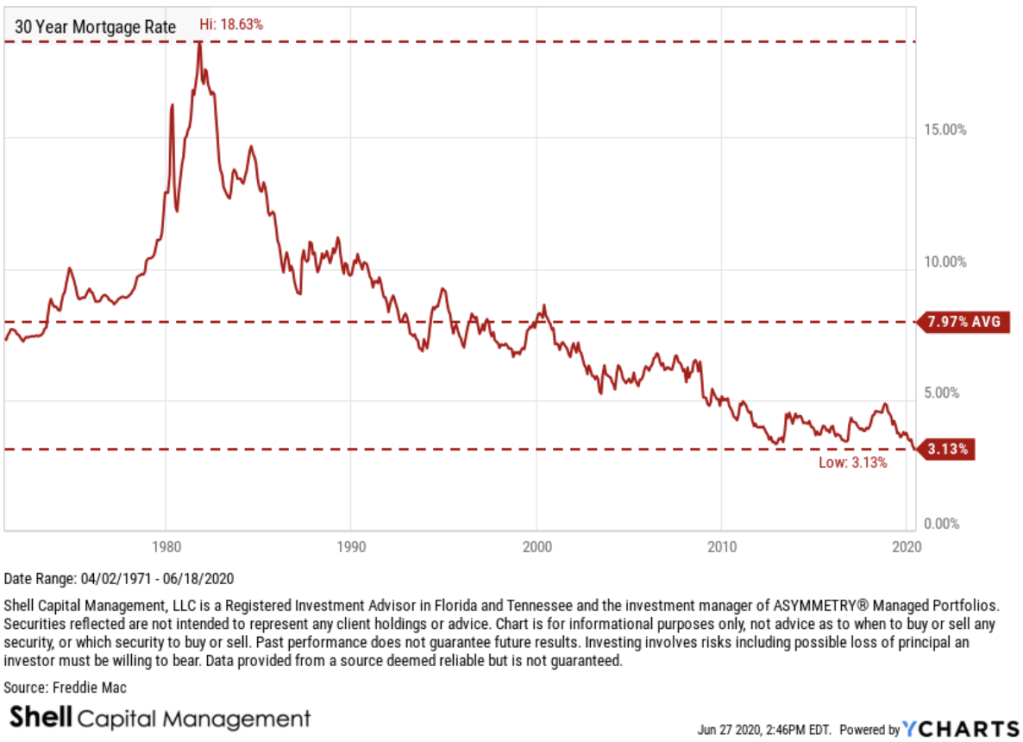

The directional trend of interest rates like the 10 Year Treasury Rate are a driver of other rates, such as mortgage rates.

The 30 Year Mortgage Rate is the fixed interest rate that US home-buyers would pay for a 30 year mortgage. Historically, the 30-year mortgage rate has trended as high as 18.6% in 1981, and up until now has trended down as low as 3.3% in 2012.

The 30 Year Mortgage Rate is at 3.13%, the lowest in 48 years, compared to 3.82% last year, and less than half of its 7.97% long term average.

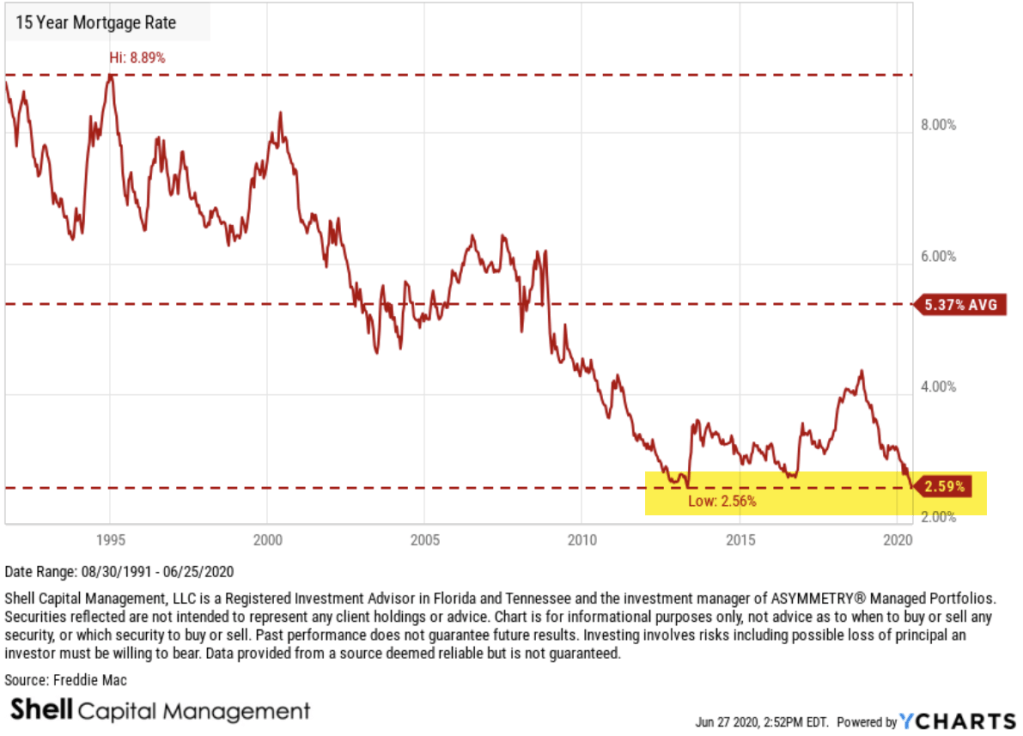

The 15 Year Mortgage Rate is trending down low enough to double tap its all time low at 2.59% reached in May 2013, which is significantly lower than the long term average of 5.36%.

That’s all for now.

Don’t miss out! Stay informed and sign up for an email of new ASYMMETRY® Observations, including some that may not be posted here.

Join 520 other subscribers

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

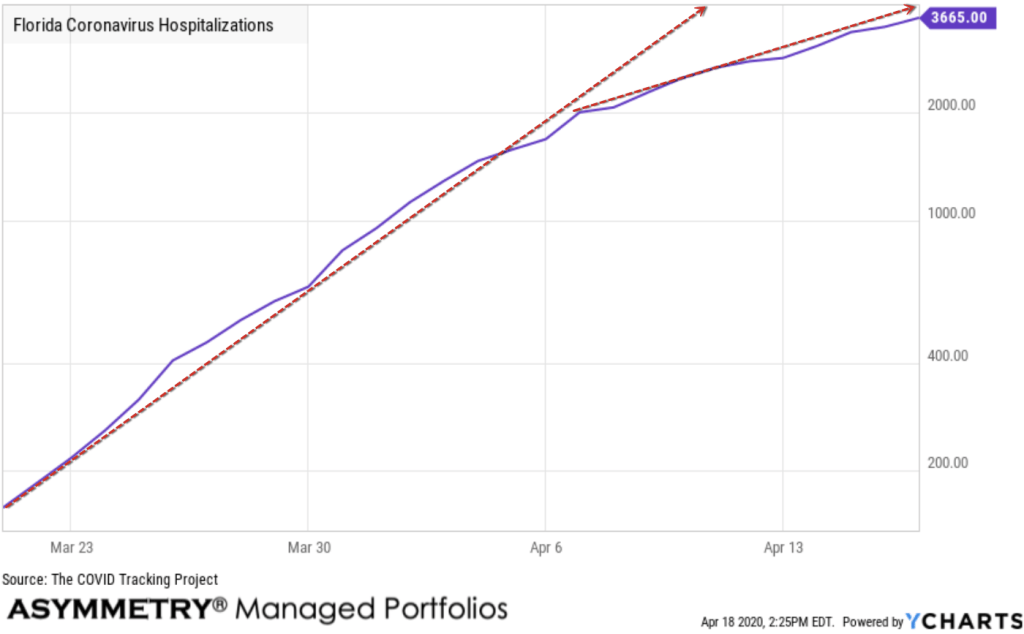

Unfortunately, we’ll see a pause in reopening as hospitalizations trend up.

Hospitalizations have much further to rise, but they shouldn’t increase as much as cases.

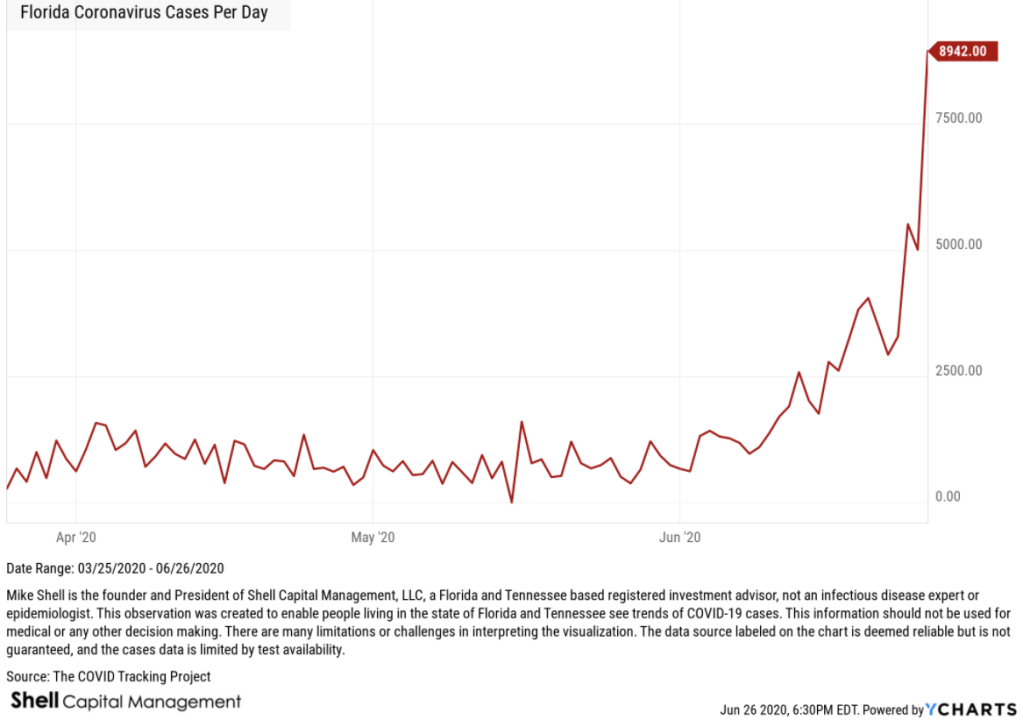

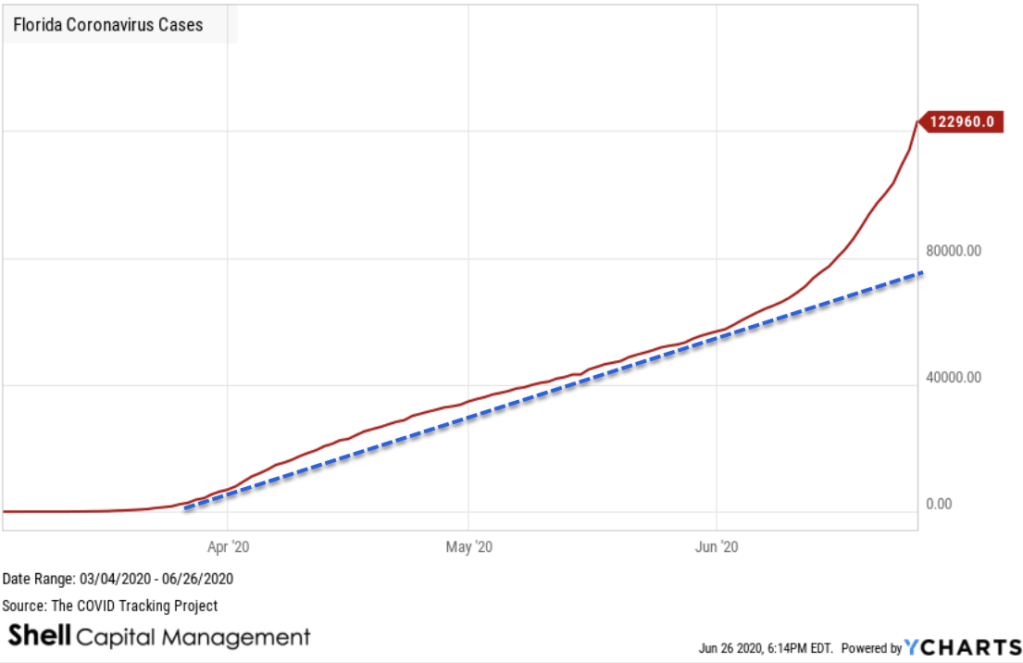

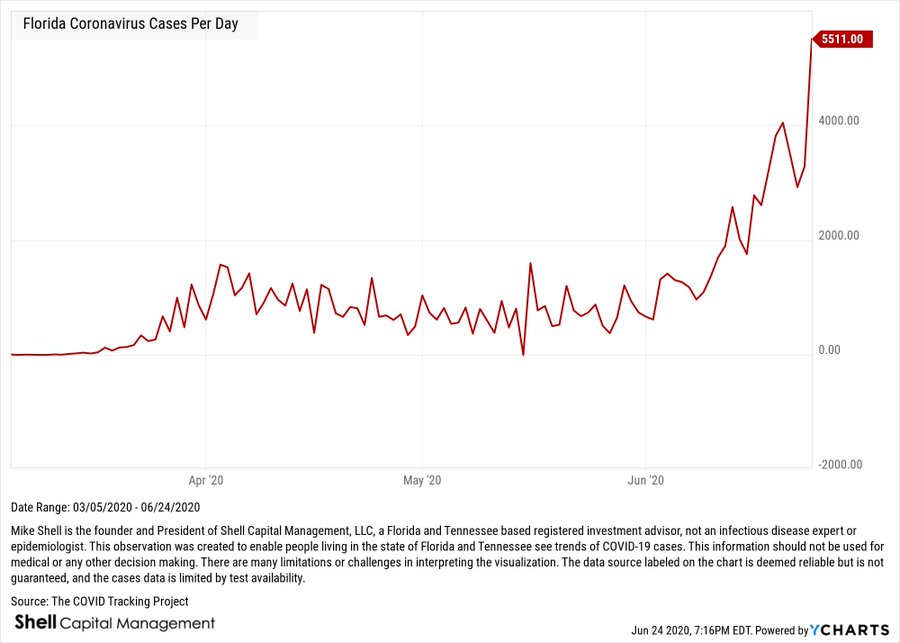

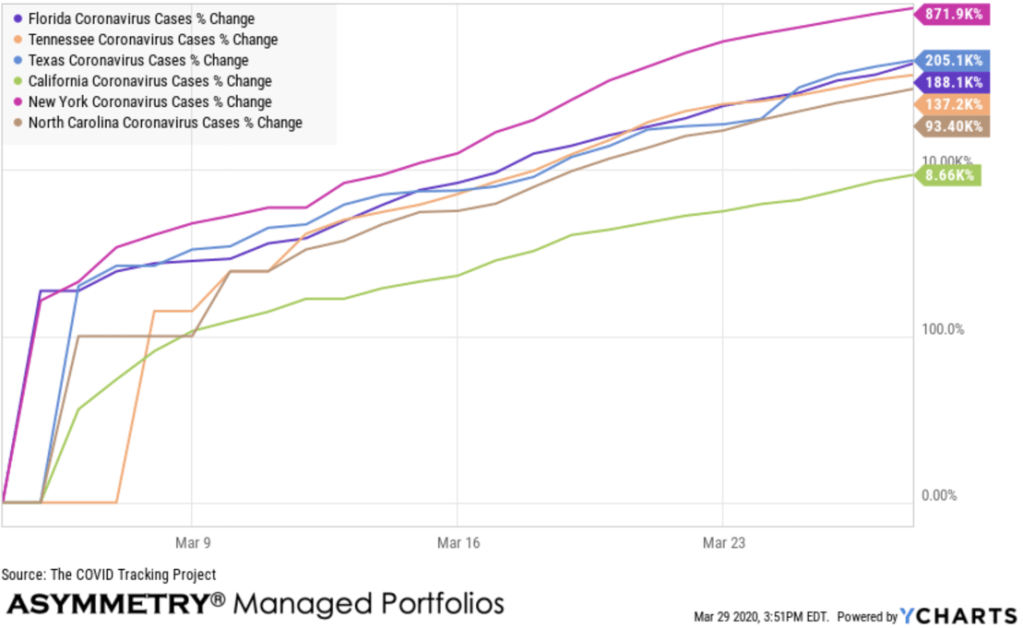

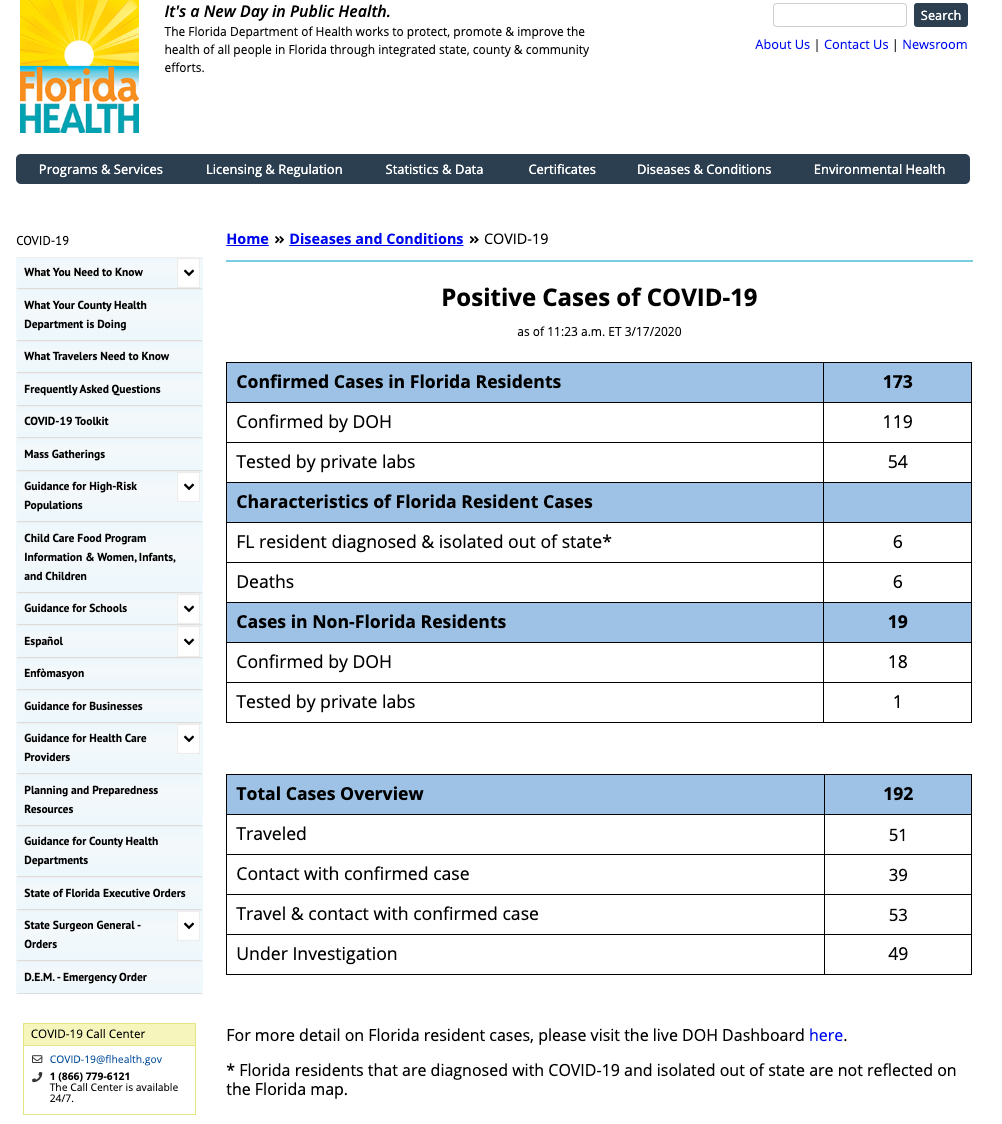

I just got an updated data feed for today. Florida Coronavirus Cases is at a current level of 122,960, up from 114,018 yesterday, and a change of 7.84% from yesterday. Cases increased by 205% this week and 1,050% over the past 30 days.

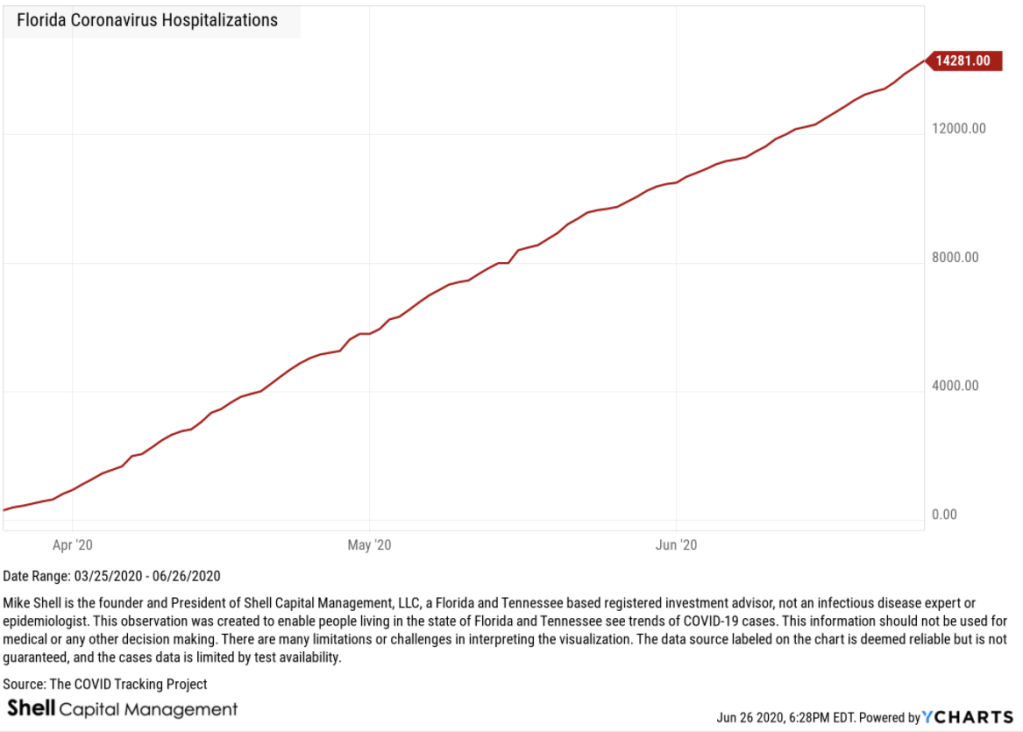

Florida COVID hospitalizations continue in a 45-degree uptrend.

I continued to reiterate the direction of a trend is important, but so is the rate of change. This new rising rate of change isn’t what we want to see and is a derivative of the reproduction rate.

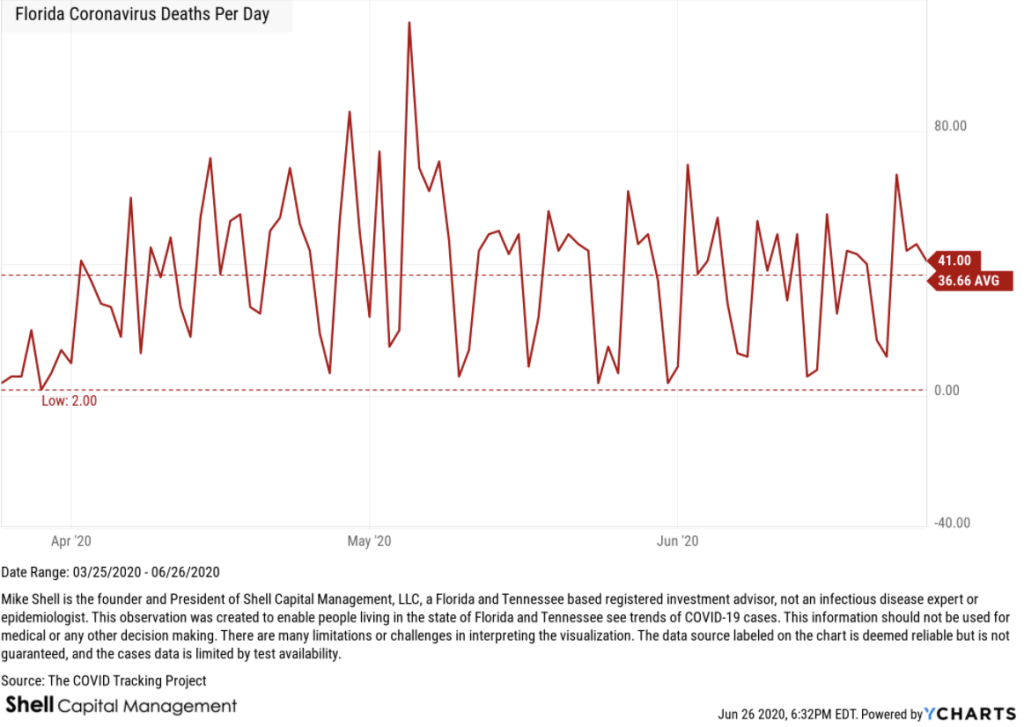

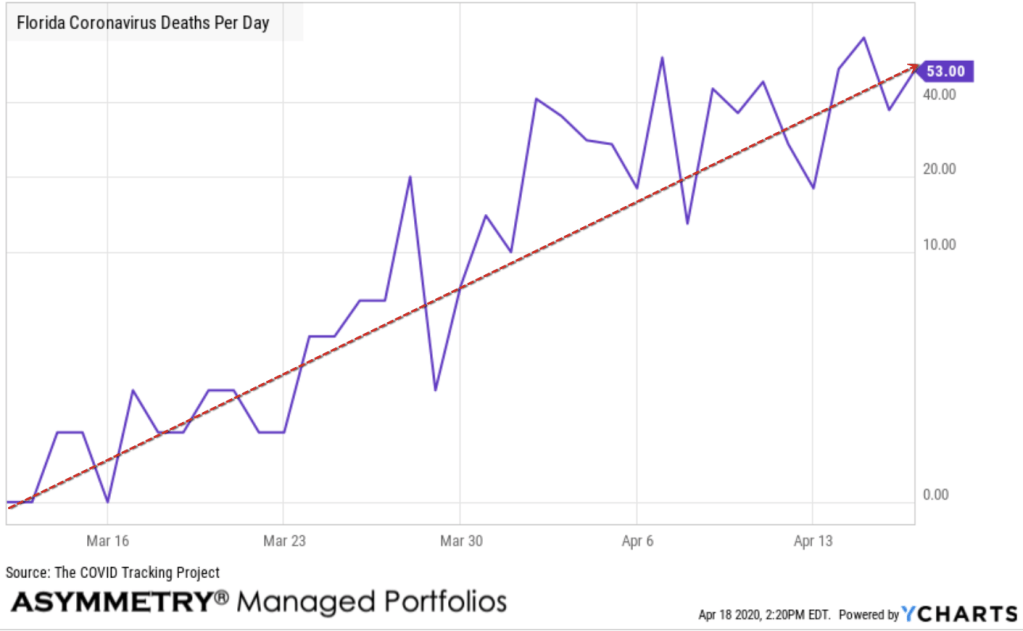

Daily deaths in Florida, however, continues to oscillate around its mean. I expect this may trend up and follow new cases, but, it will depend on how many of those new cases are younger healthy people who get over it vs. higher-risk people who may not.

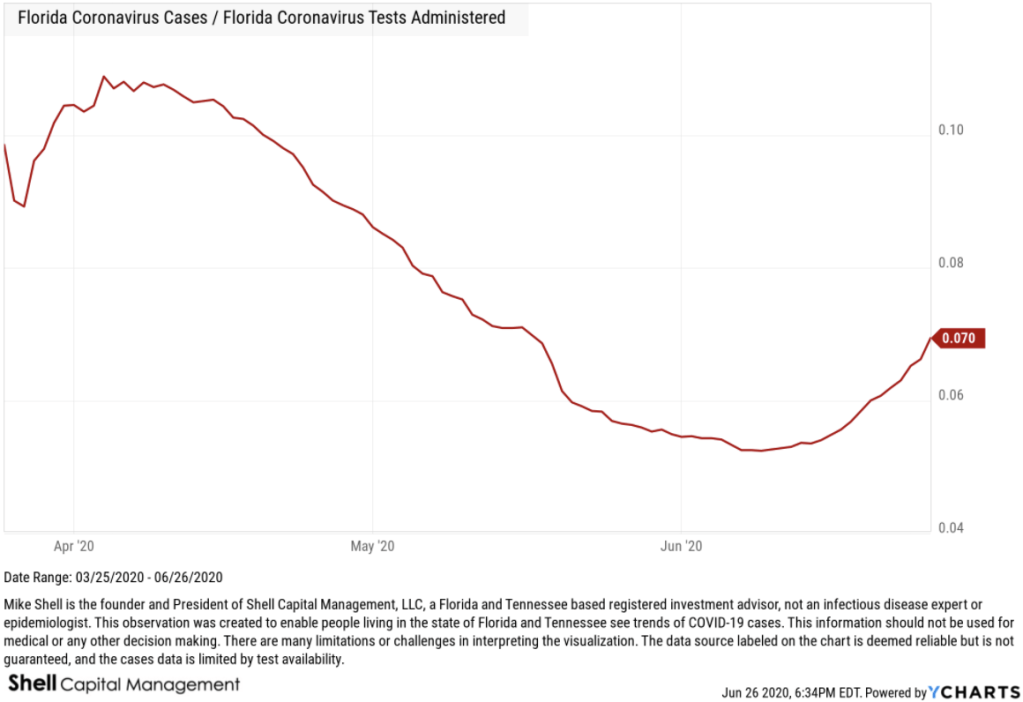

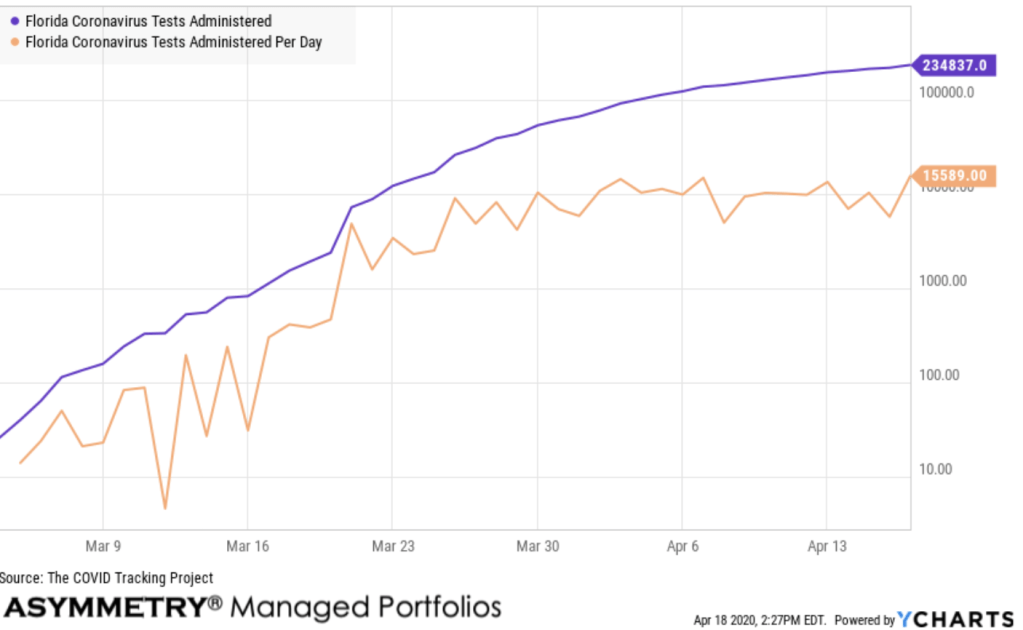

Cases relative to tests administered shows us the ratio between the two. As this trend bottomed June 9th and has seen trended up, it tells us the cases relative to tests is increasing. In other words, new cases are showing more momentum than new testing.

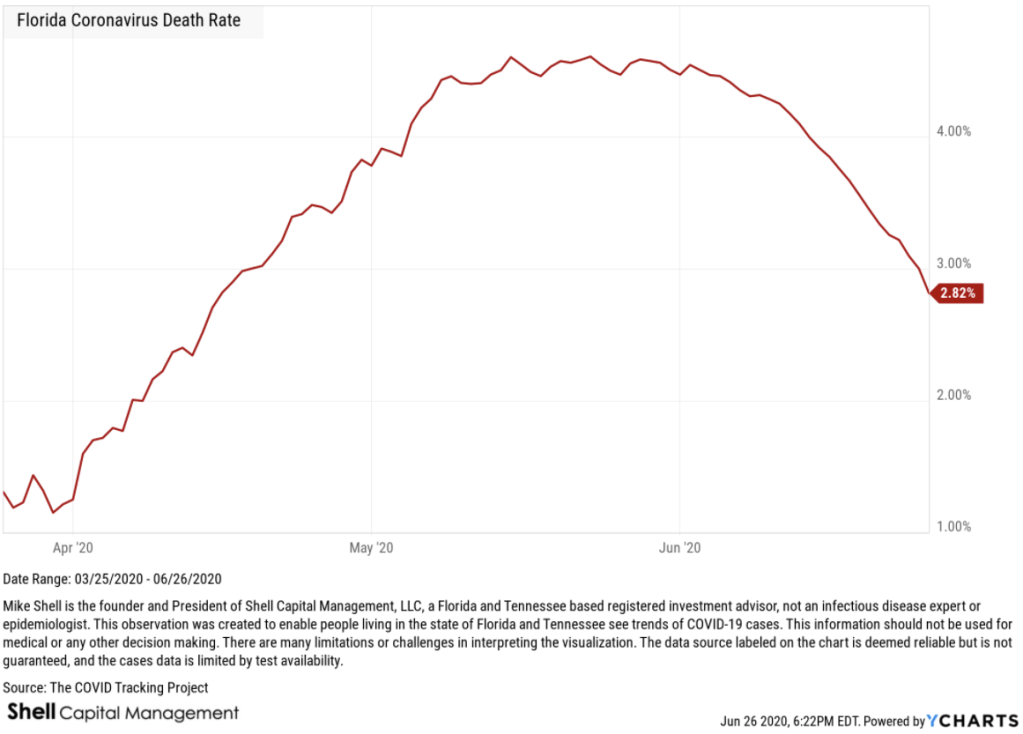

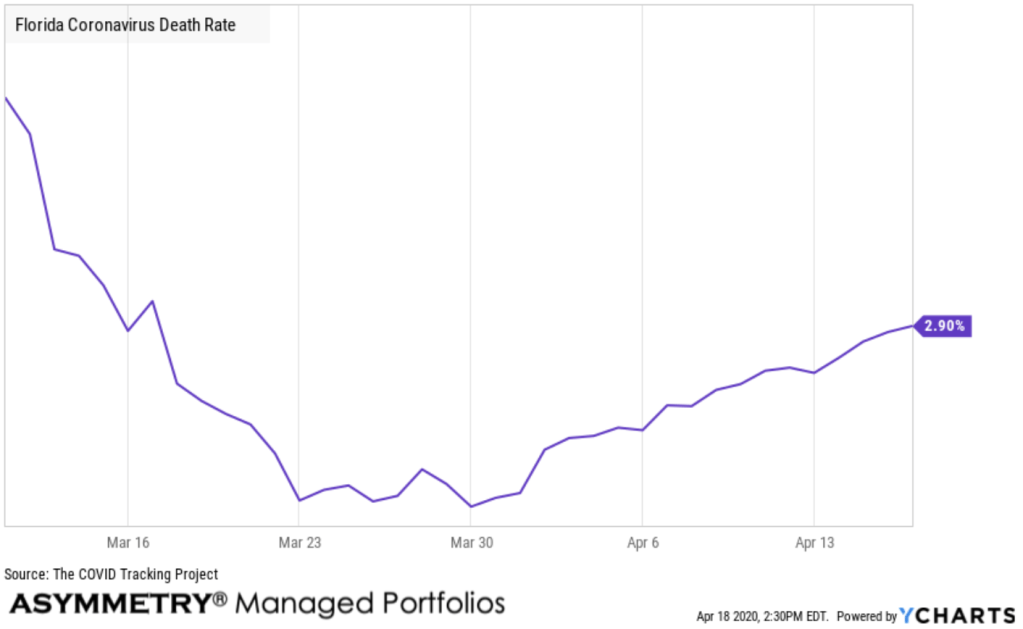

THE GOOD NEWS IS: The death rate in FL continues to fall, which is hopefully a reflection of better treatment and/or the virus weakening. I’m guessing some part of it is a function of younger people getting infected and shaking it off.

Life is full of risks and rewards, so we make the best of it by directing and controlling our possibility of loss.

Intelligent people focus on managing the downside, the surprises, the uncertainty, and the risks since the upside of rewards takes care of itself.

At this point, we’ve all been made well aware of how to direct and control our risk to the possibility of loss, so we only have to do it.

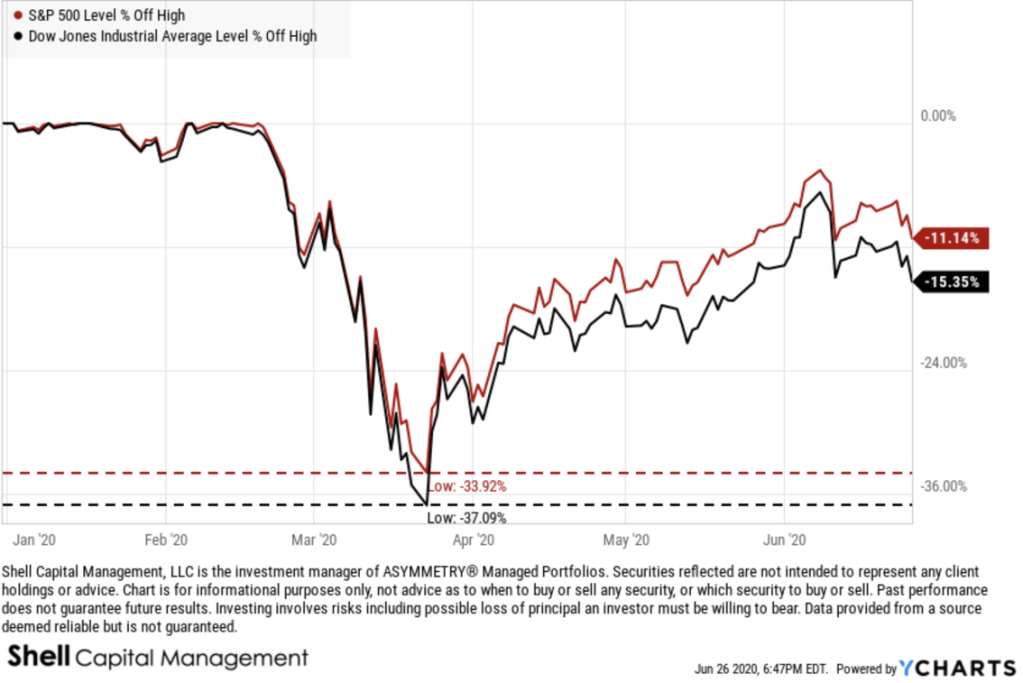

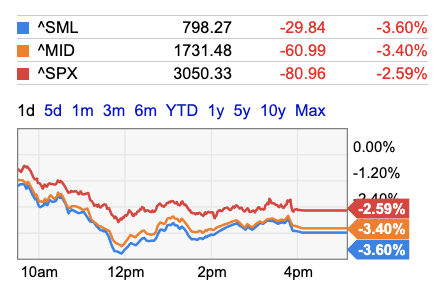

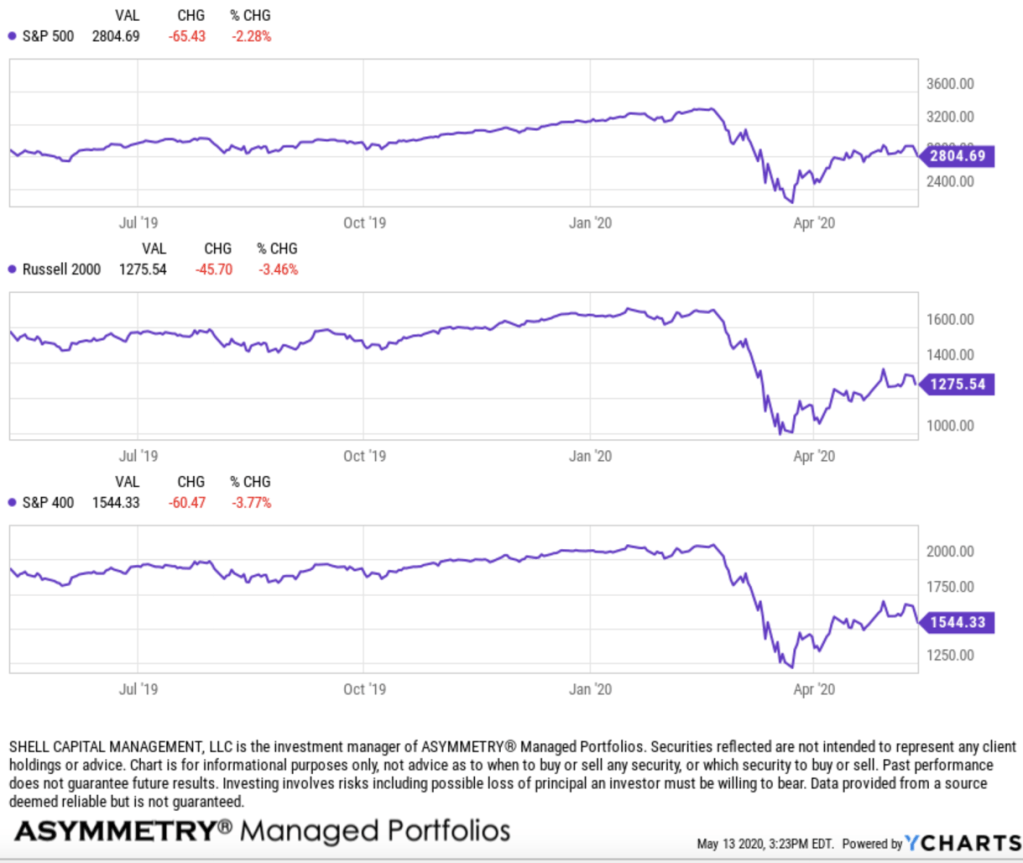

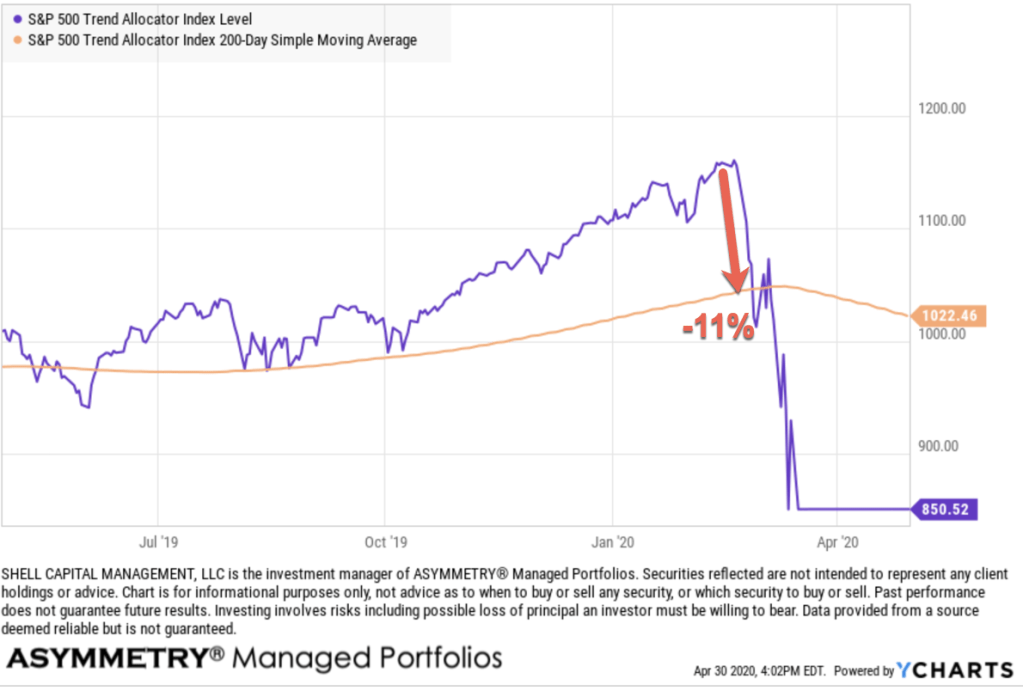

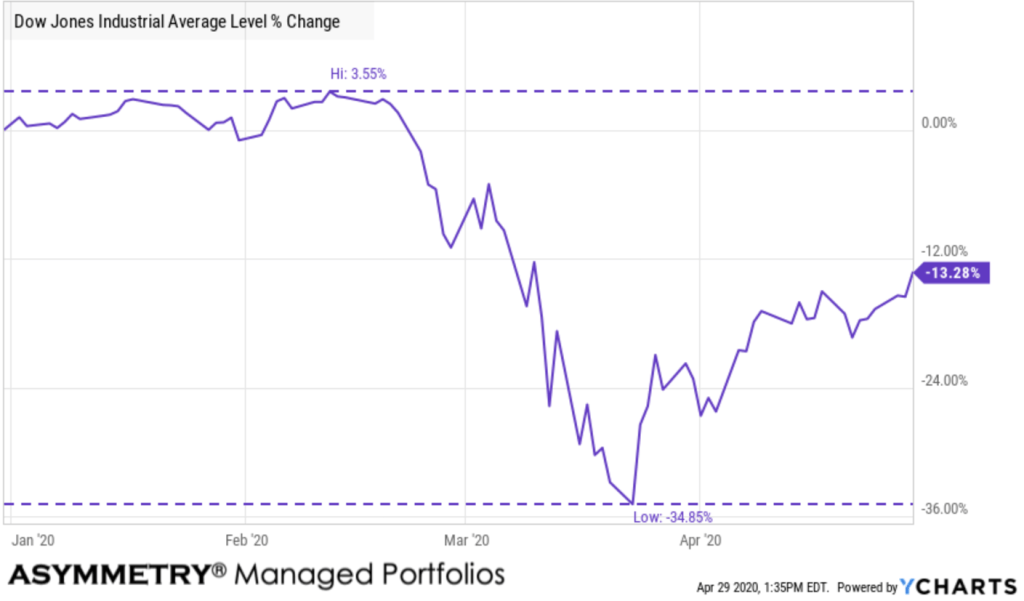

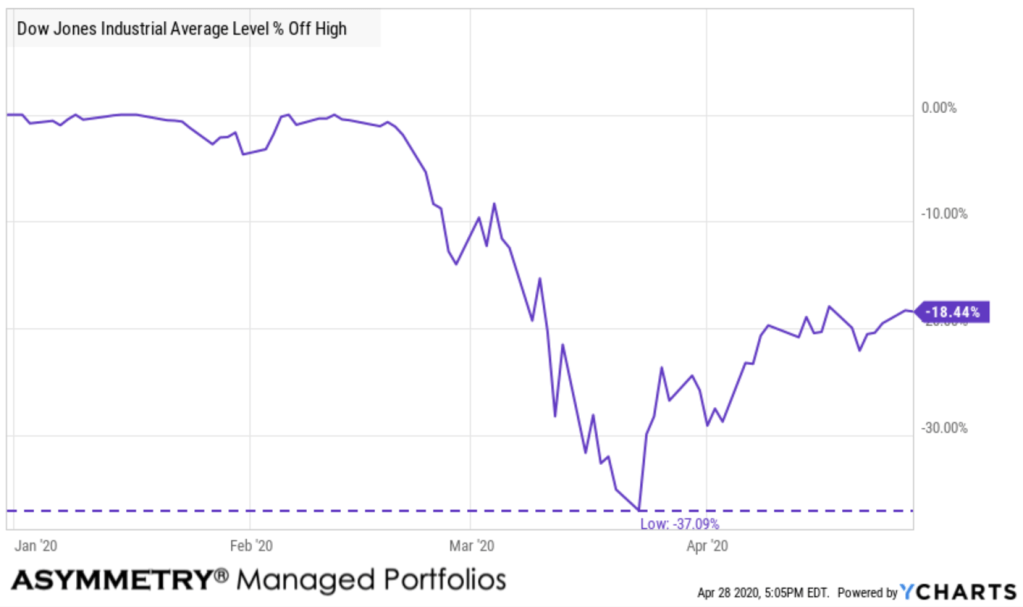

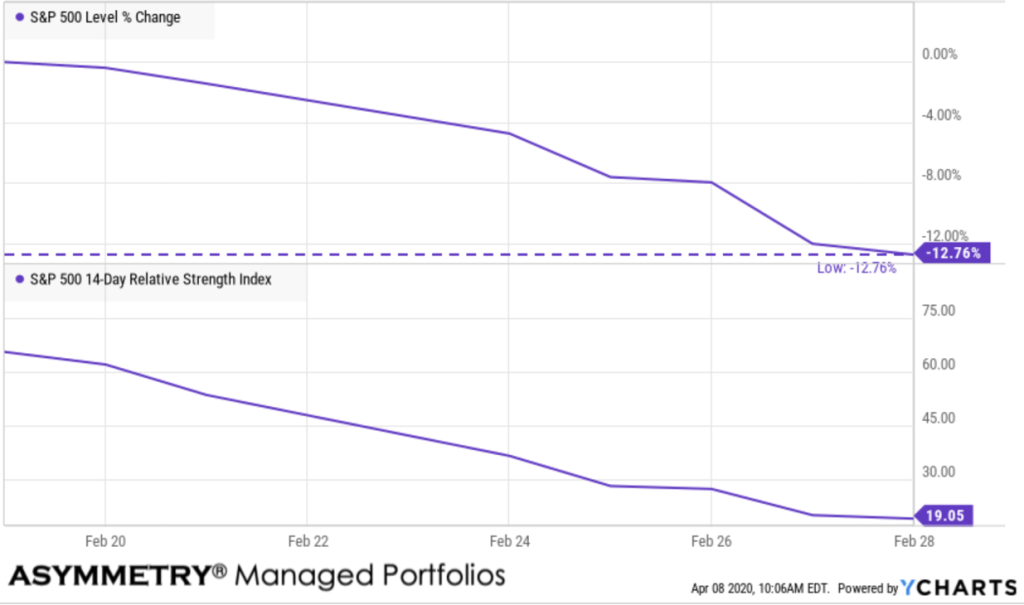

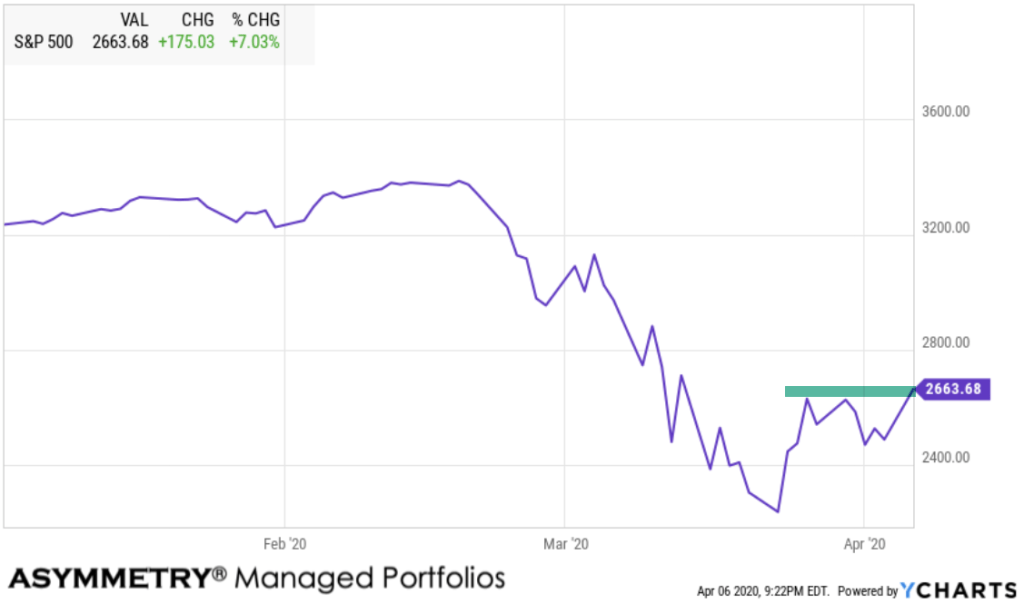

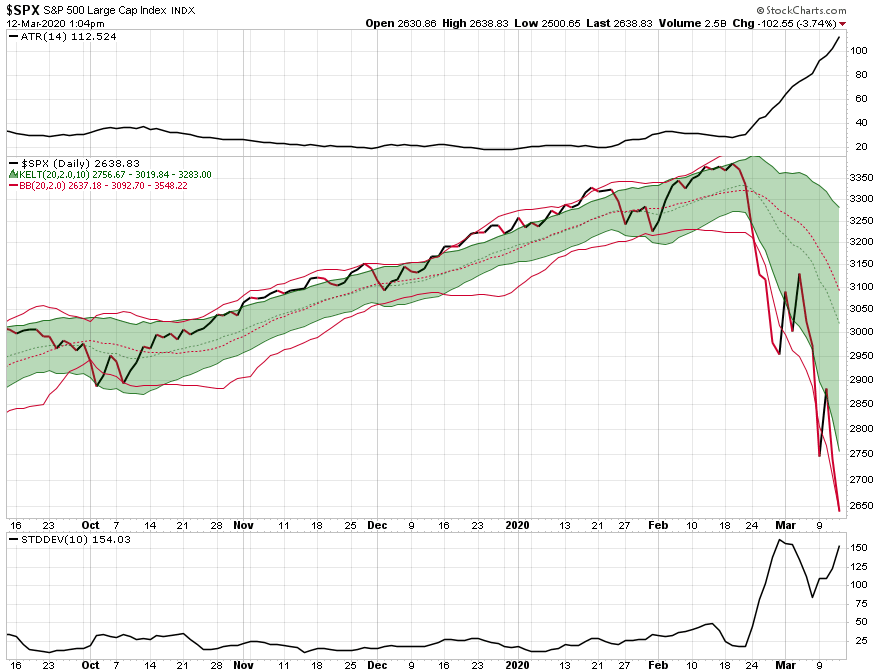

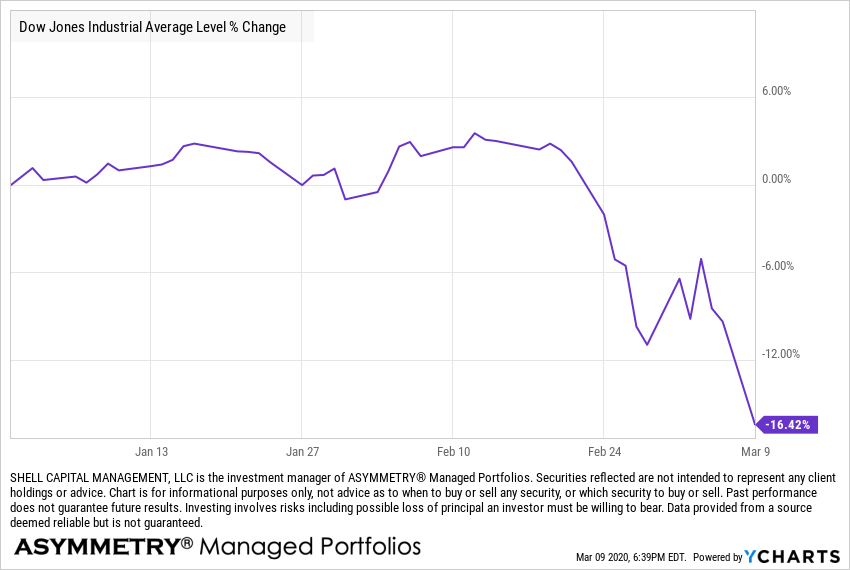

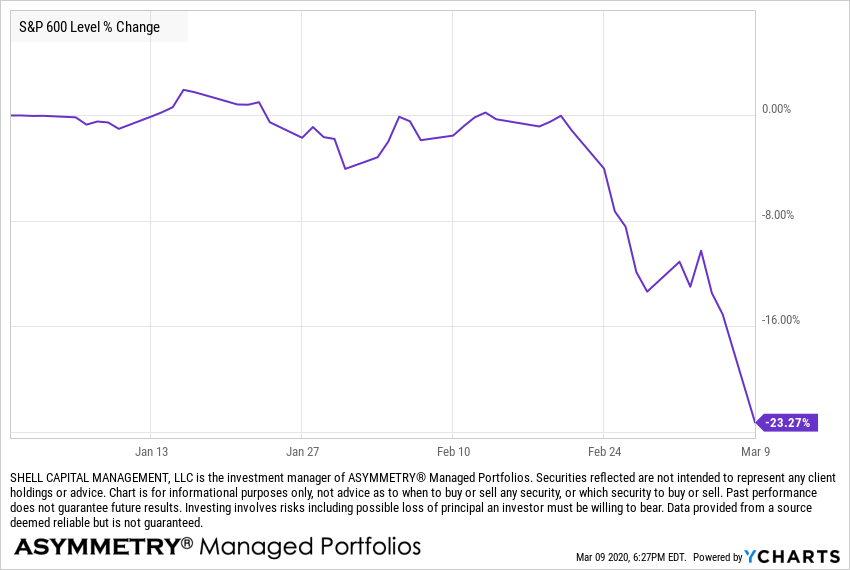

These stock indexes are now down -11% or more off their highs, and the Dow Jones is down -15% from its February high.

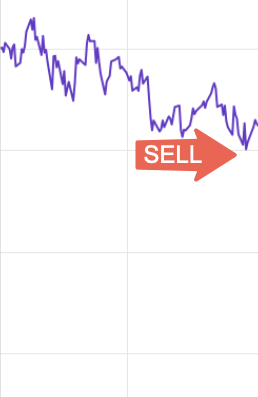

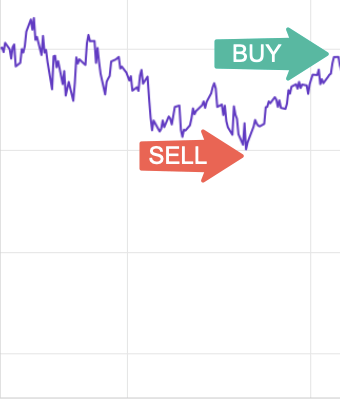

I reduced our exposure to stocks to zero a week ago.

Be informed, and prepared, not afraid.

Don’t miss out! If you want to follow along sign up for an email of new ASYMMETRY® Observations.

Join 520 other subscribers

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

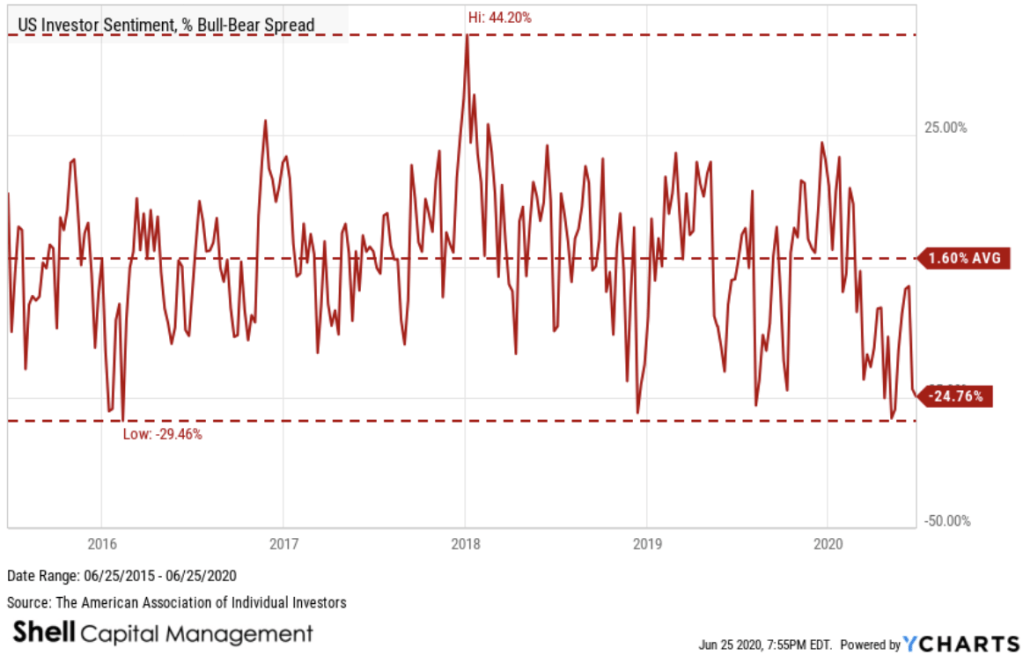

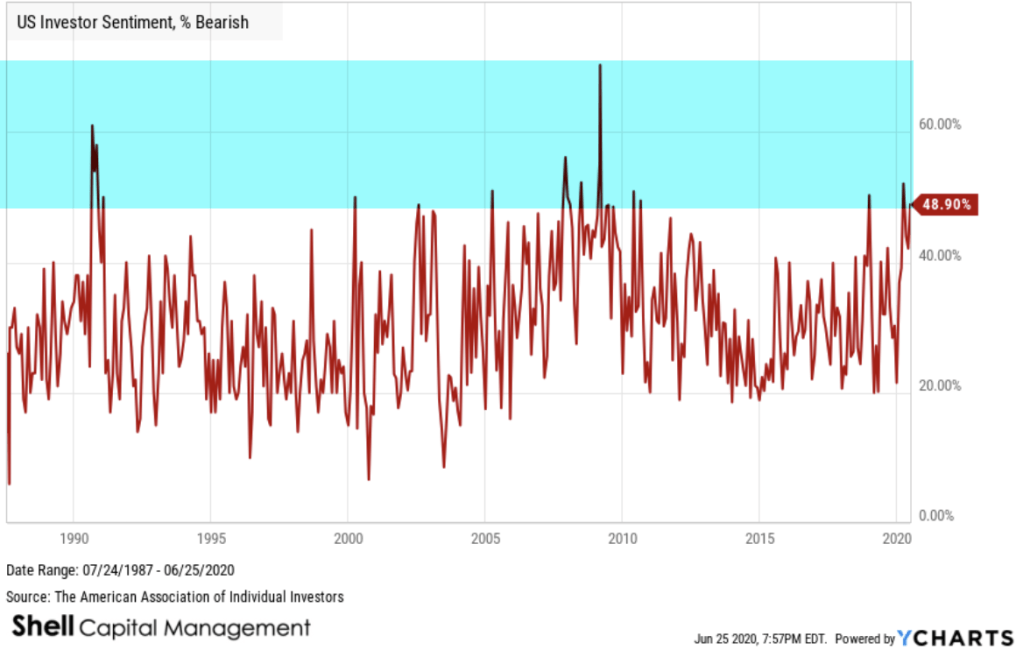

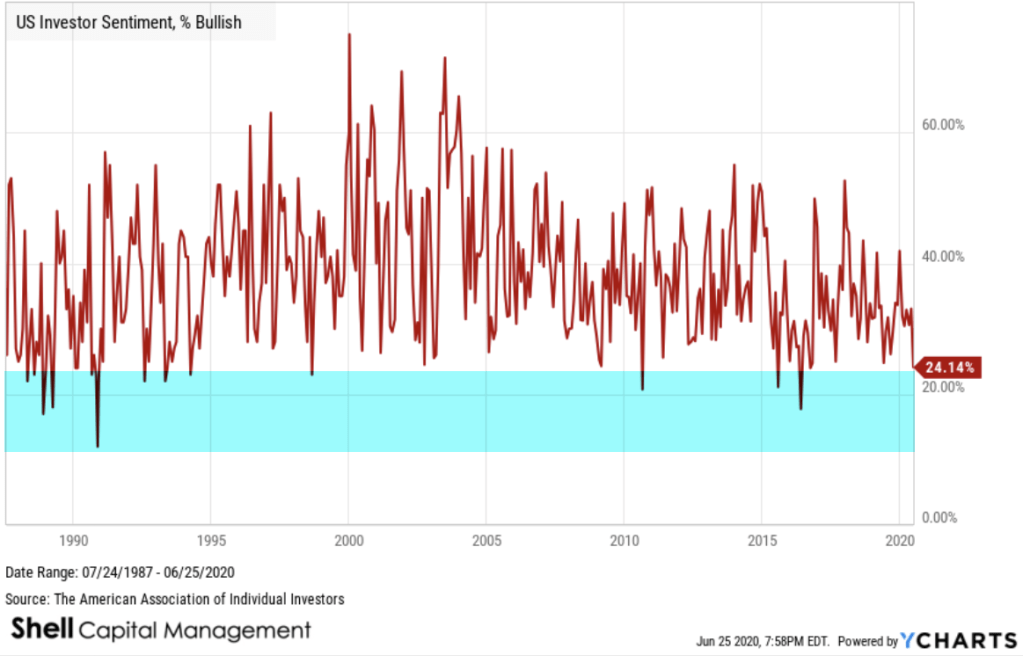

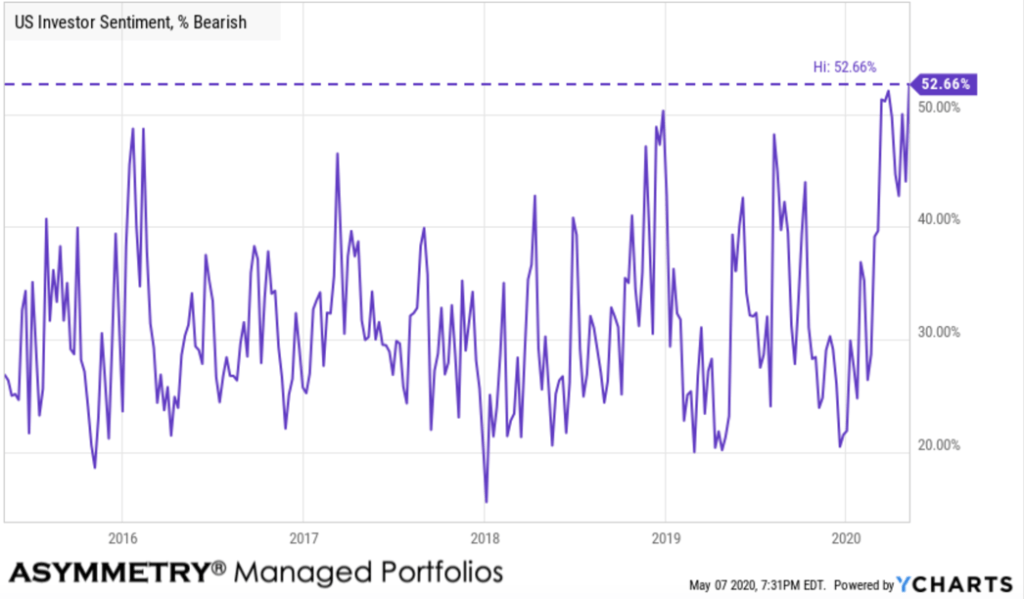

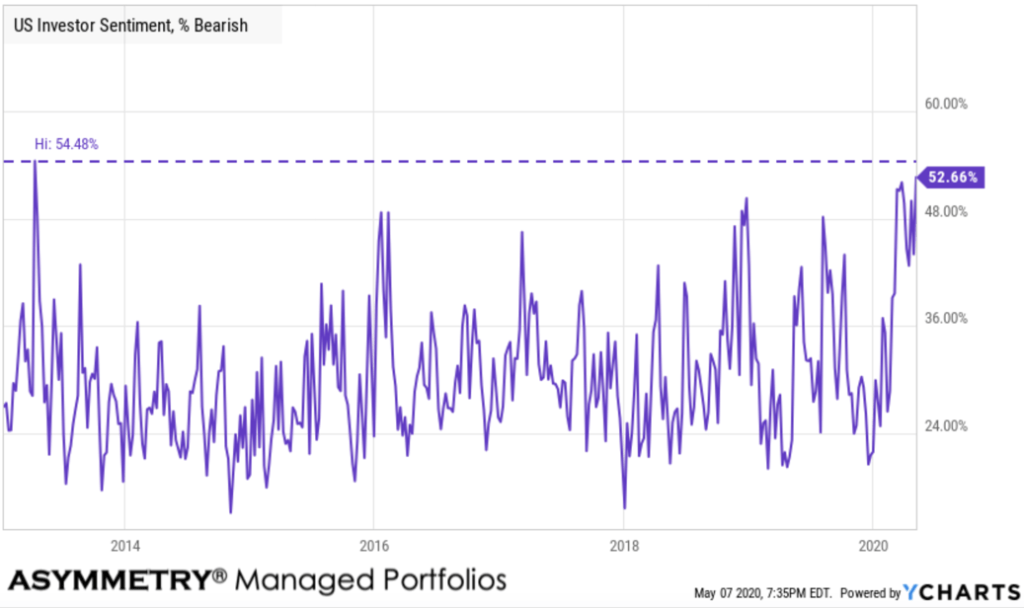

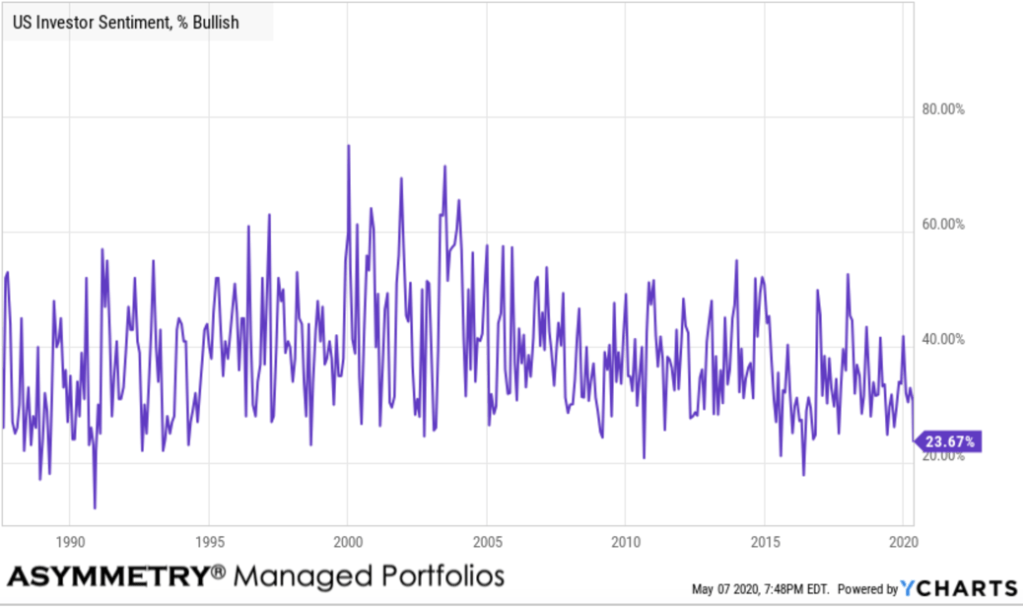

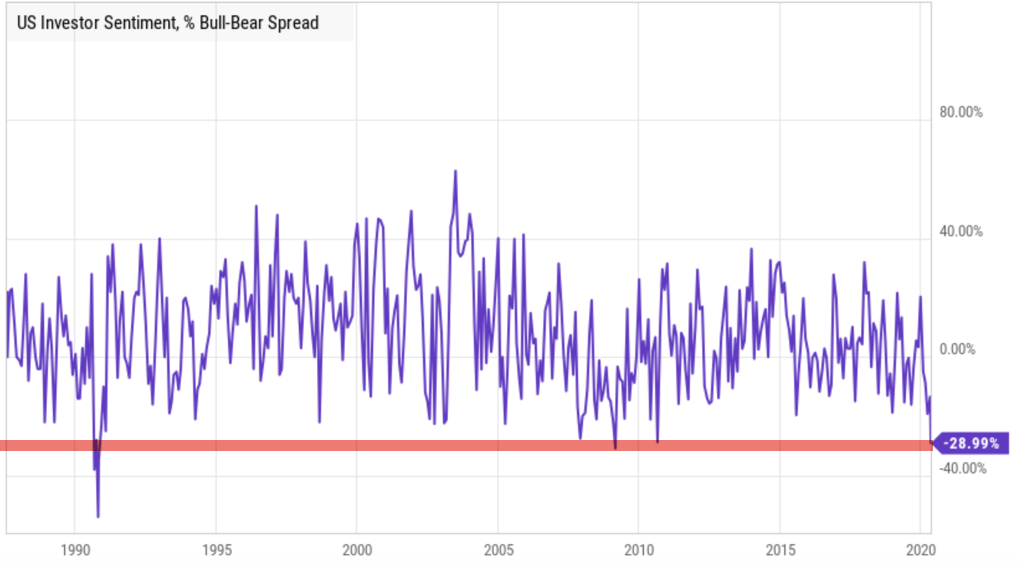

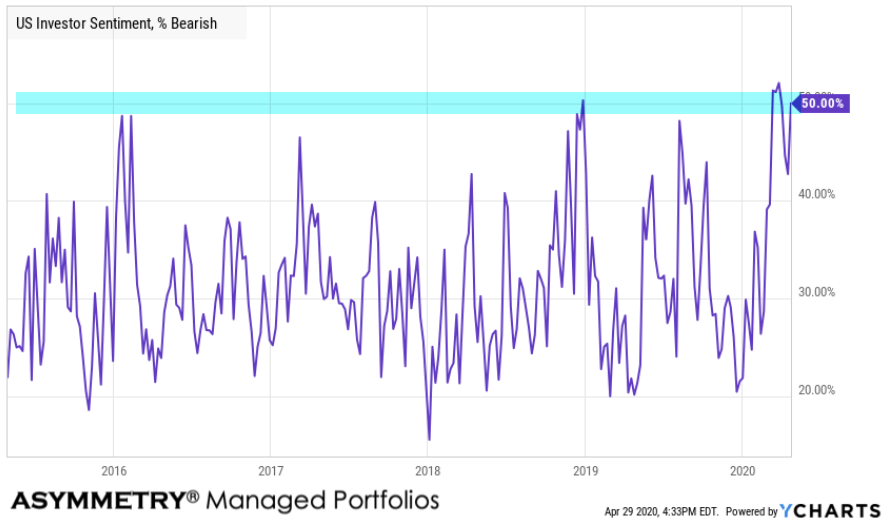

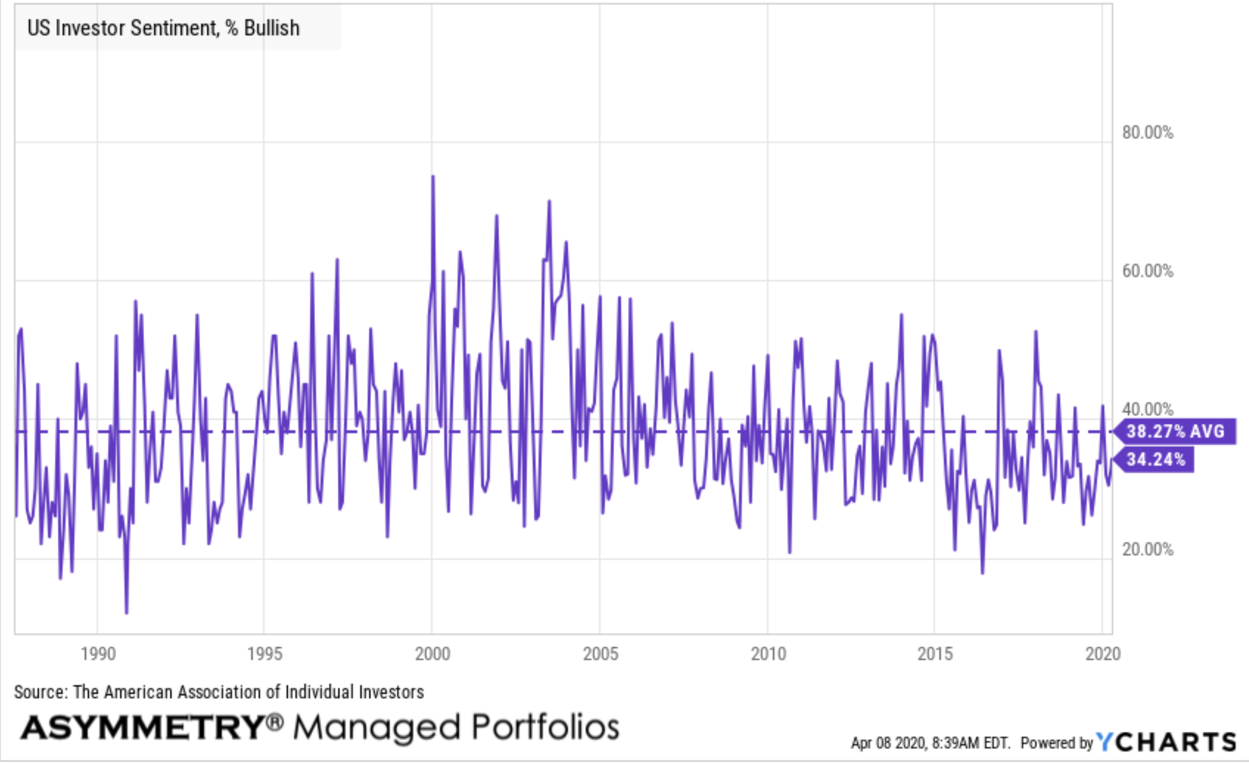

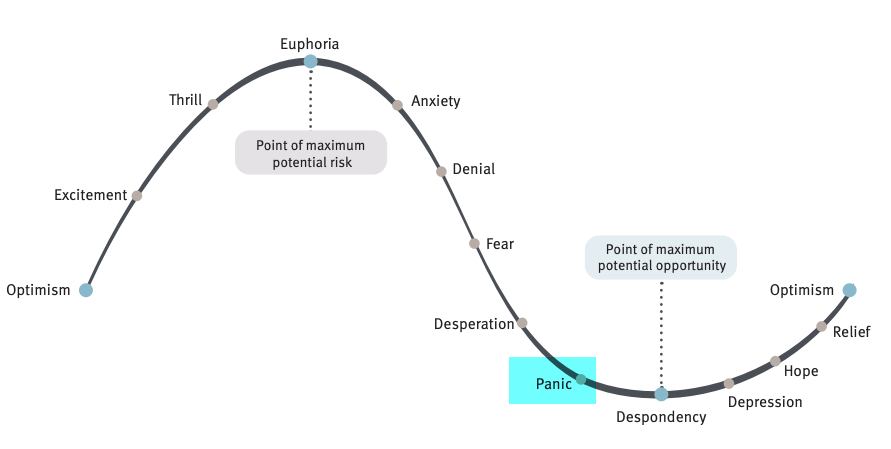

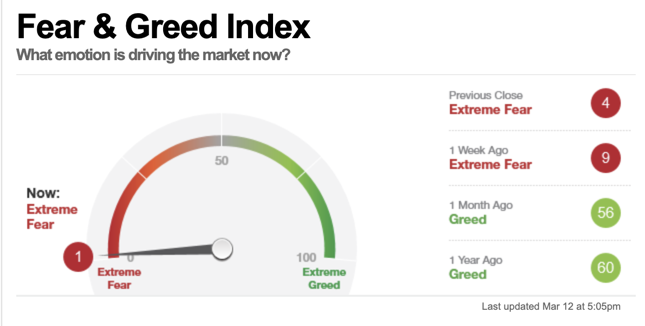

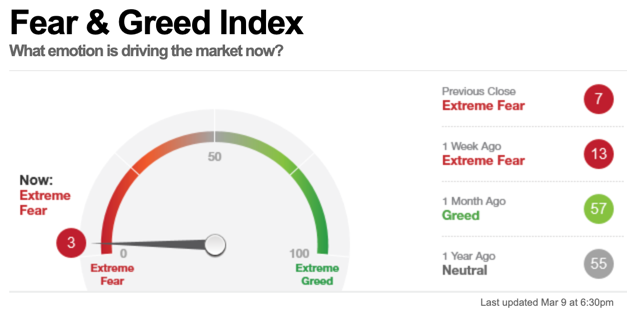

Individual investors are now bearish based on the survey and expected volatility.

Since 1987, the American Association of Individual Investors has asked the same simple question each week to see what direction individual investors think the market is headed over the next six months. The results are compiled into the AAII Investor Sentiment Survey, which offers insight into the mood of individual investors.

Since the crowd tends to get it wrong at extremes, when I see sentiment reach a historic high or low, I take note.

Falling bullish investor sentiment and rising bearish sentiment pushed the spread between bullish and bearish investors down to a low level.

Bearishness hasn’t historically trended much higher than this.

Bullish investor sentiment is about as low as it has been in history.

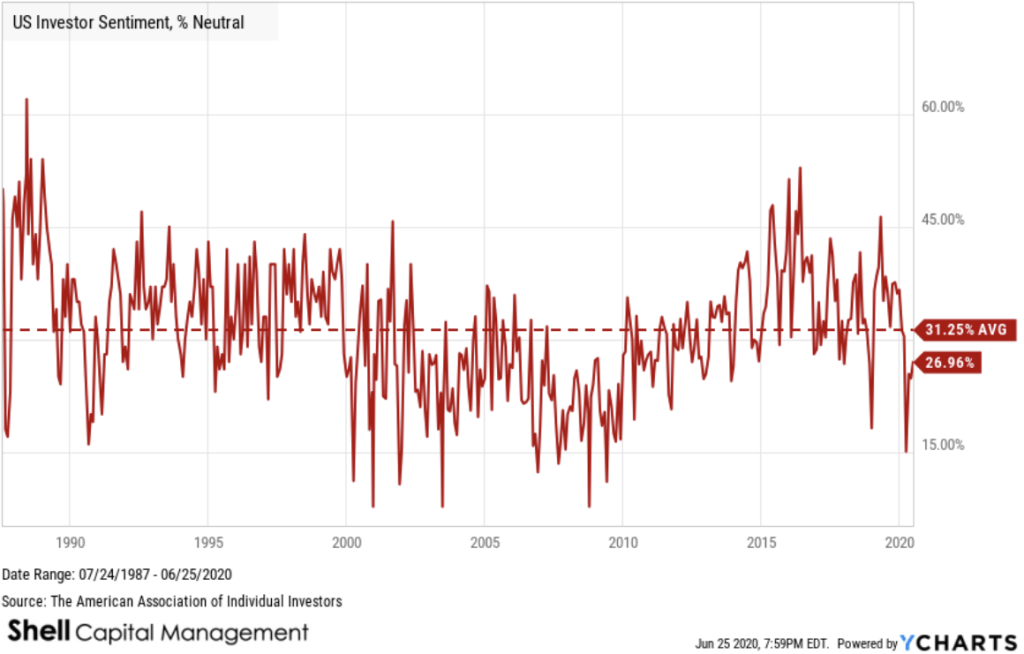

Neutral investor sentiment is about average.

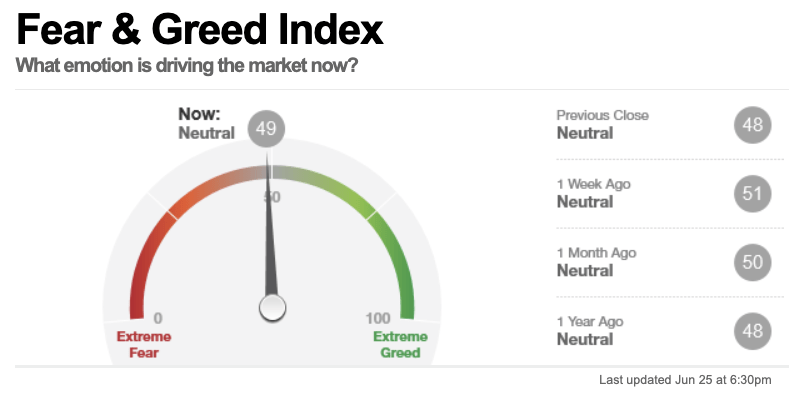

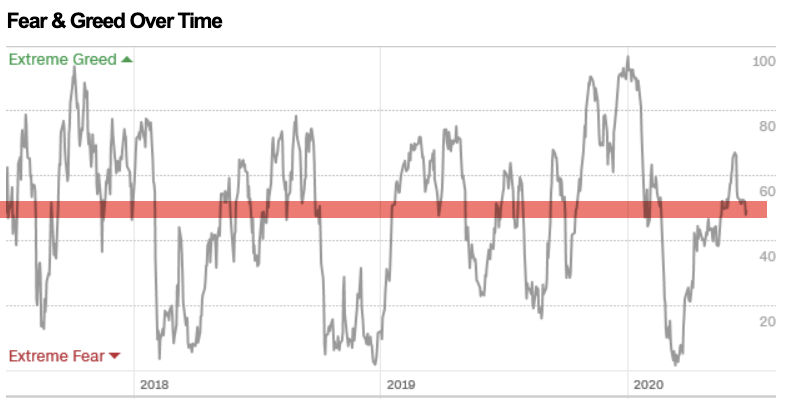

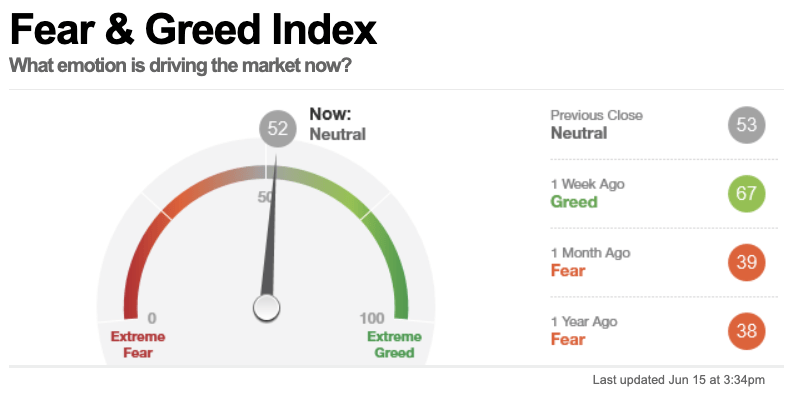

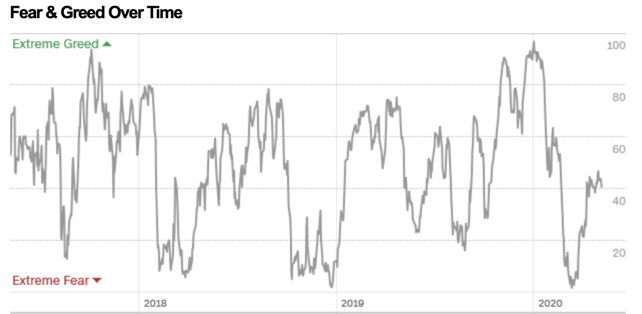

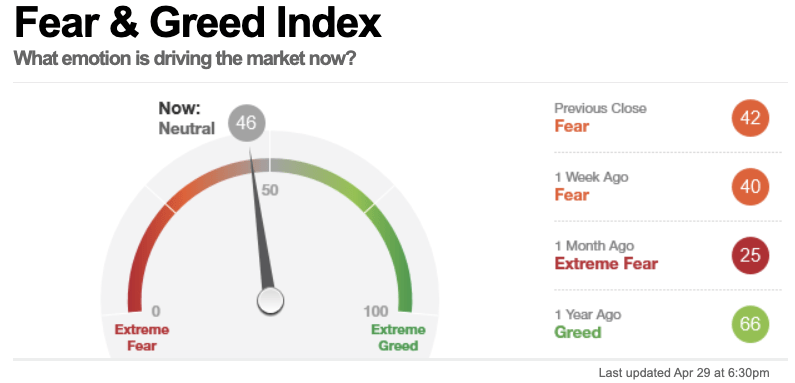

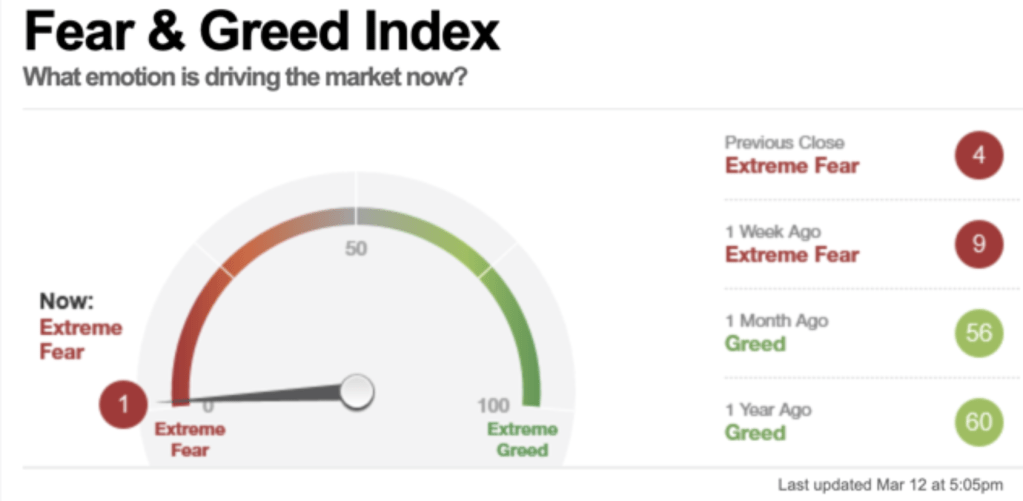

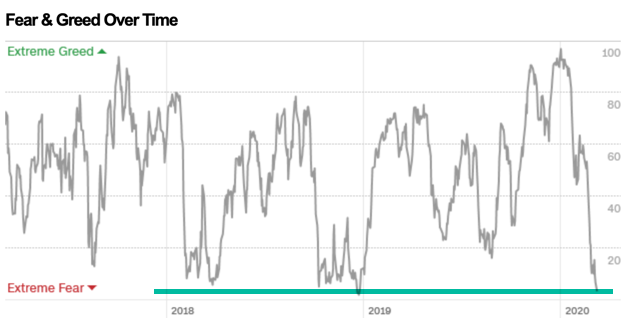

Unlike the AAII Investor Sentiment Survey, the Fear & Greed Index, which tracks seven different investor sentiment indicators, is neutral.

Investor fear and greed oscillates over time as investors swing from the fear of missing out and the fear of losing more money. Fear and greed is neutral at mid field in the cycle and is pointing down again.

Investor sentiment gauges may not be the best market timers, but the Fear & Greed Index can be a useful gauge for investors to signal when you don’t want to be part of the crowd sentiment.

At extremes, most investors feel the wrong feeling at the wrong time, so if we are to create better results than the crowd, we must necessarily be thinking, feeling, and doing the opposite of the herd.

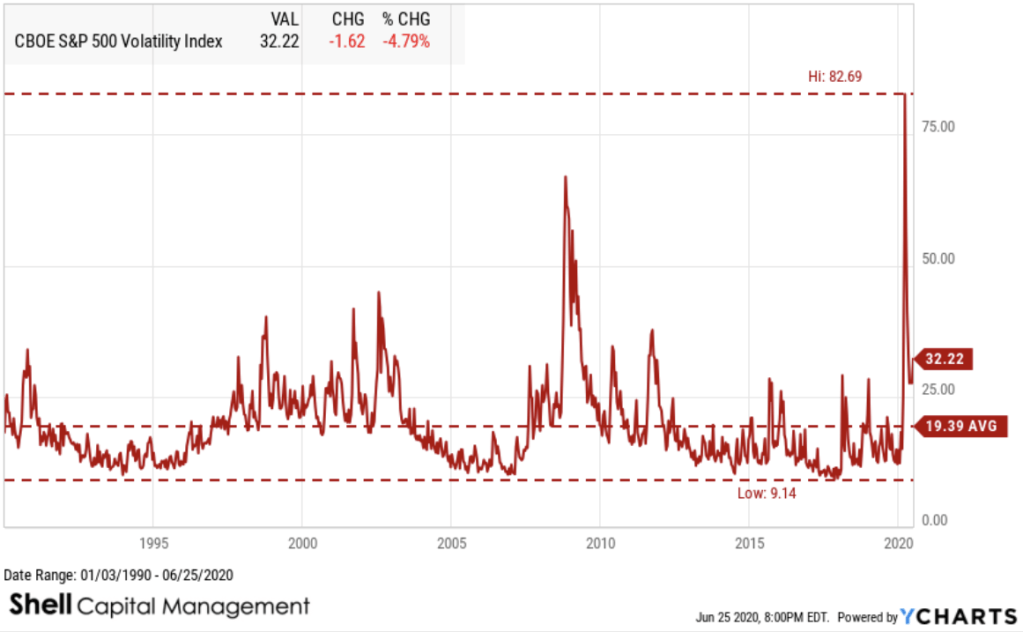

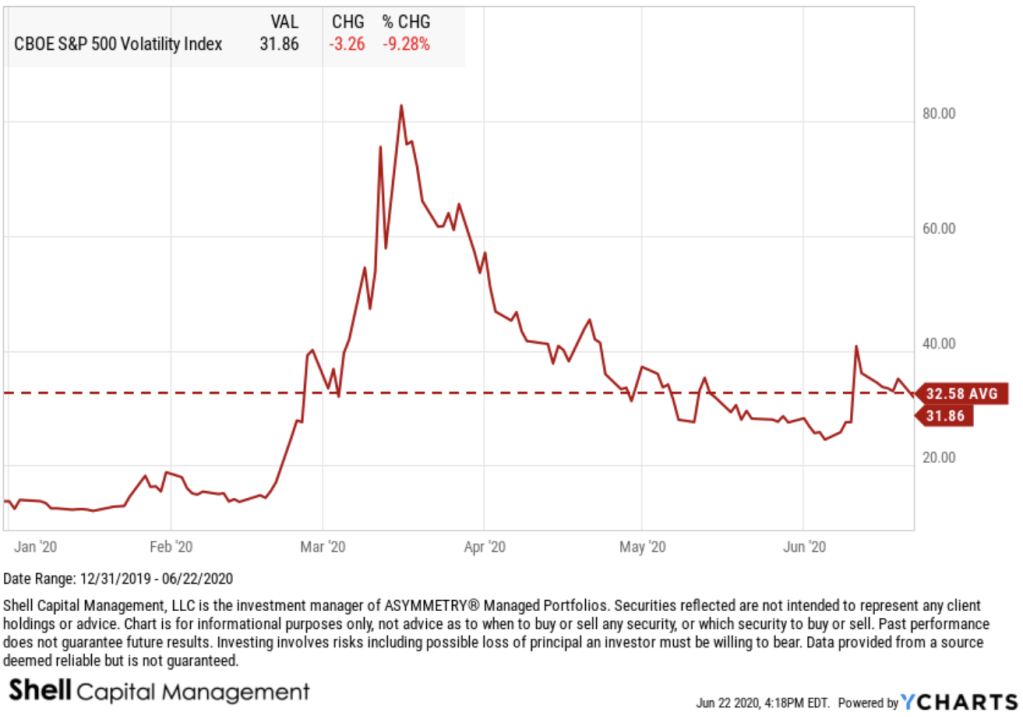

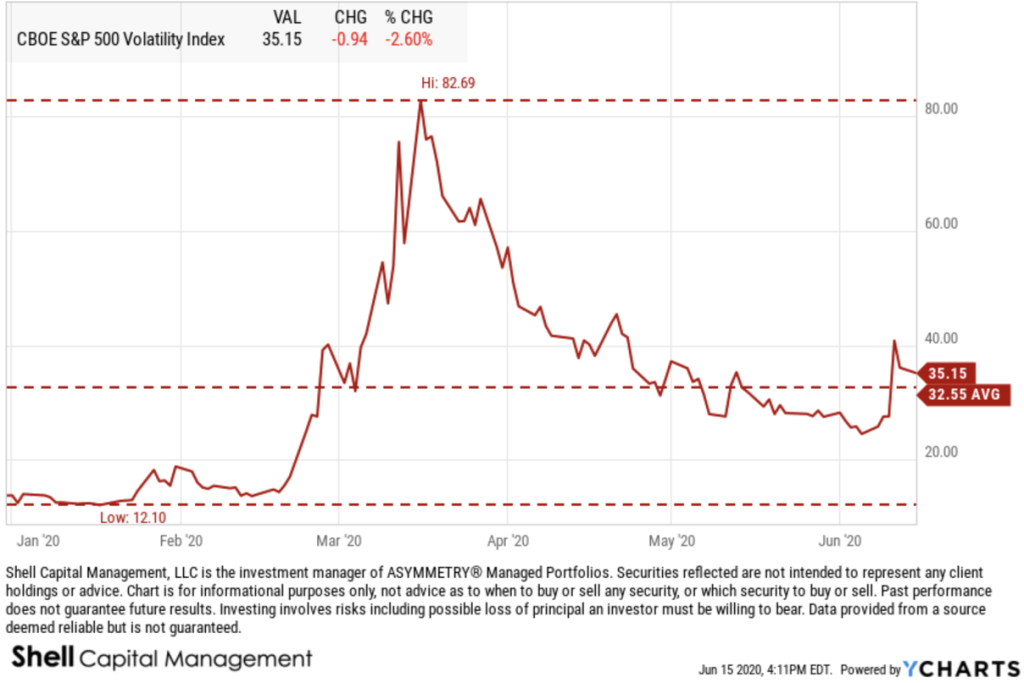

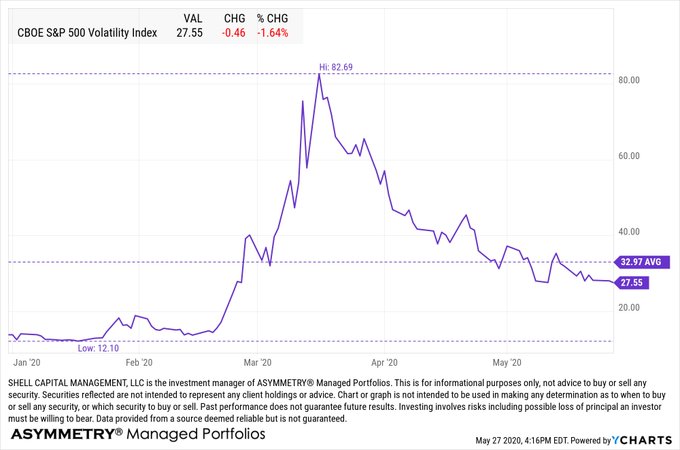

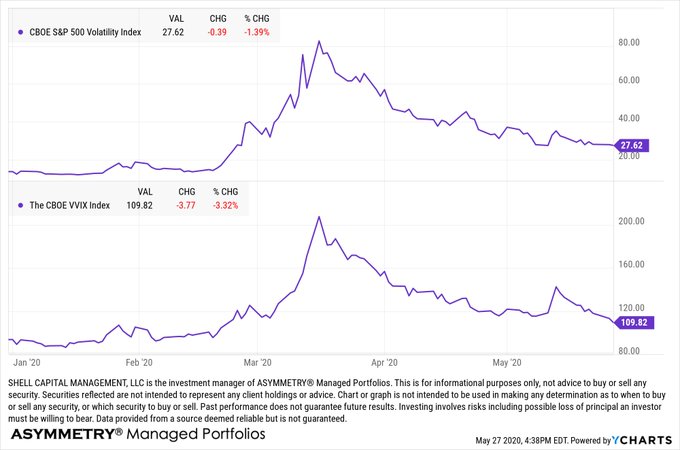

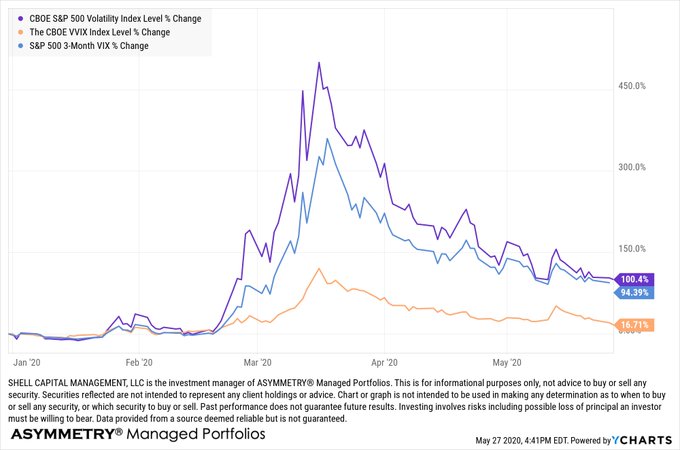

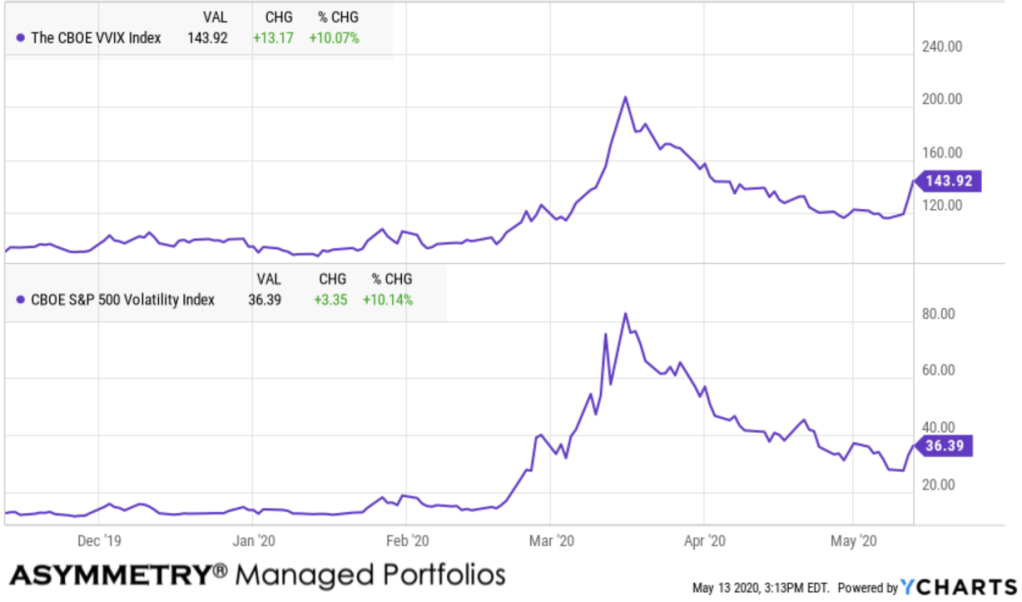

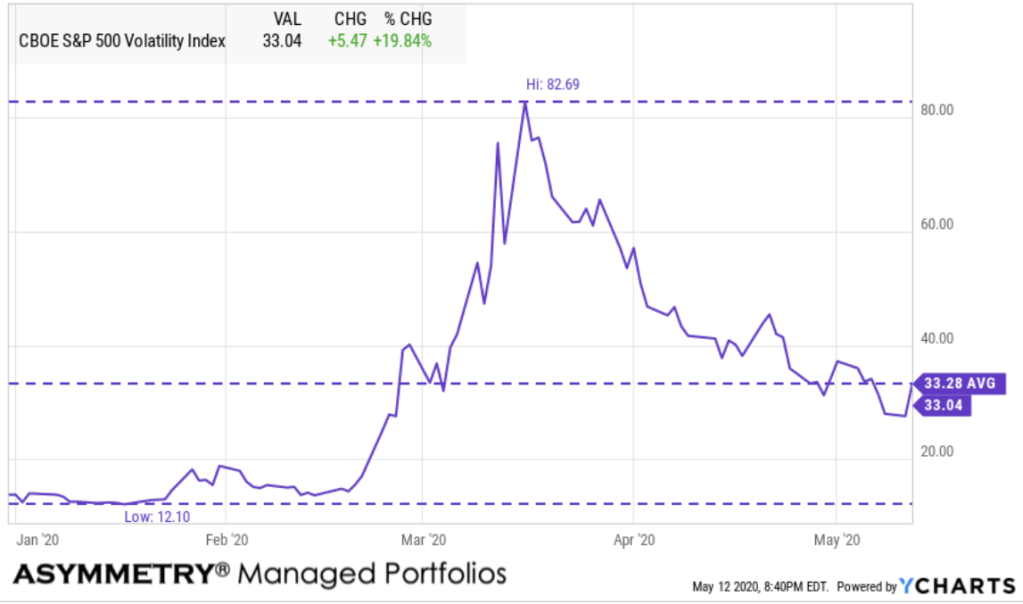

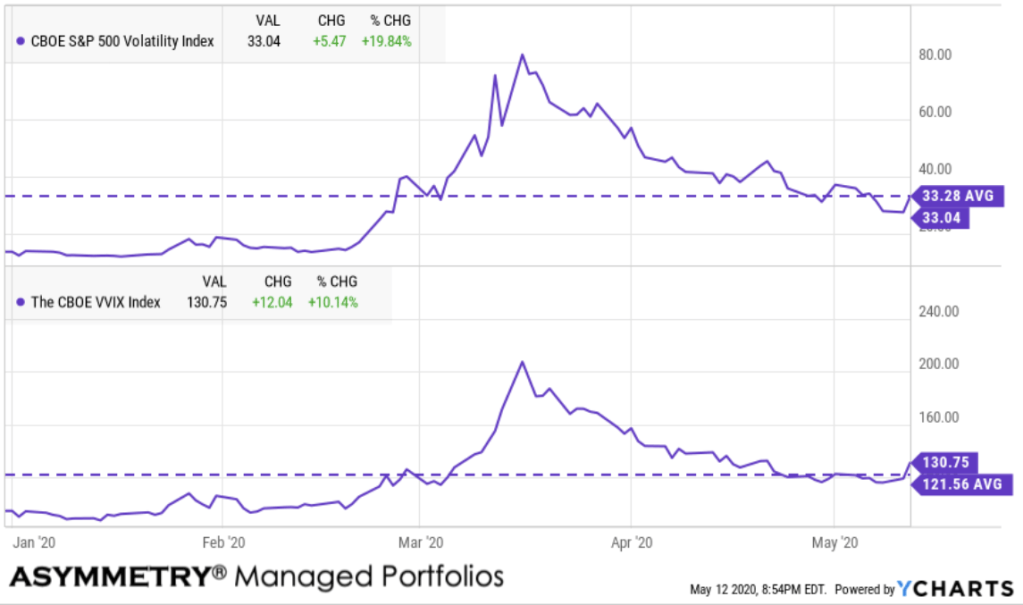

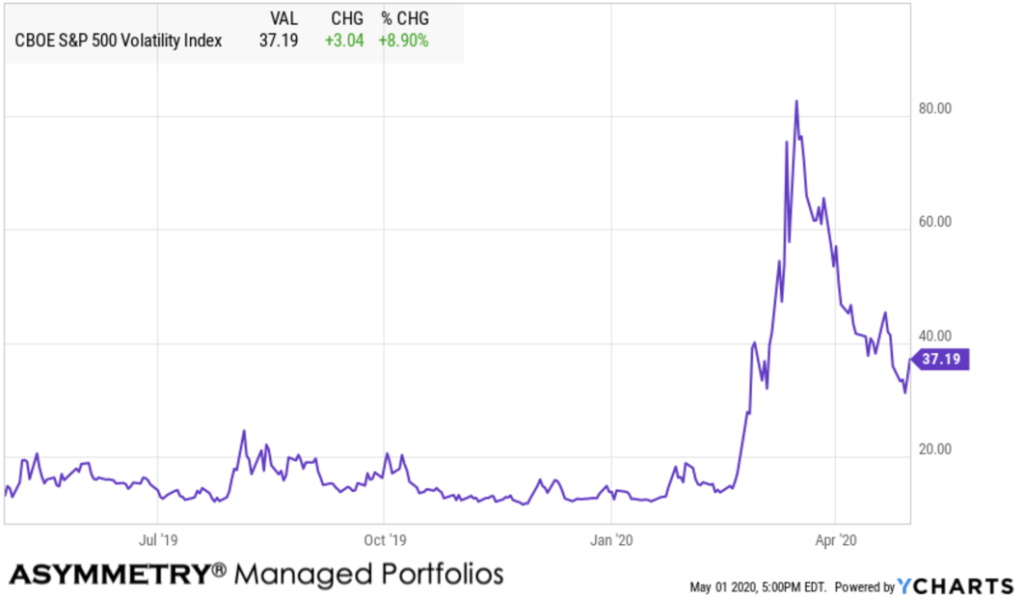

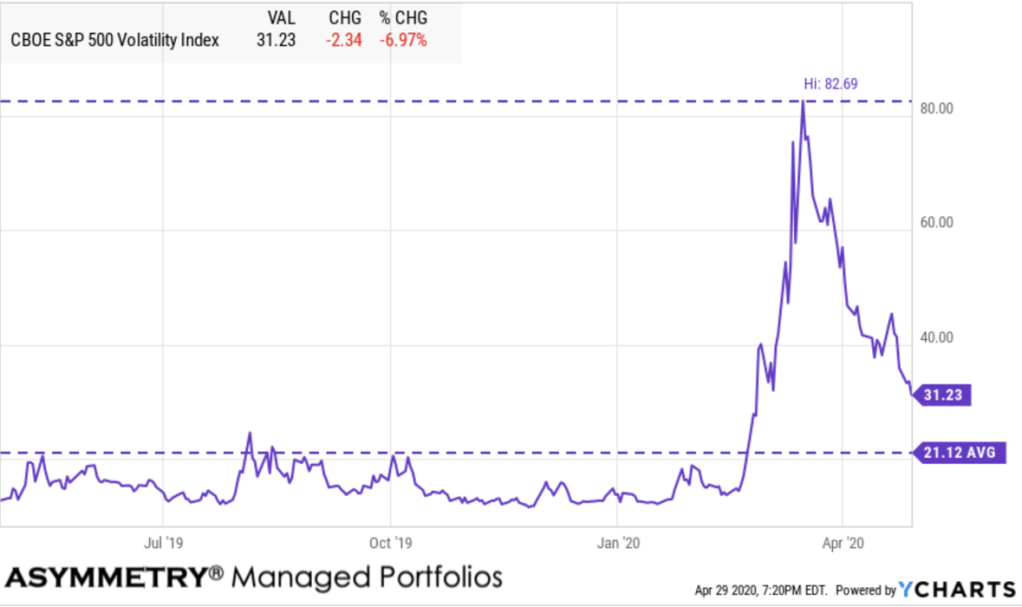

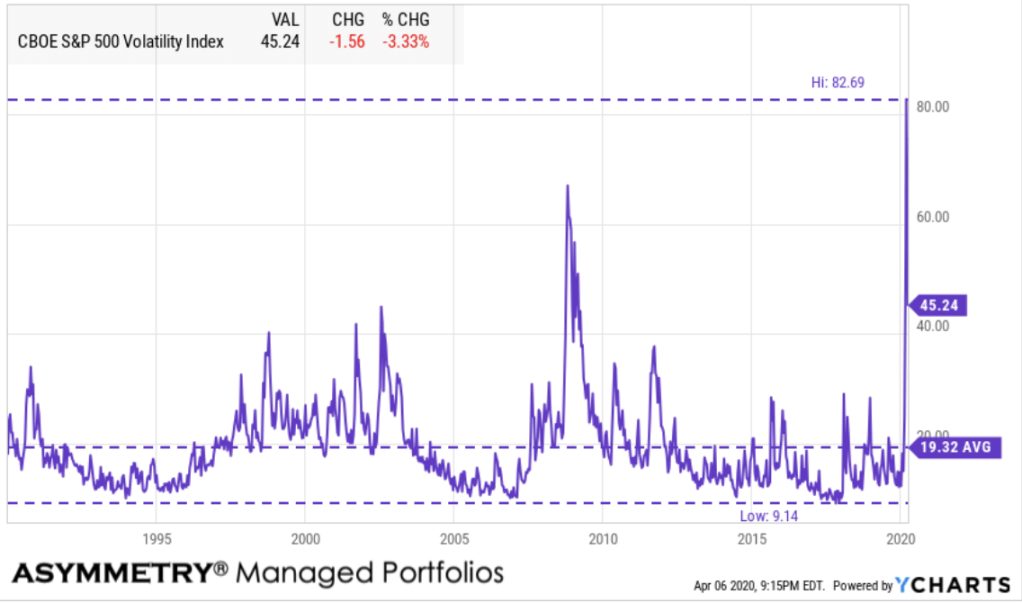

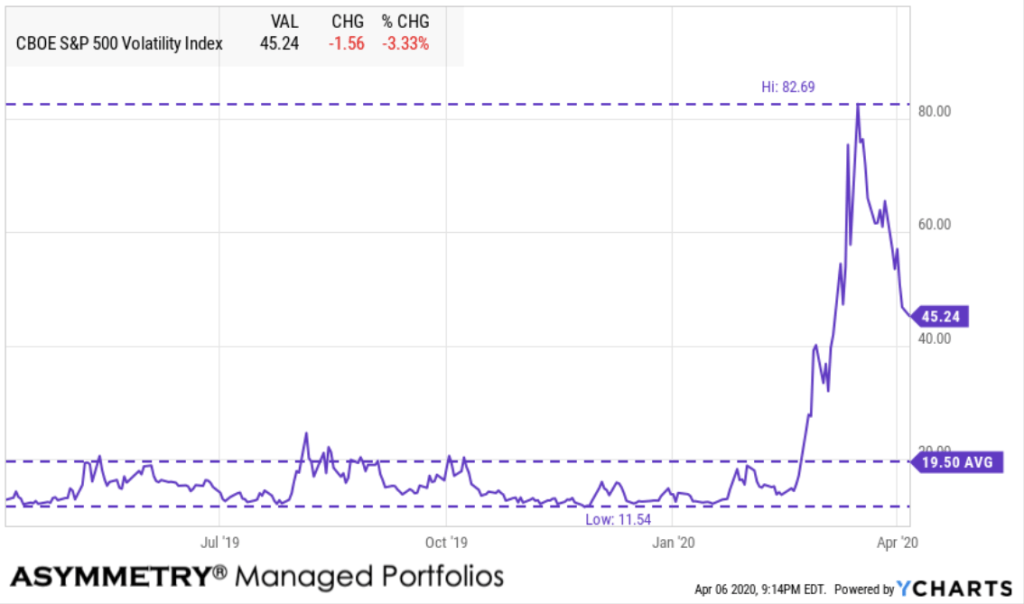

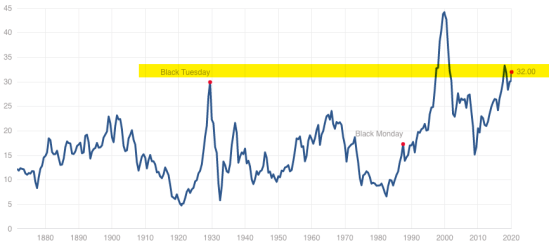

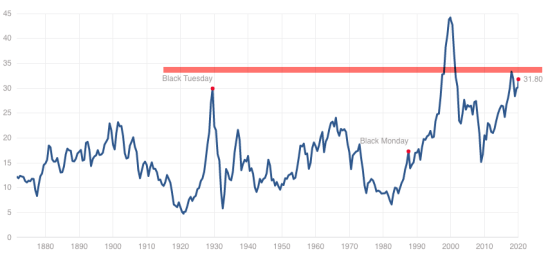

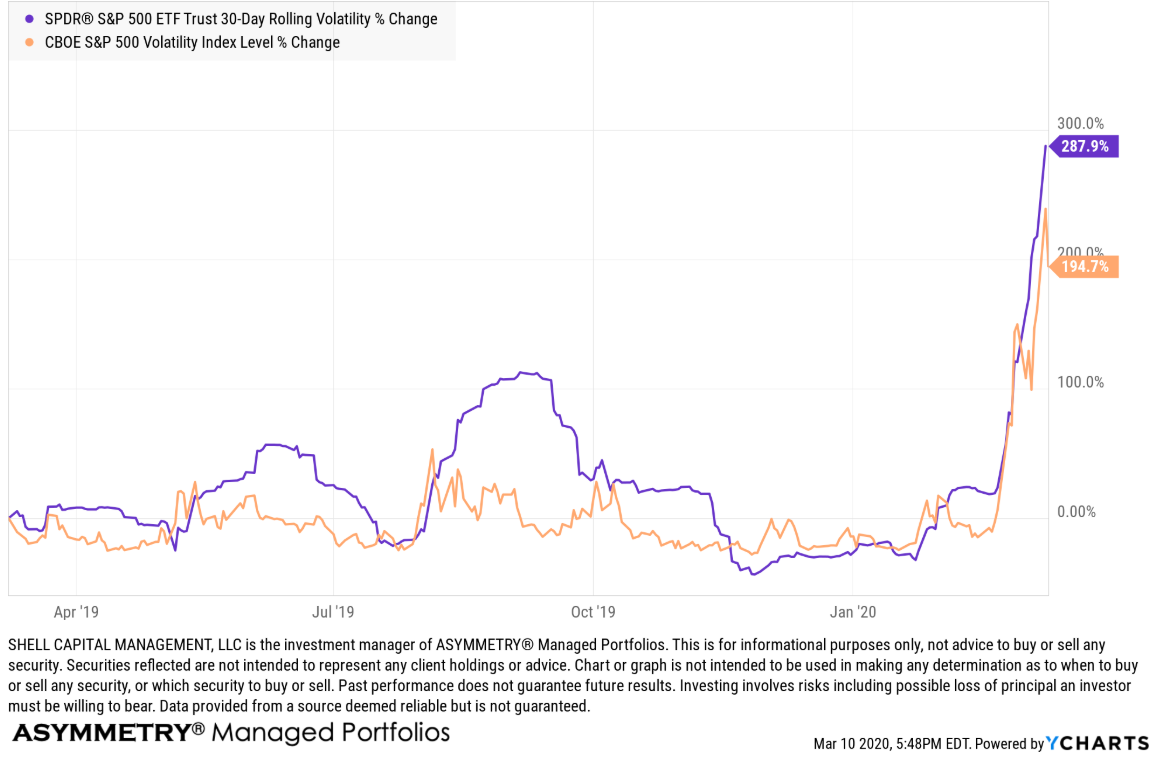

Expected volatility remains elevated, also signaling a higher than average level of fear.

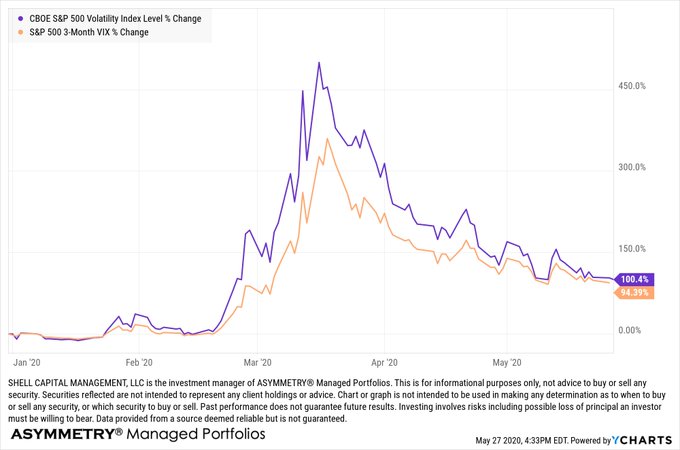

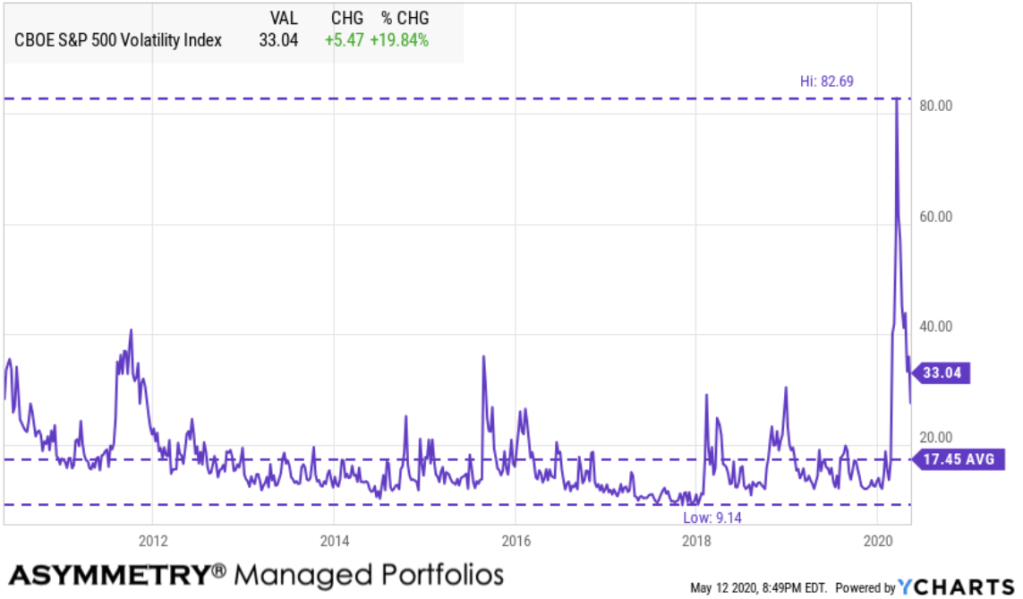

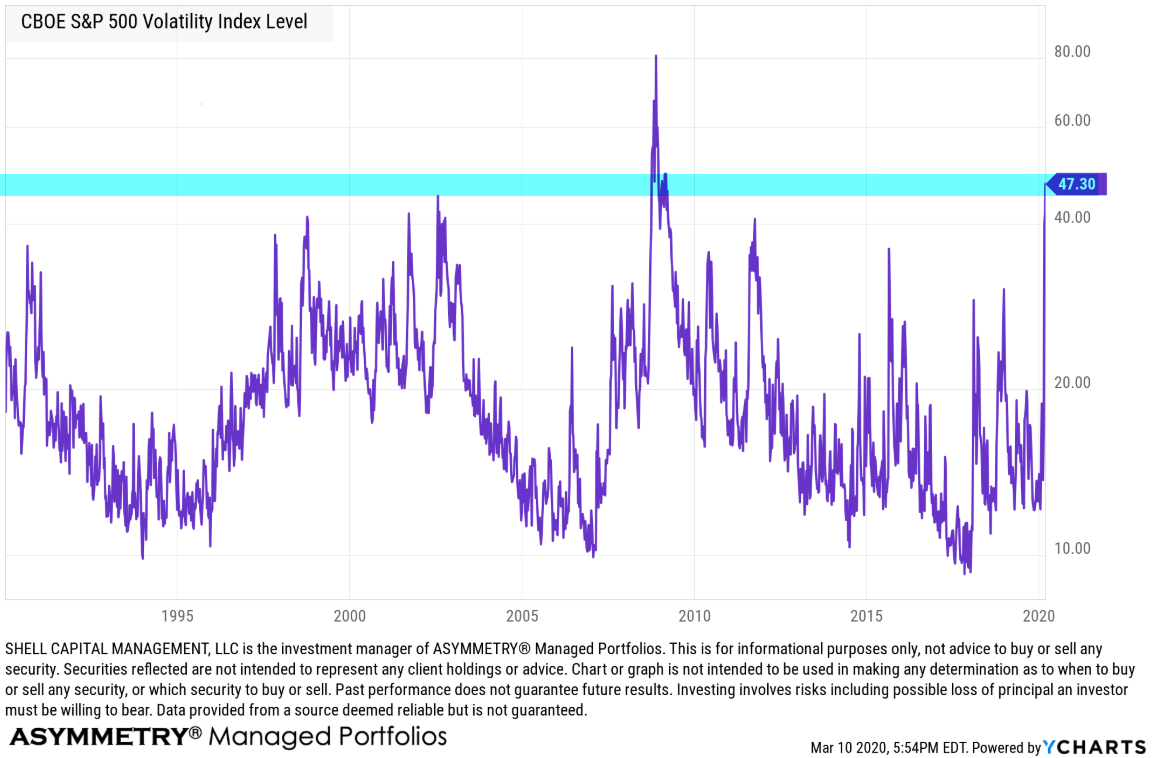

After the biggest volatility expansion, ever, implied volatility (VIX) has settled down to 32, which is elevated. The CBOE Volatility Index (VIX) is a real-time market index that represents the market’s expectation of 30-day forward-looking volatility. The VIX is derived from the price of the S&P 500 index options, and provides a measure of market risk and investors’ sentiments.

So, I’m guessing one of two things is about to happen. Either this bearishness will prove wrong and the stock market will trend up, or it will get a lot worse.

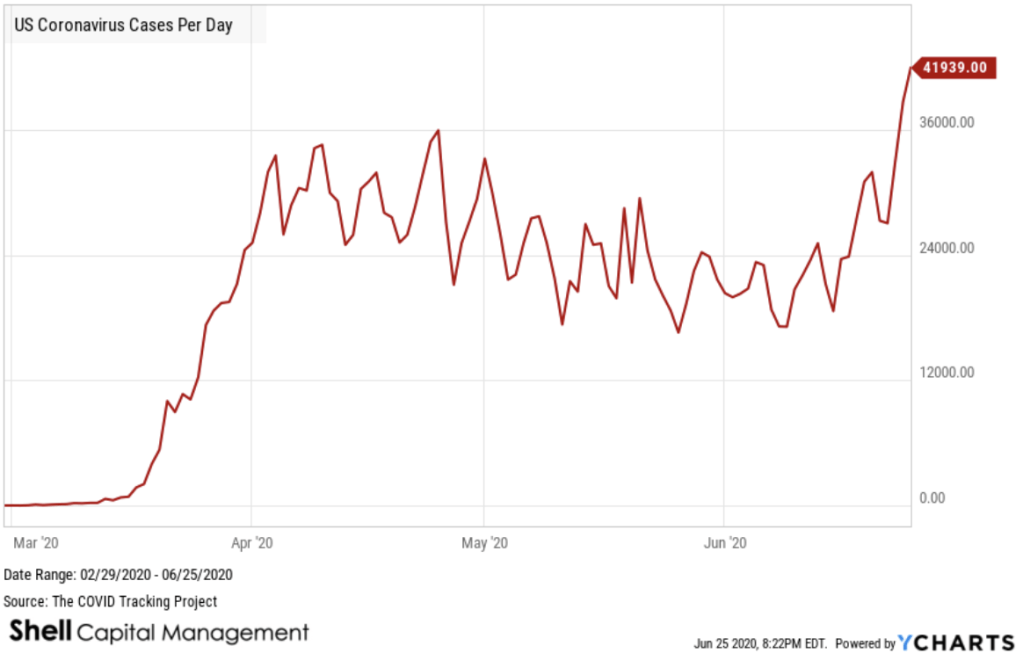

It seems like investors are probably becoming more concerned about the new uptrend in COVID 19 cases.

I don’t believe Coronavirus was the primary driver of the stock market crash in March, but it may be more of an issue now that it continues to spread.

Don’t miss out! If you want to follow along sign up for email alerts.

Join 520 other subscribers

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

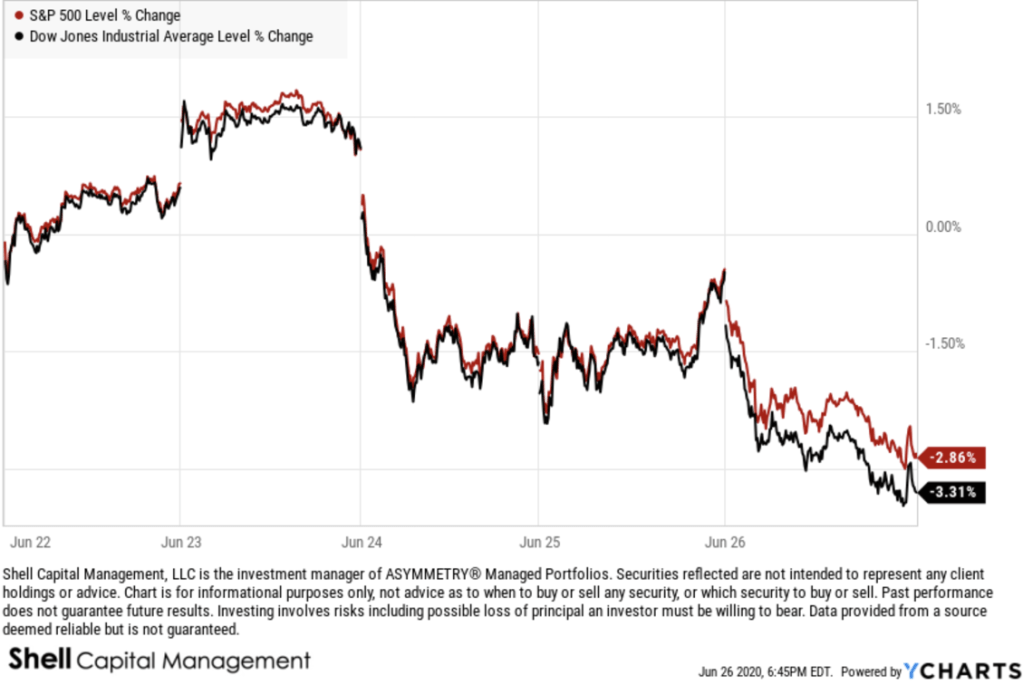

Indeed, the stock market indexes seem to be reflecting something negative today.

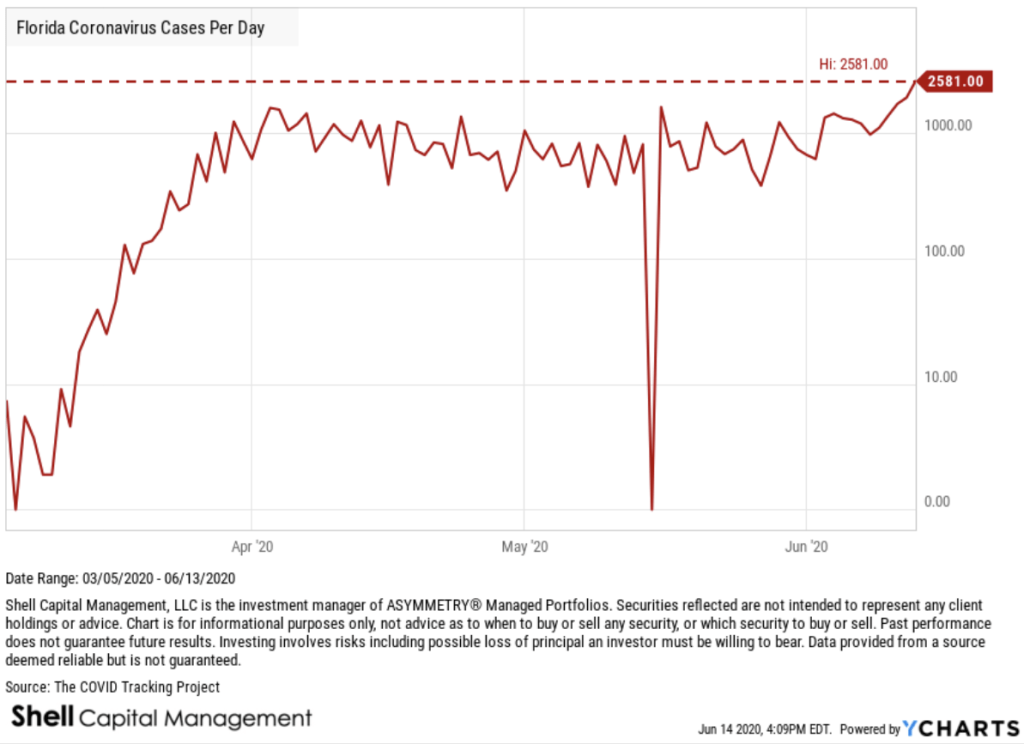

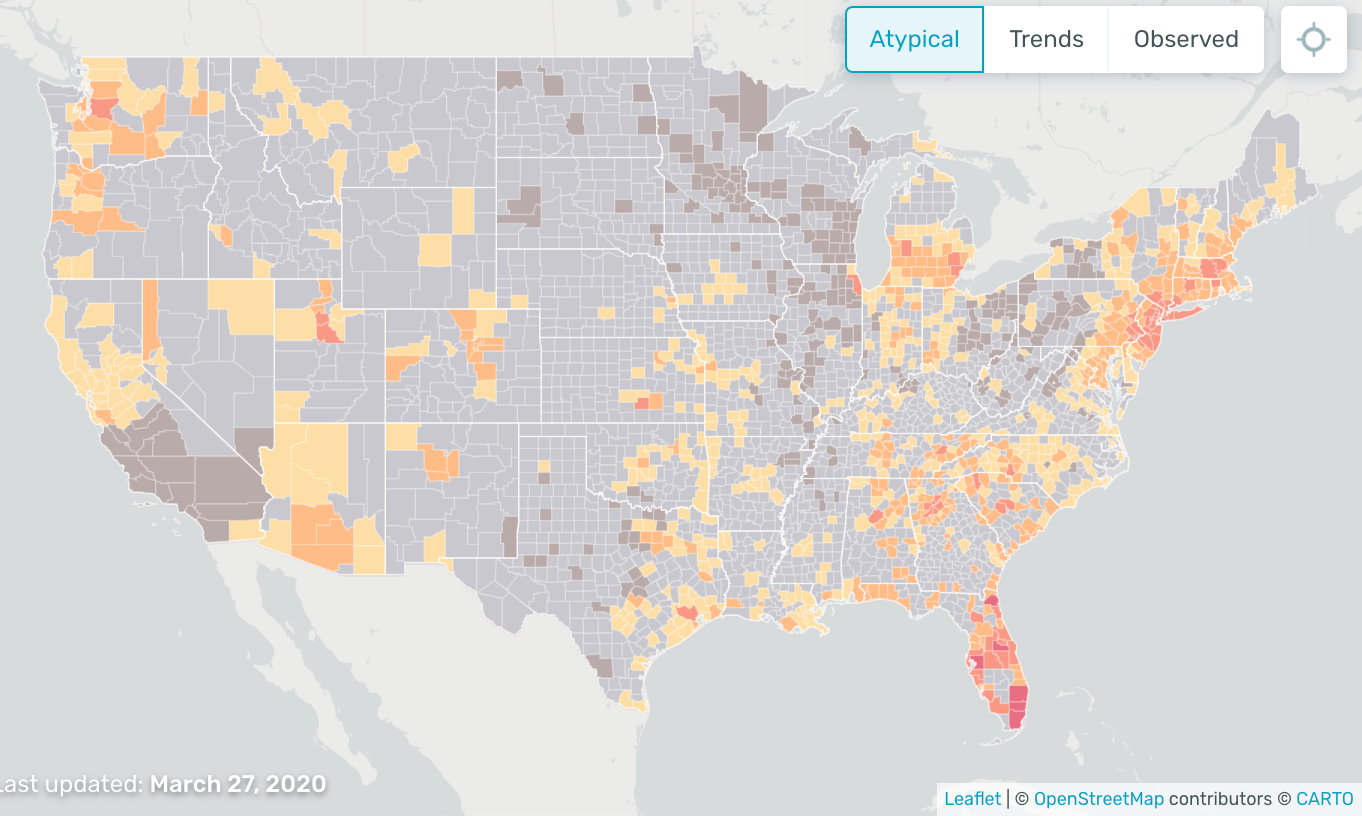

I’m guessing it may be the uptrend in new cases per day. For example, Florida has reached a significant new high.

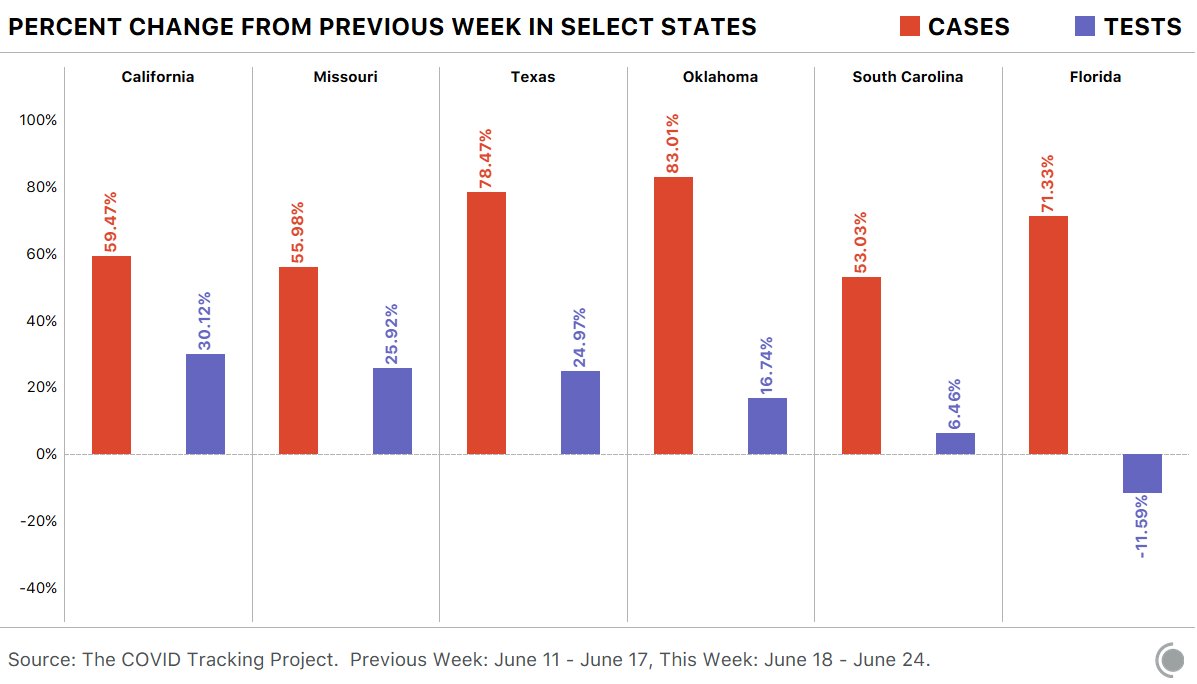

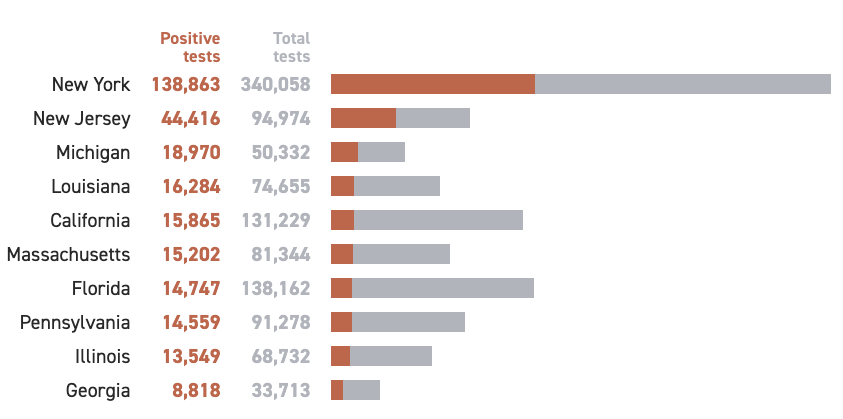

As I’ve been saying for the past two weeks, the new uptrend breakout in cases per day is NOT driven by more testing. Below is a sample of the states with the highest new cases, and as you can see, the bars show the percent increase in new cases and testing.

This is NOT the kind of asymmetry I like to see.

Considering the elevated risk level in the stock market by my measures, it is likely we’ll see more downside for stocks.

So, we have been positioned in long U.S. Treasuries for over a week.

Join 520 other subscribers

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Macroeconomics is a branch of economics dealing with the performance, structure, behavior, and decision-making of an economy as a whole. Macroeconomics is the part of economics focused on the big picture: analyzing economic phenomena such as interest rates, growth, unemployment, and inflation. Macro is in contrast with microeconomics, the study of the behavior of individual markets, workers, households, and firms. Macroeconomic phenomena are the product of all the microeconomic activity in an economy.

Global is relating to, or involving, the whole world, not just one country or state.

Global Macroeconomics, or Global Macro, then, is looking at the whole world for trends and behavior of big picture trends.

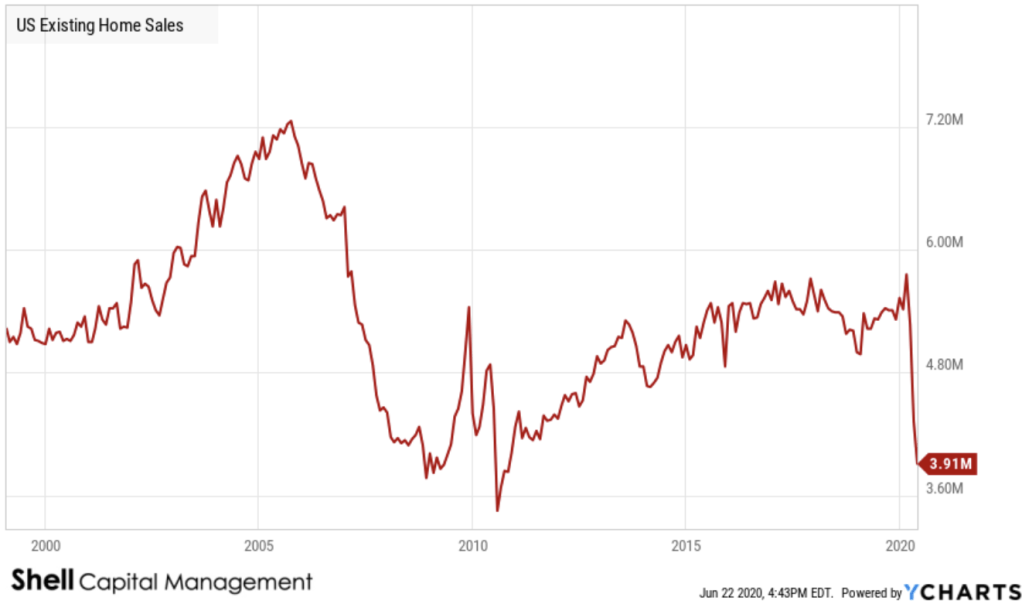

US Existing Home Sales reflects the total unit sales of US homes that are already built. It is a lagging indicator tracking the US housing market, which is impacted by changes in mortgage rates. Historically, US Existing Home Sales declined to a trough of 3.77 million units sold in November 2008 as foreclosures increased and home values fell during the US Housing Crisis.

US Existing Home Sales is at a current level of 3.91M, down from 4.33M last month and down from 5.33M one year ago. This is a change of -9.70% from last month and -26.64% from one year ago.

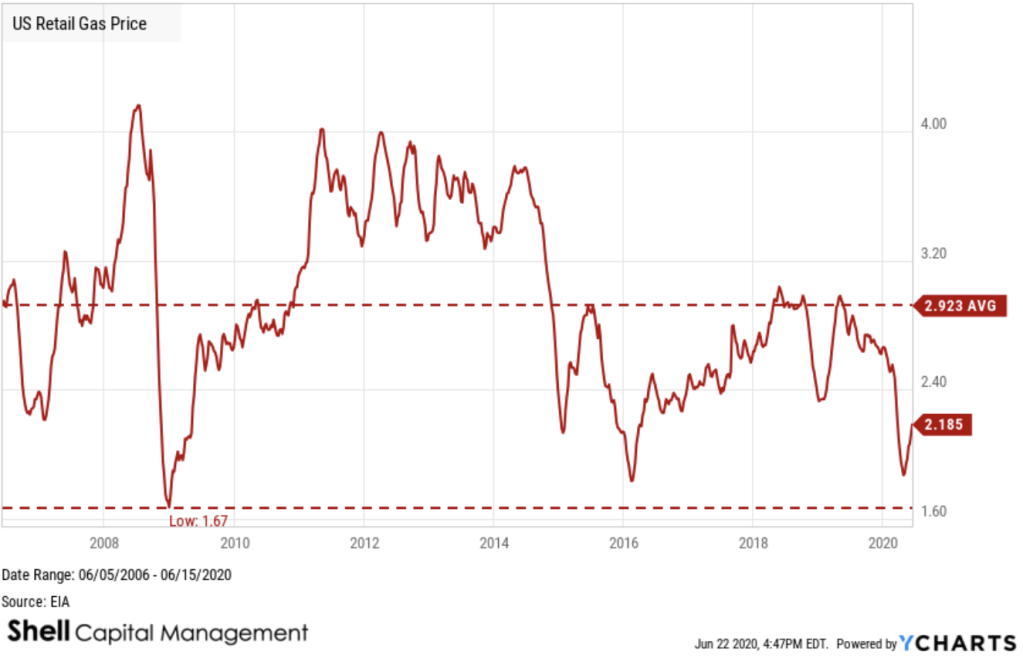

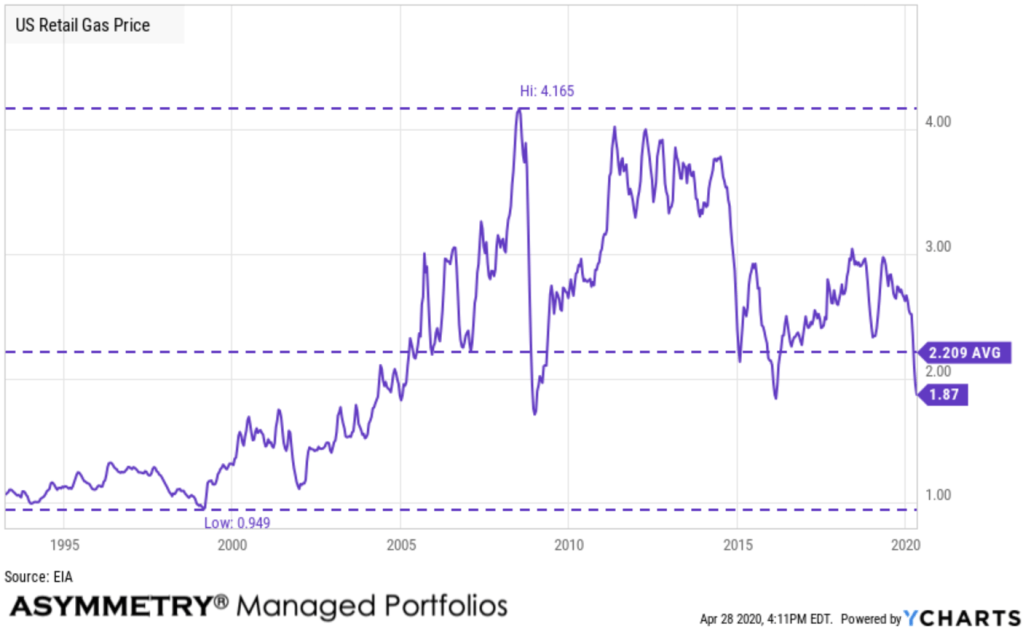

The US Retail Gas Price is the average price that retail consumers pay per gallon, for all grades of gasoline. Retail gas prices are important to view in regards to how the energy industry is performing. Additionally, retail gas prices can give a good overview of how much discretionary income consumers might have to spend.

US Retail Gas Price is at a current level of 2.185, up from 2.123 last week and down from 2.821 one year ago. This is a change of 2.92% from last week and -22.55% from one year ago. US Retail Gas Price is trending up from its recent low, which was around the same level of support gas had at prior lows of the past decade.

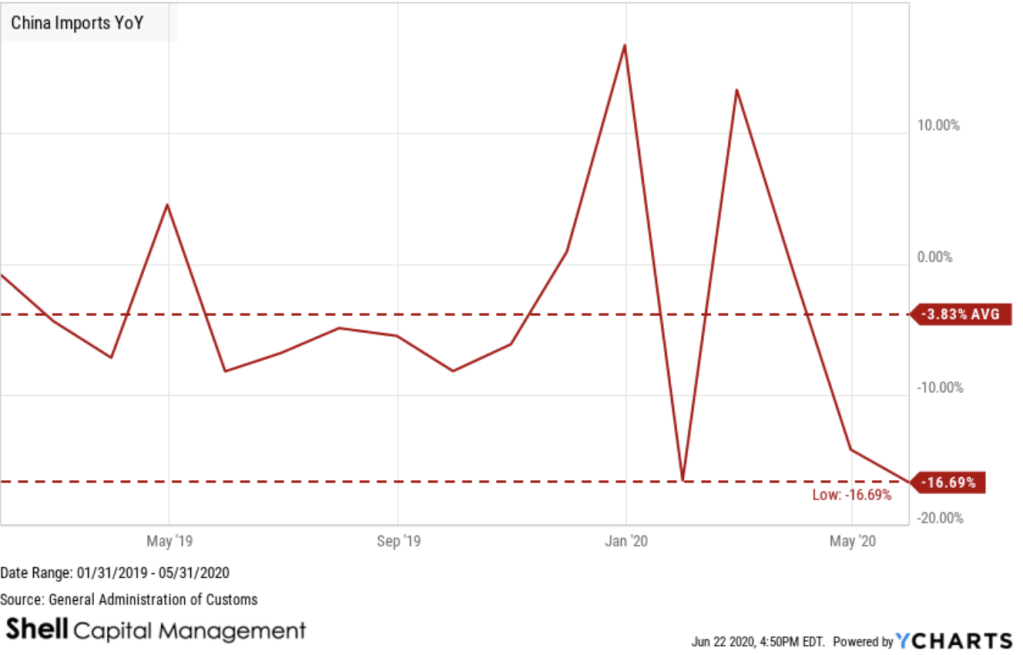

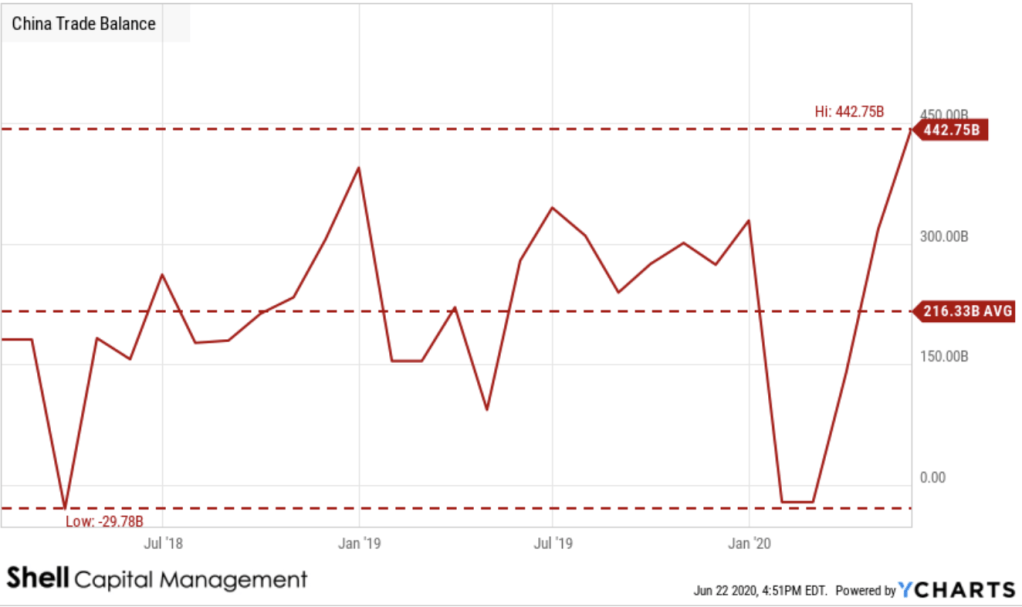

China Imports YoY is down -16.69%, compared to -14.19% last month and -8.22% last year. This is lower than the long term average of -3.83%.

China Trade Balance is at a high of 62.93B, up from 45.33B last month and up from 41.20B one year ago. This is a change of 38.82% from last month and 52.73% from one year ago.

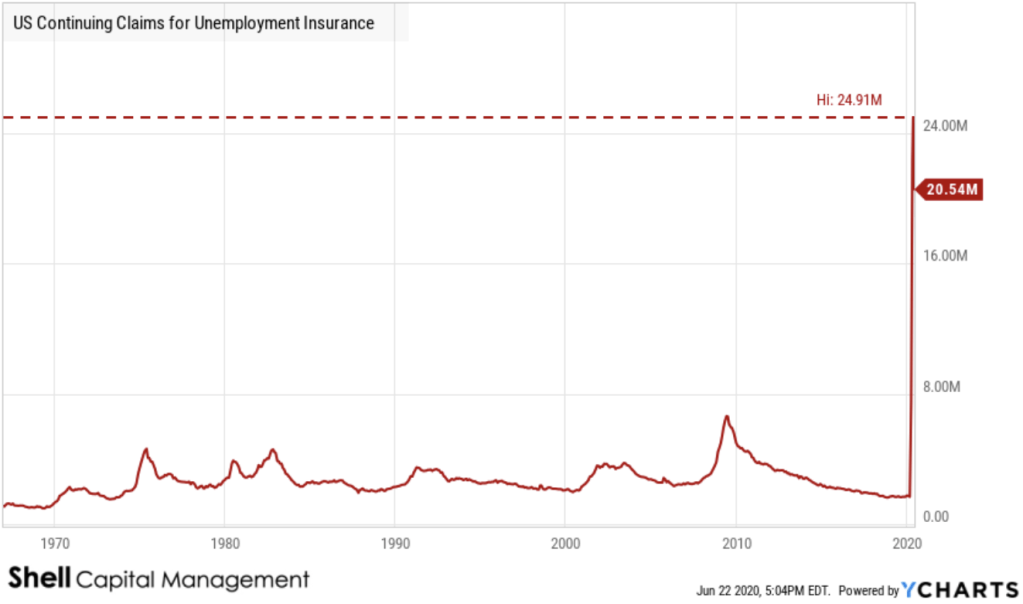

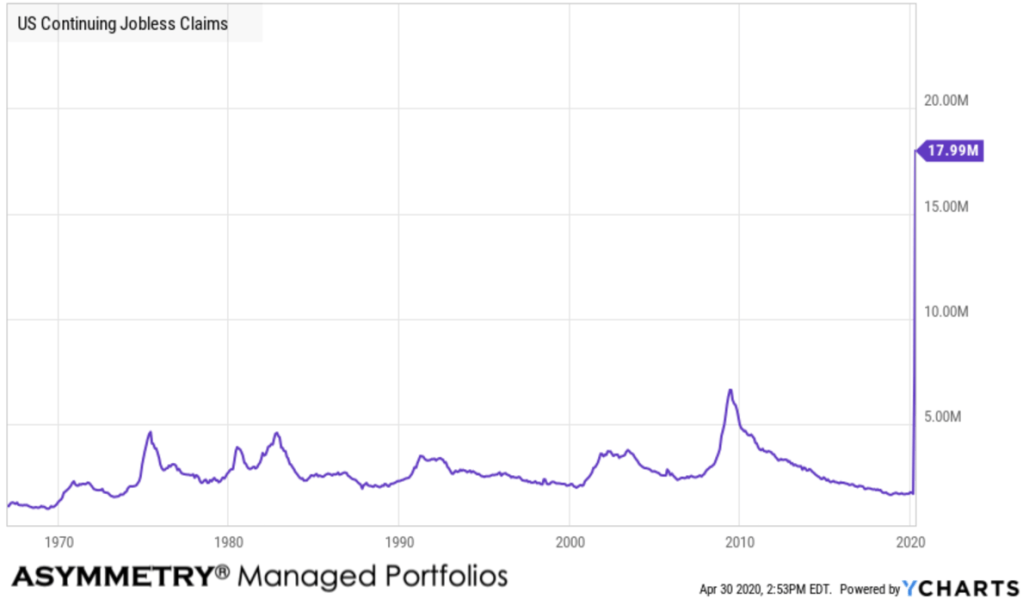

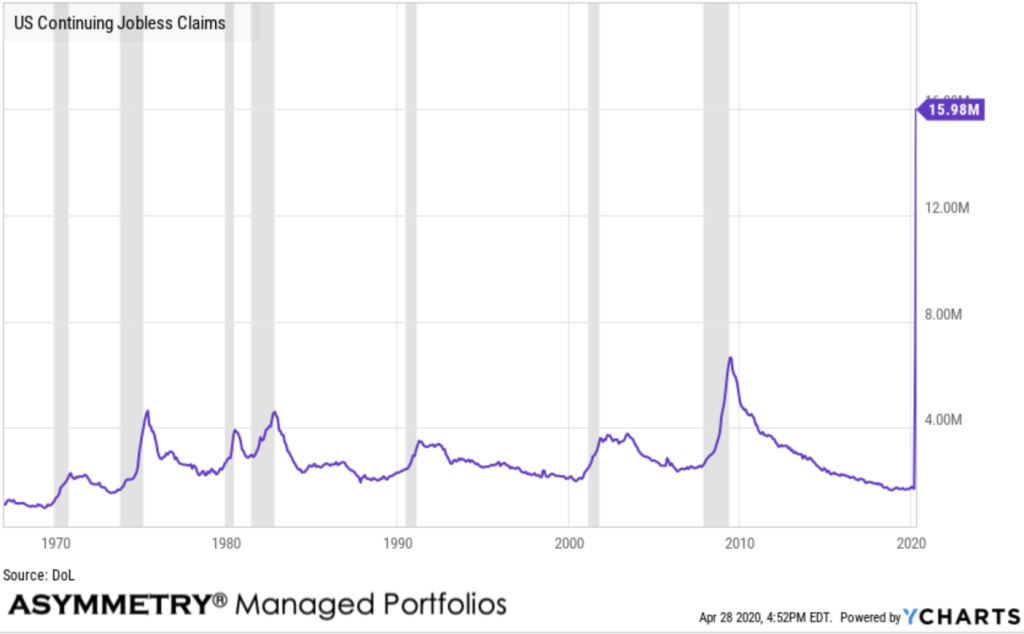

US Continuing Claims for Unemployment Insurance is at a current level of 20.54M, down from 20.61M last week and up from 1.70M one year ago. This is a change of -0.30% from last week and 1.11K% from one year ago.

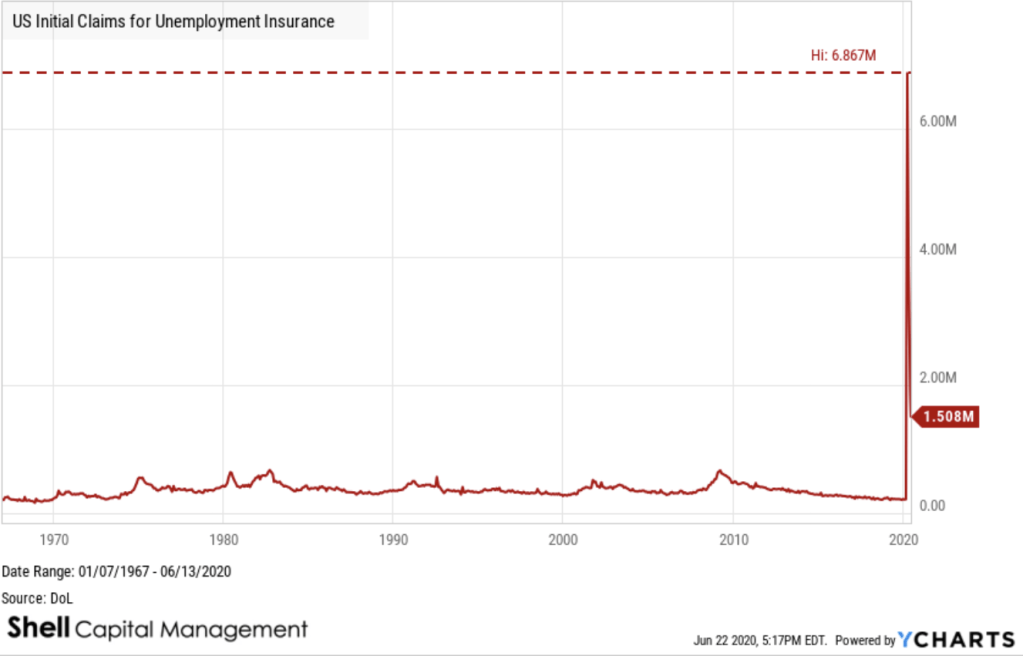

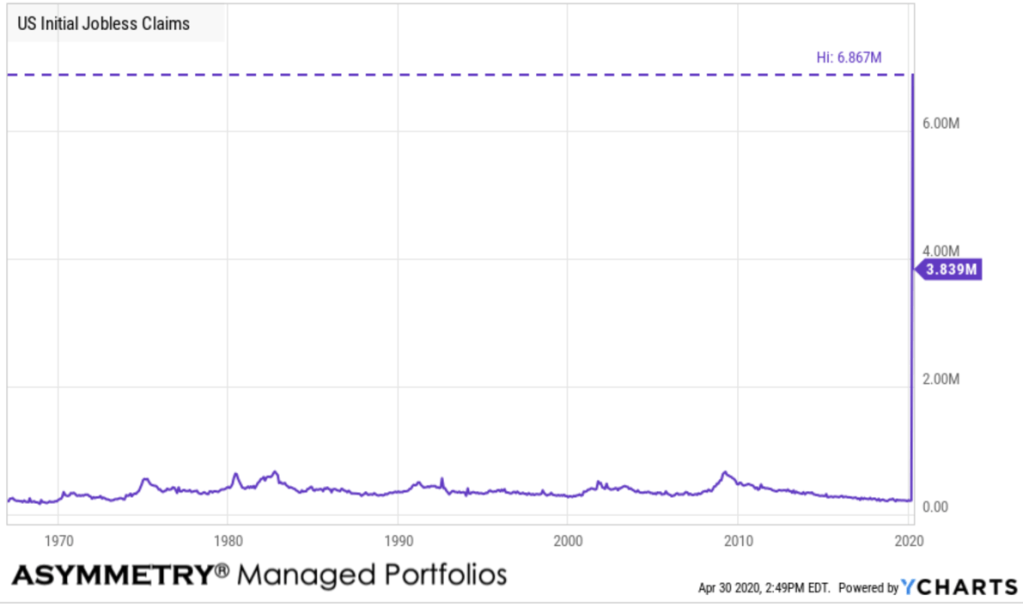

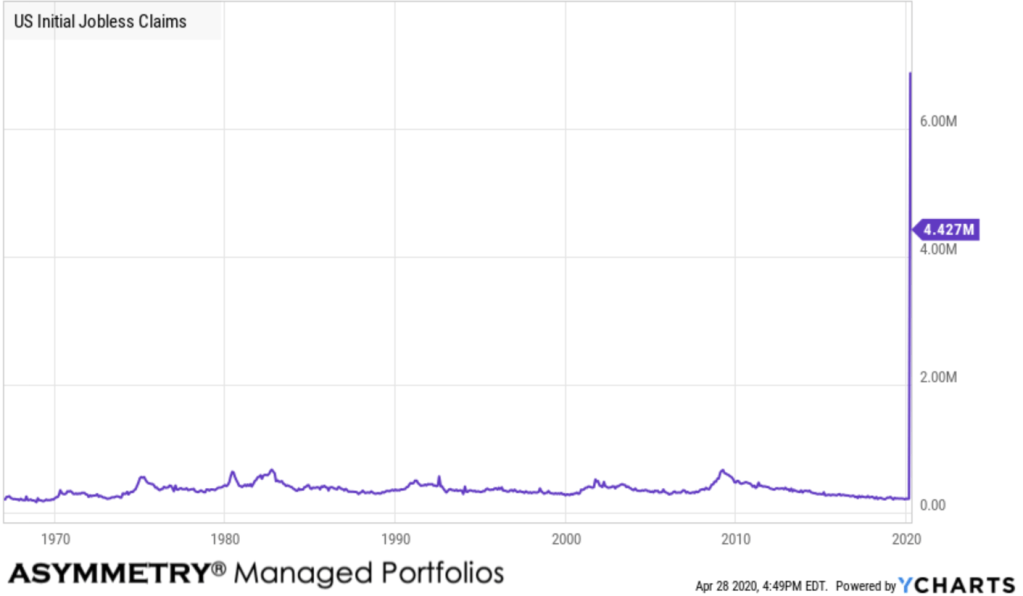

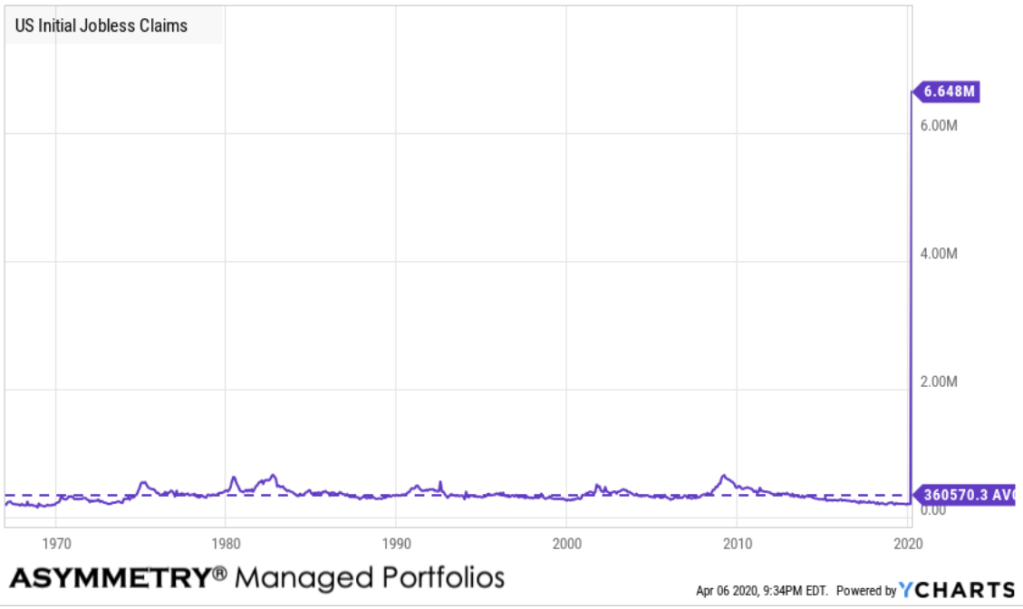

US Initial Jobless Claims, provided by the US Department of Labor, provides underlying data on how many new people have filed for unemployment benefits in the previous week. We can gauge market conditions in the US economy with respect to employment; as more new individuals file for unemployment benefits, fewer individuals in the economy have jobs. Historically, initial jobless claims tended to reach peaks towards the end of recessionary periods such as on March 21, 2009 with a value of 661,000 new filings.

US Initial Claims for Unemployment Insurance is at a current level of 1.508M, down from 1.566M last week and up from 222,000 one year ago. This is a change of -3.70% from last week and still up 579.3% from one year ago.

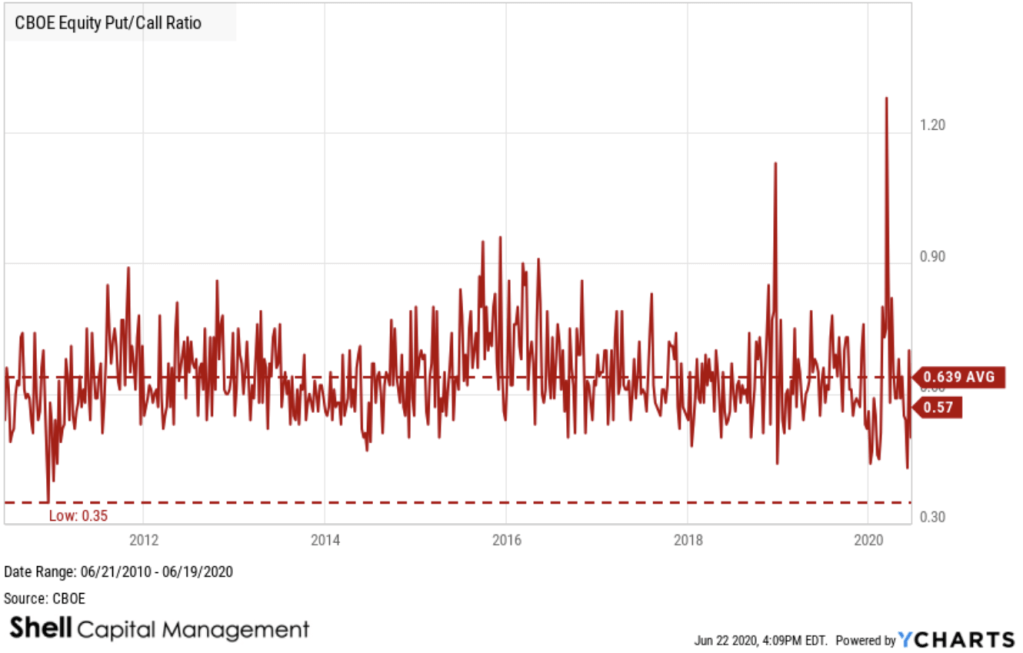

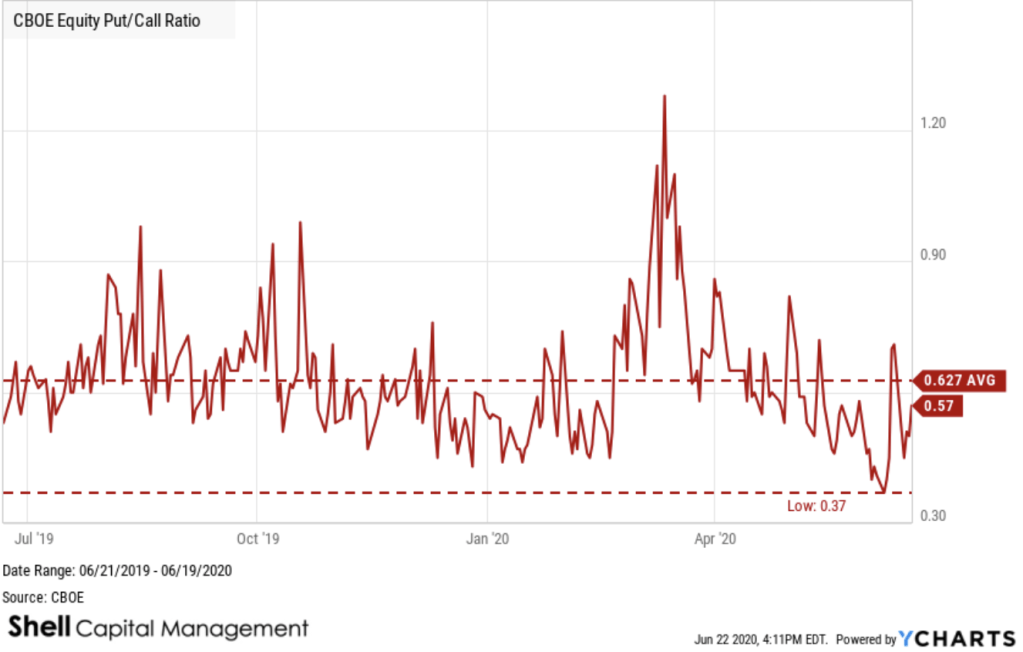

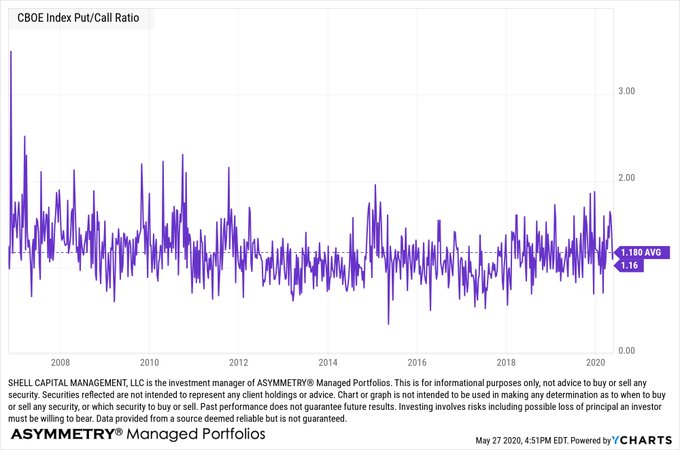

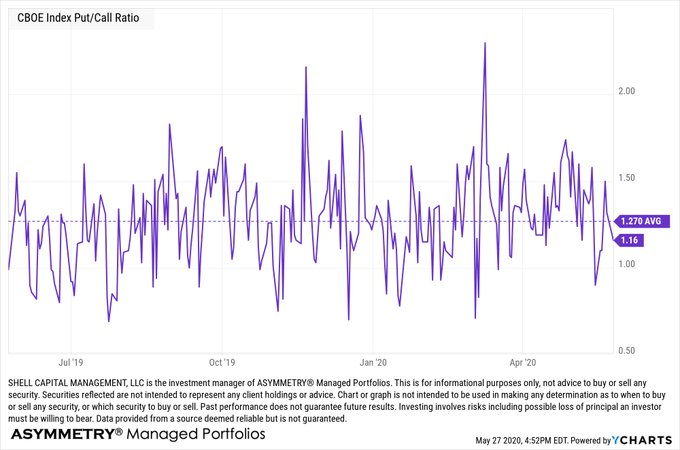

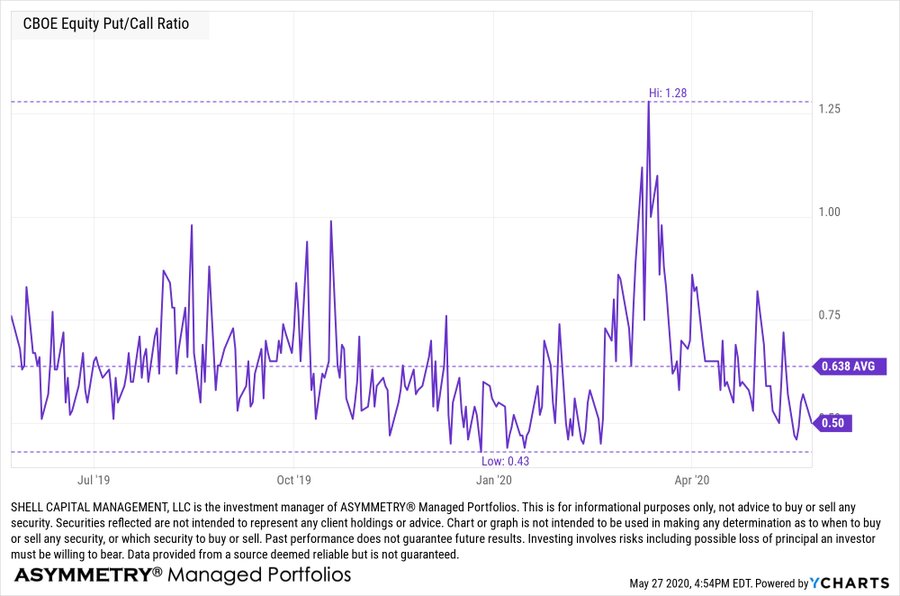

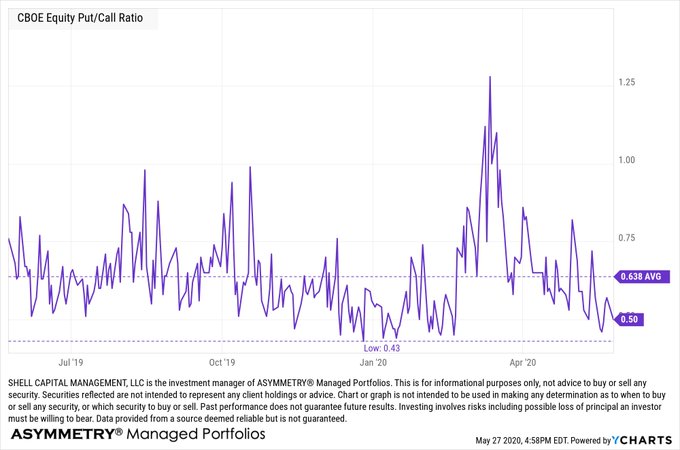

Equity option demand continues to be focused on call buying relative to put options.

The CBOE Equity Put/Call Ratio had reached a very low level, indicating options traders were mostly operating in speculative call options over put options for hedging.

“CBOE Equity Put/Call Ratio is trending toward the low level was saw before the waterfall decline in March. A falling put-call ratio, or a ratio less than 1, means that traders are buying fewer puts than calls. It suggests that bullish sentiment is building in the market.”

Shortly after, we saw a -7% decline in the stock indexes.

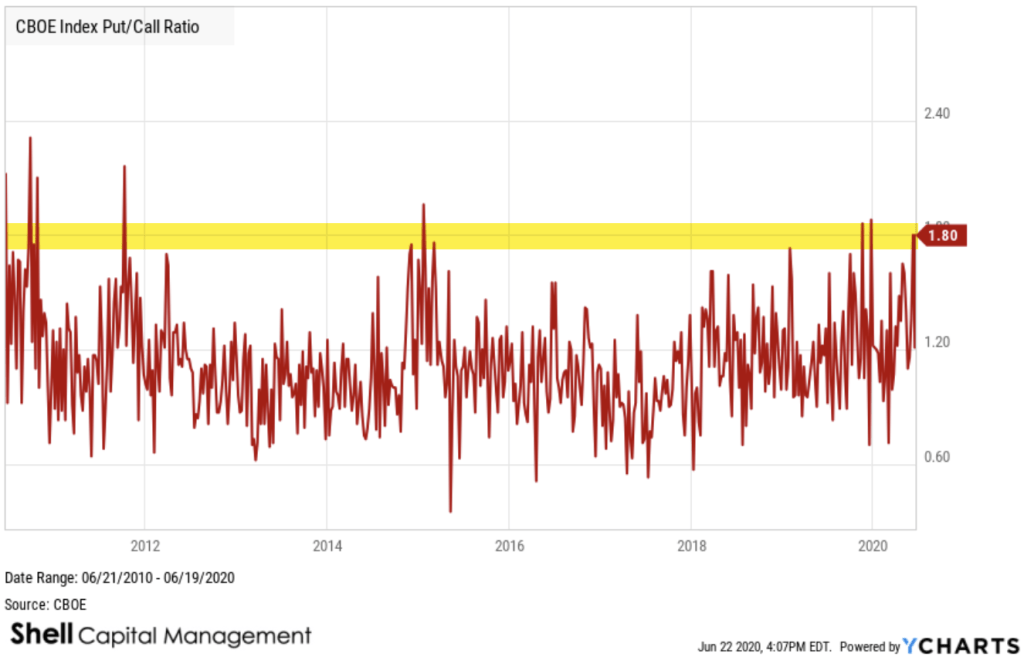

However, I’m seeing evidence of hedging now. The CBOE Index Put/Call Ratio shows a relatively high degree of hedging with put options.

Implied volatility as measured by the CBOE Volatility Index (VIX) remains very elevated, even though it declined nearly 10% today. In fact, it has mean reversed, as it does. The VIX is at its one year average.

Global Macro trends are all over the place.

Join 520 other subscribers

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

As much as I wish it wasn’t so, some important trends are in the wrong direction.

New COVID – 19 cases here in Florida are trending to a material new high.

Contrary to what some seem to blindly say; it isn’t because of more testing.

In Florida, testing slowed down 3% while new cases grew 88% over the last week.

Yesterday, Governor Ron DeSantis acknowledged that the rising number of new Covid-19 cases in Florida cannot be explained away by an increase in testing, and announced plans to step up enforcement of social distancing practices in bars and nightclubs in “DeSantis pivots on Covid-19 surge, says testing doesn’t account for spike.“

“Even with the testing increasing or being flat, the number of people testing positive is accelerating faster than that,” DeSantis told reporters during a briefing at the state Capitol. “You know that’s evidence that there’s transmission within those communities.”

Of course, it isn’t just Florida.

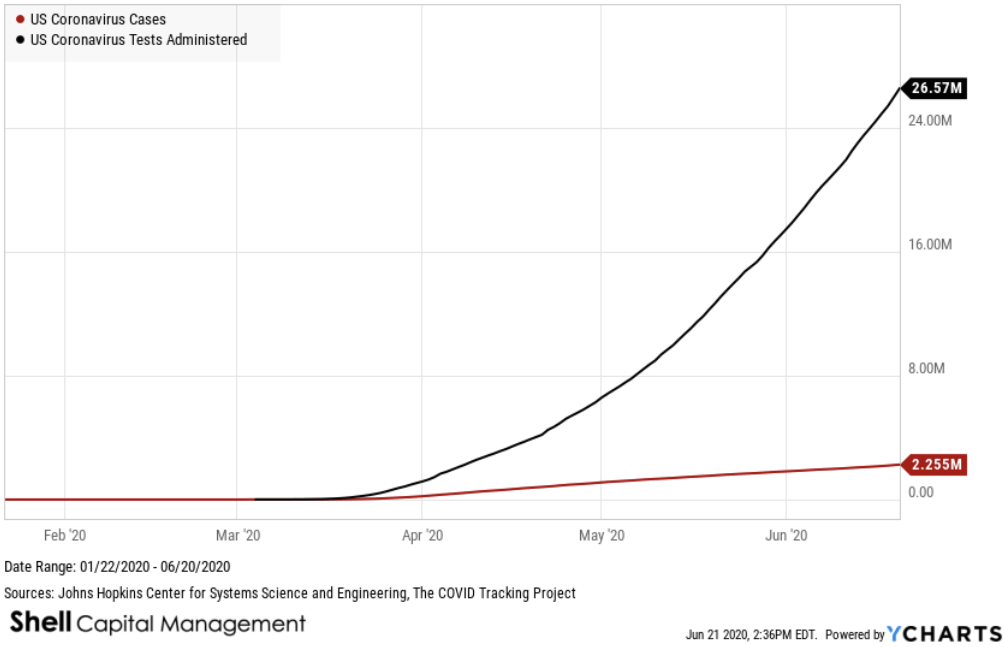

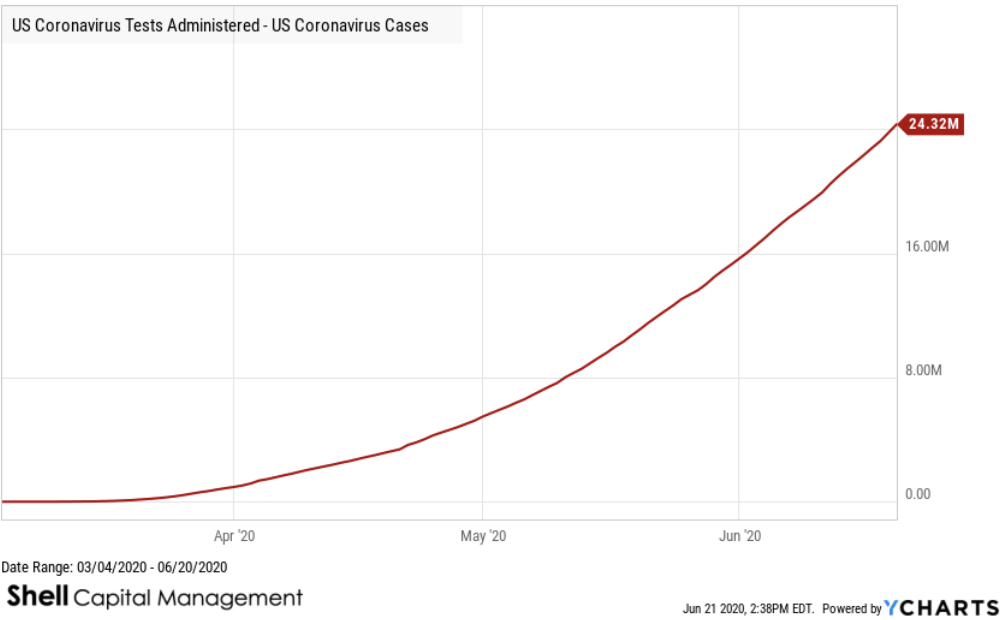

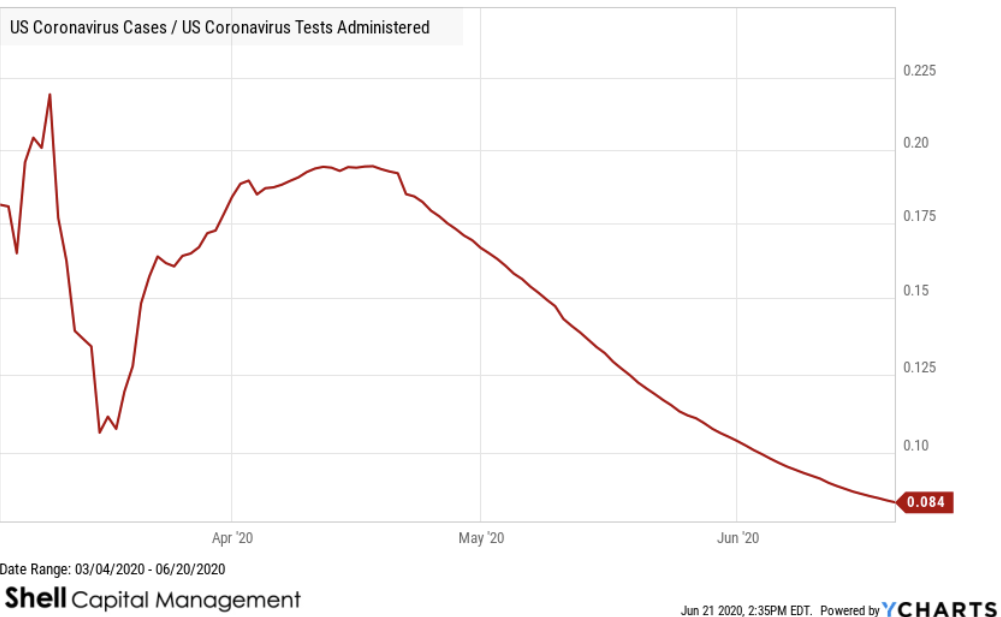

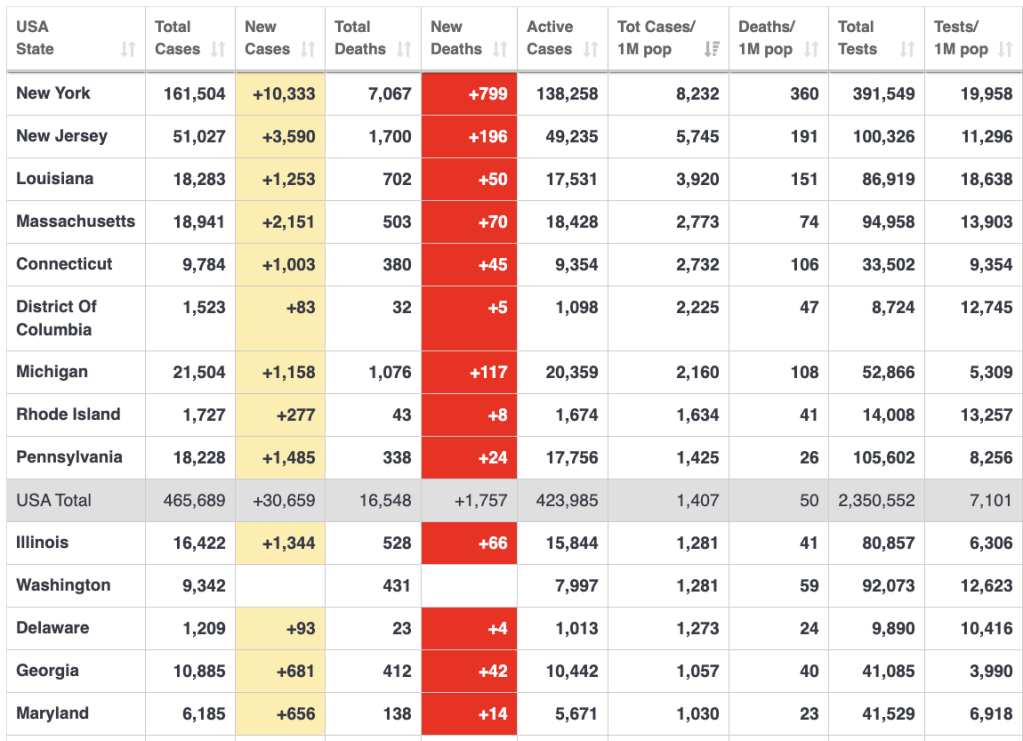

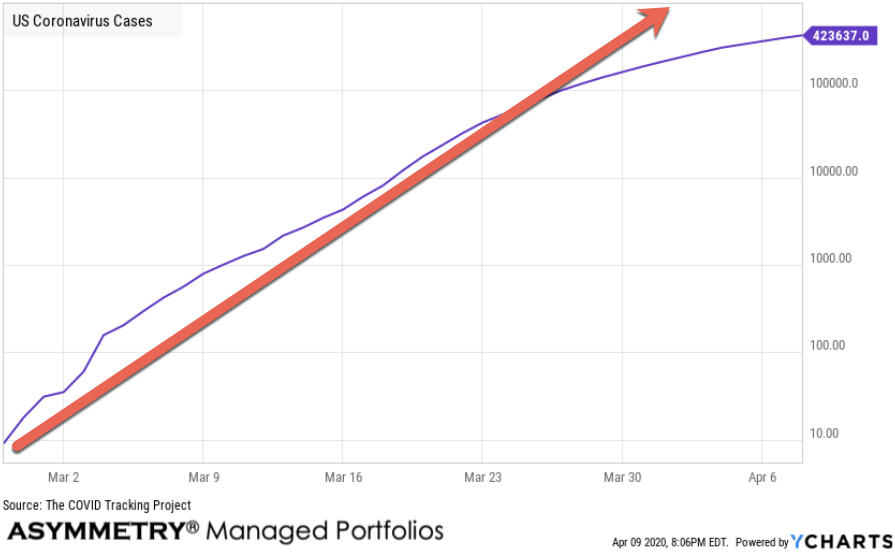

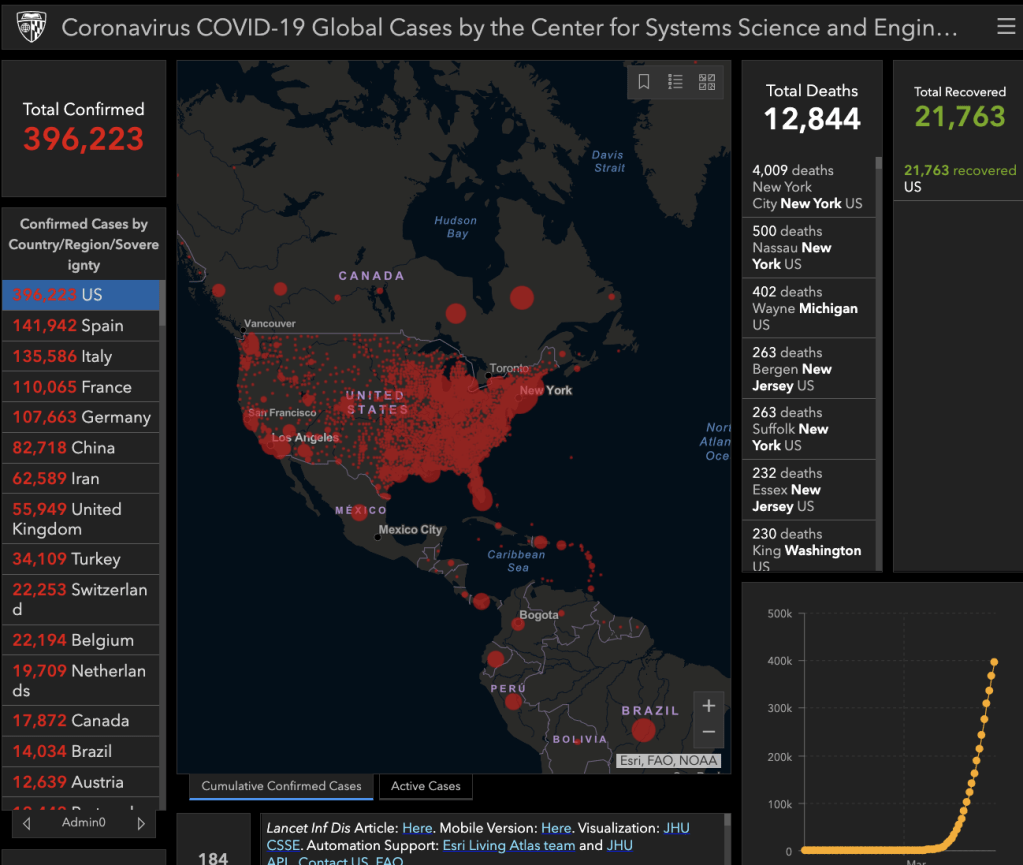

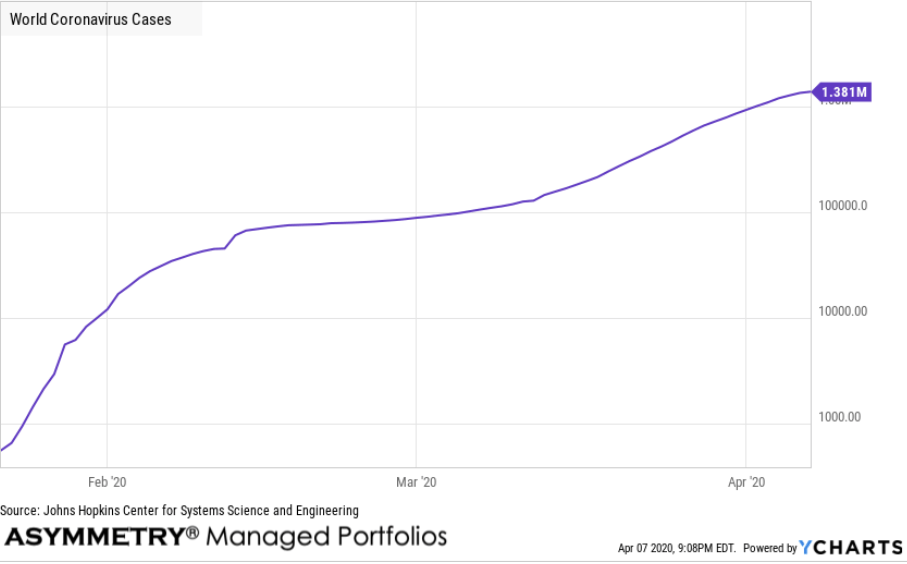

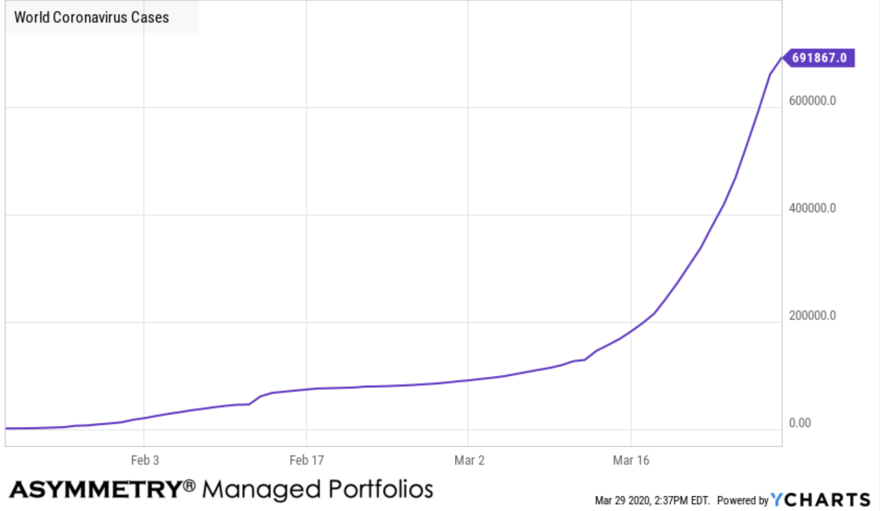

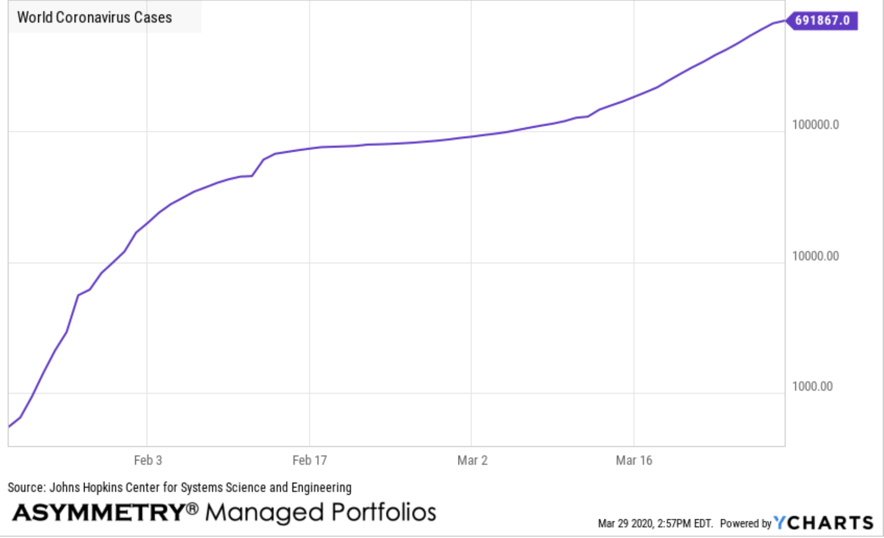

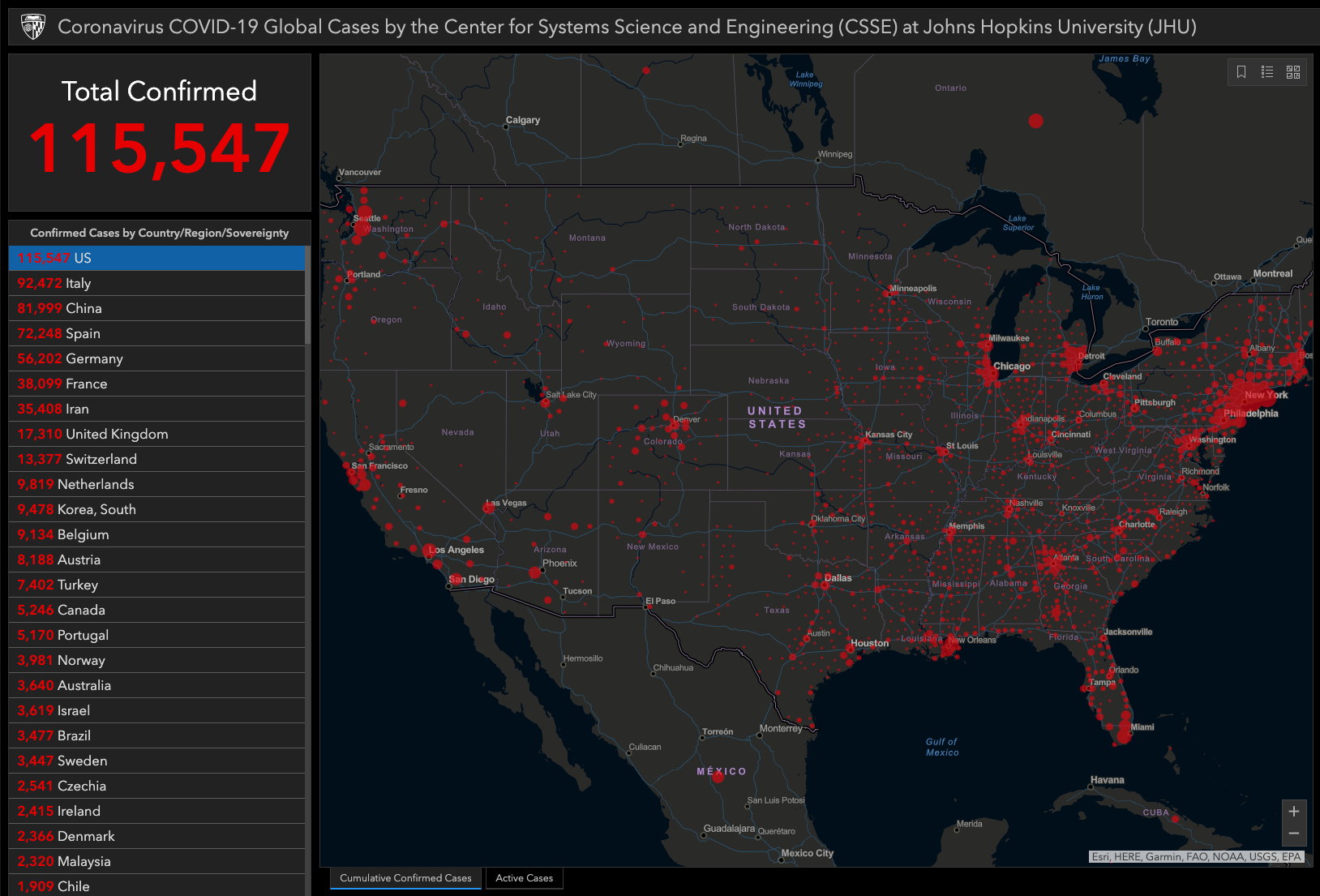

As of today, US Coronavirus Tests Administered is at a current level of 26.57 million, up from 25.98 million yesterday. It’s a change of 2.25% from yesterday.

US Coronavirus Cases is at a current level of 2.255 million, up from 2.223 million yesterday, which is a change of 1.46% from yesterday.

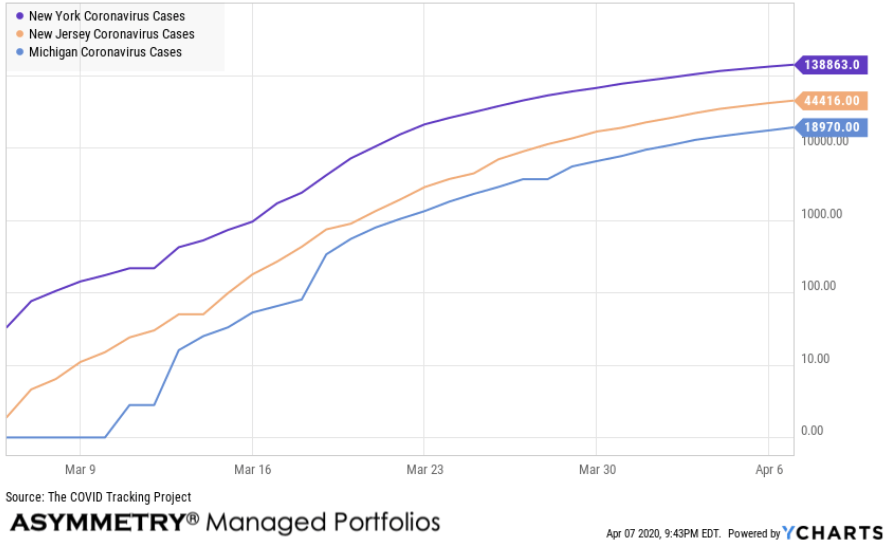

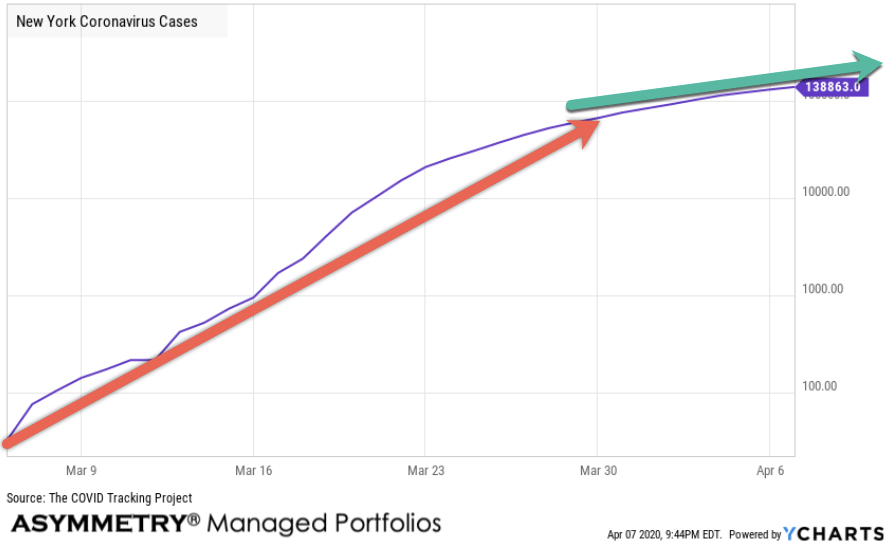

Here are the absolute trends in comparison.

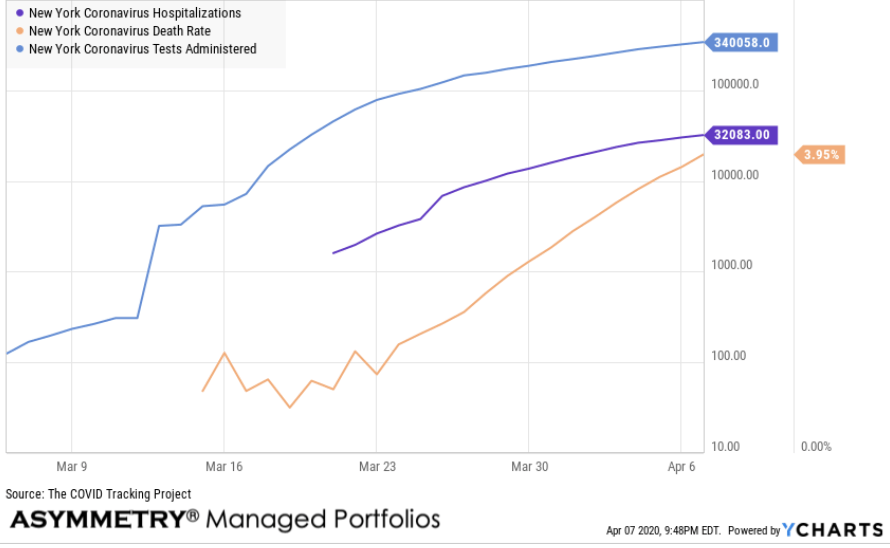

The good news is the spread between US Coronavirus Tests and Cases is in an uptrend, so negative tests overwhelm positive test results.

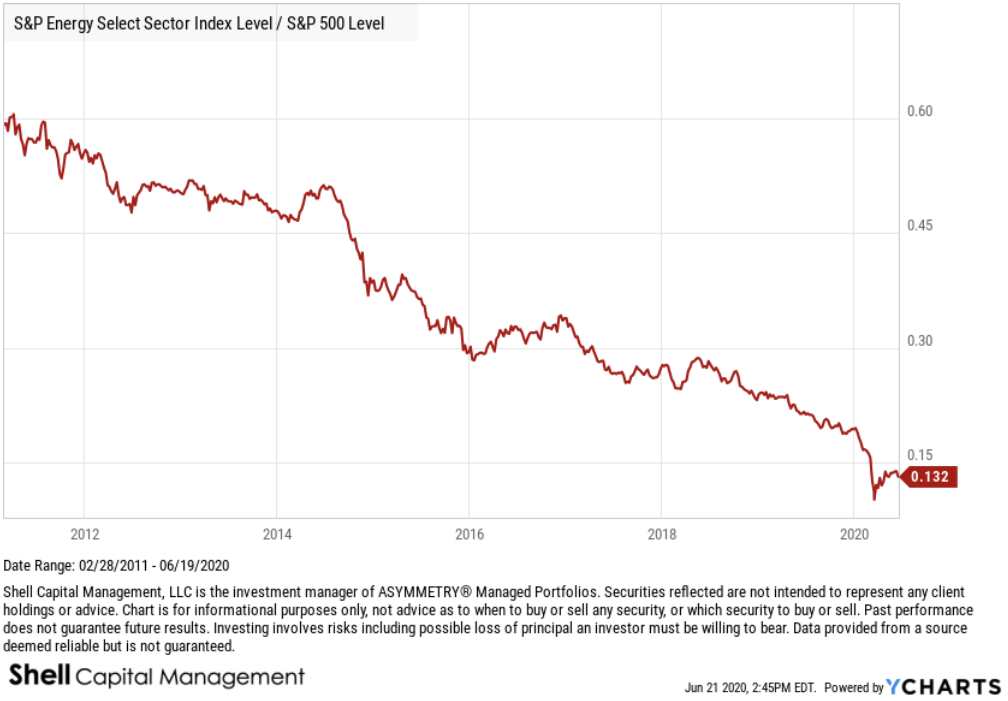

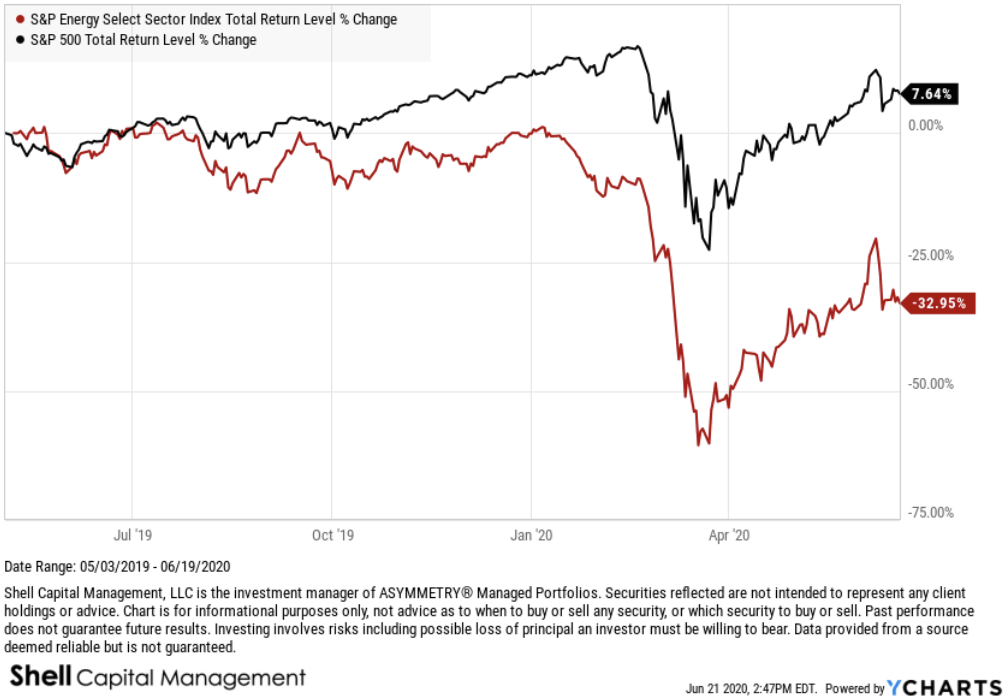

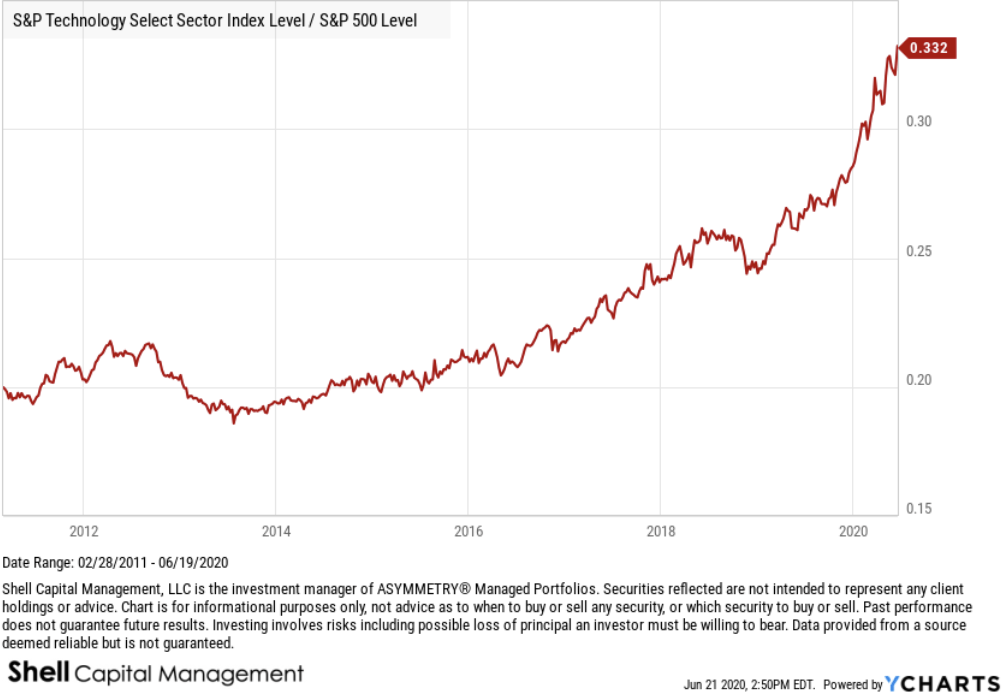

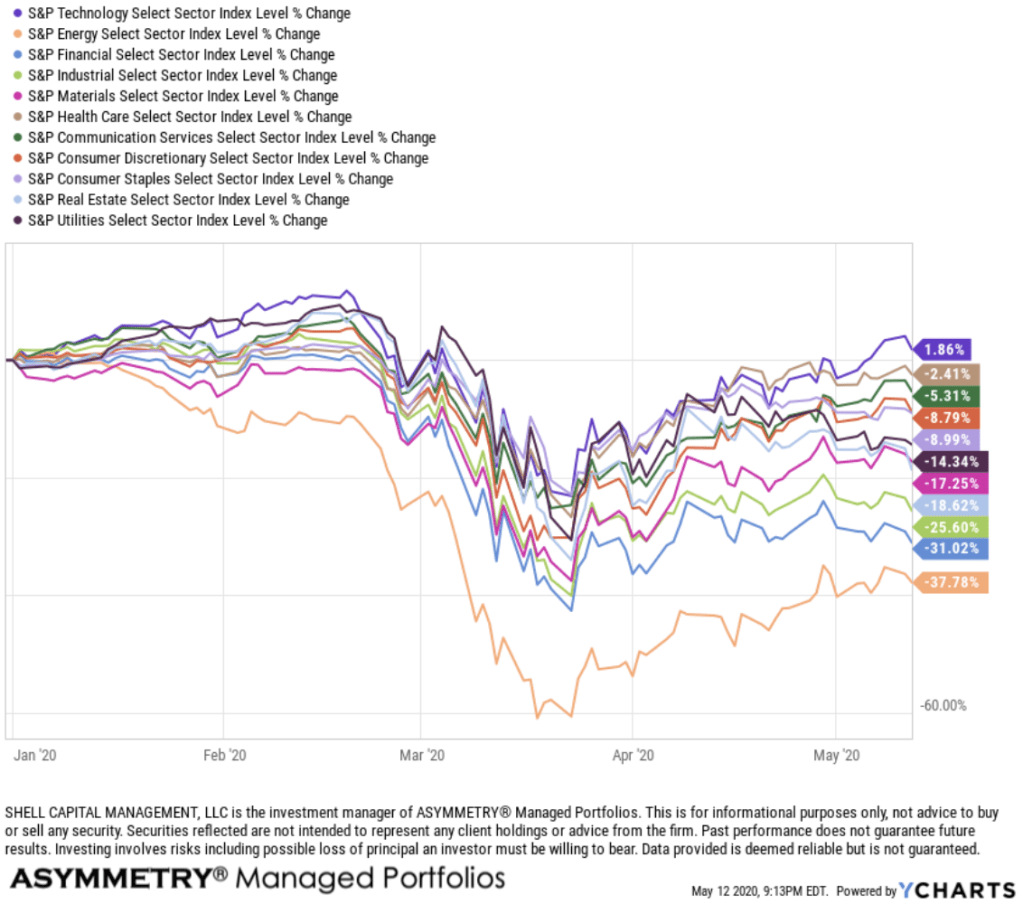

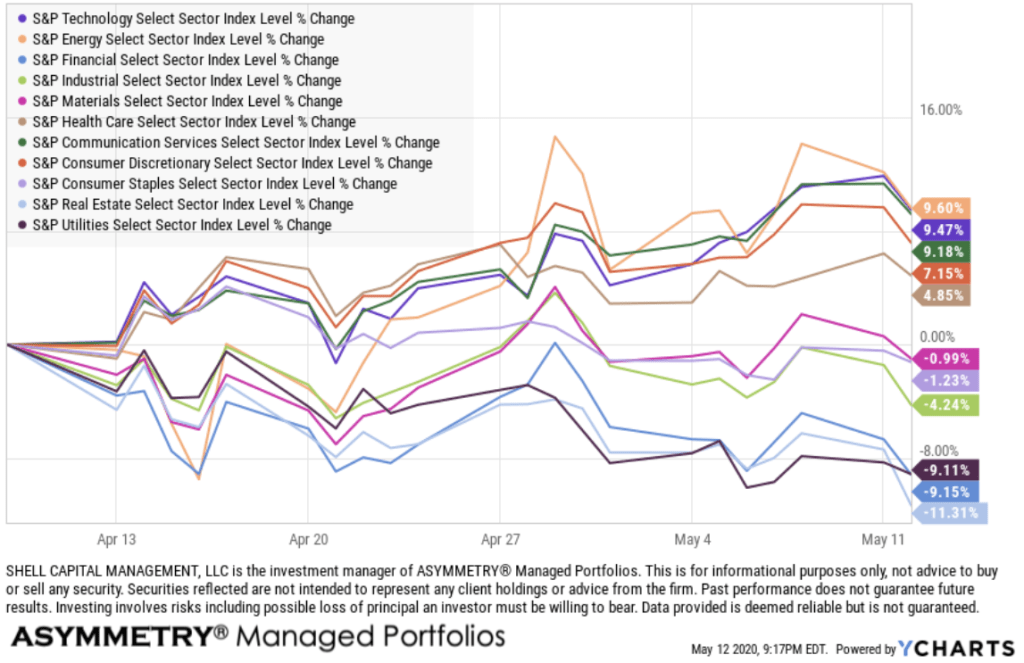

We can use a ratio chart to see the relative trend in cases and tests. I do the same with global market trends. For example, we can compare the US Energy sector to the S&P 500 to see the relative strength or weakness. When the trend is down as it is here, the sector is lagging.

Here is a simple analog chart comparison.

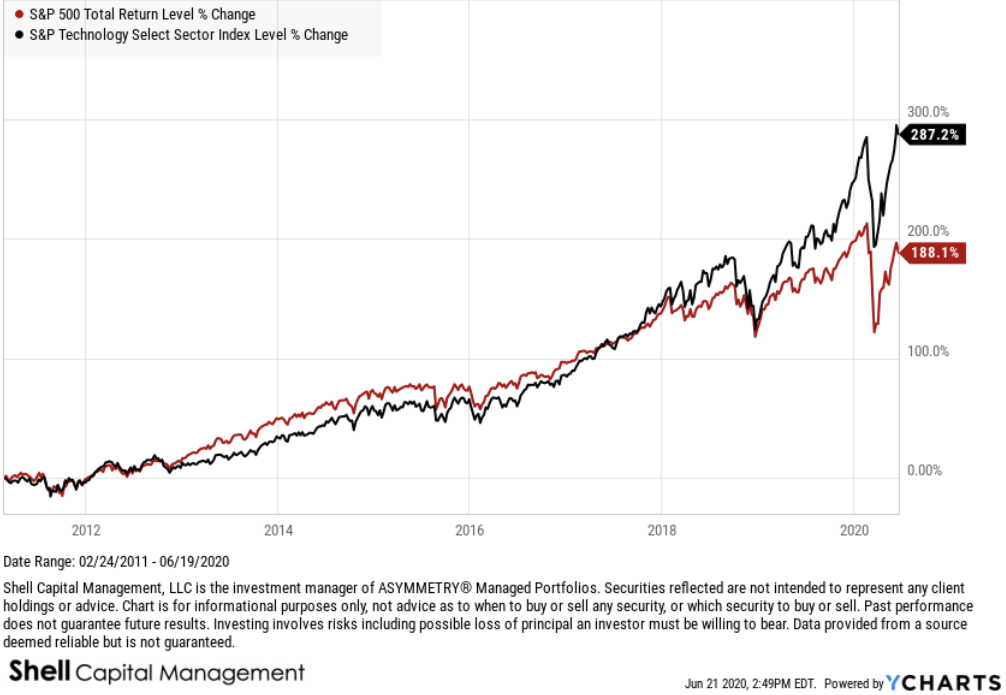

In contrast, the Technology sector has been relatively stronger than the S&P 500 stock index.

And the relative strength ratio between Technology and the broader stock market index shows the opposite trend than what we saw from Energy.

So, back to the COVID trend, taking this same ratio methodology applied to tests and cases, the relative trend is down, so cases are lagging tests by a material amount. We want to see this trend continue.

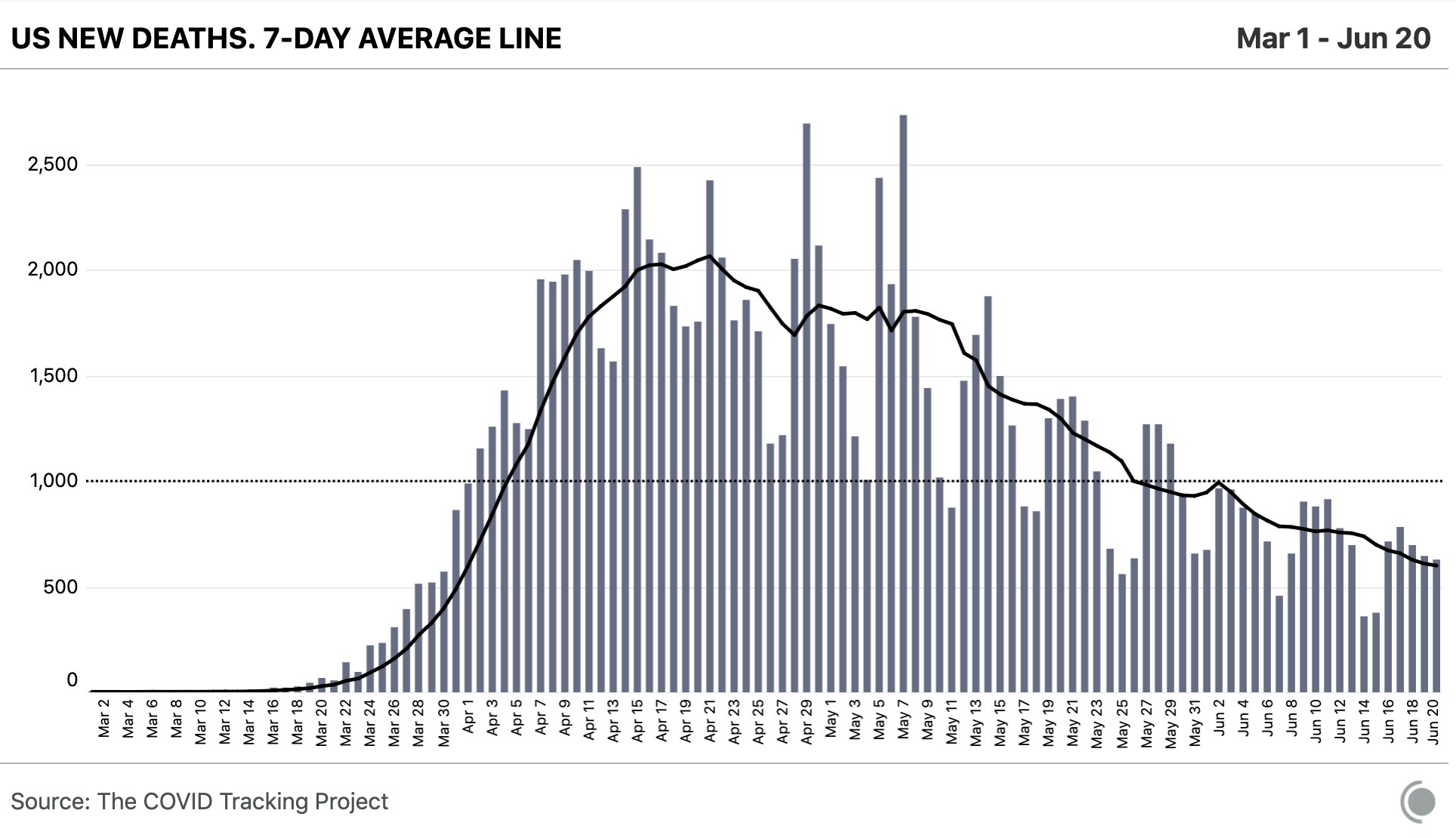

So far, states have reported 630 deaths and the trend is down, so we are seeing a national decline. Death reporting lags approximately 28 days from symptom onset, according to CDC models that consider lags in symptoms, time in hospital, and the death reporting process.

So, that’s the good news.

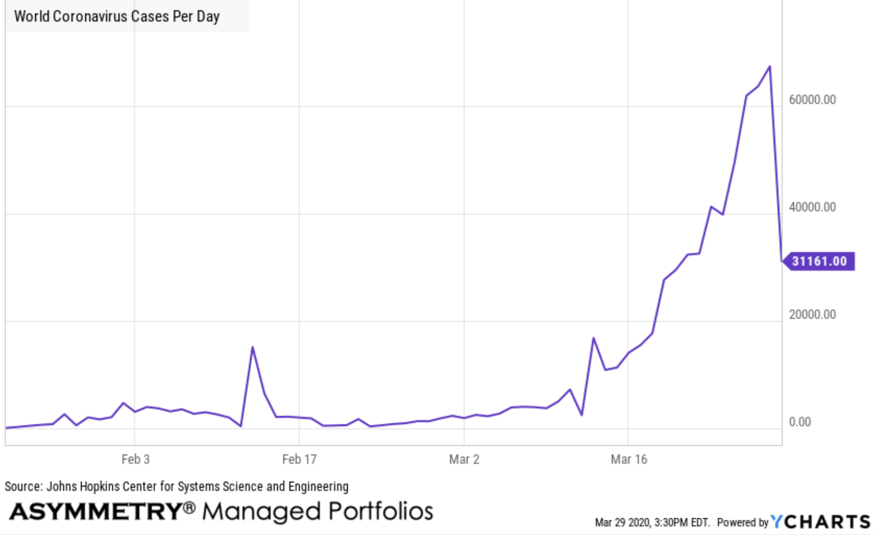

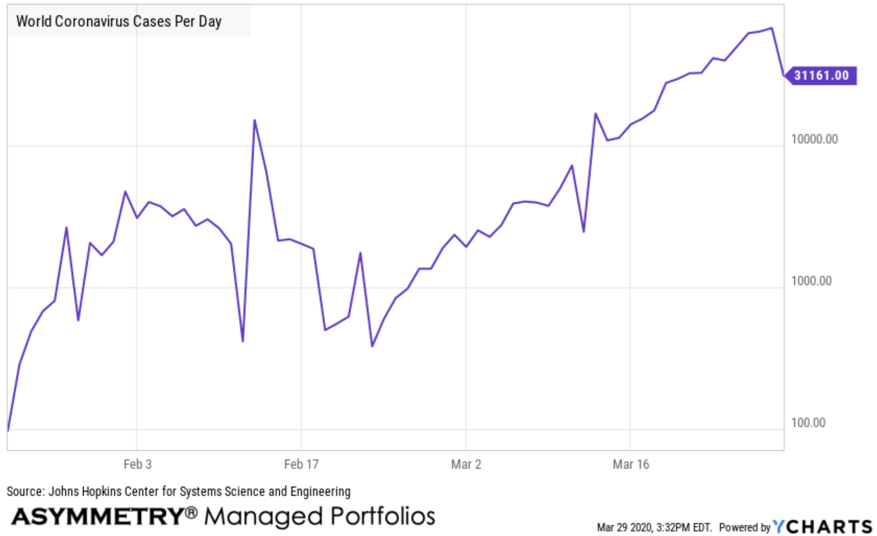

What I believe people will increasingly focus on is the breakout in new cases per day. Many trackers are normalizing the trend with a 7 day moving average, but the data already has a natural lag between contraction, testing, a positive case, so I’m not adding one myself.

Instead, I want to see a new breakout as soon as it develops. If we wait for a 7 day moving average new high, the lag will delay noticing the breakout.

I pointed out over a week ago I’m seeing new breakouts to the upside.

I’m still seeing new breakouts in cases per day.

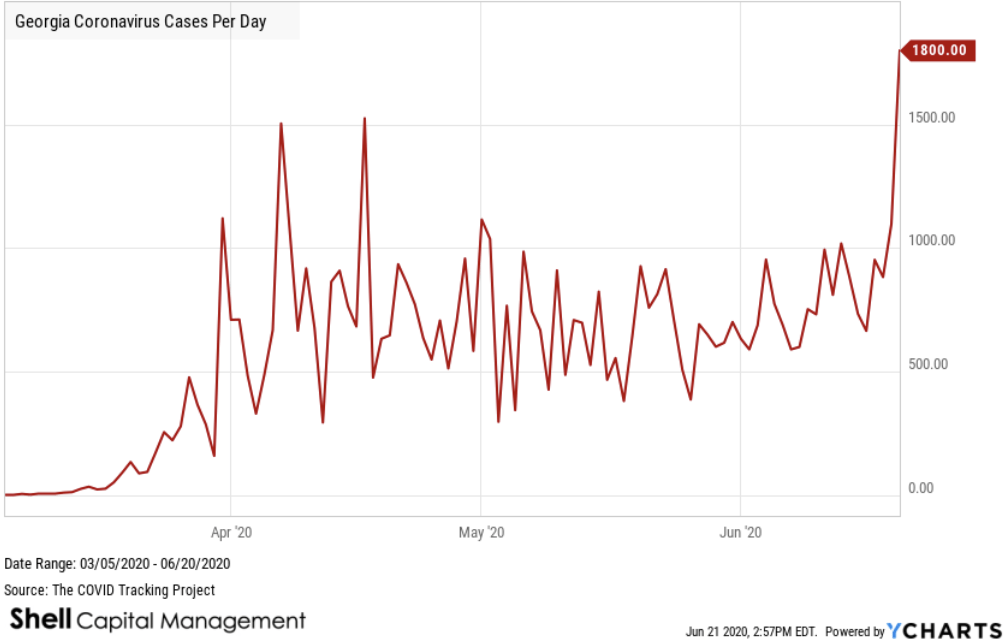

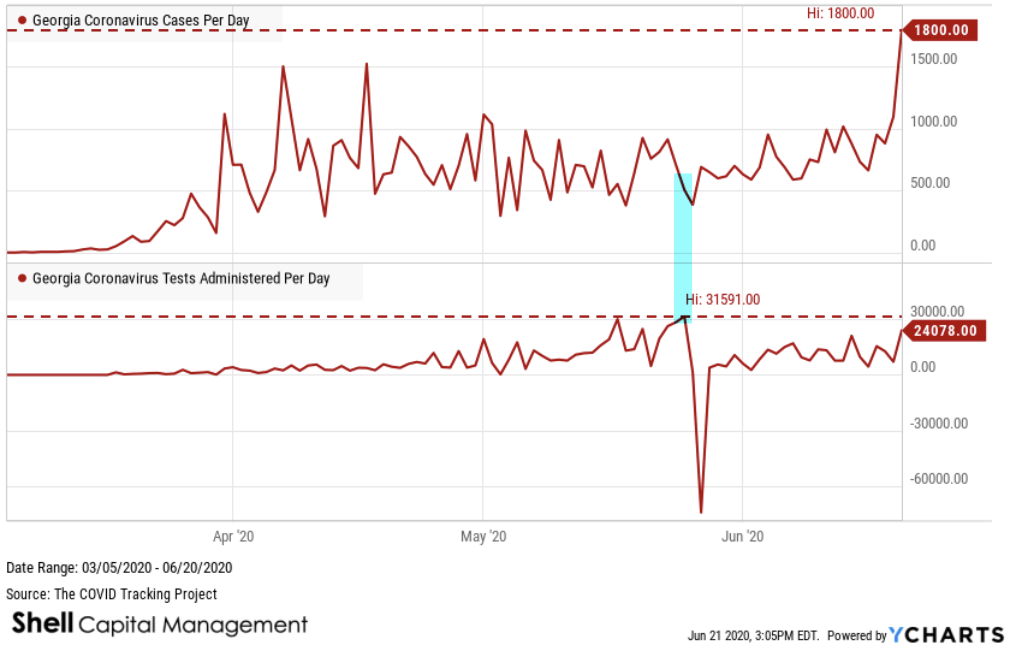

I pointed out Florida, Arizona, and Texas. Now add Georgia.

And it isn’t just more testing in Georgia.

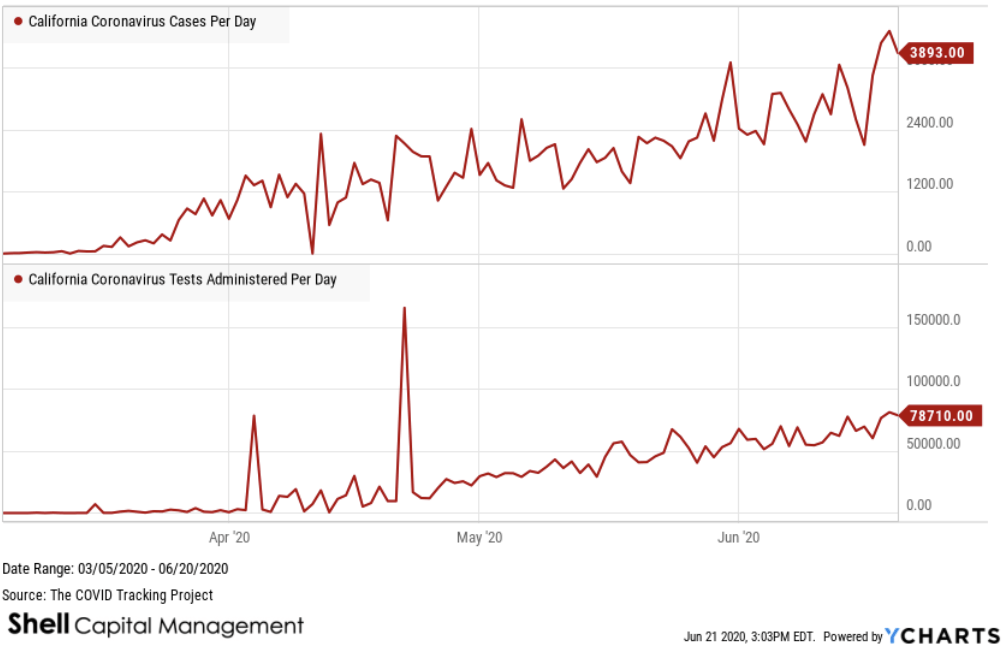

California is still trending up, and although their testing is rising, it isn’t just an increase in tests.

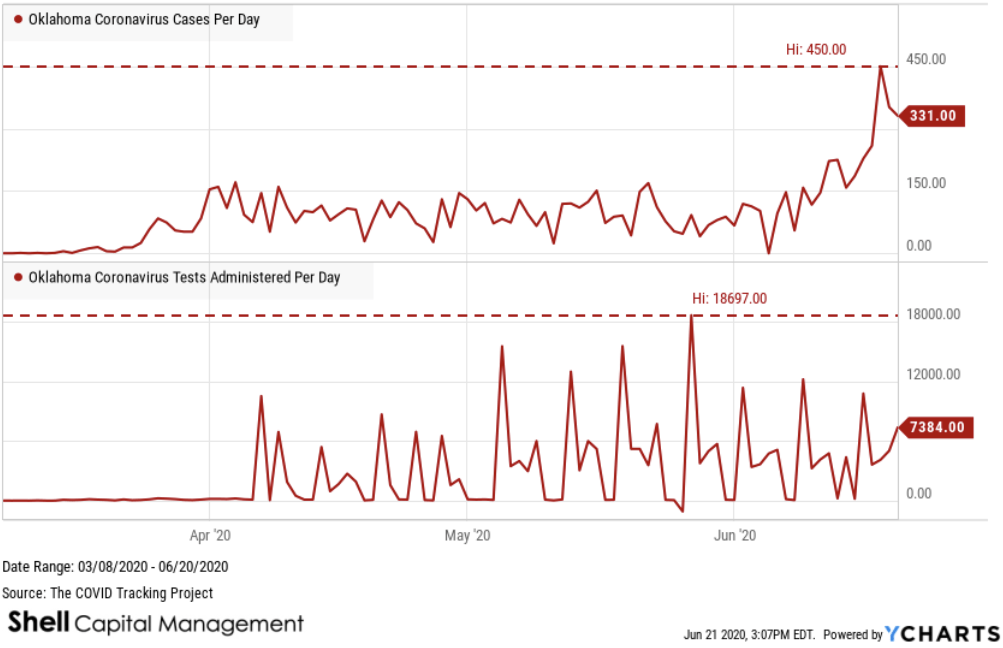

Oklahoma cases have now broken out into an uptrend. Again, the new high in cases per day doesn’t correspond to a new high in testing.

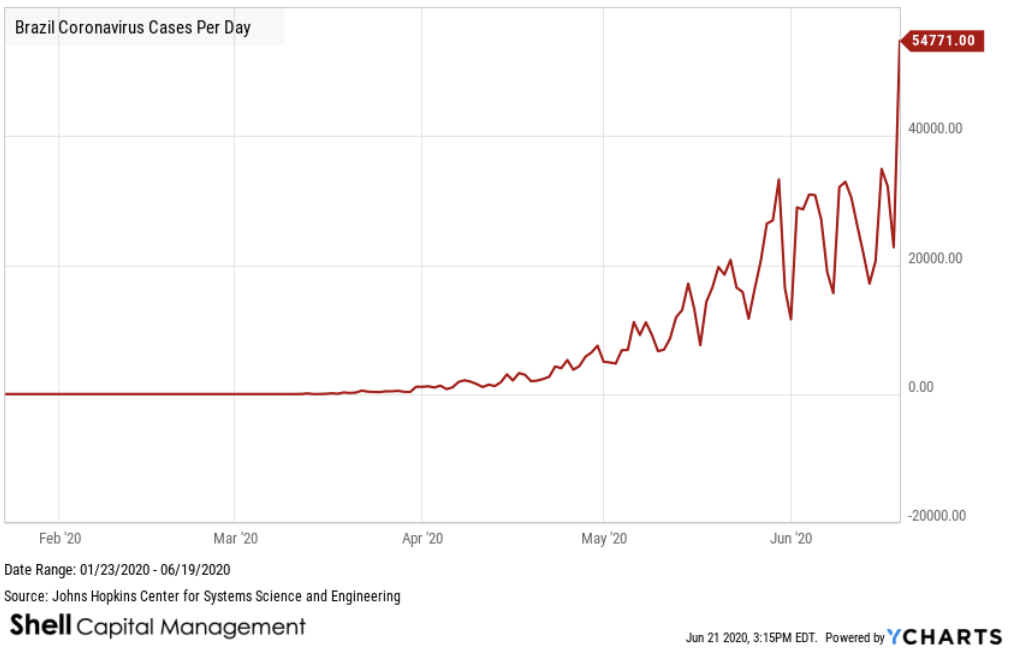

We’re seeing breakouts in other countries, too, such as Brazil.

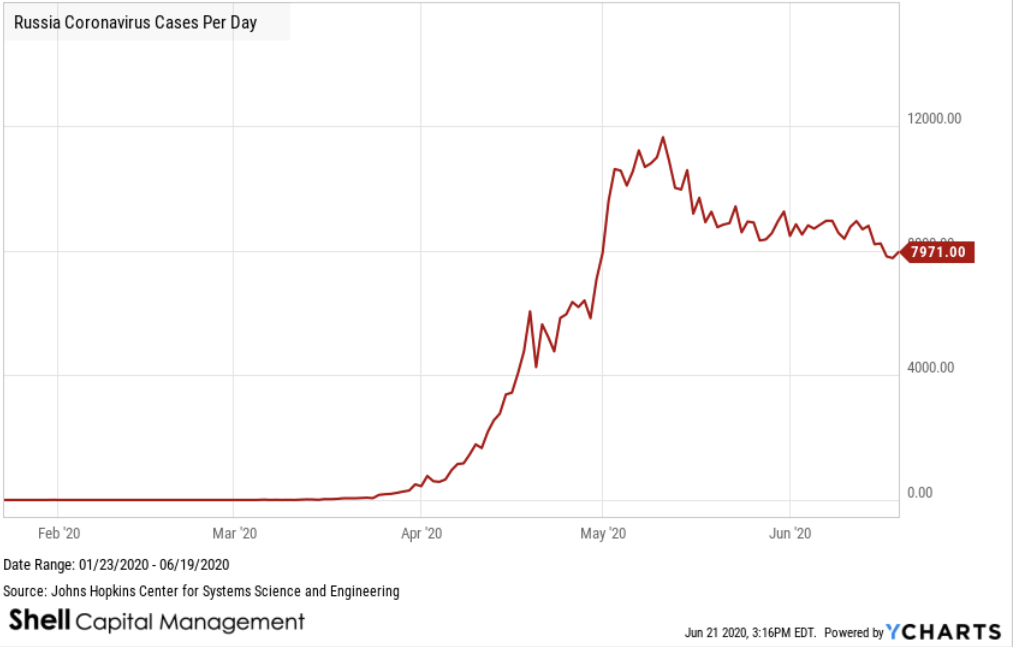

Others like Russia have peaked and are drifting down.

So, there’s the trends.

What about the momentum of the trend?

Just as I have proprietary momentum and relative strength algorithms to define the speed of a price trend in global markets, they also have a measure of the speed of the COVID – 19 trend.

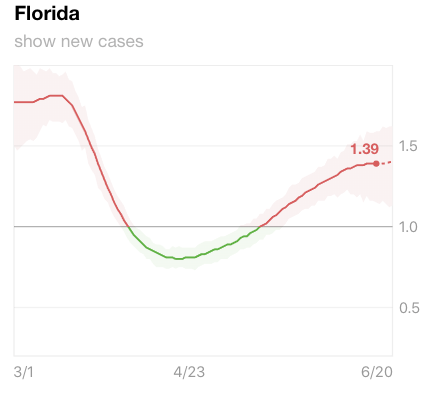

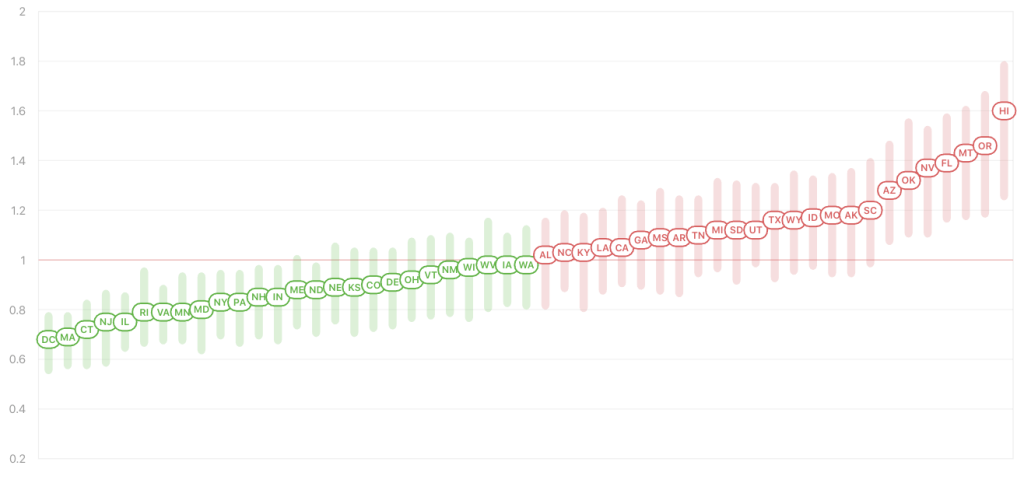

The values for Rt is a key measure of how fast the virus is growing. It’s the average number of people who become infected by an infectious person. If Rt is above 1.0, the virus will spread quickly. When Rt is below 1.0, the virus will stop spreading. Projecting the reproduction number is essential to understand how explosive an uptrend in new cases may be.

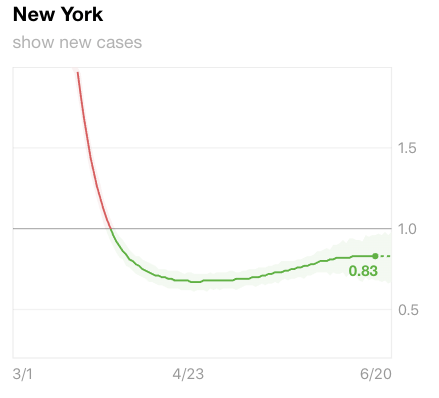

The Rt for Florida is 1.39, so it’s likely to spread relatively fast and we’ll see cases trend up as the new cases are spreading it to others. Florida has been in the top five of all states since I’ve been monitoring it.

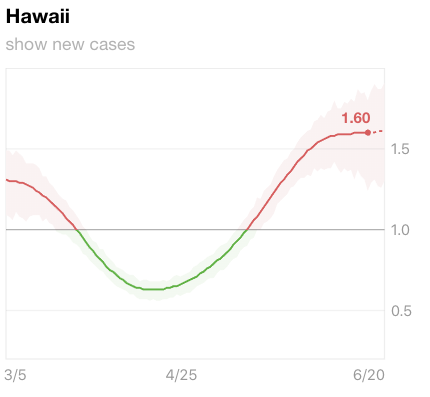

Hawaii has the highest reproduction number in the United States.

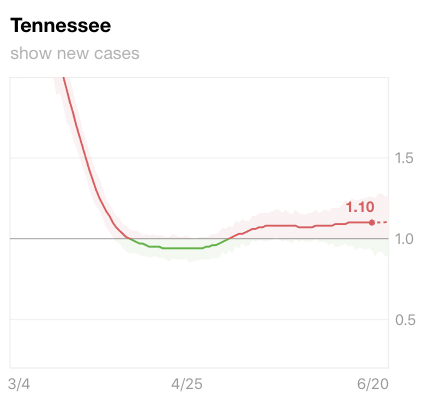

Tennessee hasn’t been spreading it as fast.

The Rt for New York was as high as 2 early on, so a person who contracted the virus spread it to about two more, but it has slowed.

The states with the lowest Rt levels are in the north right now and the highest are in the south, or the warmest climates.

So much for the theory that heat will smoother the Coronavirus. It doesn’t seem to be the case.

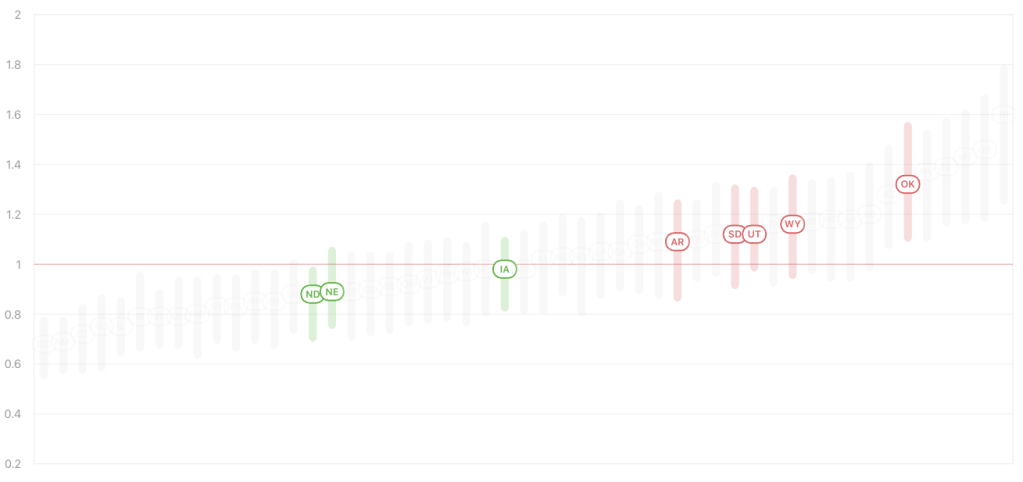

Here are all of the states ranked from lowest to highest R.

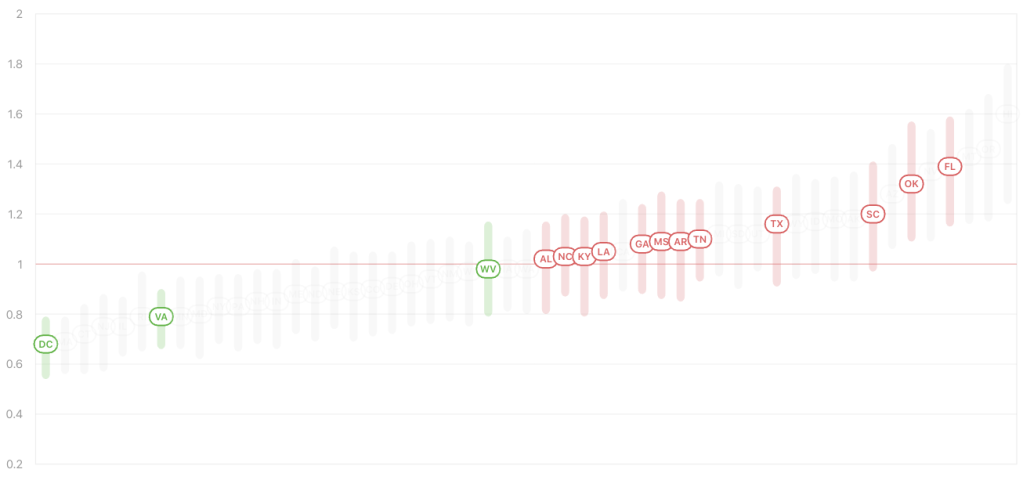

Here are the Southern states. Most are in the red zone.

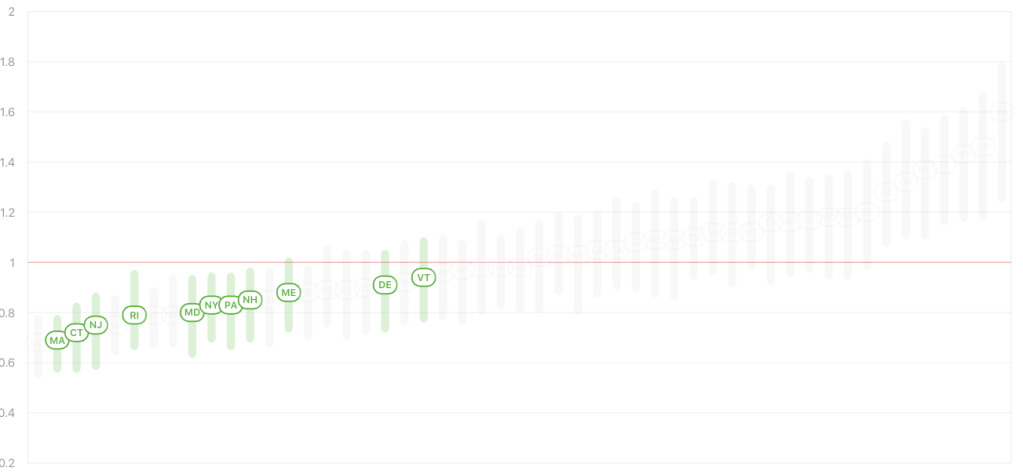

Next is the Northeast, who has maintained the most aggressive shelter in place and such.

Does this mean it’s working? Well, yes, if you aren’t around people, the spread will slow. However, only time will tell if these more city like areas come back sharply once they are back to full production.

By the way, here are the states that never sheltered.

So, we should prepare for the media to increasingly make this a big story again. As I see it, the odds of catching it is relatively low if less than 1% of the population has it. The trouble is, without testing everyone, we don’t know the positive rate. Right now the positive rate in Florida is increasing at 12%.

We should also prepare for the likelihood the stock market will eventually respond to these rising trends in new cases and the possibility of fear driving the stock market down again.

Although, it isn’t just a reaction to the continuation of COVID, but also the high risk level of the stock market.

The stock market is at an elevated risk level based on both fundamental valuation and quantitative momentum measures.

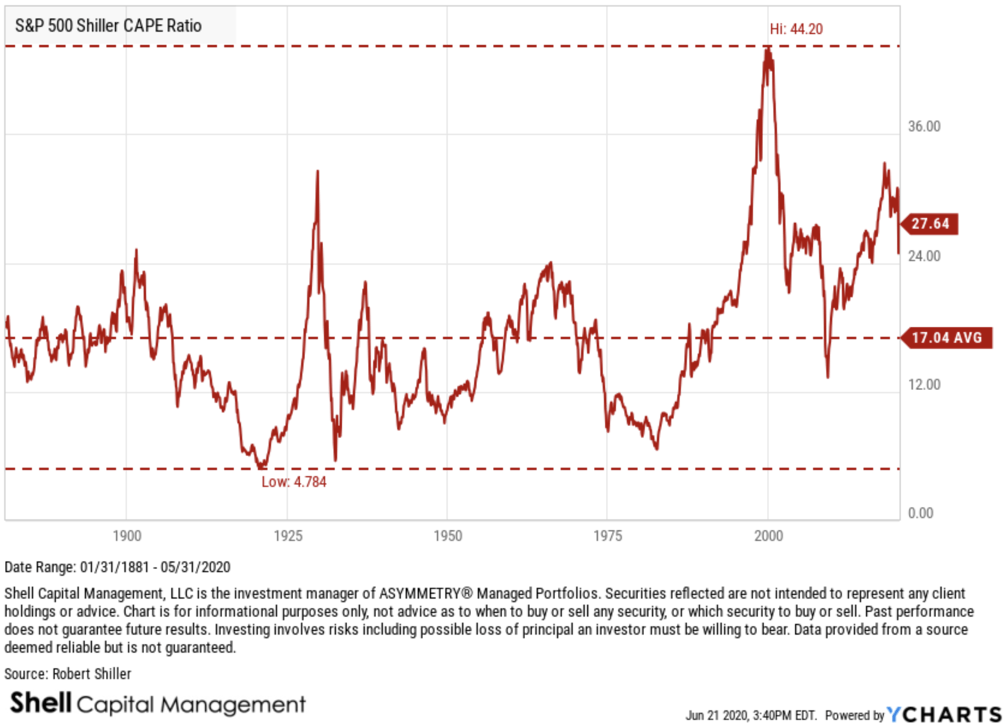

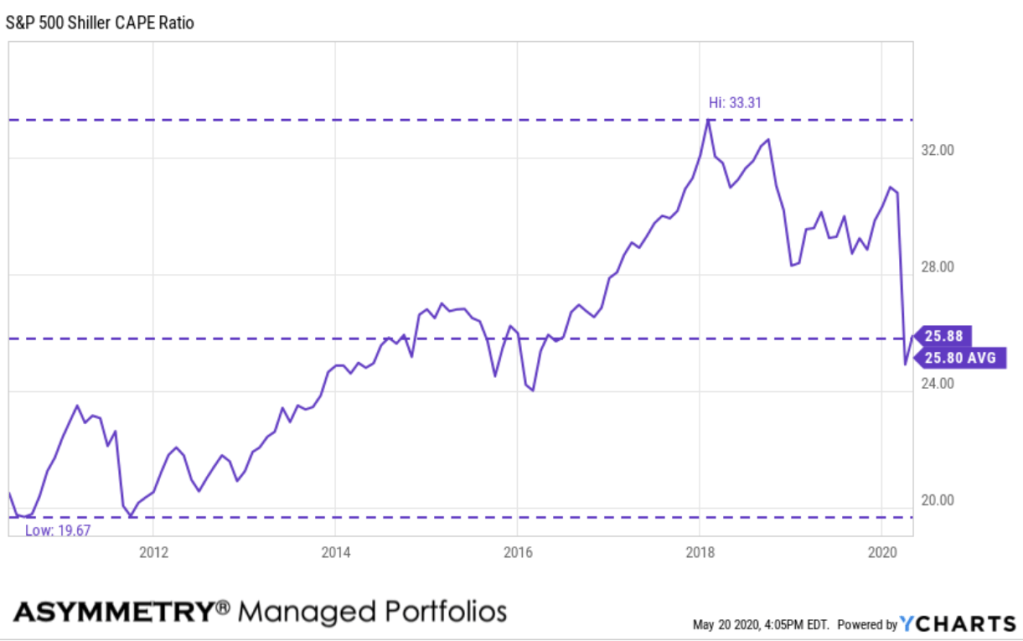

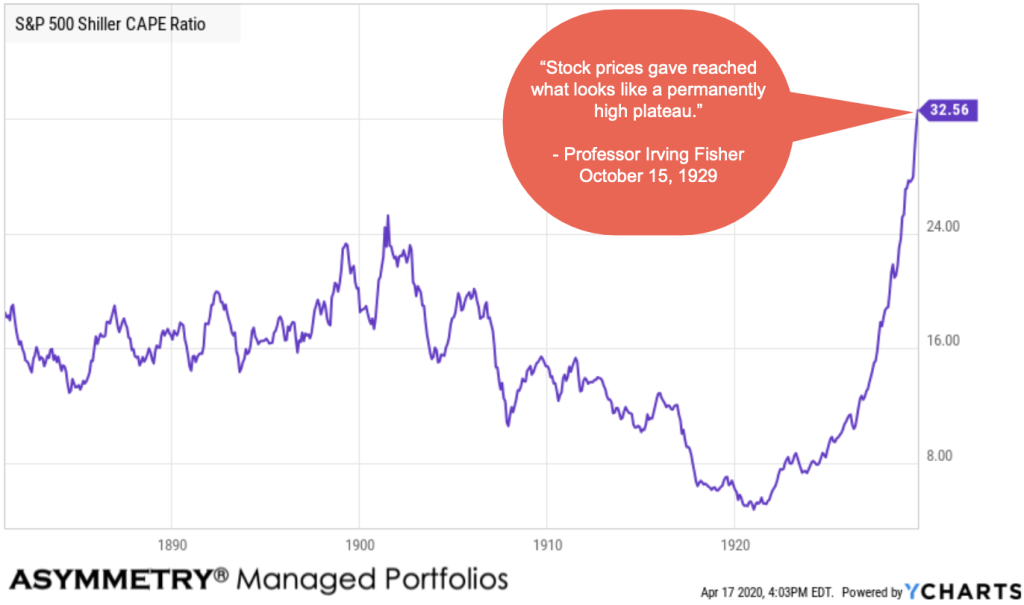

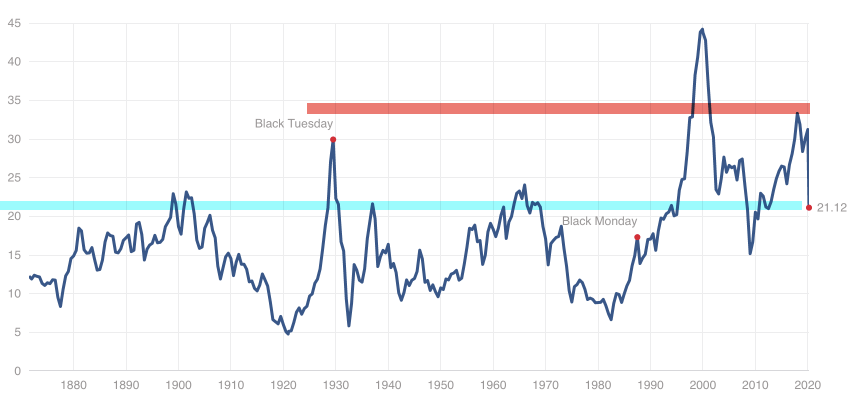

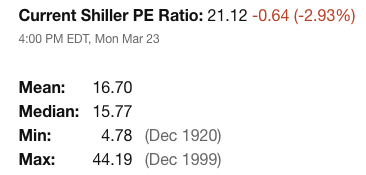

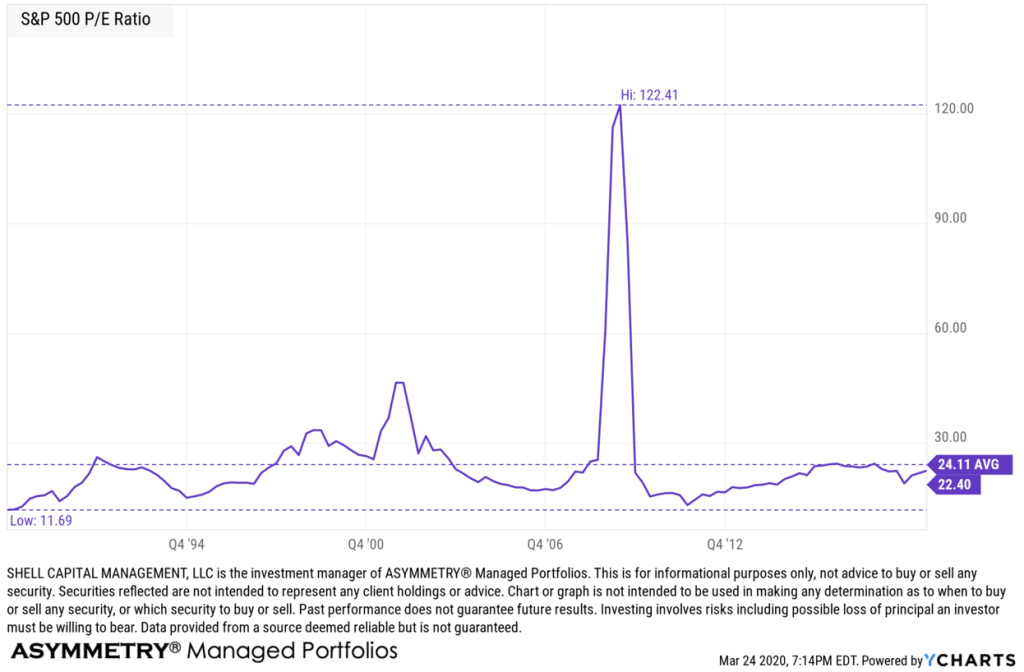

The S&P 500 Shiller CAPE Ratio, also known as the Cyclically Adjusted Price-Earnings ratio, is defined as the ratio the the S&P 500’s current price divided by the 10-year moving average of inflation-adjusted earnings. The metric was invented by American economist Robert Shiller and has become a popular way to understand long-term stock market valuations. It is used as a valuation metric to forecast future returns, where a higher CAPE ratio could reflect lower returns over the next couple of decades, whereas a lower CAPE ratio could reflect higher returns over the next couple of decades, as the ratio reverts back to the mean.

S&P 500 Shiller CAPE Ratio is at a current level of 27.64, up from 26.03 last month and down from 29.24 one year ago. This is a change of 6.18% from last month and -5.48% from one year ago. It remains well above average and it’s at the third highest level it has ever been. These trends in valuation get resolved eventually, even if the Fed is trying to support stable prices.

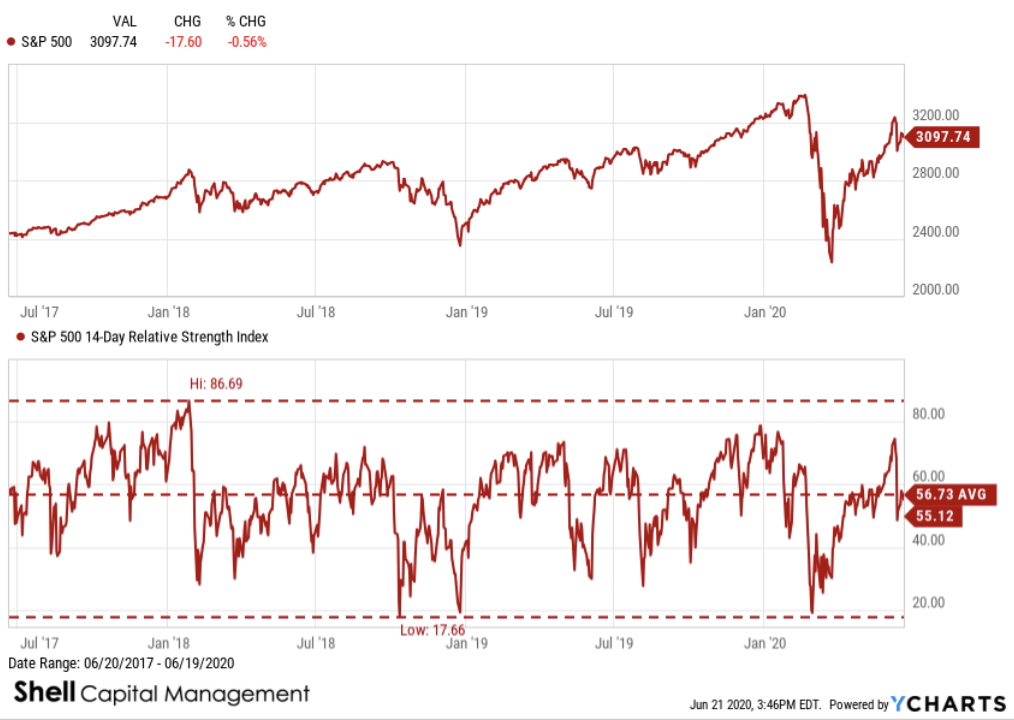

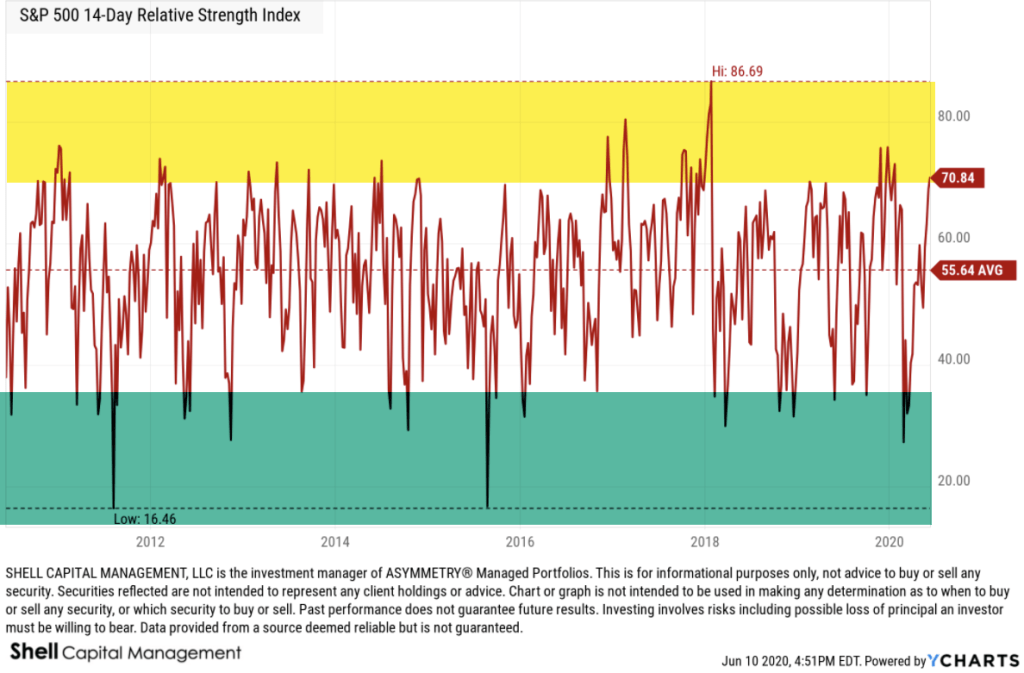

The short term relative strength reading the speed and magnitude of the moves isn’t as overbought as it was when I pointed it out two weeks ago, but it’s also far from oversold.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

“It doesn’t matter what we think about a trend, it matters what the crowd thinks about it, but more importantly, how they will respond to it.”

– Mike Shell

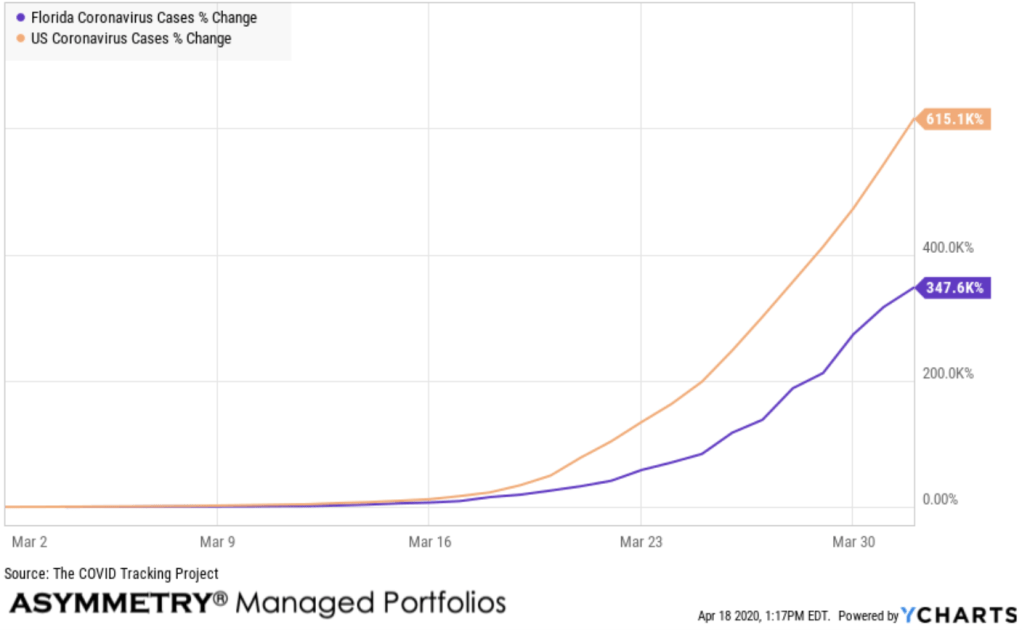

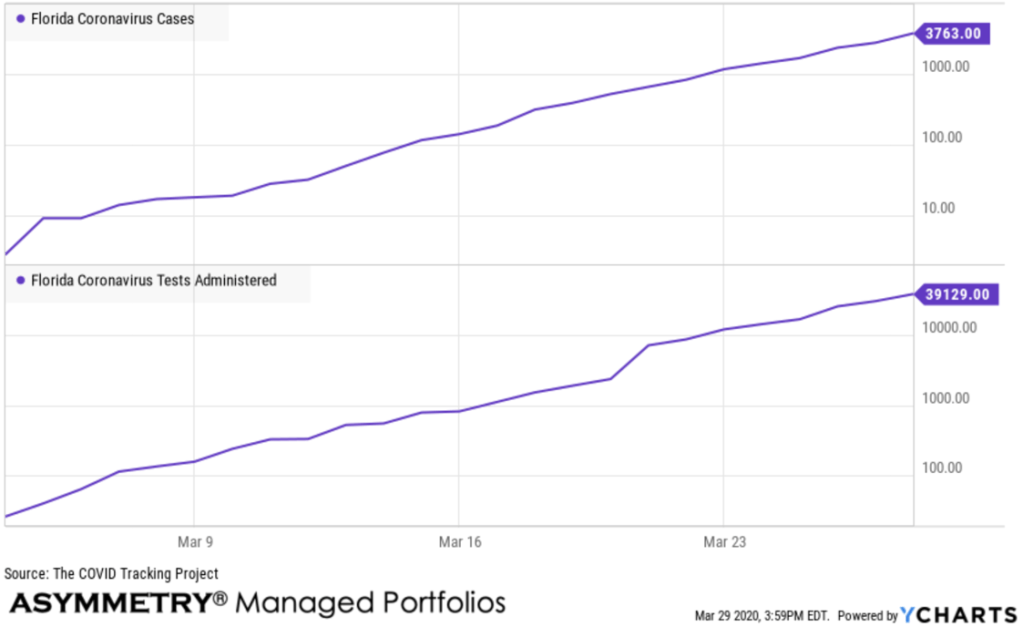

For a quick update on the Coronavirus COVID – 19 trend, I’ll use my home state of Florida as the example.

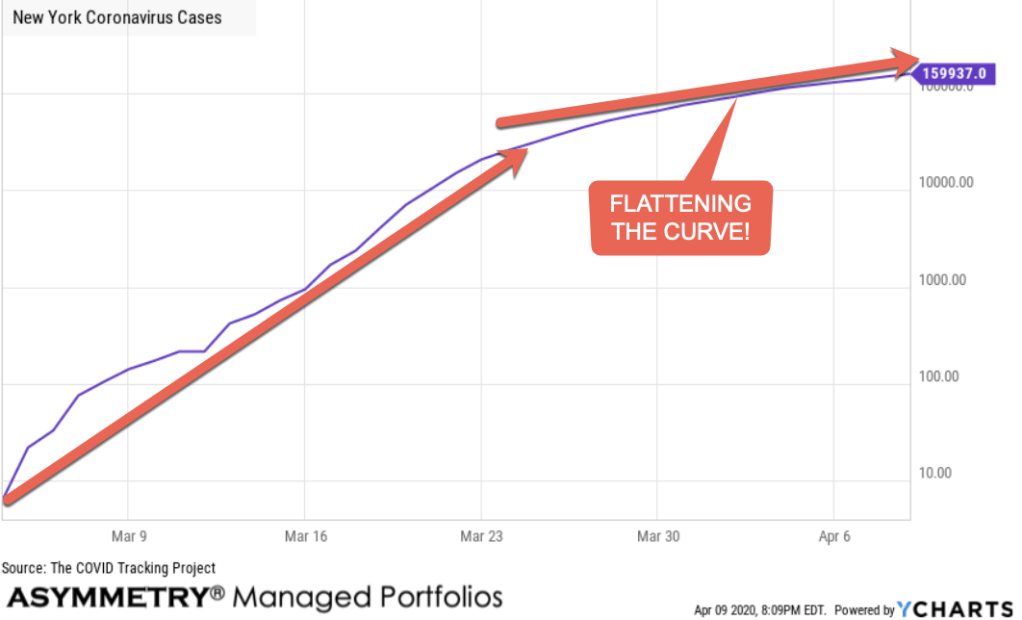

The first cases of Coronavirus (COVID-19) were confirmed on March 1st, 2020, which occurred in Manatee and Hillsborough County. During the initial outbreak of Coronavirus in the United States, Florida’s public beaches and theme parks were under scrutiny as being areas of large crowds. Some in the news media criticized Florida for being relatively late in issuing a “Shelter-At-Home” order, finally putting it in place beginning April 3rd, 2020. Cases ramped quickly from 2 on March 4th, to over 5000 by the end of the month. Since then, however, the number of cases in Florida has leveled off, slowing the rate of change.

I focus on the direction of the trend and its rate of change.

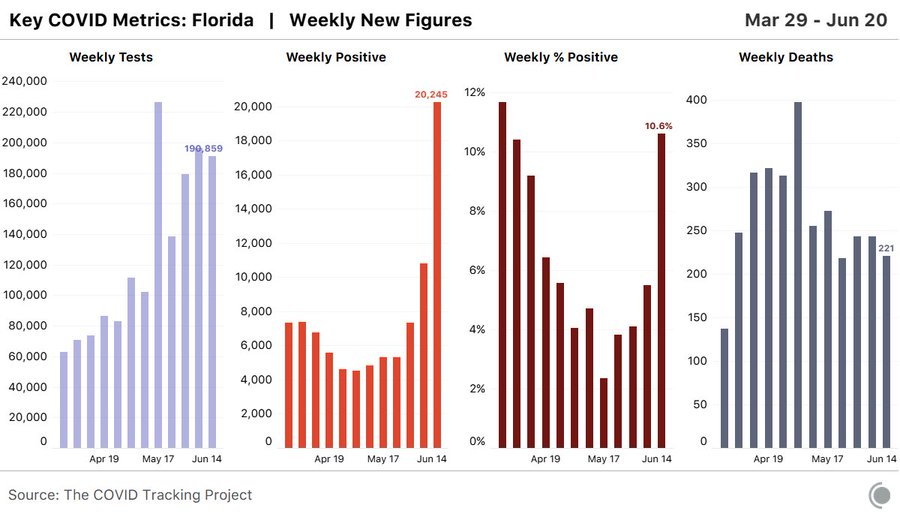

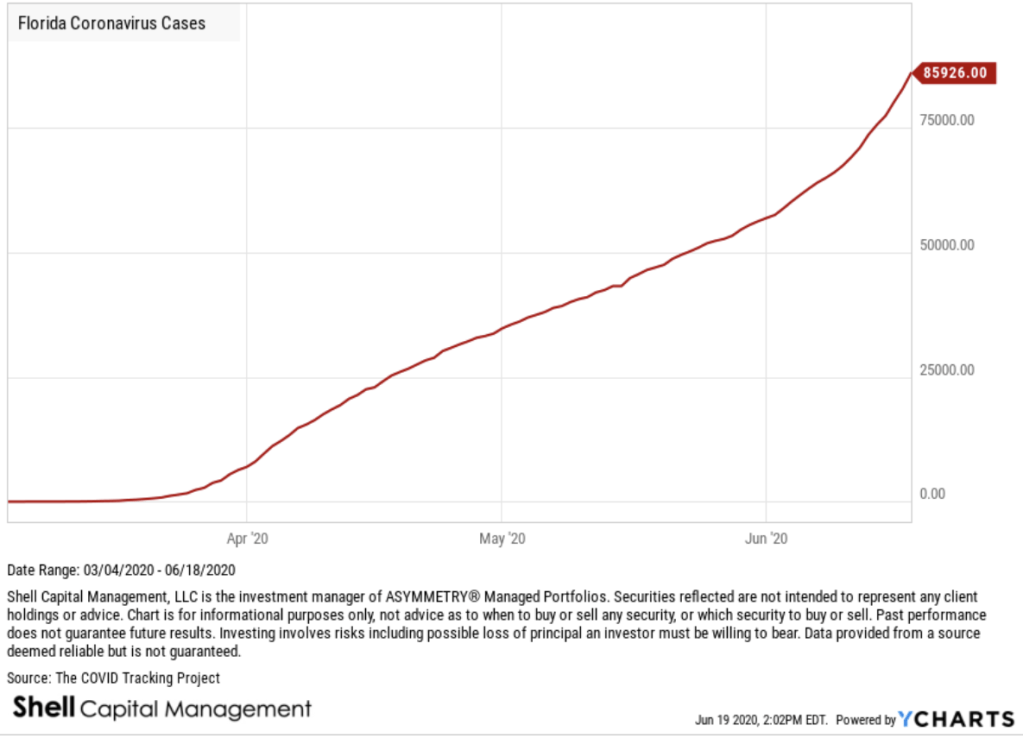

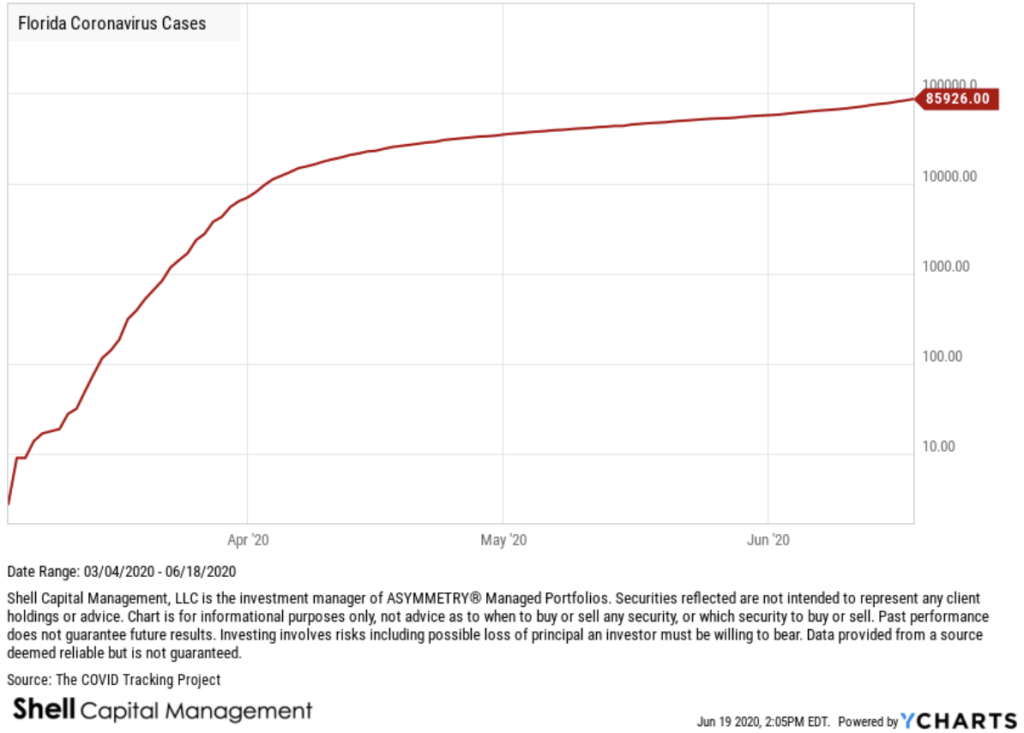

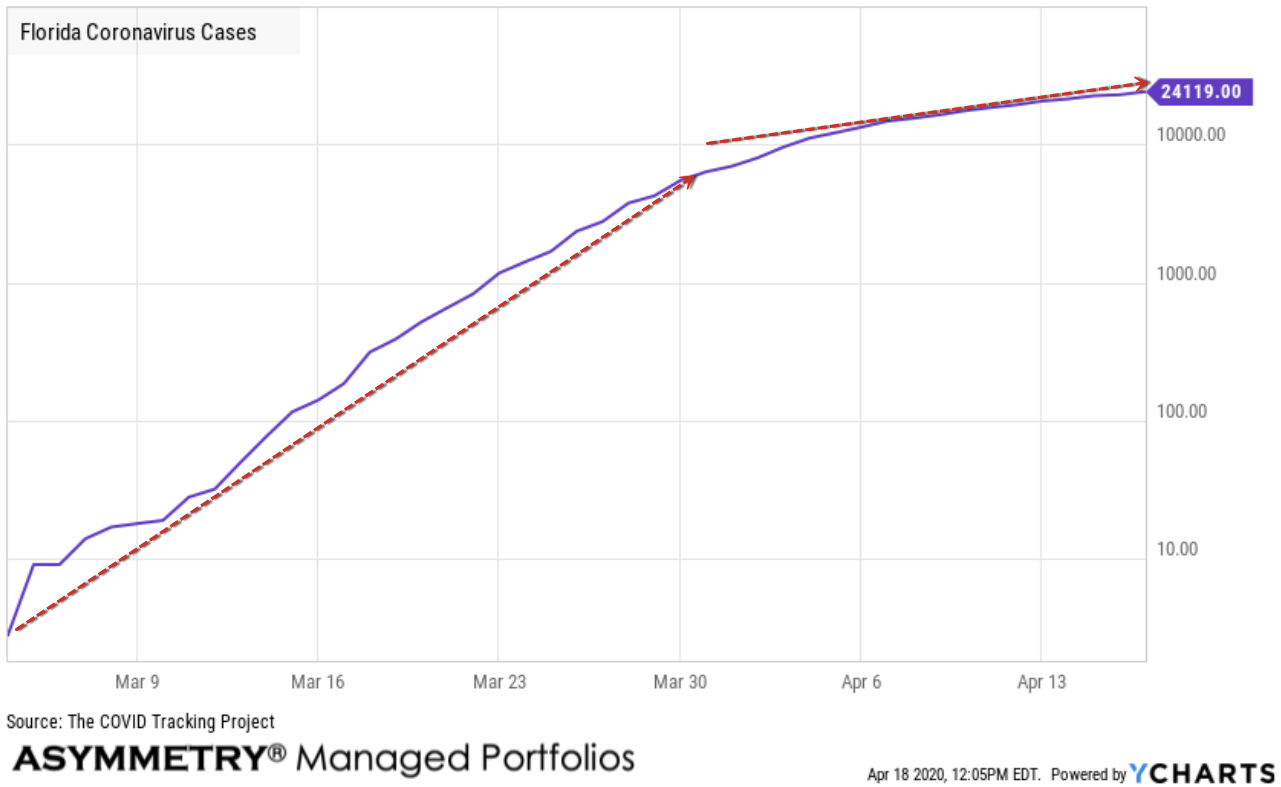

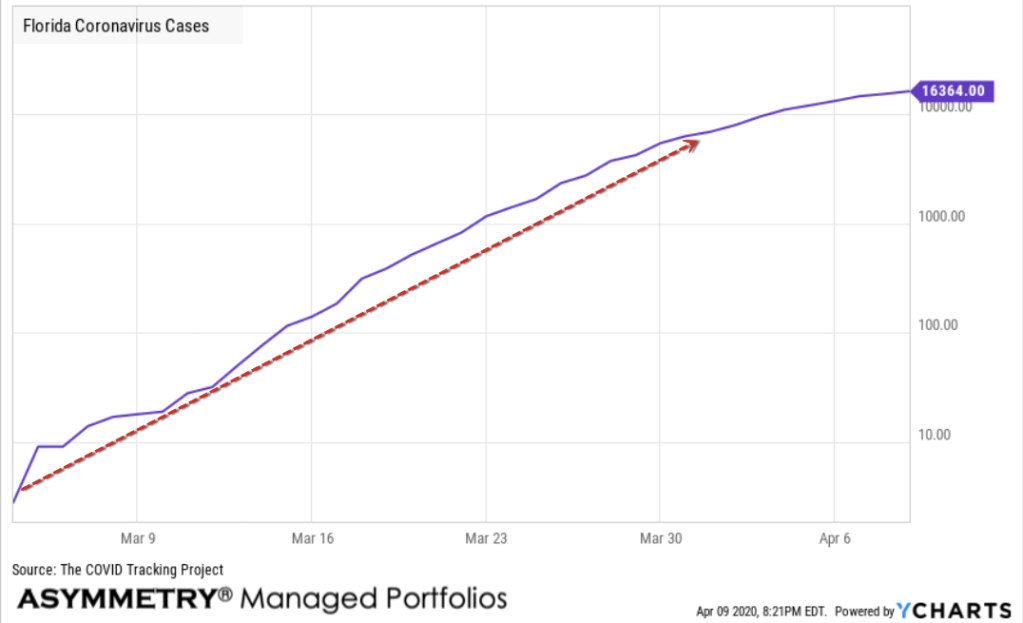

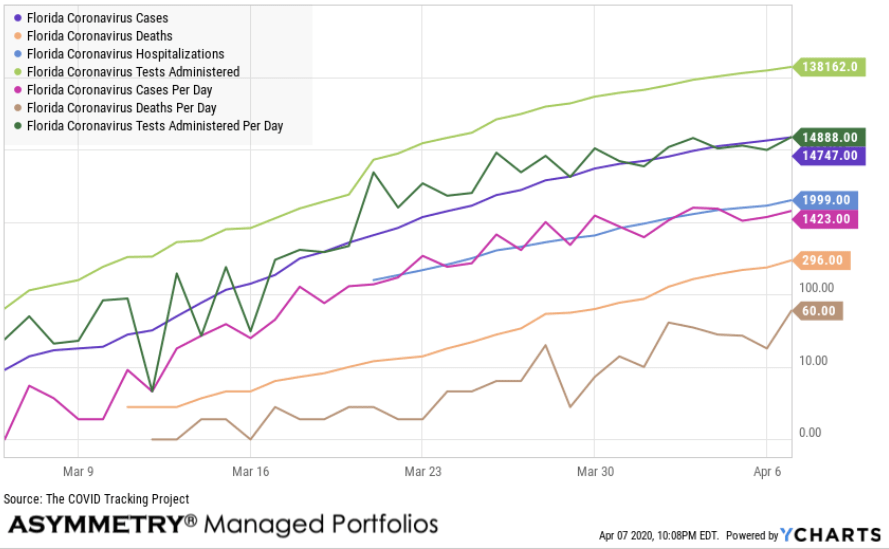

The COVID Tracking Project has now tracked 85,826 cumulative Florida Coronavirus cases , up from 82,719 Thursday. This is a change of 3.88%. Here, I show the standard arithmetic scale on the chart.

The concern I see in the above chart is it seems to be forming a rough S-shaped curve. That is, cases trended up though April and May around the same pace, but this month the rate of change is notably stronger in the linear price scale of an arithmetic chart. The arithmetic or linear chart doesn’t illustrate or scale movements in relation to their percent change, but instead, the linear price scale plots price level changes with each unit change according to a constant unit value. So, there is an equal distance between the data points as each unit of a change on the chart is represented by the same movement up the scale, vertical distance, regardless of what the level when the change happened. The arithmetic chart is the standard basic chart, especially over shorter time series, and it shows absolute trends.

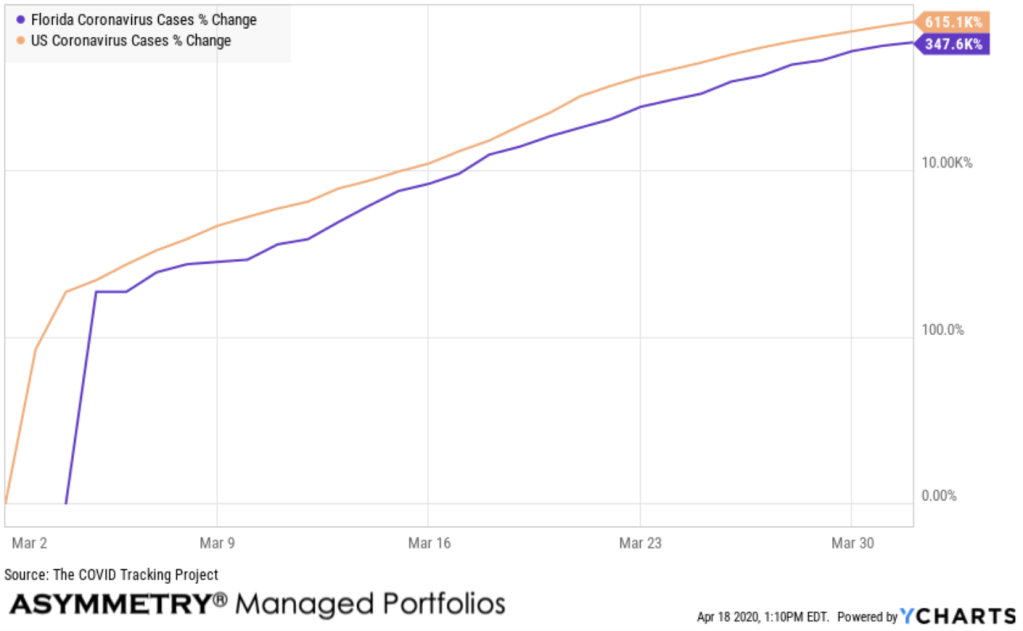

To see how the time series unfolds with a focus on percentage of change, we changed the scale to logarithmic. The logarithmic chart is plotted so that two equal percent changes are plotted as the same vertical distance on the scale. Logarithmic scales are better than linear scales for normalizing less severe increases or decreases. Applying a logarithmic scale, the vertical distance between the data on the scale the percent change, so we can better identify changes in rates of change. Here, we see a strong uptrend in March, then the rate of change has since leveled off. The trouble, however, is it is still trending up and at its high.

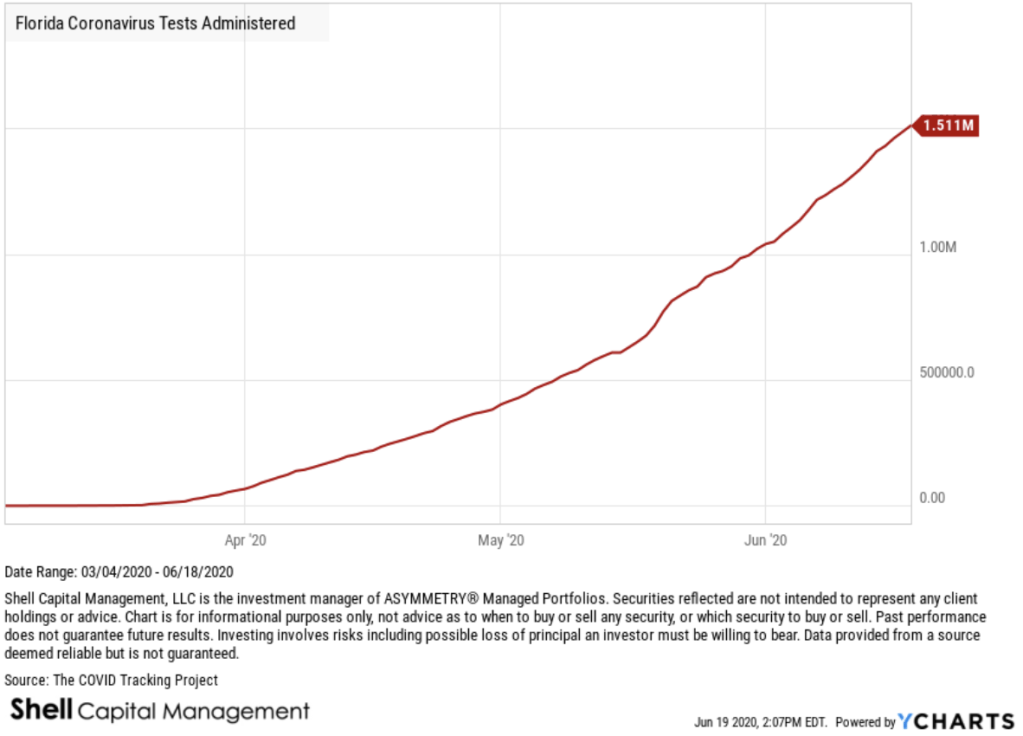

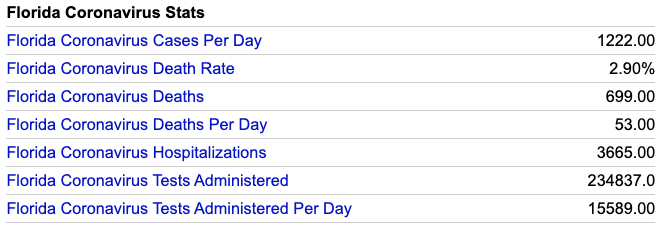

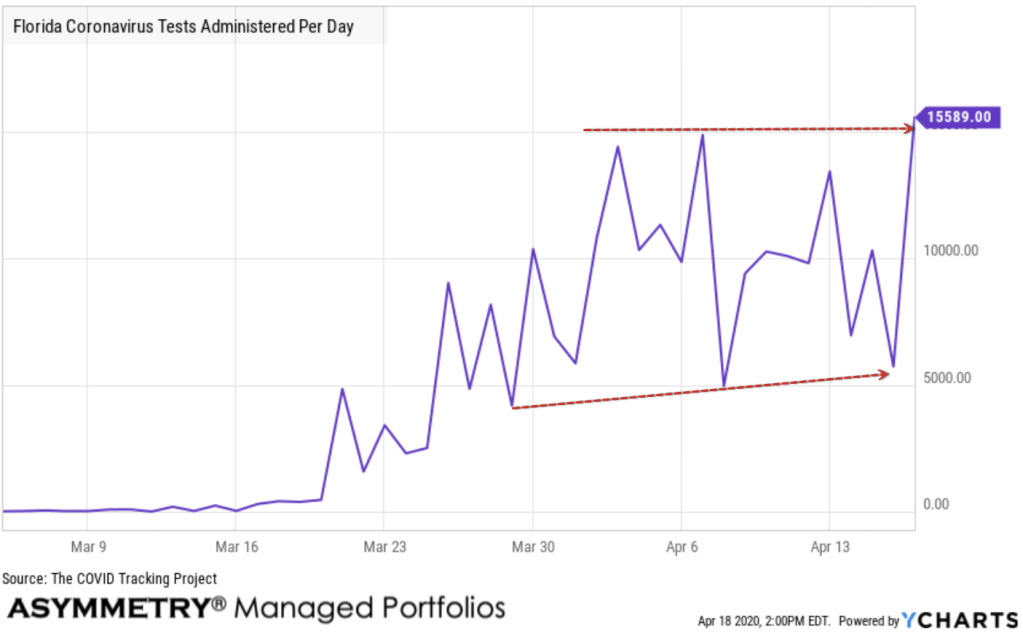

Florida Coronavirus Tests Administered is at a current level of 1.5 million, which up from 1.486 million the day before, an increase of 1.72%.

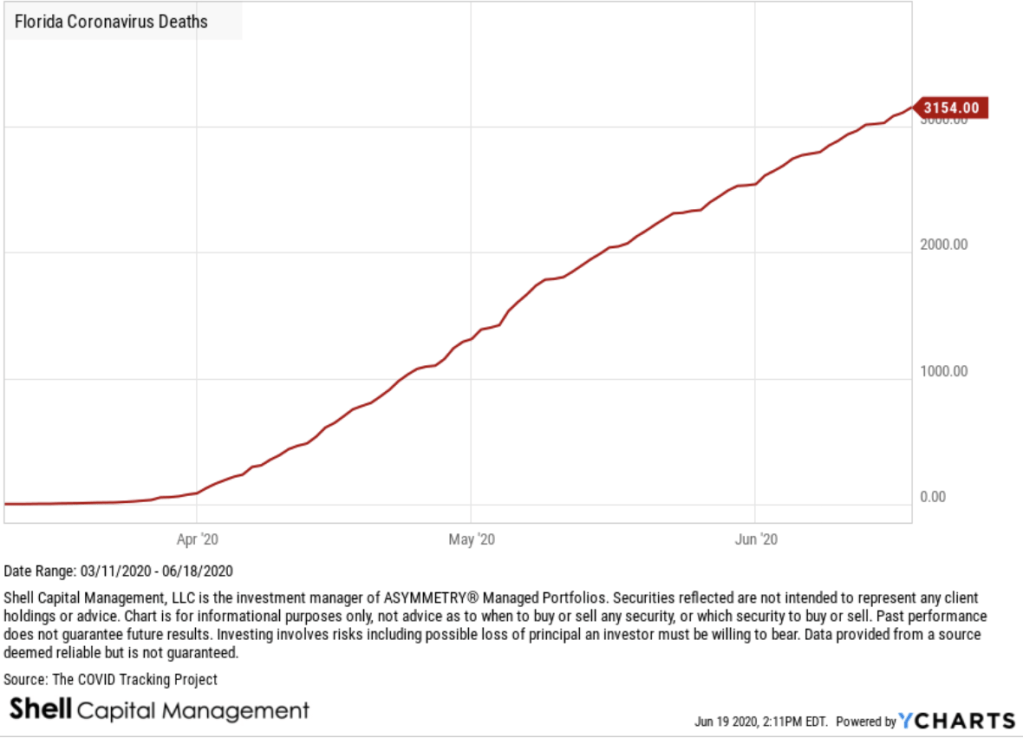

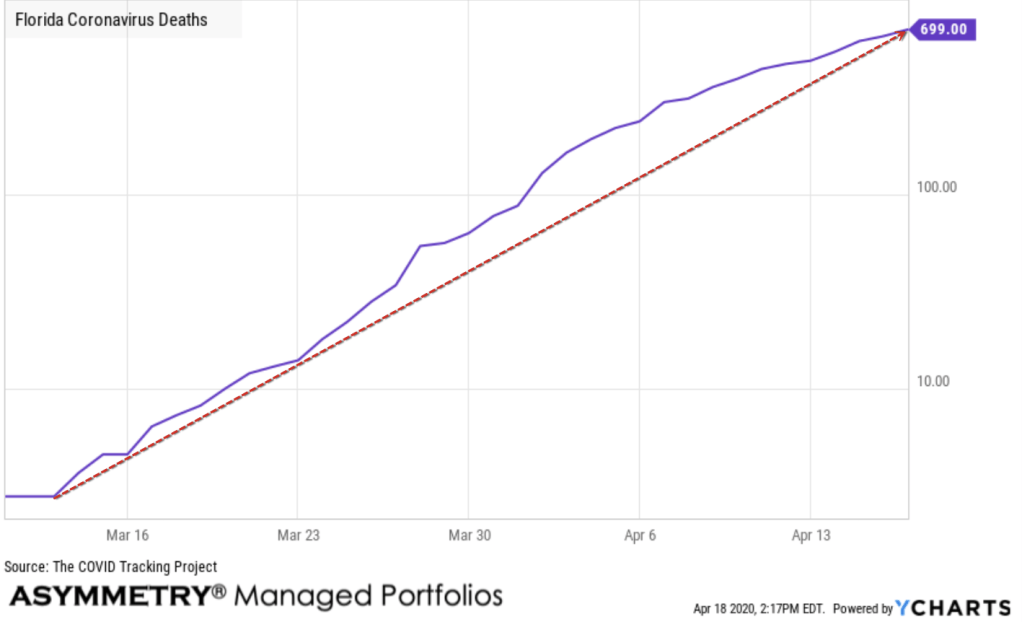

COIVD – 19 Deaths have increased 1.4% since Thursday. Deaths are obviously an essential factor to track. Florida Coronavirus Deaths is at a current level of 3,154.00, up from 3,110.00 yesterday.

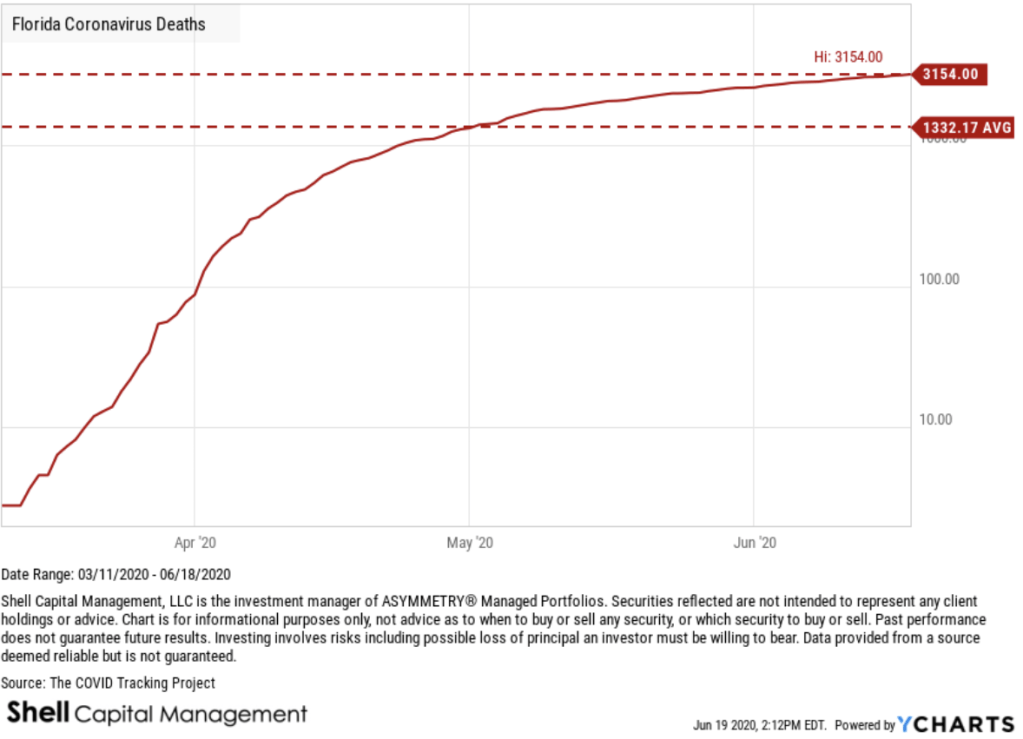

The steep uptrend in deaths is scary looking using the arithmetic scale showing the absolute trend in cumulative deaths. In the next chart, we observe the same trend as a log scale, which shows the rate of change is in an uptend, but has been slowing. I labeled the highest high (now) and the average over the period for reference.

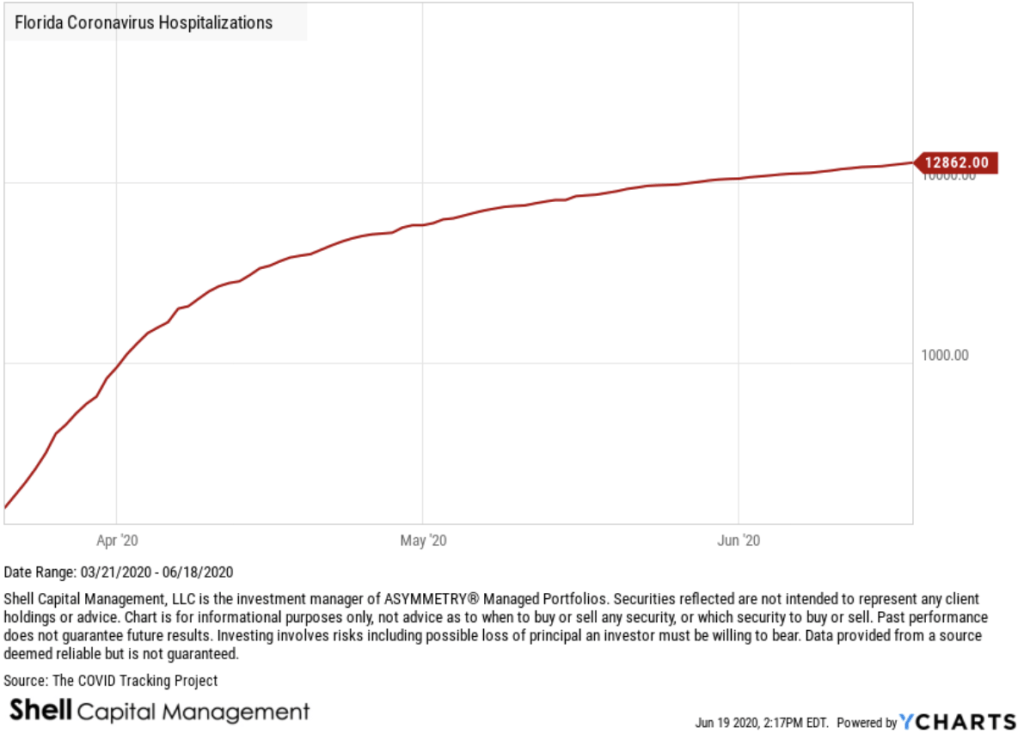

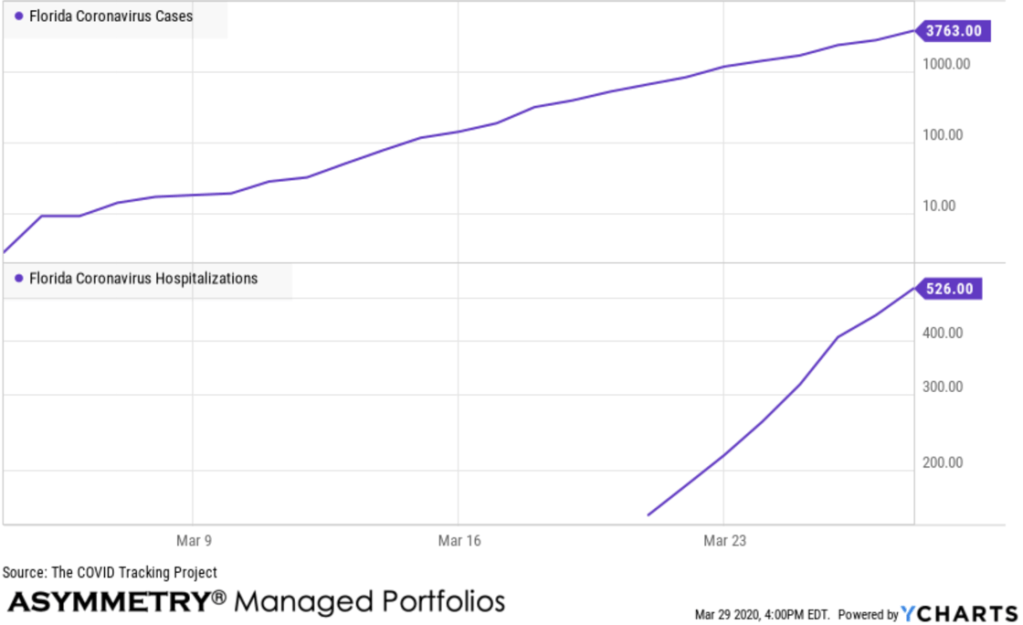

Florida Coronavirus Hospitalizations is at 12,862, up from 12,673 the prior day, which is a change of 1.49%. To focus on the rate of change, here is the log scale chart.

Keep in mind, my objective here isn’t to rehash the research of others, but instead to share what I see in the trends and rates of change. As such, this isn’t a complete analysis of the virus. It’s my observations, as a quant and trend system developer and operator. The data source is The COVID Tracking Project which can only report the data as provided by the states.

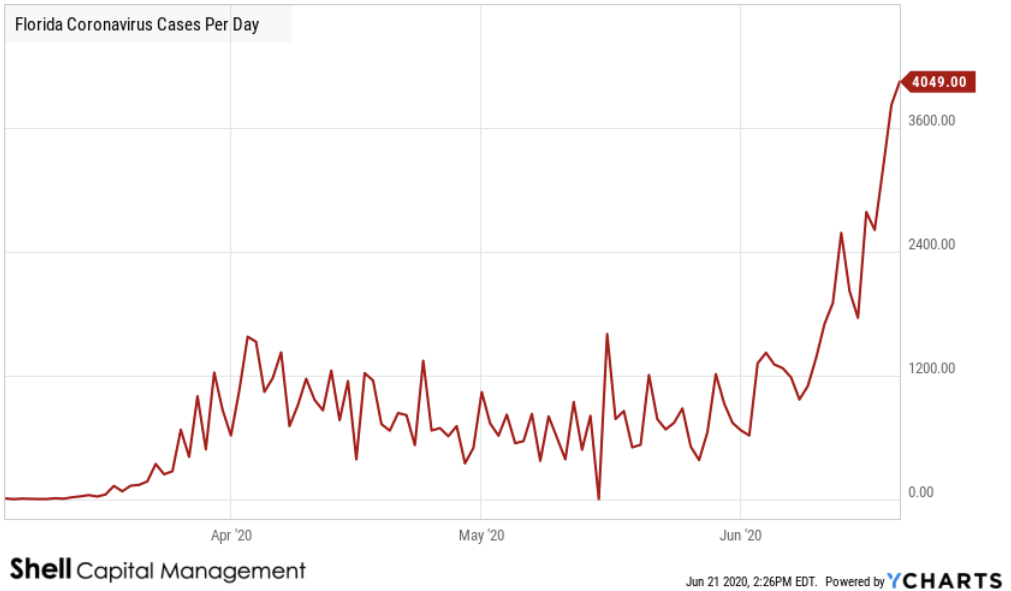

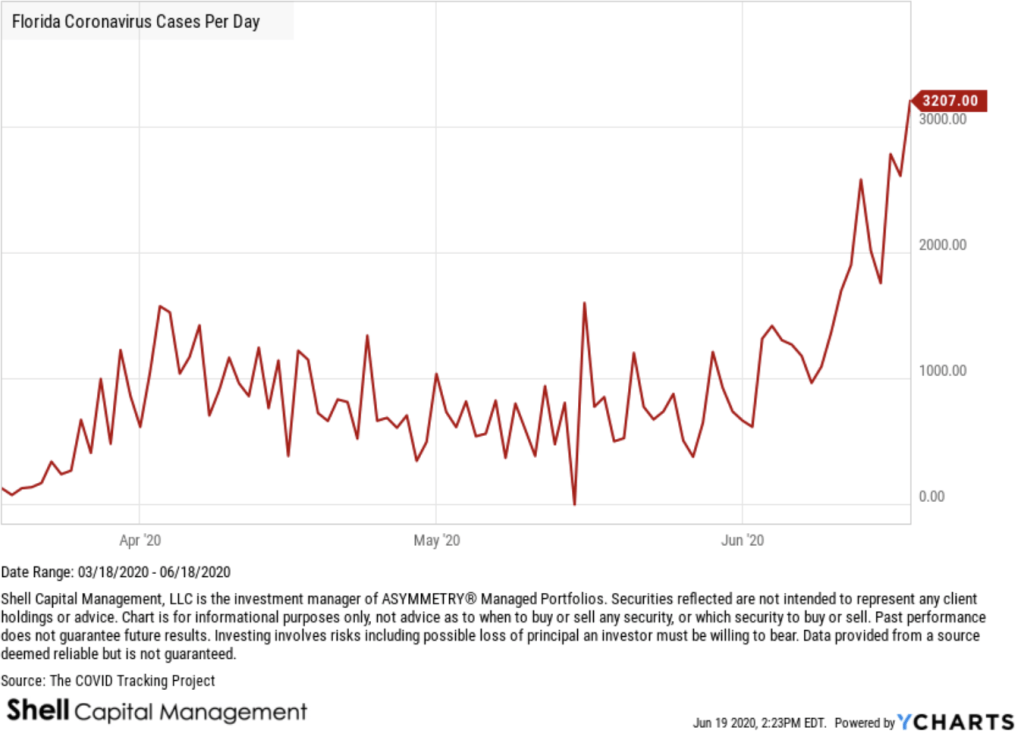

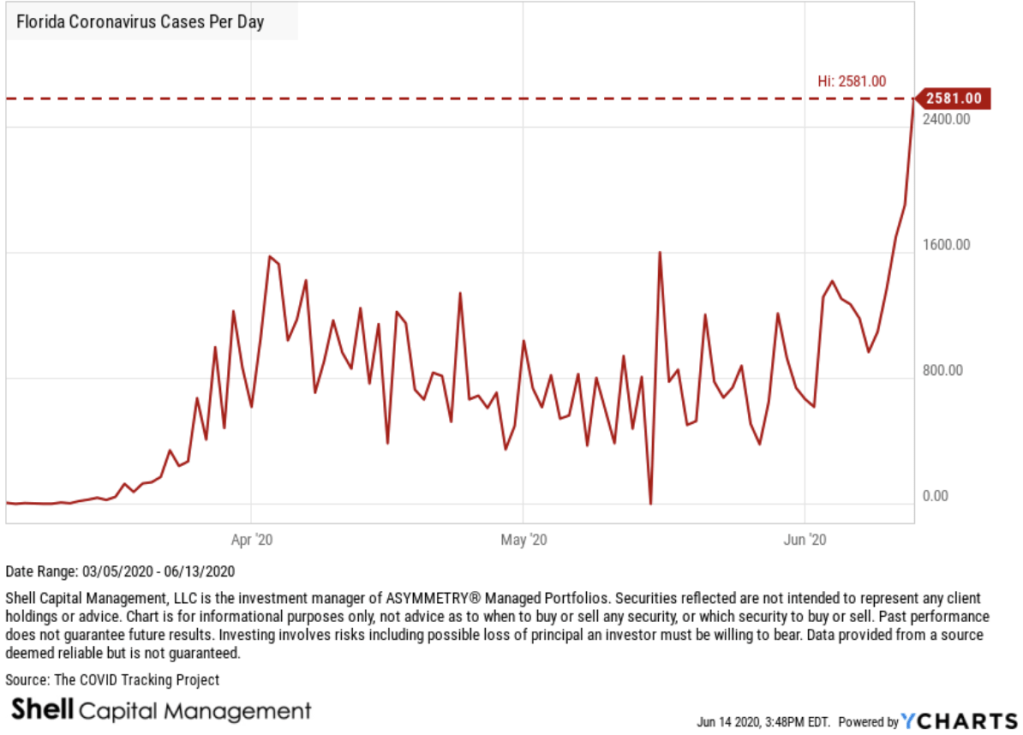

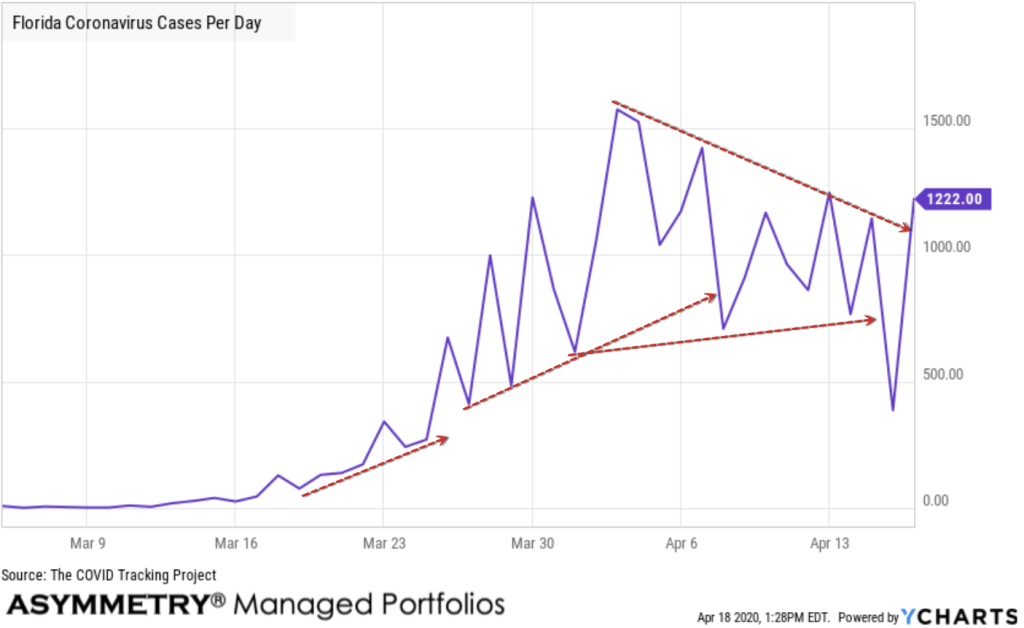

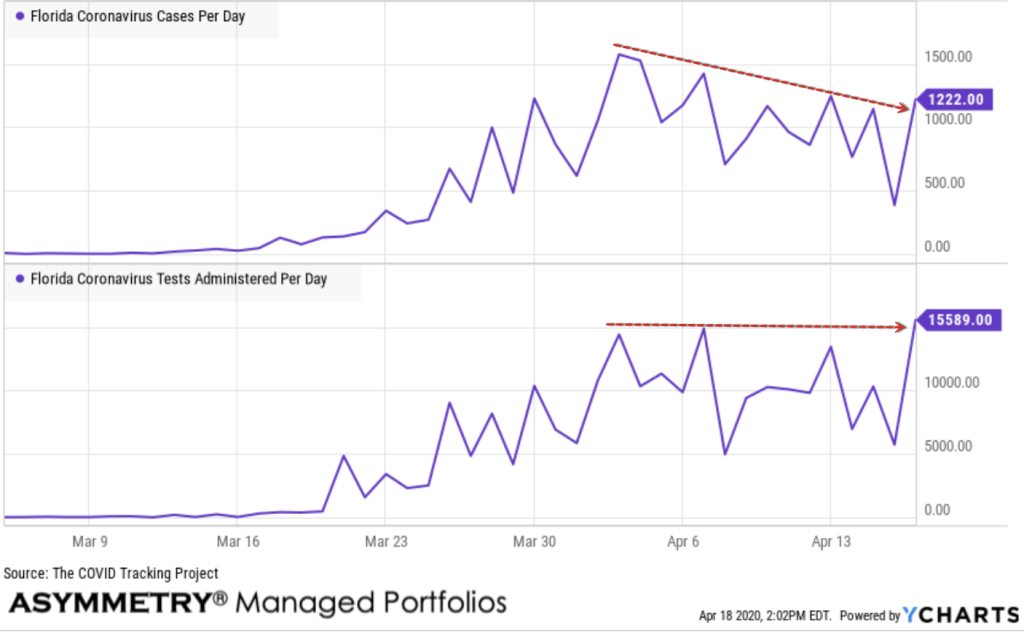

The uptrend in Florida Coronavirus cases per day has indeed continued and with a notable new high.

I don’t like to see an uptrend like this because it’s a virus, and viruses are contagious, so they spread. In the case of Coronavirus, we can get an idea of the speed and rate of spread by the reproductive number (R0), or ‘R-naught’, represents the number of new infections estimated to stem from a single case. The reproductive number (R0) is relatively high, according to a research paper on the CDC: Assuming a serial interval of 6–9 days, we calculated a median R0 value of 5.7 (95% CI 3.8–8.9).

I’m not going into the details here, but, with a reproductive value of 5.7, an increase in new cases is material in my opinion. That is, once it trends up as we are seeing now, it seems more likely to continue.

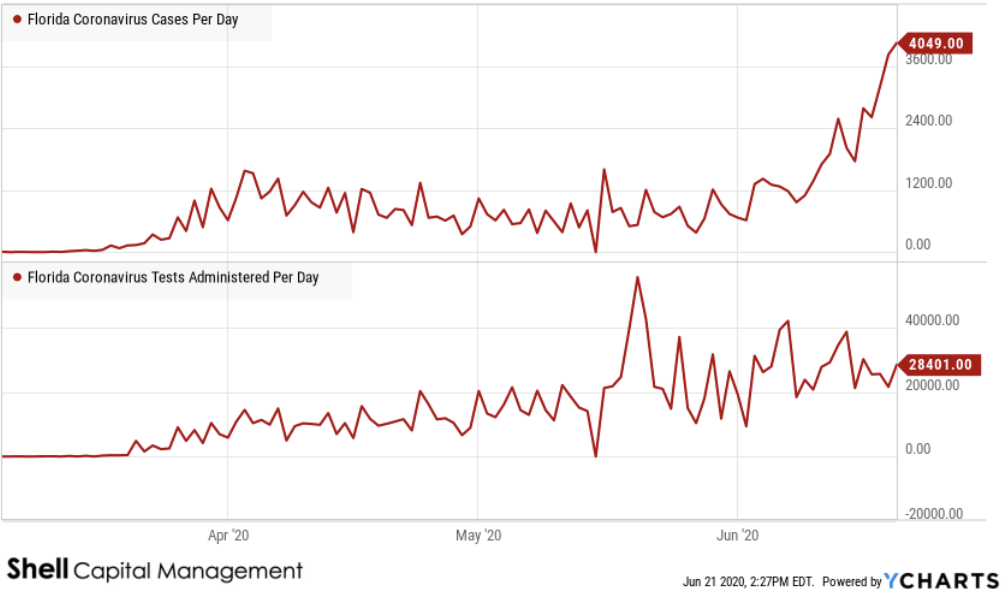

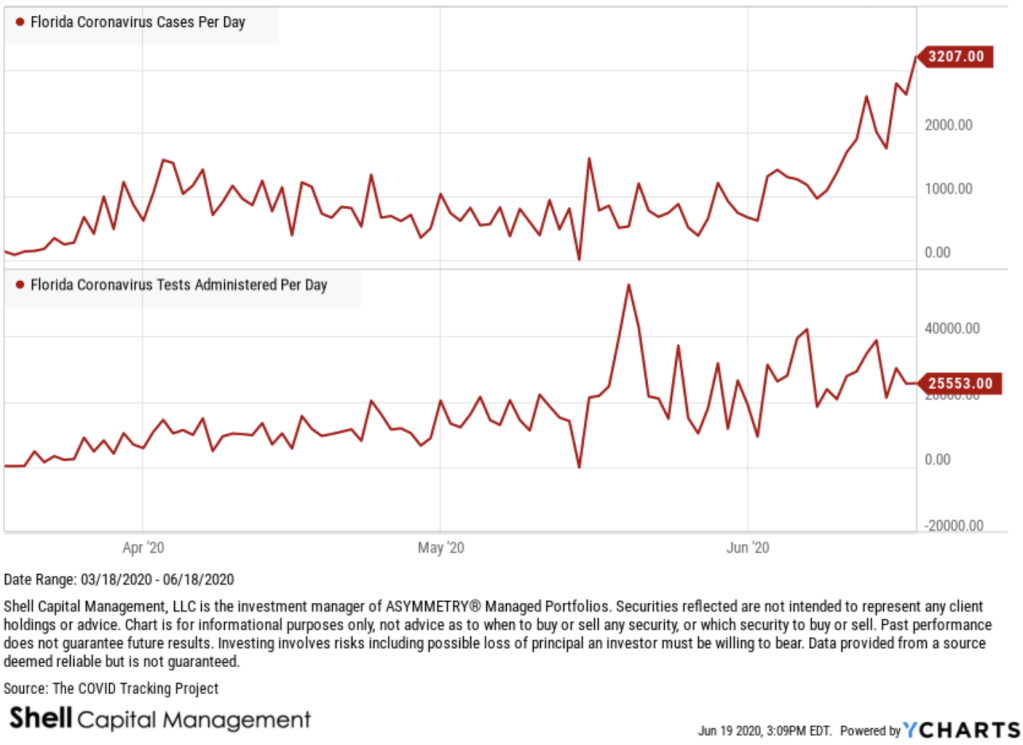

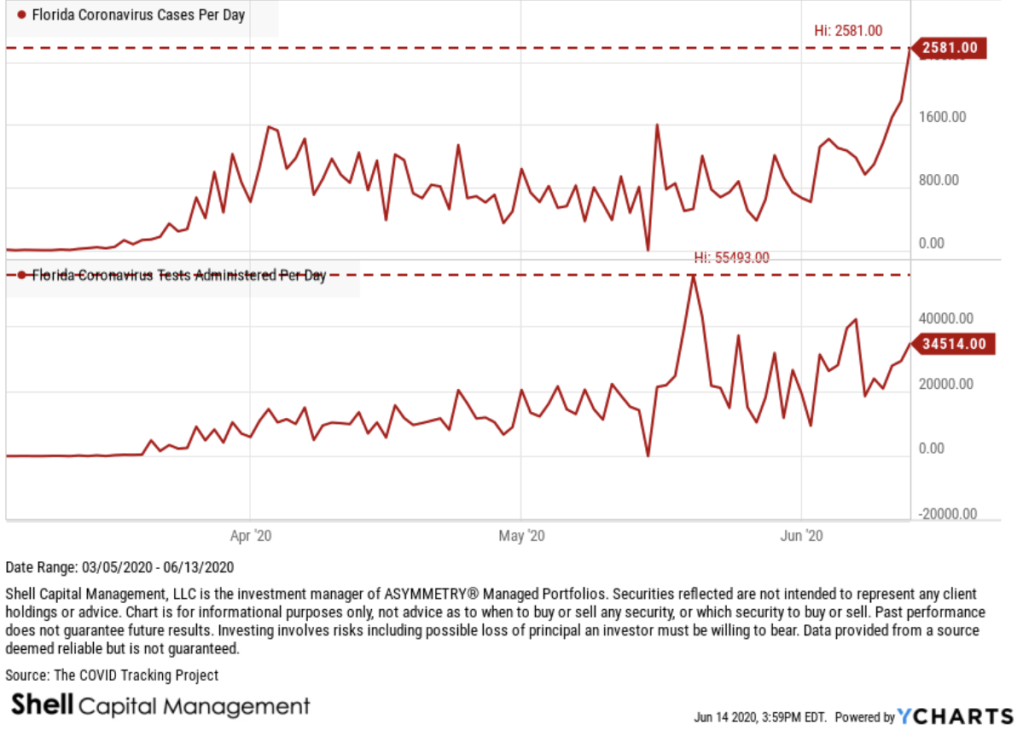

Are new cases a function of increased testing?

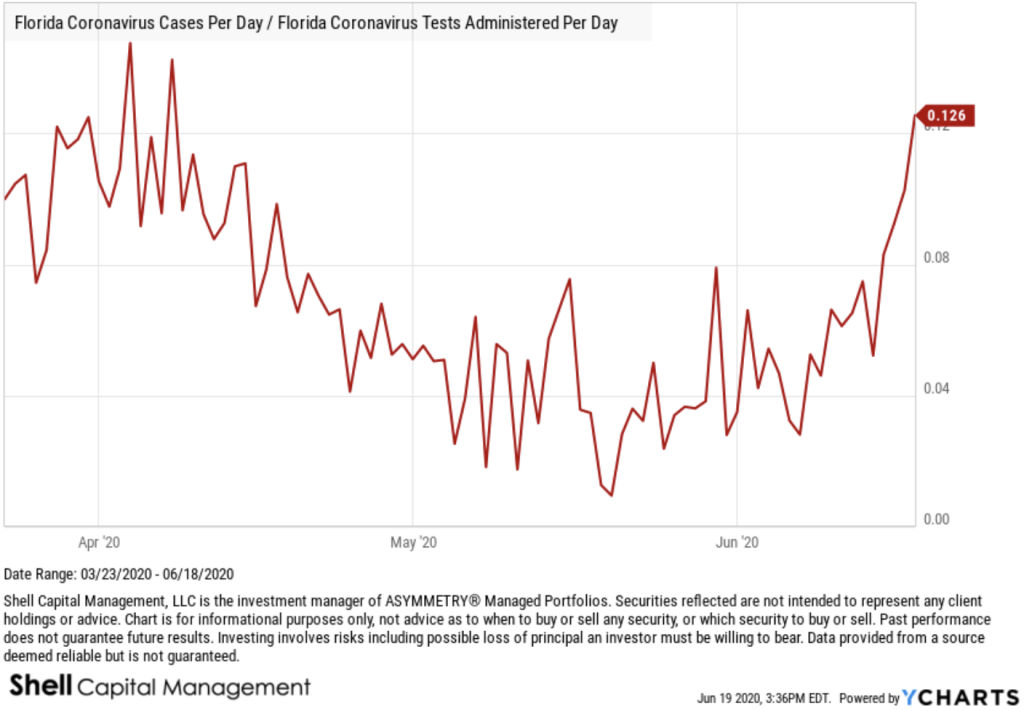

Some say the increase in new cases per day is a result of more testing. That doesn’t seem to be the case. Below is a charge of cases per day with a time series of tests administered per day under it. Visually, we see no correlation. However, there are many caveats to the data. So, anyone who wants to make a cased leaning one way or another can find ways to skew it, but it is what it is. We have a material increase in cases in Florida.

QUANTIATIVE ANALYTICS

Now, we’ll take a deeper dive and apply some analytics to the trends by observing some ratios.

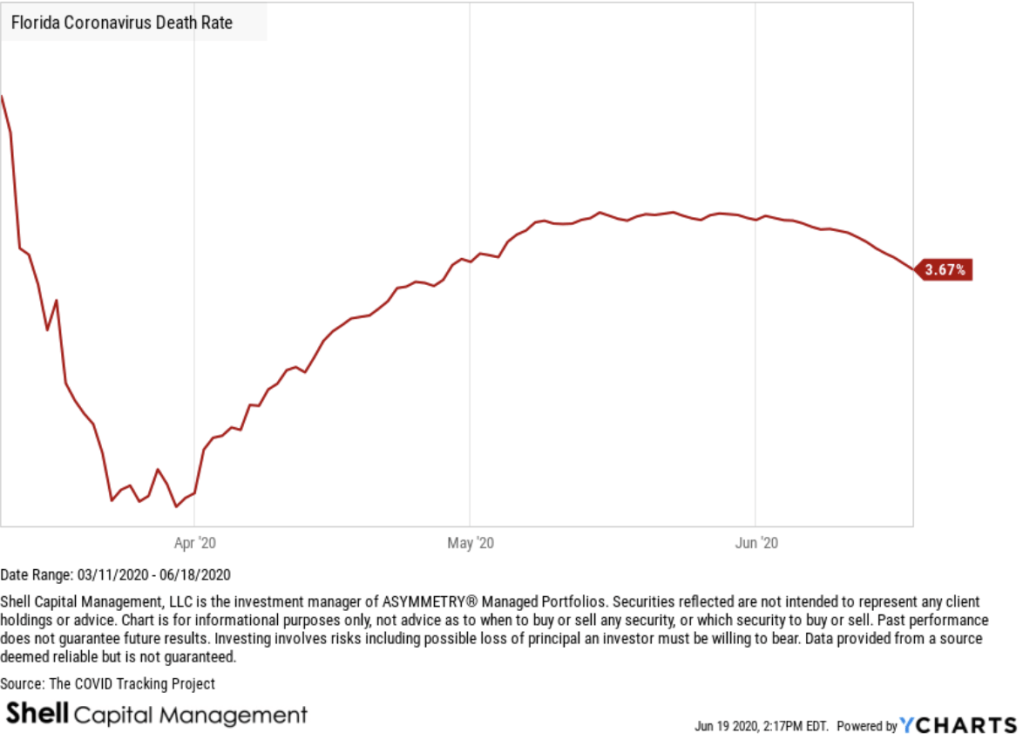

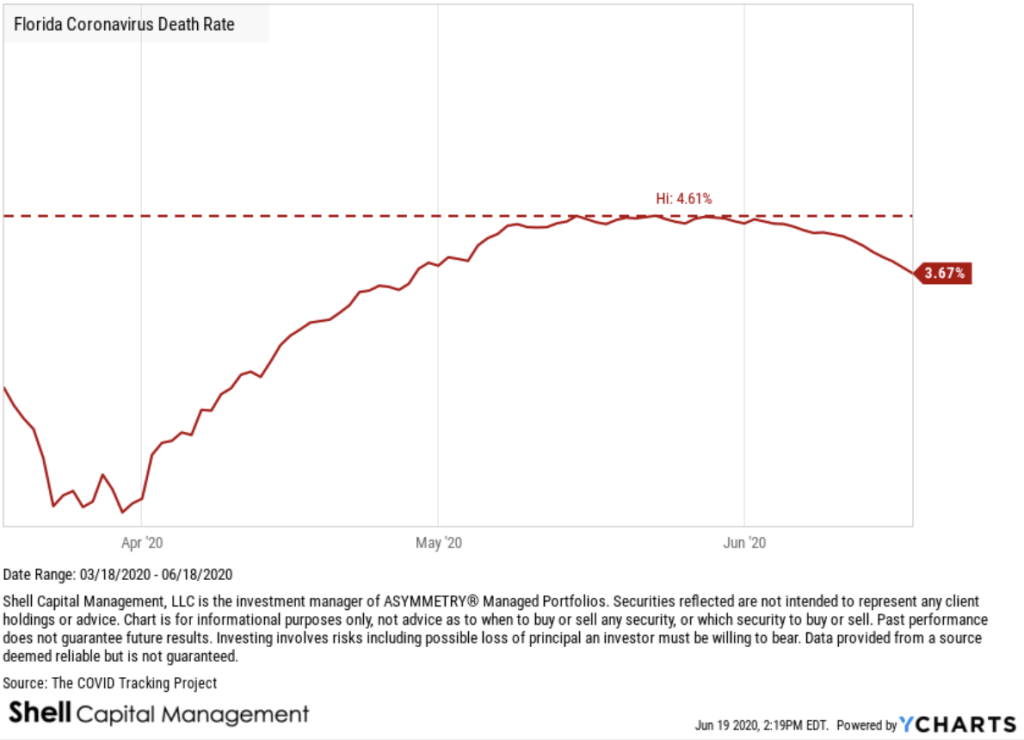

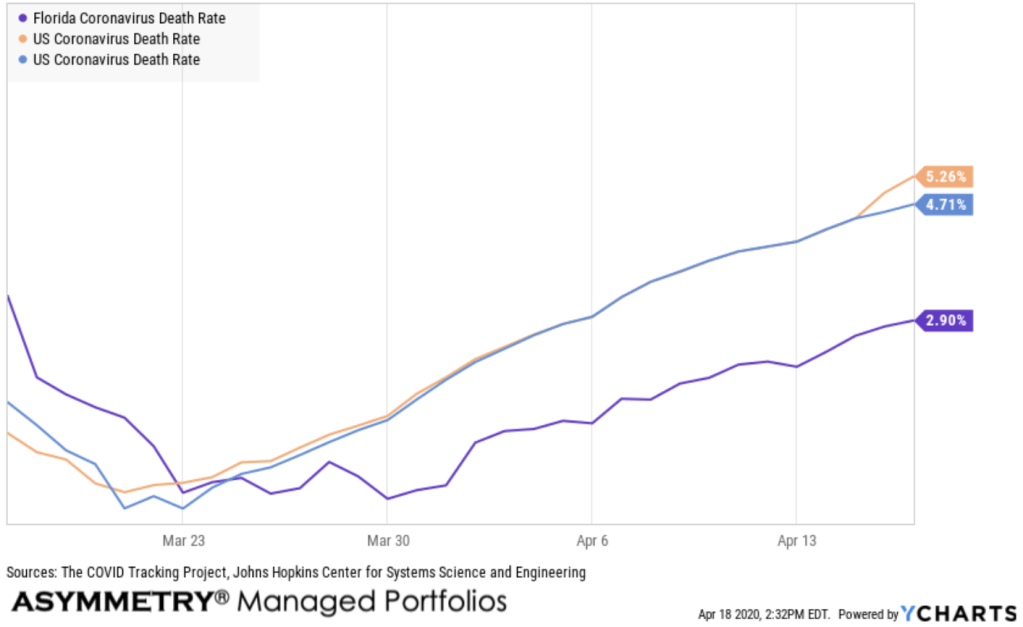

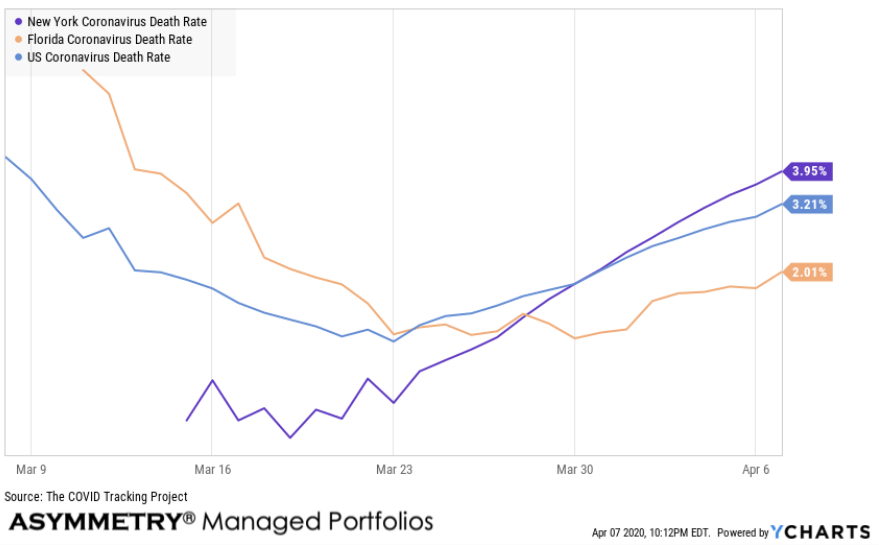

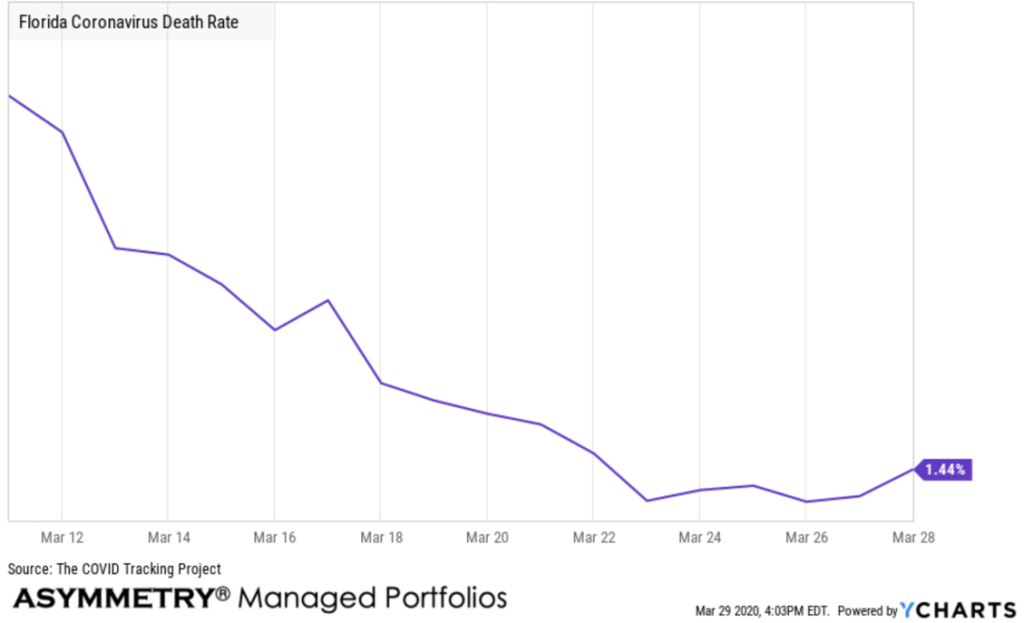

The Florida COVID – 19 Death Rate has been gradually trending down. Florida Coronavirus Death Rate is at 3.67%.

In the past two weeks of May, the death rate was 4.6%, so it is falling.

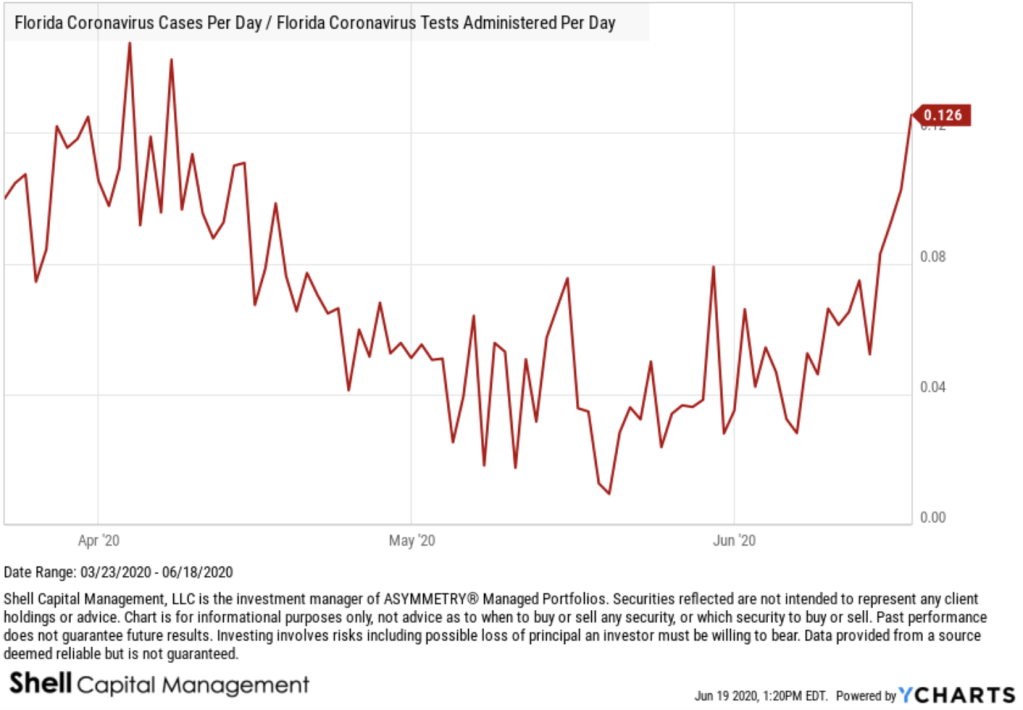

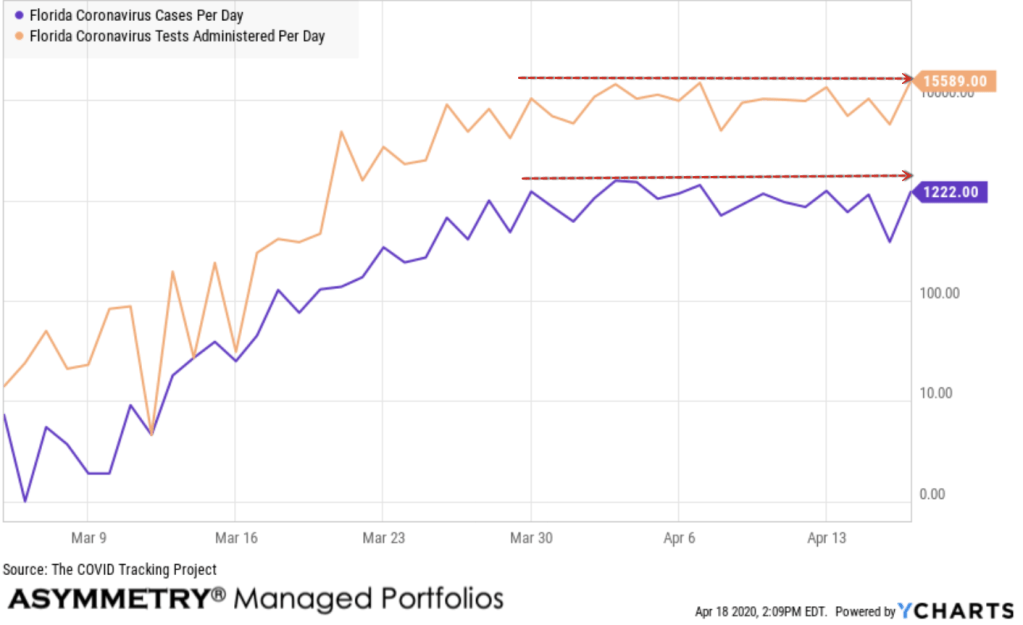

In our investment management, I’ve been drawing ratio charts for over two decades to determine which market or stocks has greater trend momentum than another. When the numerator (top) is trending stronger than the denominator (bottom value) we say it has stronger relative strength or momentum. In this case, I have used Florida Coronavirus Cases Per Day as the numerator (top value) and Florida Coronavirus Tests Per Day as the denominator (bottom value), which shows a clear uptrend in the cases per day relative to the tests per day. This concerns me because of the rate of spread. As you look at the ratio chart, consider that a value of 0 would mean new cases per day is the same as new tests per day. Instead, new cases is currently trending higher than testing.

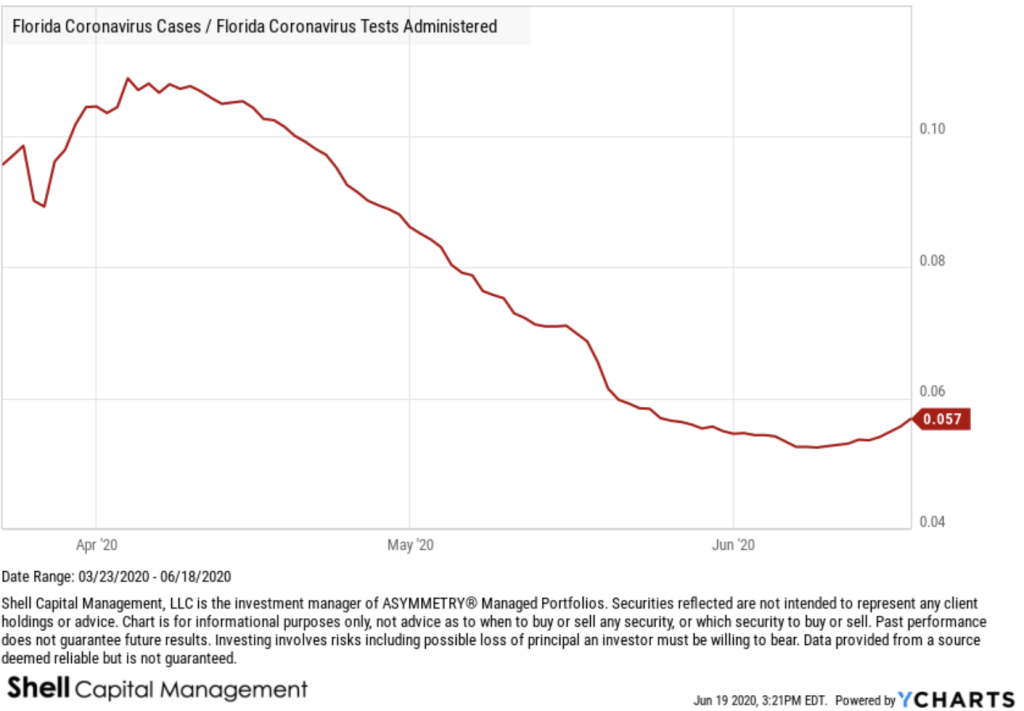

Florida cumulative cases relative to tests administered is also showing some change in trend. the past few weeks. Again, not of the date collected is perfect, but it’s still representative of a statistically significant sample of the population.

My objective for trend following is to identify a trend early in its stage to capitalize on it until it changes.

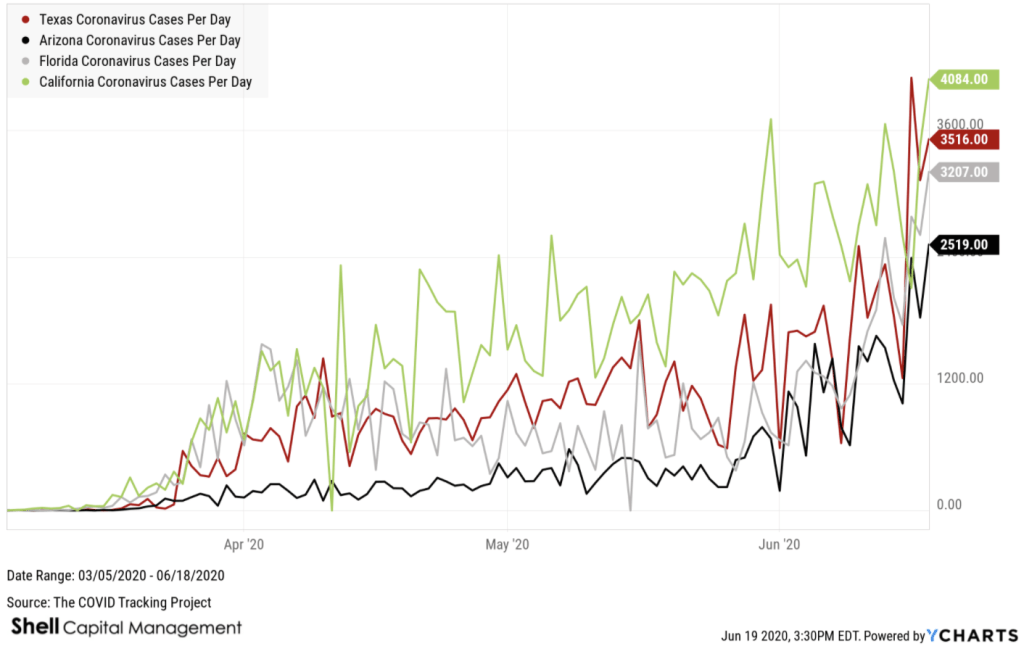

Comparing per day cases to other states doesn’t mean a lot, since the data needs to be normalized. For example, what President Trump said a few weeks ago is a true statement: the number of cases are a function of testing. If we didn’t test and didn’t categorize a case as COVID, there would be no “COVID cases.” Some people, politically motivated, seem to have difficult understanding that simple statement. I’m not politically motivated, so I just say it like it is. With that said, California is winning the match of the most cases per day followed by Texas. Florida is above Arizona.

Again, this doesn’t tell us anything aside from the absolute number. A relative comparison is often necessary and this is an example. For example, we could first calculate per day cases relative to tests or population, then compare them. That’s beyond the scope of my objective today.

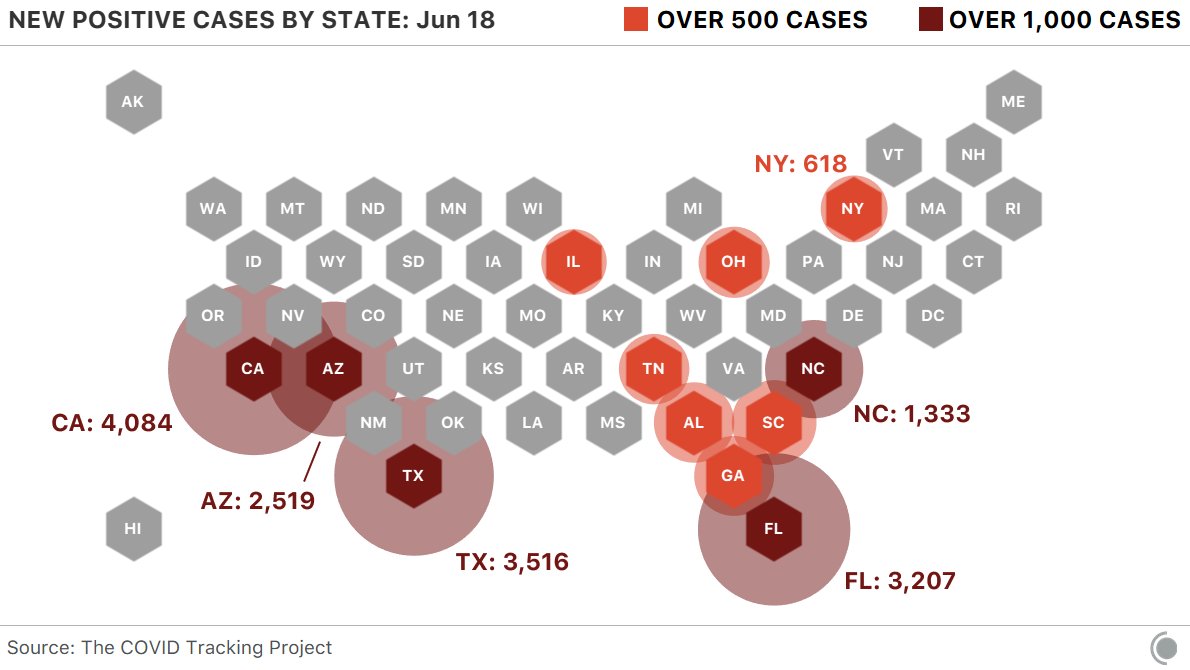

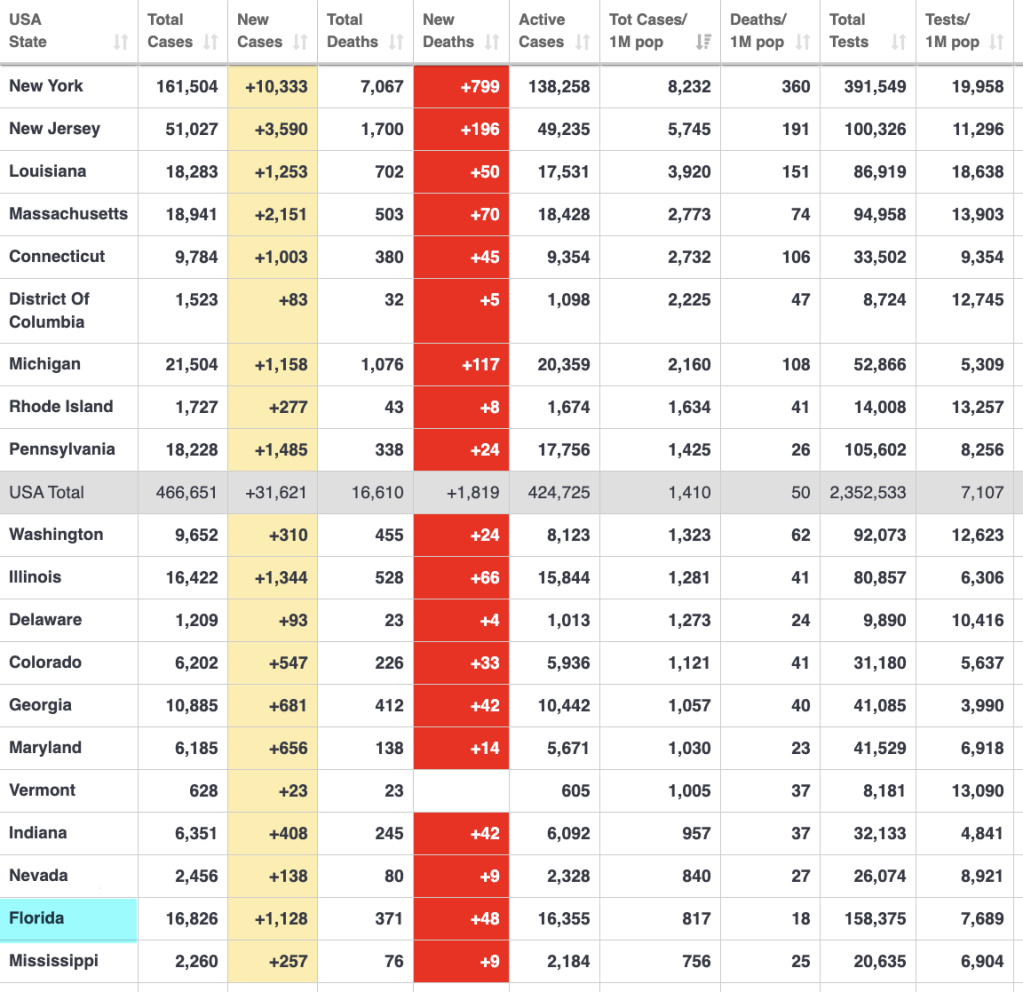

Here are the states that reported over 500 new cases. We are seeing some large bubbles in the southwestern United States right now.

The bottom line is, we want to see these levels drifting down, not up. We want to see this trend down.

People who are at high risk should continue to operate according to the risks, but also keep it in perspective that at this point, it isn’t yet so wide spread.

In the big picture, the population in Florida is 22 million and about 86 thousand cases have been labeled COVID 19. 86,0000 out of 22 million is about 4 tenths of a percent, or 0.40%.

That’s 40 cents of $100.

Our changes of contracting COVID 19 in Florida, then, is less than half of 1% at this point.

Everything is relative.

Join 520 other subscribers

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

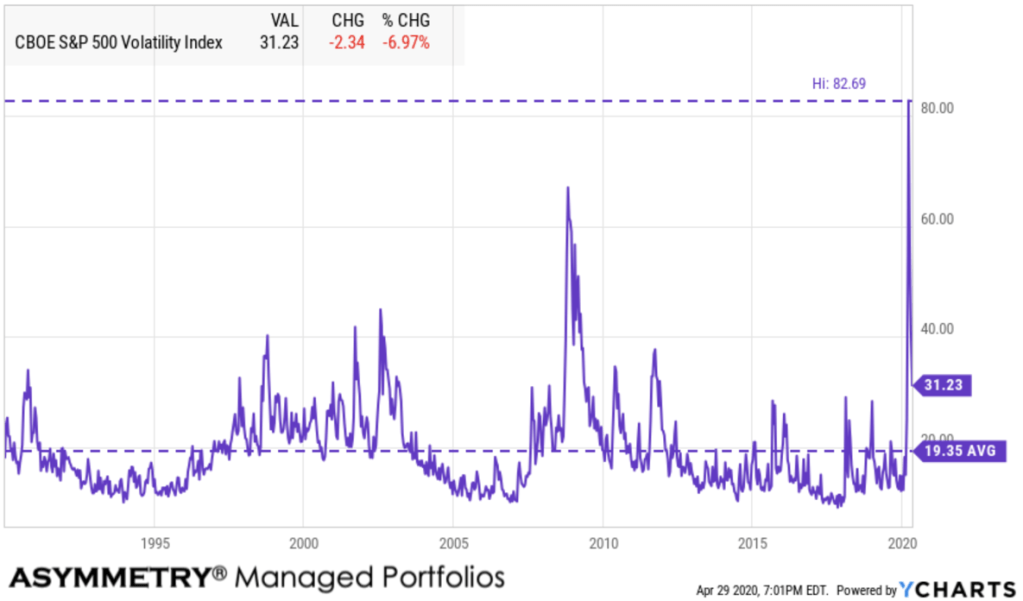

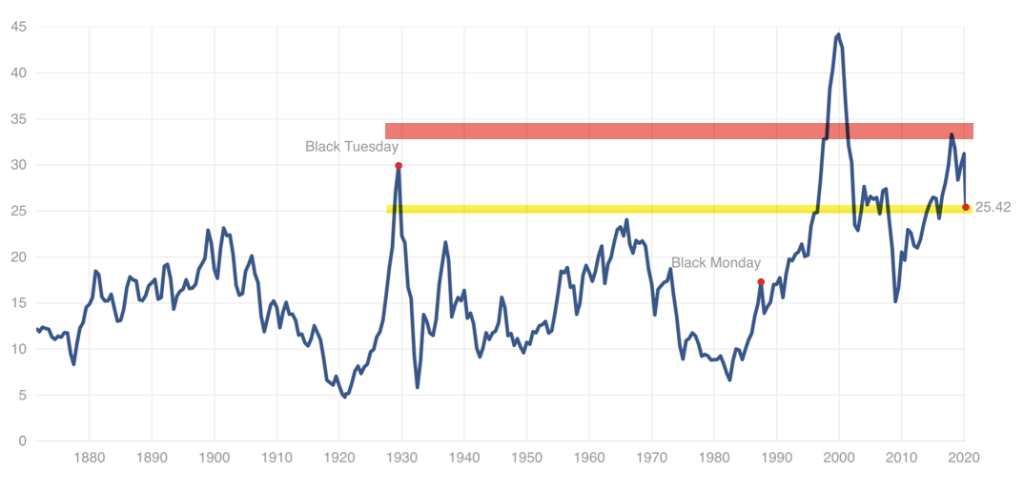

Implied volatility, as measured by the CBOE Volatility Index (VIX) has trended up about 50% since the most recent low on June 5th. I’ll call it a moderate volatility expansion. Normally a volatility expansion from 23 to 40 would be considered a material event, but relative to the highest spike we’ve seen in March, it doesn’t seem huge for 2020.

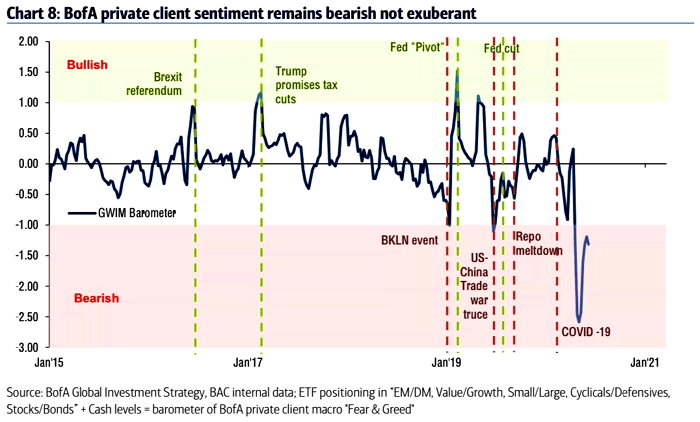

The Bank of America Bull & Bear Indicator is at 0.90 vs. 0.40 last week. It is used as contrarian indicator to identify market extremes in investor sentiment. Currently, their measure of investor sentiment is very bearish, which is bullish for the stock market.

Bank of America Private Client Sentiment shows bearishness, and here is a line chart showing its history.

On the topic of investor sentiment, and the Bank of America Bull & Bear Indicator, here is a chart of its history going back to 2002. As marked on the chart, it was backtested pre-2013.

I share the CNN Fear & Greed Index a lot, because it’s easily assessable, so anyone can view it. The Fear & Greed Index is neutral right now.

Within the Fear & Greed Index are seven different investor sentiment indicators. Unlike the Bank of America Private Client Bull & Bear Indicator, which is a survey of their clients, the Fear & Greed Index is derived from quantitative technical indicators.

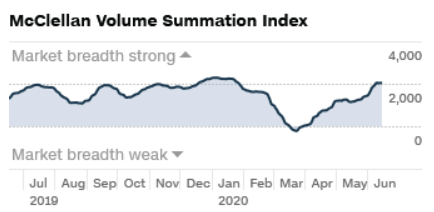

Stock price breadth, or how well stocks are participating in the uptrend, is the leading driver on the Greed side. They use the McClellan Volume Summation Index, which measures advancing and declining volume on the NYSE. It shows during the last month, approximately 8.08% more of each day’s volume has traded in advancing issues than in declining issues, pushing this indicator towards the upper end of its range for the last two years, which is extremely bullish.

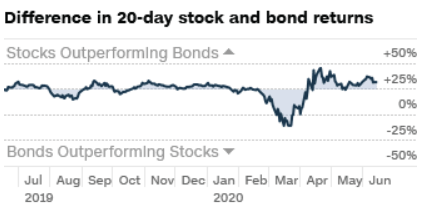

The only other of the seven indicators showing bullish investor sentiment is safe haven demand. That is, the demand for bonds over stocks. They measure it by the difference between the past 20 day stock and bond returns. Stocks have outperformed bonds by 6.99% during the last 20 trading days. This is close to the strongest performance for stocks relative to bonds in the past two years and indicates investors are rotating into stocks from the relative safety of bonds. Of course, this bullish investor sentiment is a sign that greed is driving the market. Notwithstanding these two extremes, overall, the Fear & Greed Index remains neutral.

Value is a Value

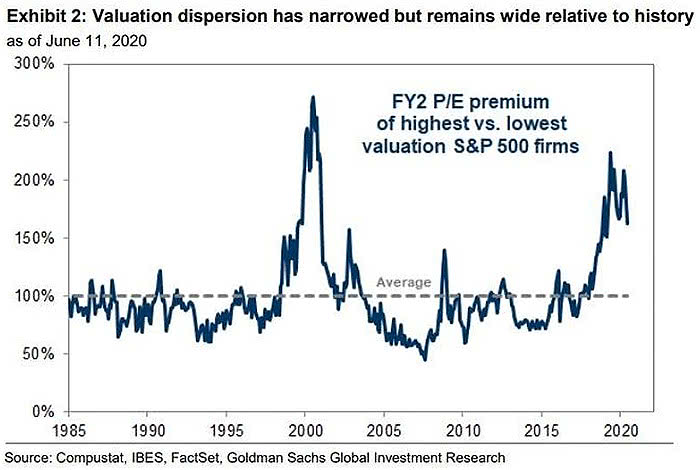

The dispersion of stock valuation multiples between the lowest and highest valuations has narrowed. But, despite the recent relative strength in value, it is still wide relative to history. So, value stocks remain a relative value.

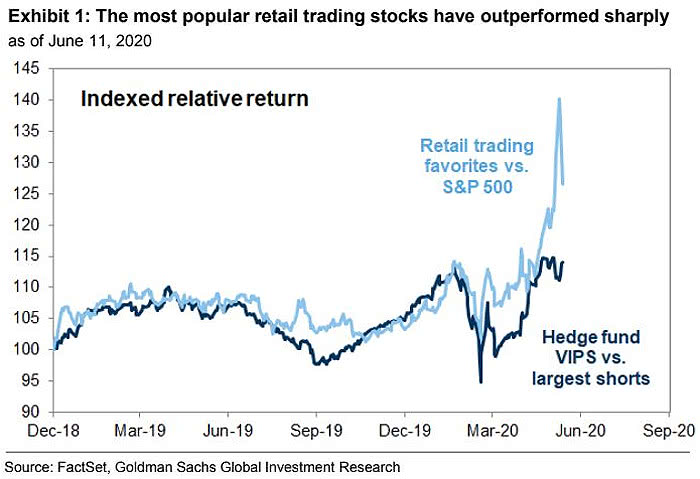

Hot Momentum Stocks are Showing Relative Strength

According to Goldman Sachs, the most popular retail trading stocks have materially outperformed the S&P 500, so far.

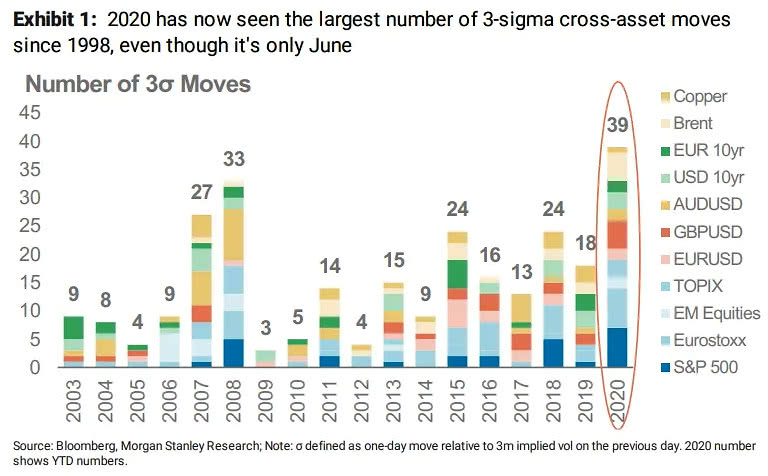

Cross-Asset Realized Volatility has been Extreme

Another sign of dispersion is the number of 3 standard deviation prices moves. We’ve already seen more extreme trends across asset classes in 22 years.

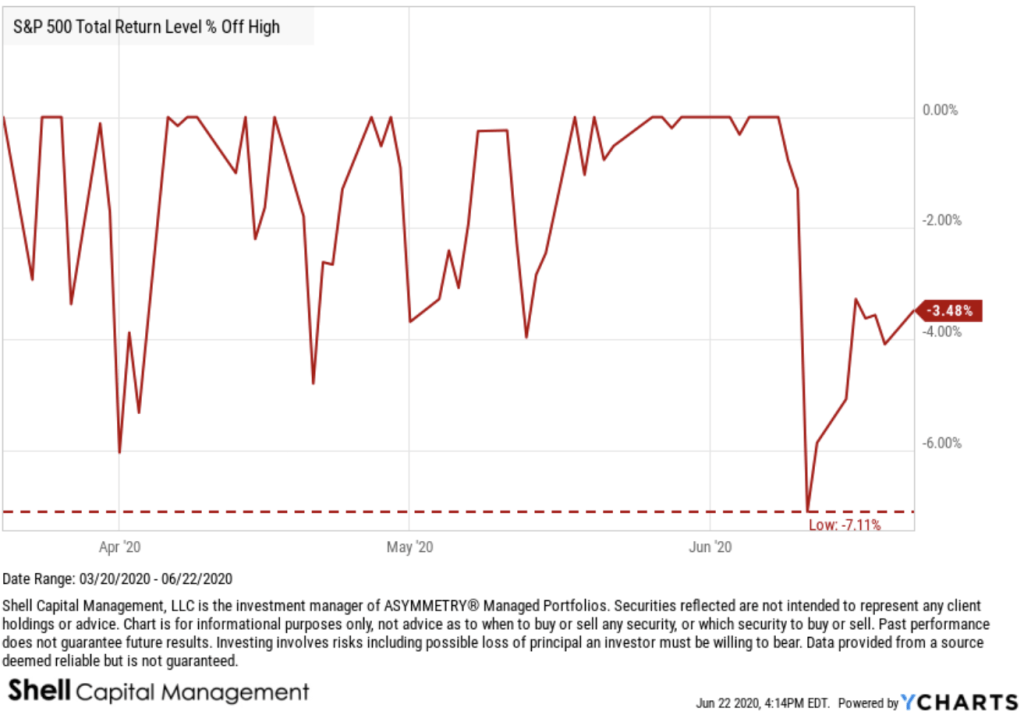

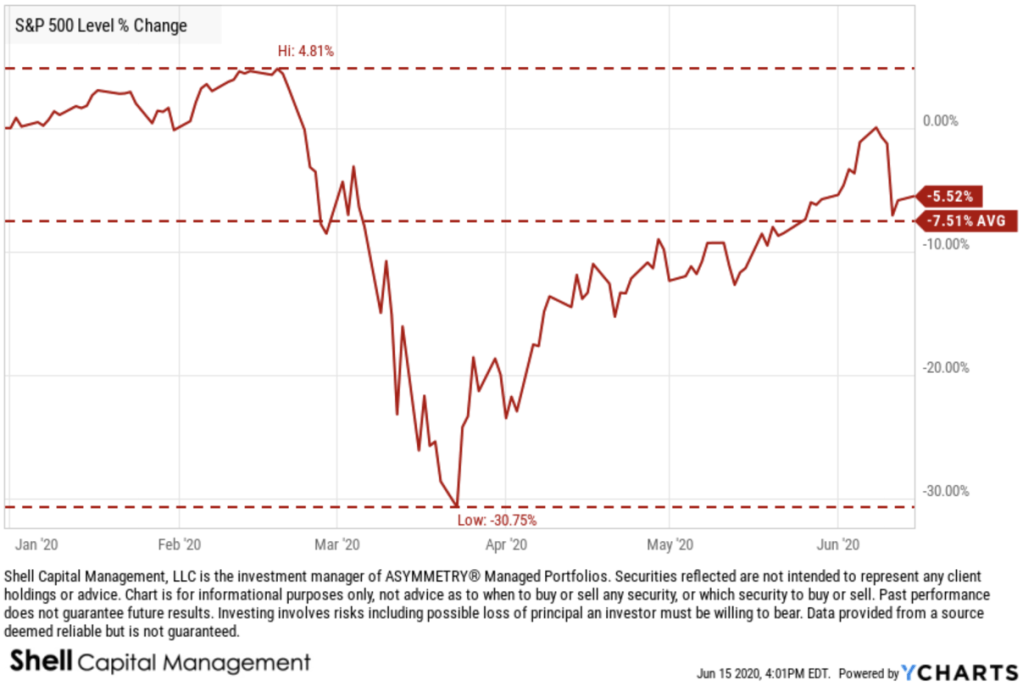

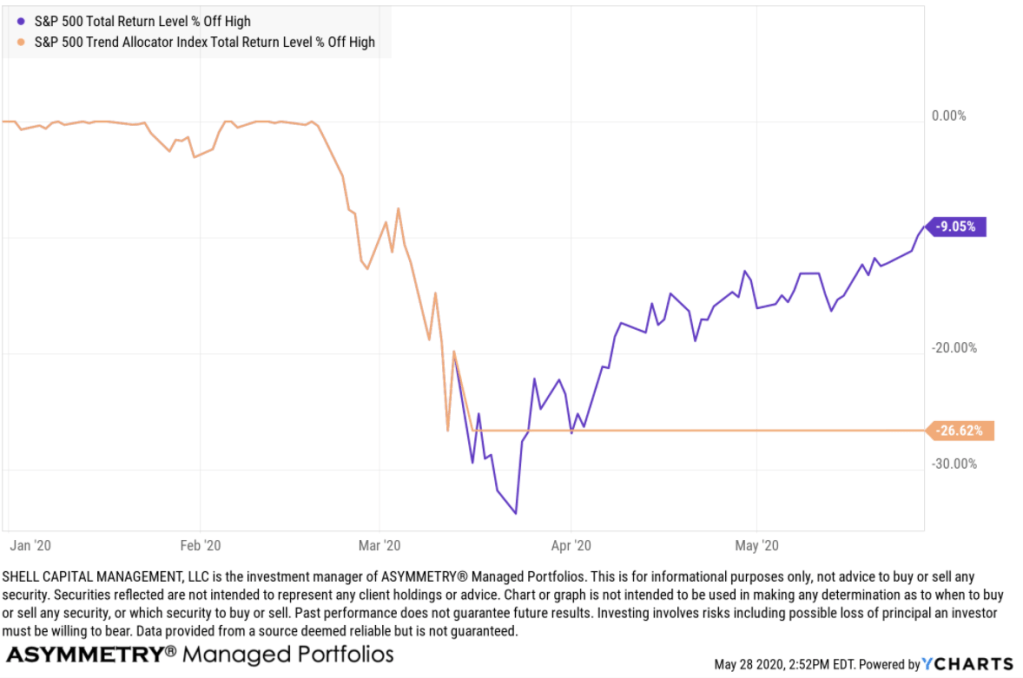

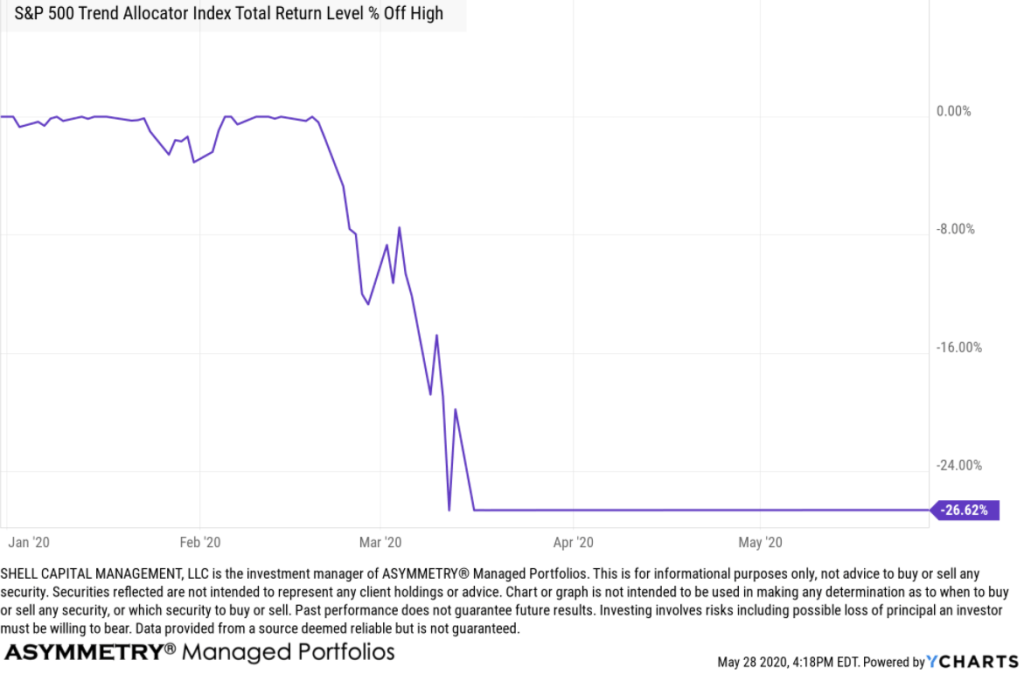

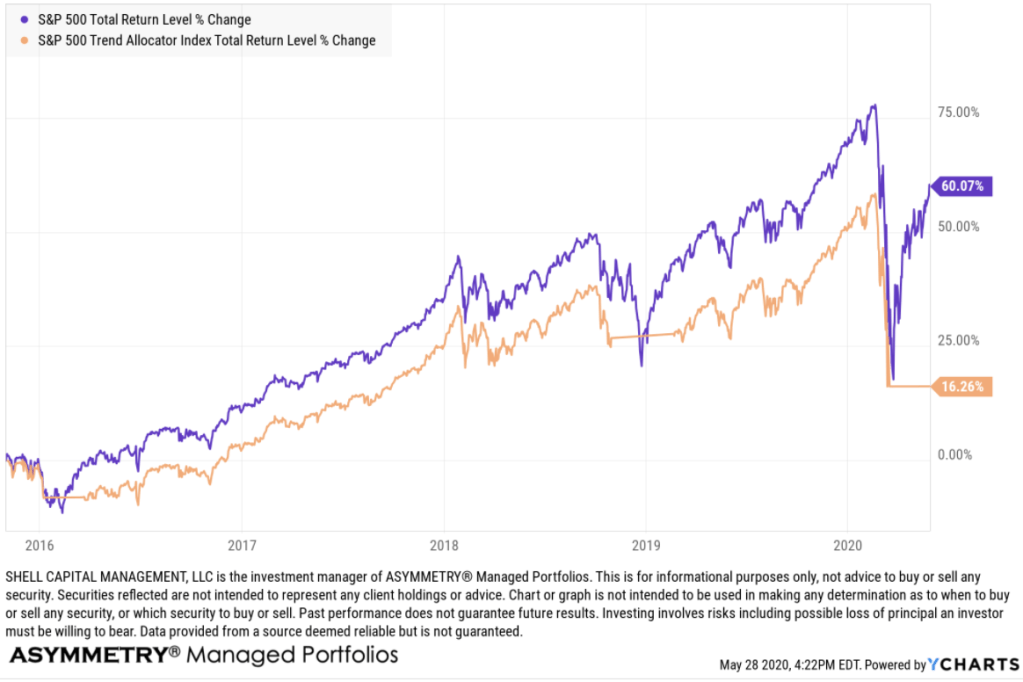

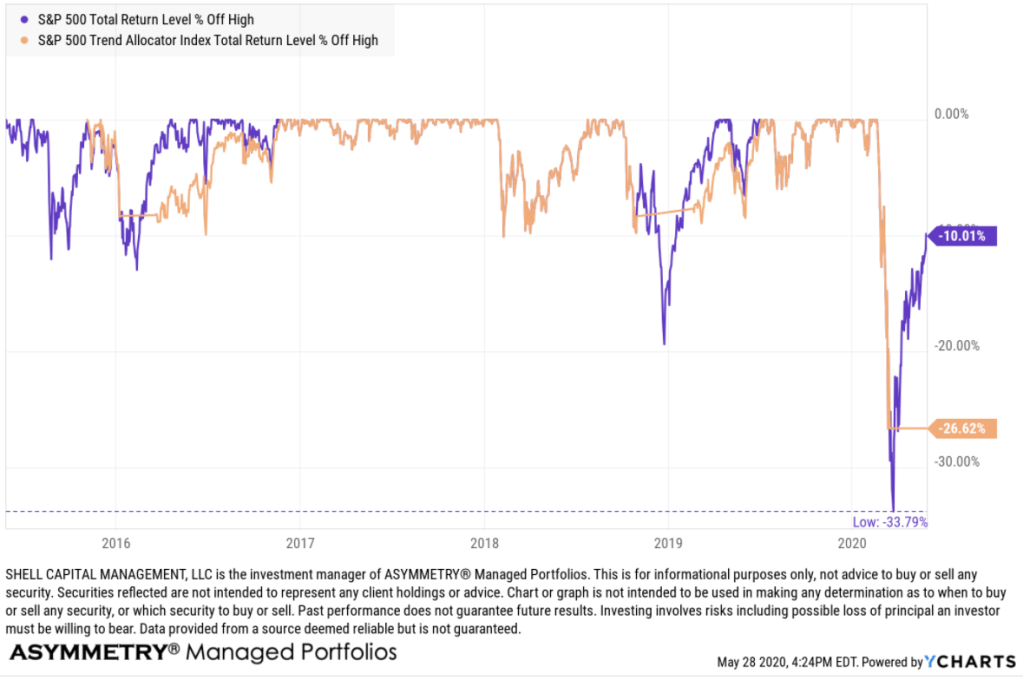

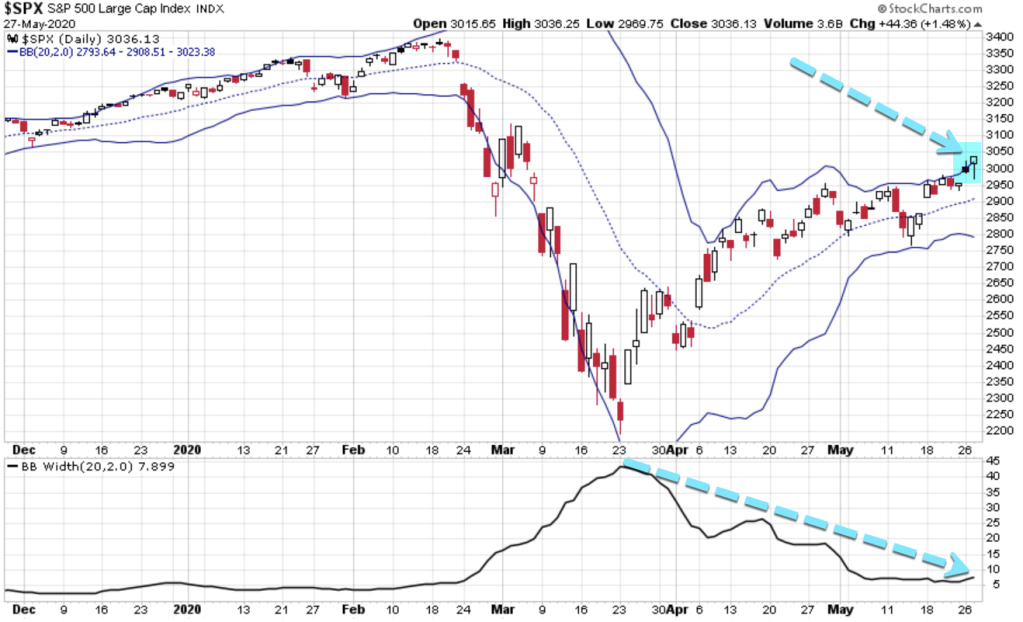

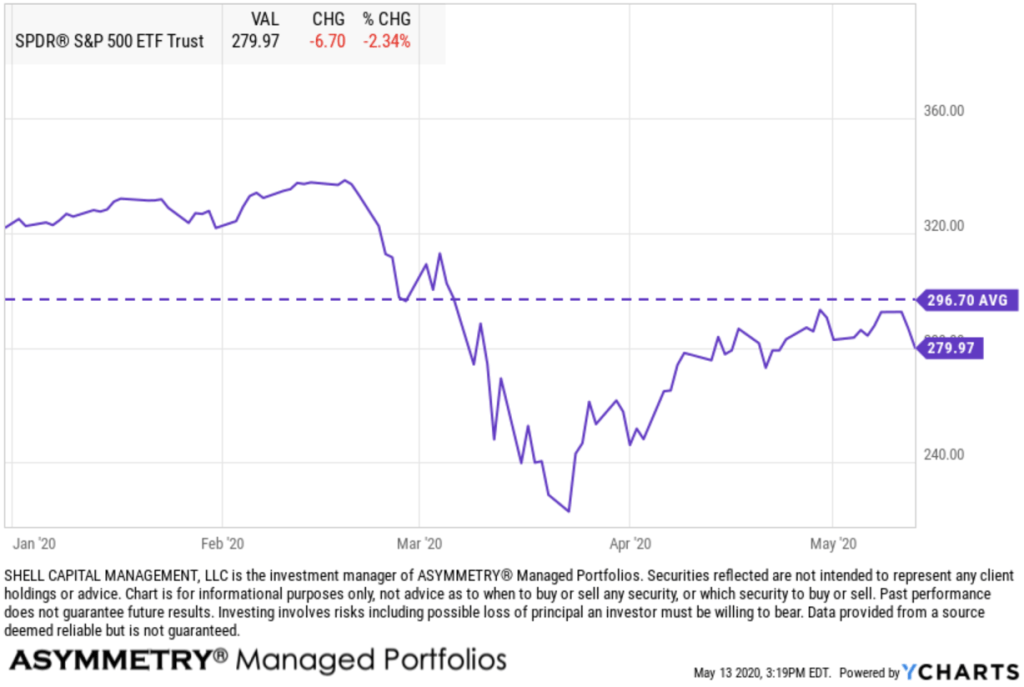

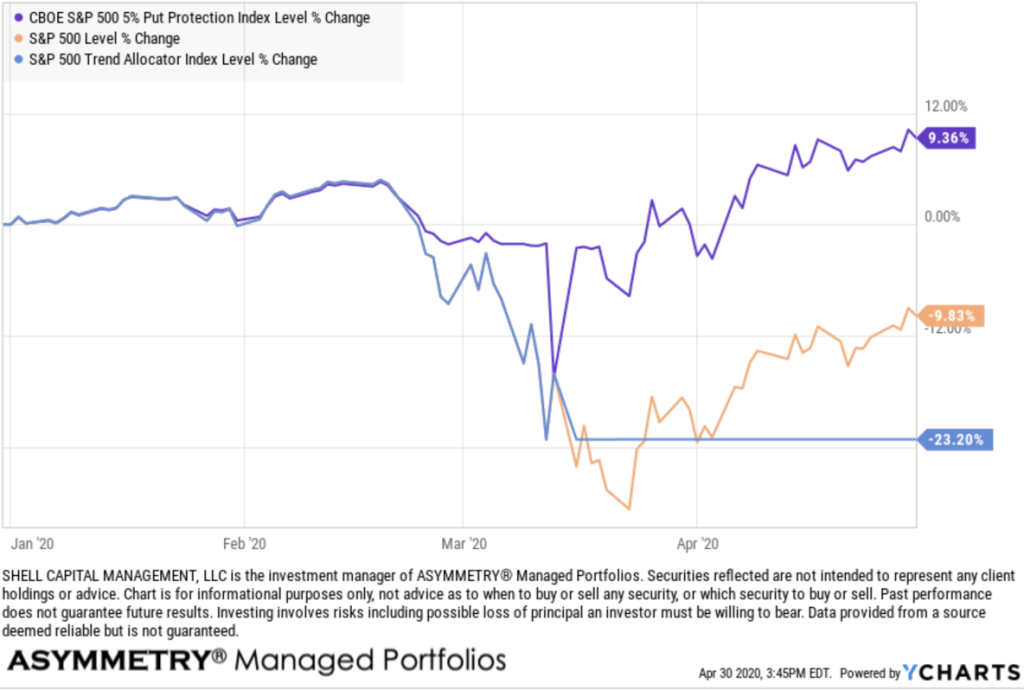

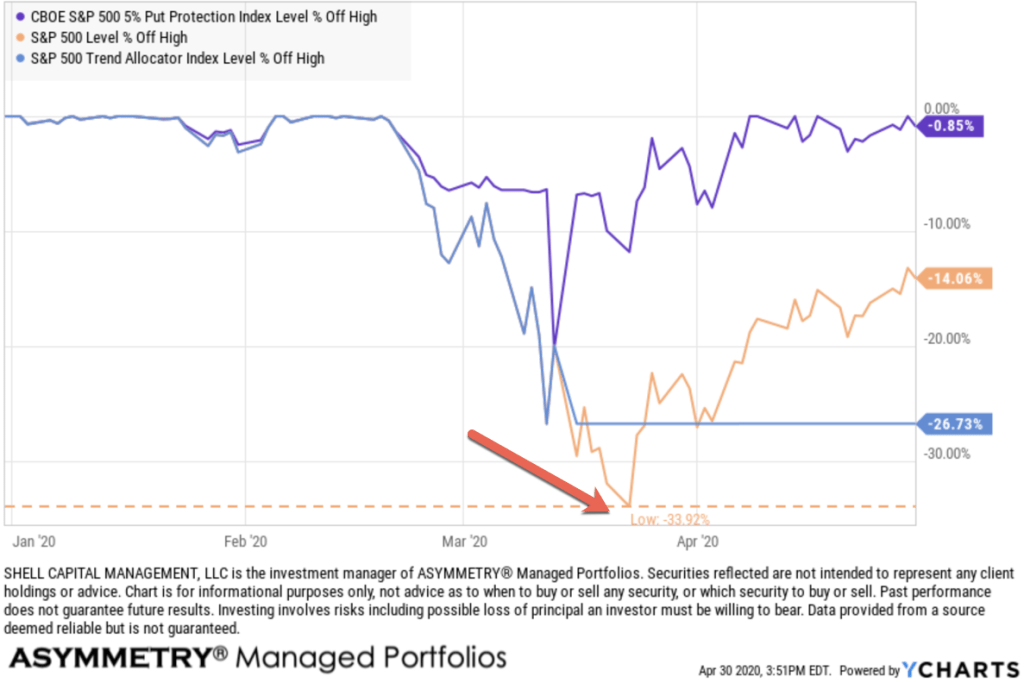

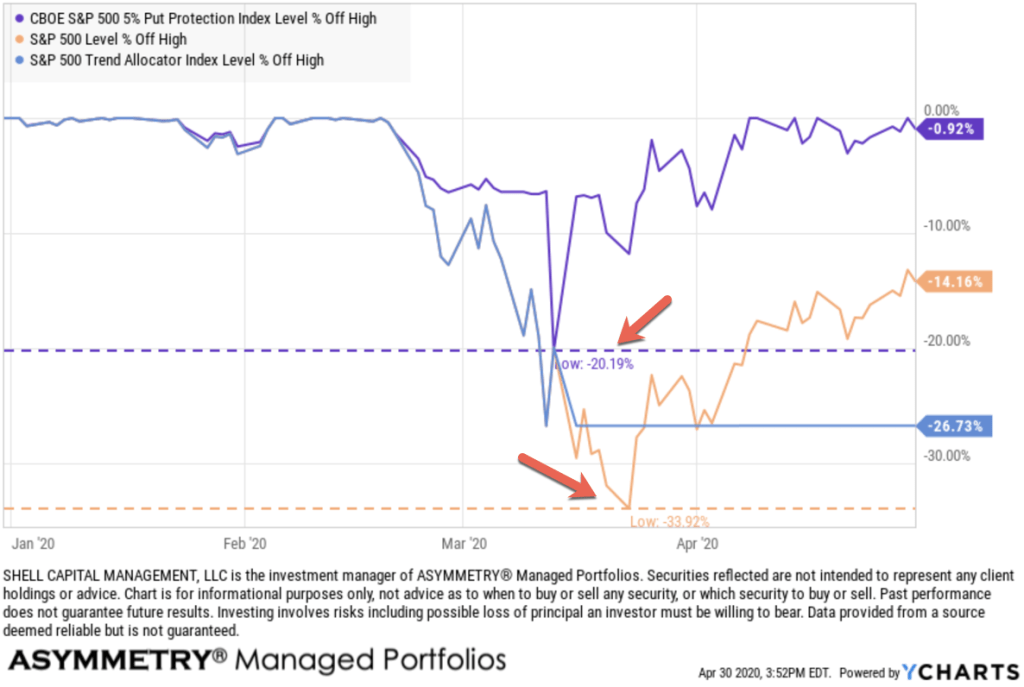

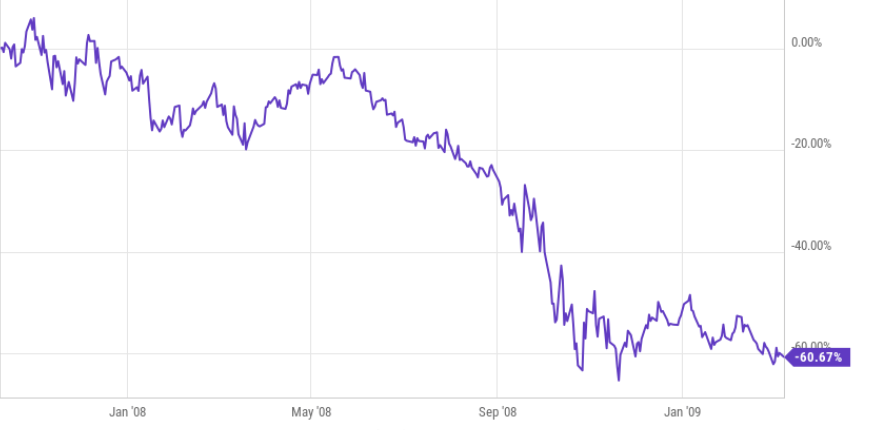

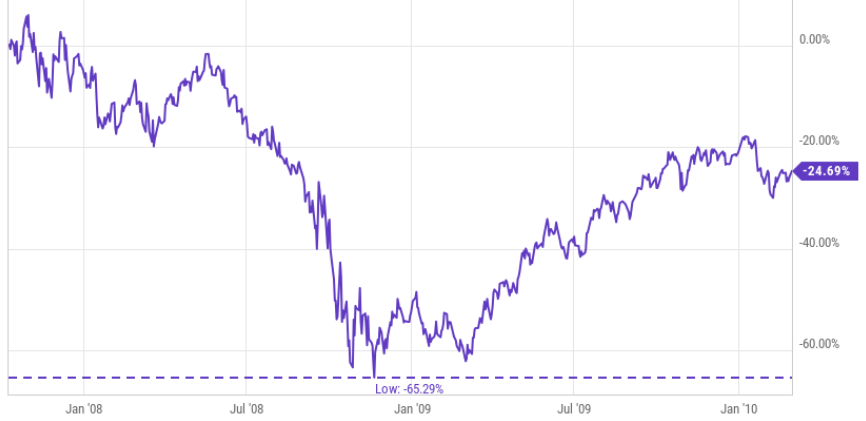

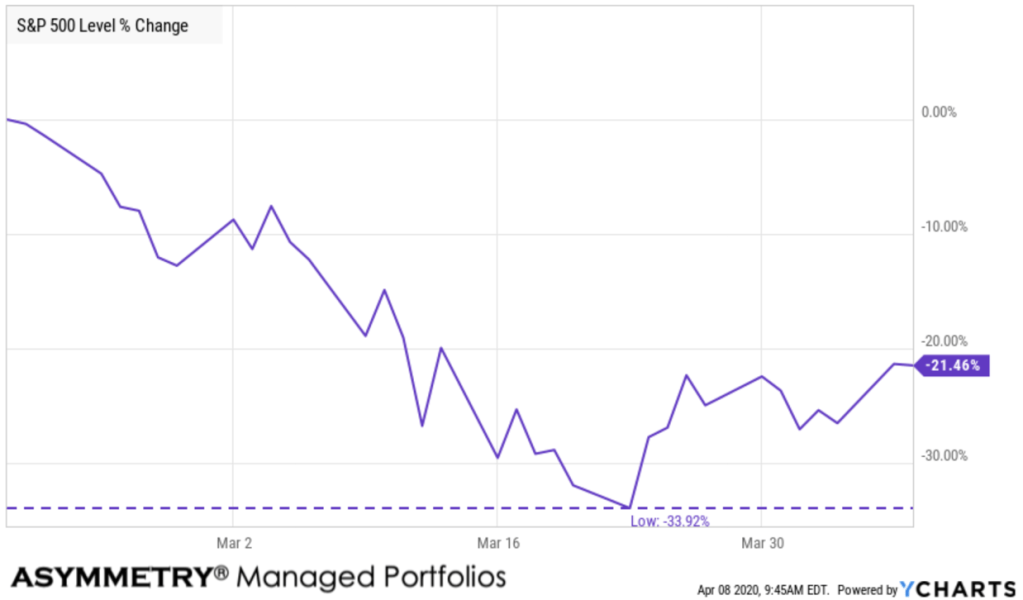

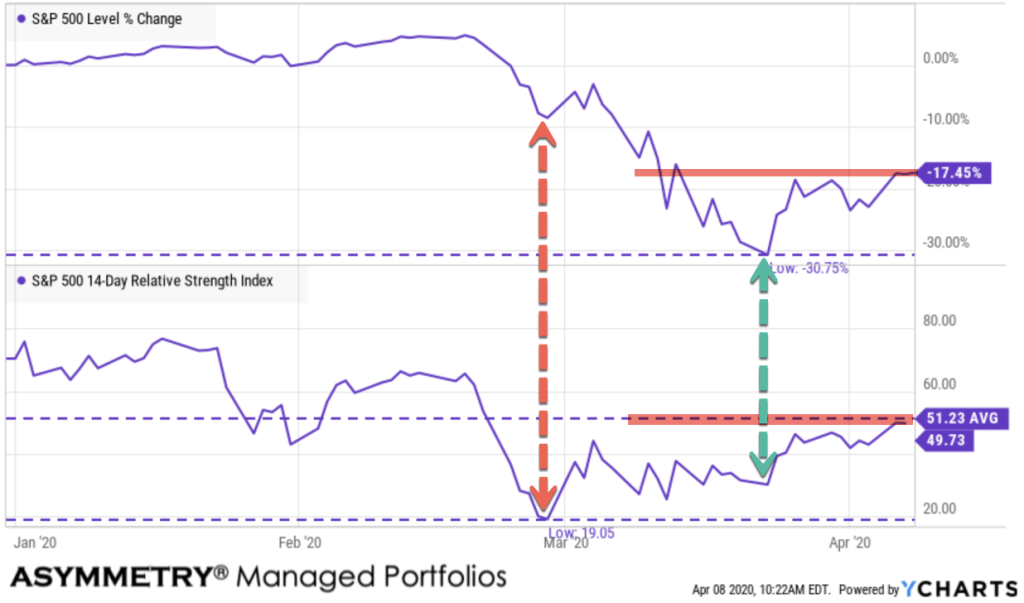

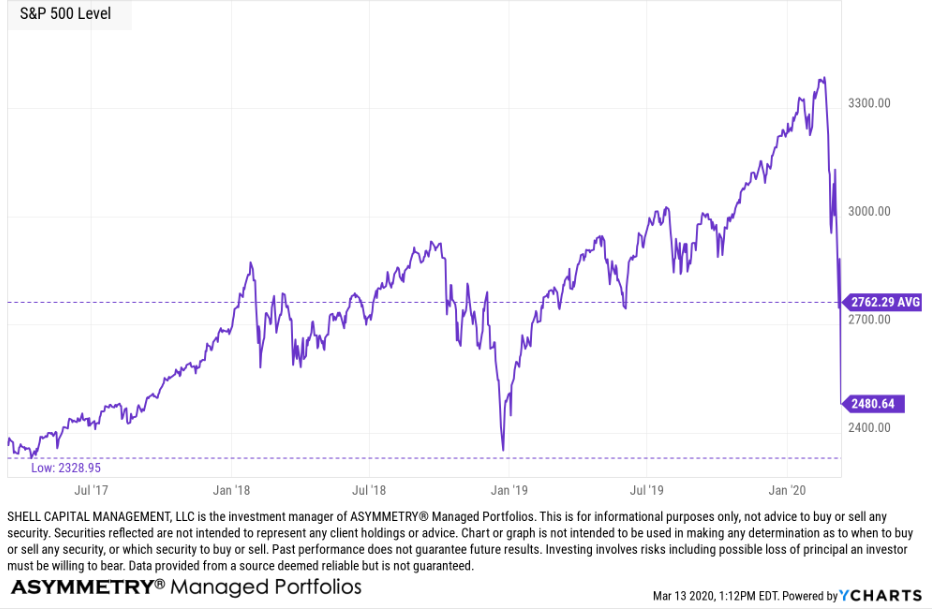

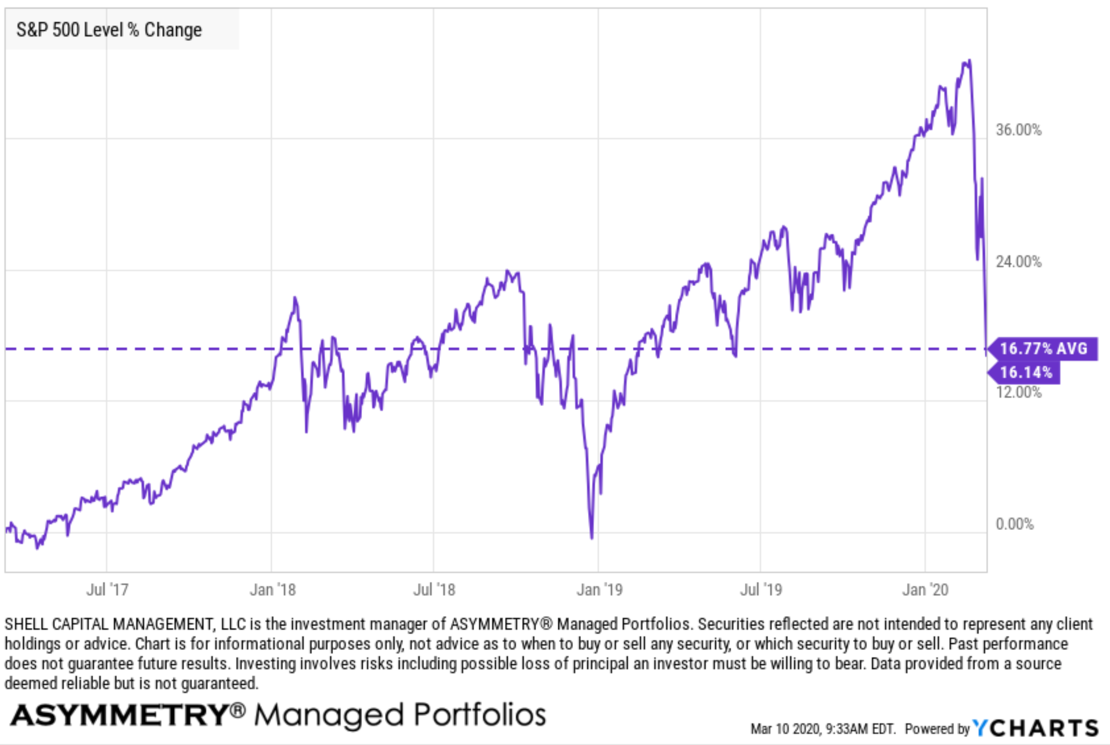

Despite the impressive V shaped rally from what is so far the low on March 23rd, I continue to notice the mean reversion year to date and over the past year. Here is year to date, and I marked the high, low, and average percentage.

At the low, the S&P 500 was down about -31% YTD. With the help of a very aggressive Federal Reserve proving liquidity, it has recovered most of the decline in one of the fastest in history.

It ain’t over till it’s over, and this ain’t over.

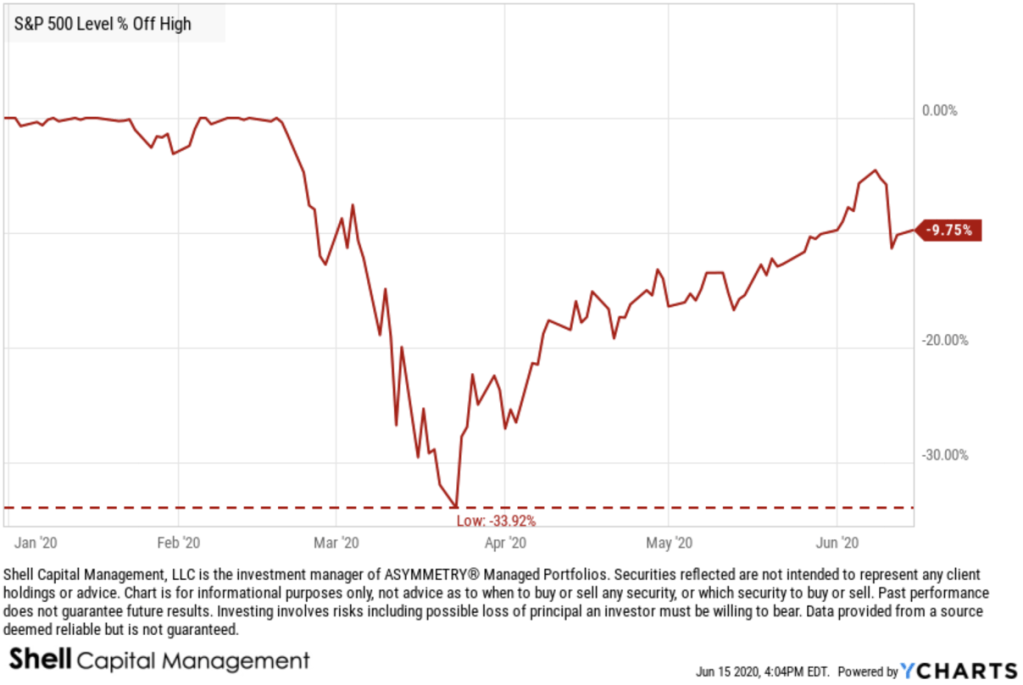

Asymmetry is about the upside vs. the downside in terms of asymmetric risk/reward. No observation of the price trend is complete without also noting the downside drawdown it took to achieve it. The drawdown for the S&P 500 was an astonishing -34% in just 23 days. It’s a reminder of risk.

I believe risk must be measured, directed, and controlled if we are to compound capital positively.

It doesn’t matter how much the return is if the downside risk is so high you tap out before it’s achieved.

Clearly, in 2020, we’ve surely seen some of the finest examples of risk, divergence, and volatility.

Join 520 other subscribers

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

People tend to overreact and under-react to new information.

We observe it in the global capital markets more frequently than anywhere, and with immediate feedback.

So, those of us who are adept at identifying and monitoring directional trends in global markets have an advantage in researching trends of all kinds if our quantitative trend methods are robust, and our qualitative judgment and decision-making process is repeatable.

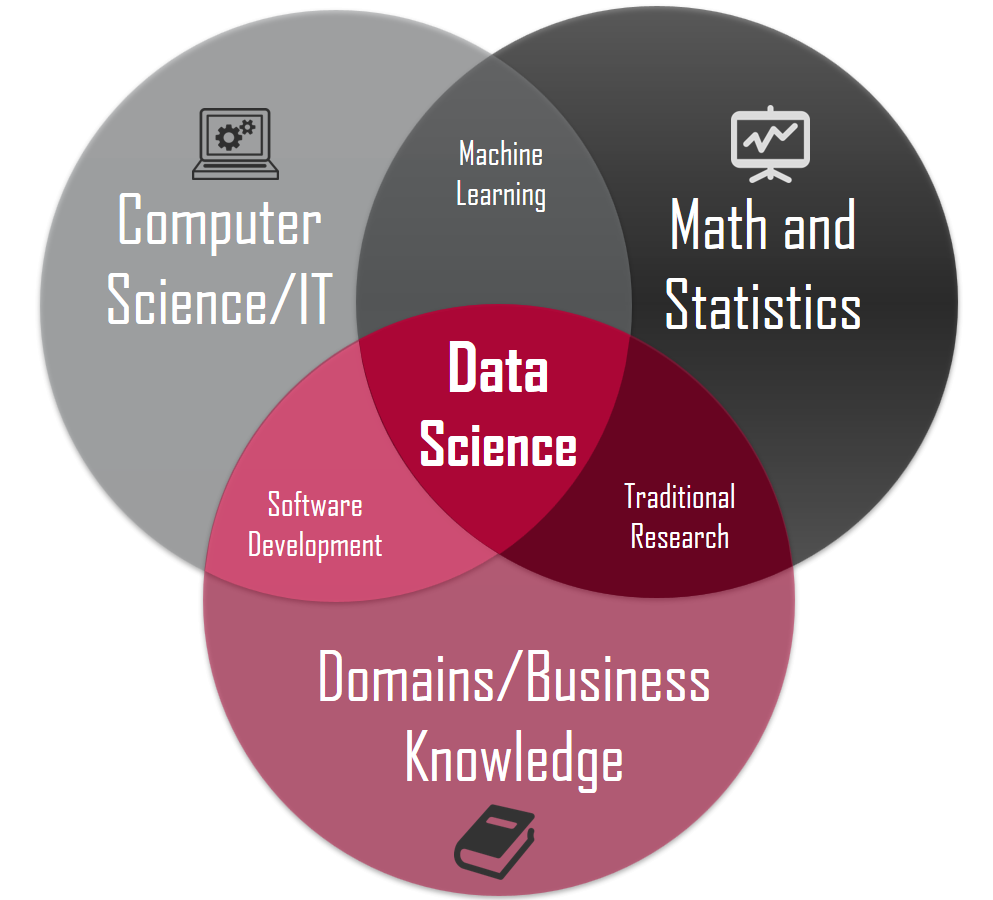

Intellectual skills that are associated with acquiring reliable information about nature are parts of the scientific process. Scientists of all kinds need skills like: communicating, observing, classifying, measuring, predicting, inferring, and researching.

Science isn’t just science, there’s also some art to it. I believe the first skills are more art, such as communicating, observing, classifying.

Many say investing and investment management is both art and a science. Some believe investment management is more art than science, others believe it’s more science than art. Quants try to make it more scientific than artistic.

I do a combination. I am Man + Machine.

The way I look at trends and how time series interact with each other is a robust process that may be applied to anything.

I don’t read articles in Bloomberg or The Wall Street Journal to hear the opinions of others to decide what I believe for myself. When I was a young rookie I did read a lot at first, as we all do, then learned the hard way to focus my efforts on my own original research and thinking.

I do best when I do my own work, as an independent thinker.

So, over the decades as a professional researcher, I first inspect the data to observe any trends and then make sense of it afterward. Sometimes my intention is for predictive analytics, other times it’s just prescriptive. predictive and prescriptive analytics. Predictive analytics provides us with the raw information for making informed decisions, while prescriptive analytics provides us with data-backed, evidence-based decision points that we can weigh against one another.

The scientific method is an empirical method of acquiring knowledge through careful observation, and applying rigorous skepticism about what is observed, realizing how cognitive assumptions and bias can distort how one interprets the observation.

Descriptive Analytics, applying data aggregation and data mining to provide observations andinsight into the past to answer:

“What has happened?”

Predictive Analytics, applying statistical models and probabilistic forecasting methods to understand the future and answer:

“What could happen?”

Prescriptive Analytics, applying simulation and testing algorithms to advise on possible outcomes and answer:

“What should we do?”

The Scientific Method and experimenting is a systematic approach to problem-solving and decision-making.

An algorithm may look something like this:

Problem —> Hypothesis —-> Prediction —-> Test Predictions —> Evaluation

We all have biases. All industries have biases. Sometimes these biases gave blindspots. Our biases that can narrow our vision and influence behavior and beliefs. It’s why in asset management, we often consult with researchers outside the industry to help avoid blind spots from industry bias. For example, the personal financial planning profession has a tendency to blindly say “balance your risks and rewards” and “balance your portfolios”, which is about the silliest things I’ve ever heard.

If you balance your risk and reward, you get symmetry on your statement.

If we want asymmetry, we have to skew the risk and reward positively.

It’s essential to identify blind spots, own them without being defensive, and adjust our behavior to avoid it.

MY OBSERVATIONS OF COVID 19

I have an advantage, because I observe COVID 19 trends and rates of change as it is, without any bias as to beliefs about the disease and such. That is, I’m just purely looking at the data we collect and feed into our systems for observation.

It’s like this:

I focus on; what has changed?

I look for extremes in levels, like new high or low breakouts.

I also monitor the rates of change. Fast breakouts are more likely to form an ongoing trend than slow.

FLORIDA COVID 19 UPDATE

As COVID 19 and the mass quarantine strategy for suppressing the spread has become a political debate lately, so some of you may perceive what you are about to read that way.

Don’t.

I have no political bias about this whatsoever. My personal preference is to get past this virus as quickly as possible with as little human suffering as possible. Ignoring the data and facts doesn’t get us there. Exaggerating the data and facts doesn’t either. So, I suggest you try to see the trends for what they are, as I am.

My home state of Florida is now, unfortunately, trending in the wrong direction. I pointed it out with some fellow money manager friends last week of a potential breakout in the trend and it has since trended higher for a meaningful and material breakout. No one wants businesses to open and get back to normal more than me, but what is, is. The cases per day is in a strong uptrend. The prior high was 1575 on April 3rd and 1601 on May 16th. Yesterday was 2581. I hope to see this trend down.

NEW UPTREND IN FLORIDA CASES NOT DRIVEN BY NEW TESTING

The first hypothesis we think of is, well, maybe the uptrend in driven by an increase in testing. Naturally, increasing the absolute testing also should increase the number of positive tests. That isn’t the case. The high in testing was May 20th in Florida. The testing per day remains materially below that level according to the most recent data.

Keep in mind, the lower line is tests administered per day, so there is a lag between testing and the classification of a positive case. In fact, there are natural lags in all of this data. For example, I don’t expect to see the results of the protests until a week or two afterward to account for the lag in showing symptoms, going to get tested, and getting the test results. If there is any increase in the protesting areas, we’ll hear about it next week or later.

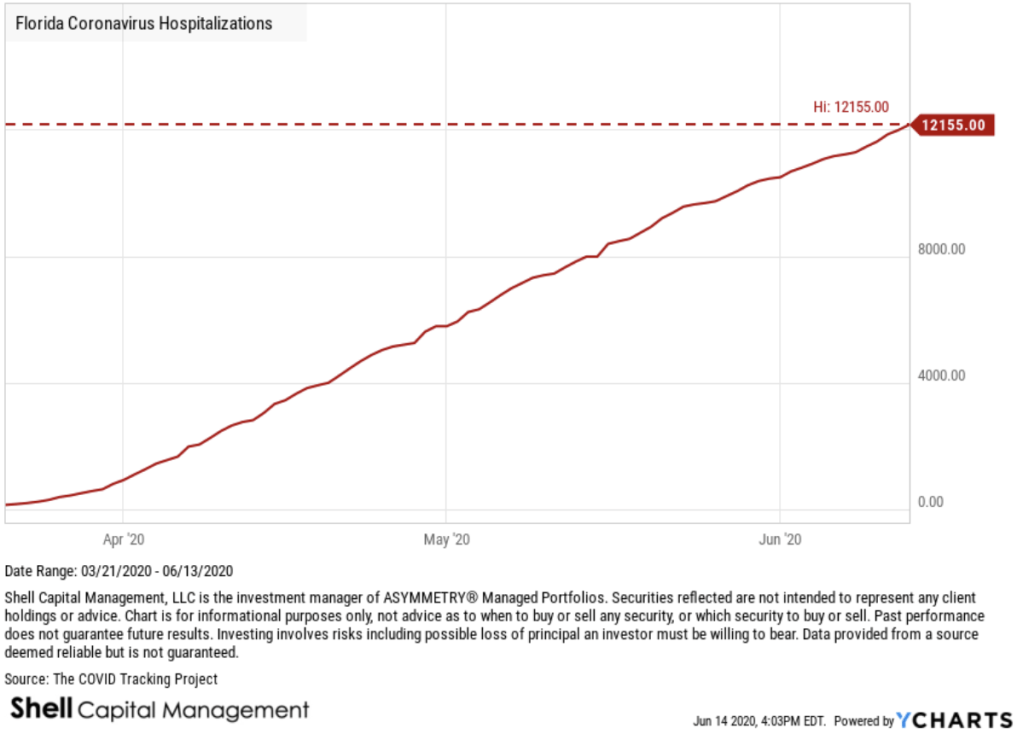

FLORIDA COVID 19 HOSPITALIZATIONS AT AN ALL TIME HIGH

Not much to add here. It is what it is.

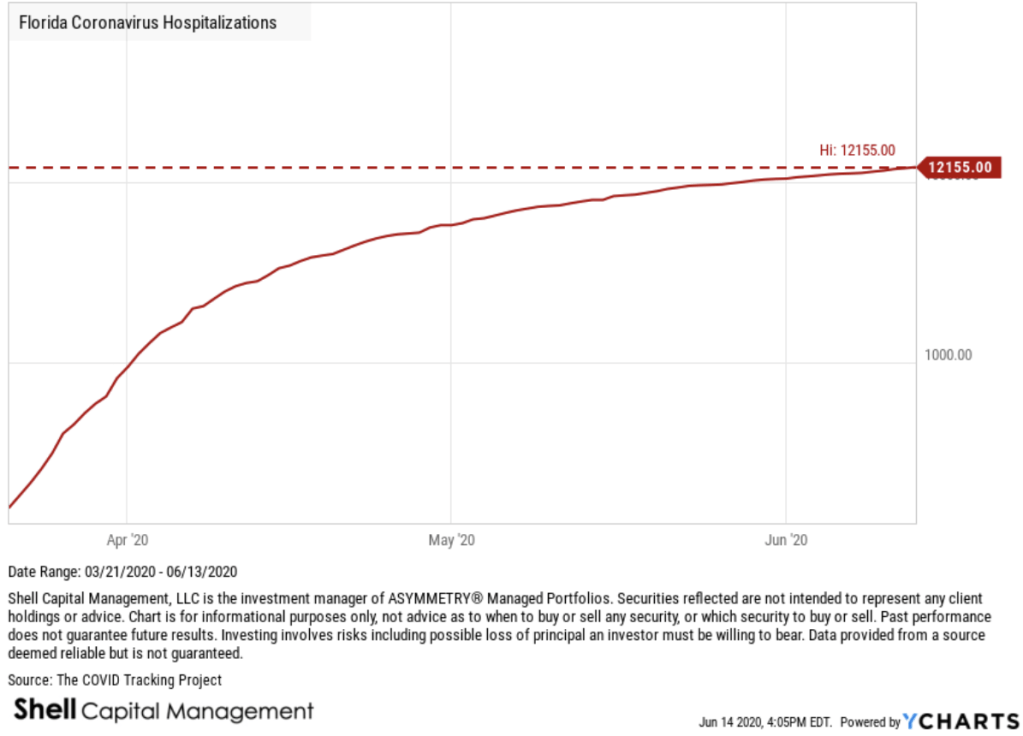

I can try to make it seem better with a logarithmic based chart, which draws the chart in a way that two equal percent changes are plotted as the same vertical distance on the scale. It visually normalizes the rate of change. The good news is the rate of change overall is slowing. The bad news is this could look like an S-curve later, which would be typical of a spread.

By the way, here is the log chart of the new cases per day. We normally use a logarithmic chart scale for long term charts to normalize the data especially if I’m comparing it to something else where relative strength (rate of change) is measured. But here, we still see a breakout in rate of change. So, it’s a material breakout in my opinion, but I hope it breaks down.

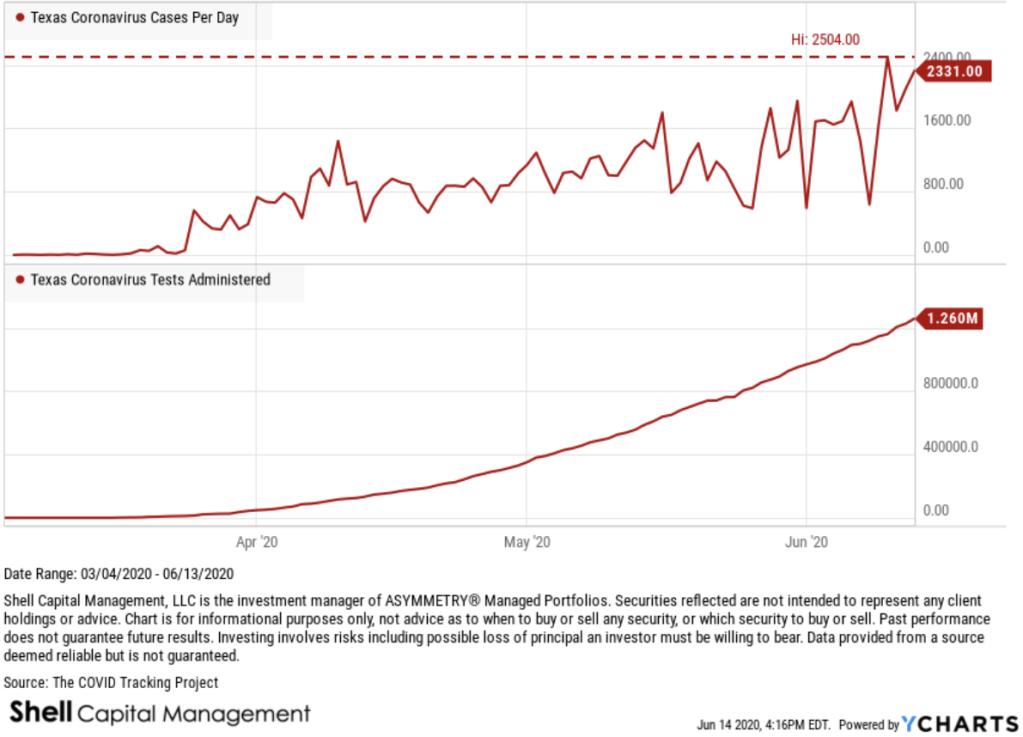

Unfortunately, three of the new uptrends are in states were we have clients; Florida, California, and Texas. Next up is Texas.

TEXAS COVID 19 UPTREND

New cases in Texas is trending up to all time highs. I think Houston, Texas is now at risk of another stay-at-home order.

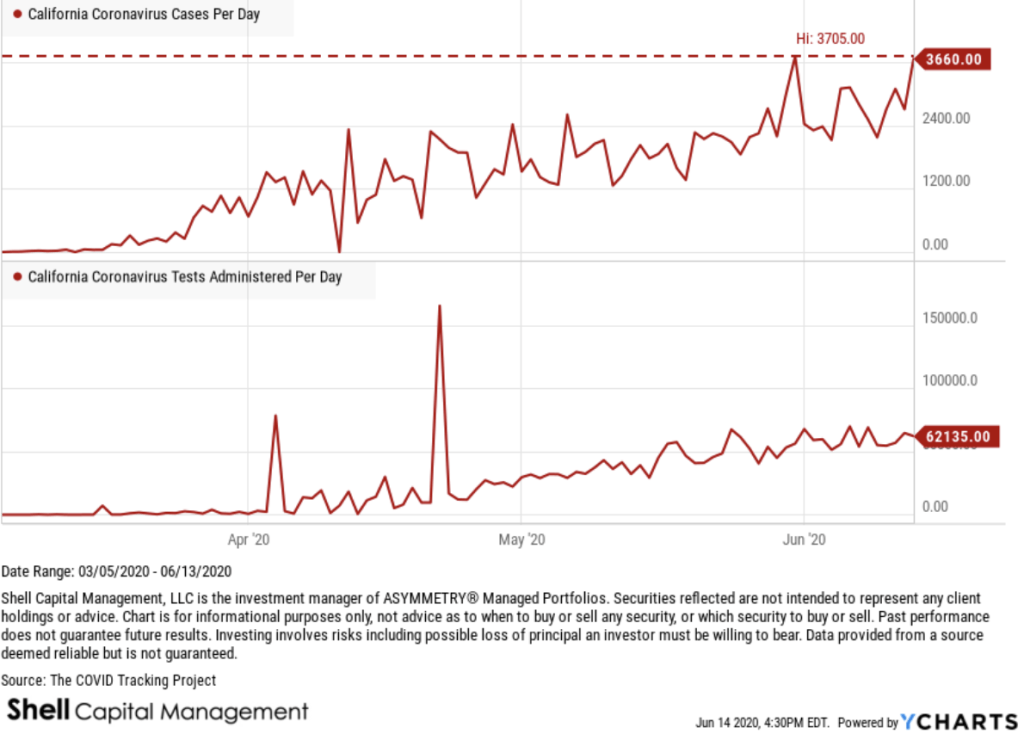

CALIFORNIA COVID 19 TREND

California new cases per day has trended up to the all time high again. It doesn’t seem to be in direct result of more testing per day, either.

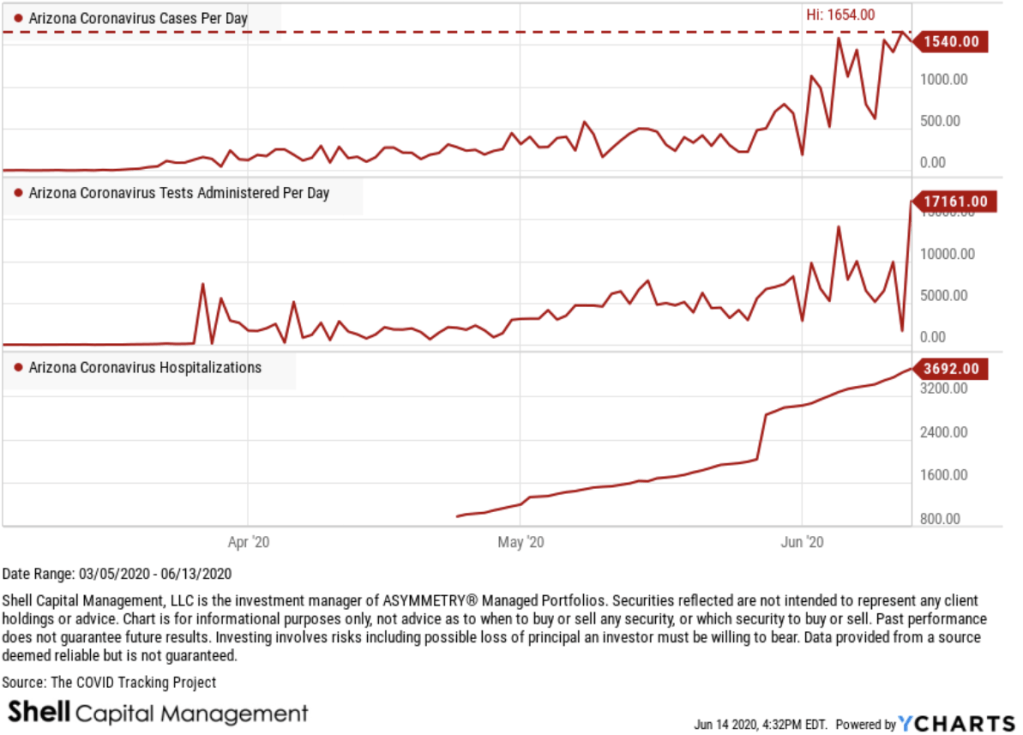

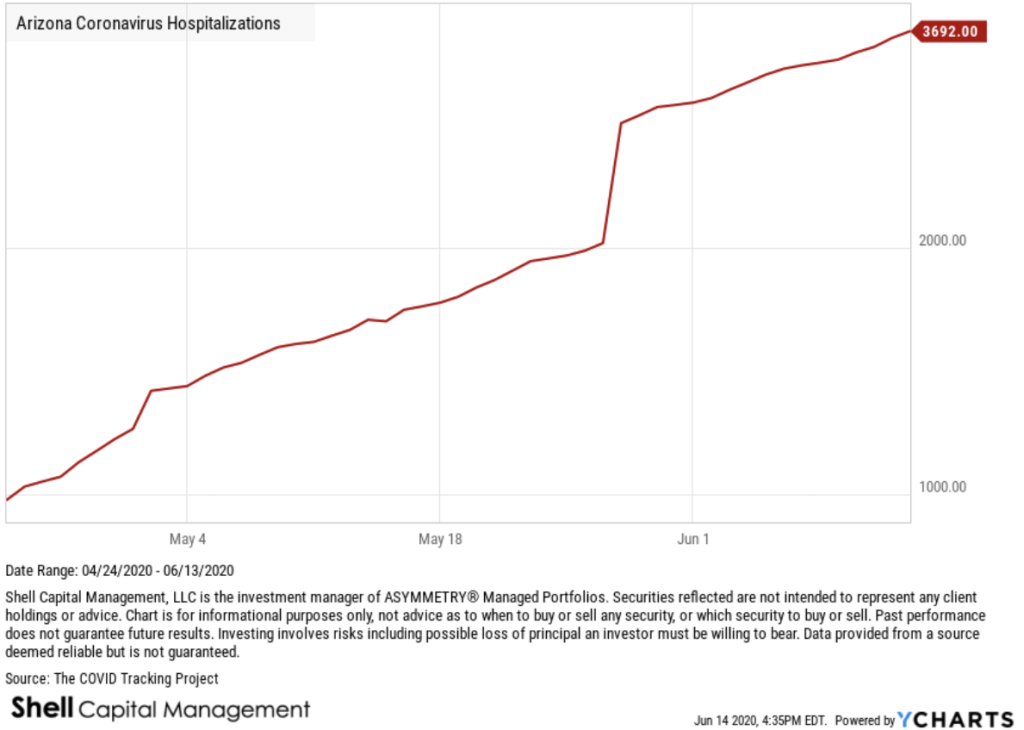

ARIZONA COVID 19 CASES AT NEW HIGH

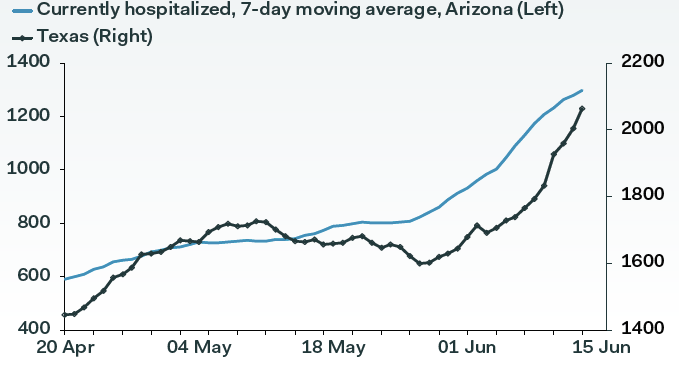

Arizona is at a high in new daily cases reported, but also in tests per day. The trouble in Arizona is the material new uptrend in hospitalizations.

The momentum in hospitalizations in Arizona is a real problem, and I’m using a logarithmic scale below, but it doesn’t help.

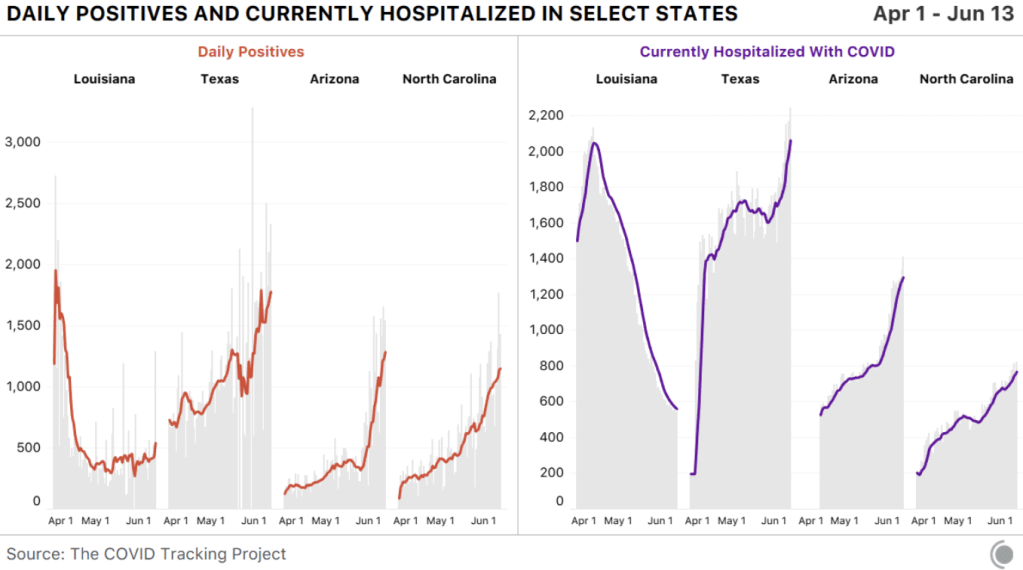

So, we are seeing new hospitalization highs in Texas, Arizona, and North Carolina. We’re showing Louisiana here as well for context, since it had an early COVID-19 outbreak.

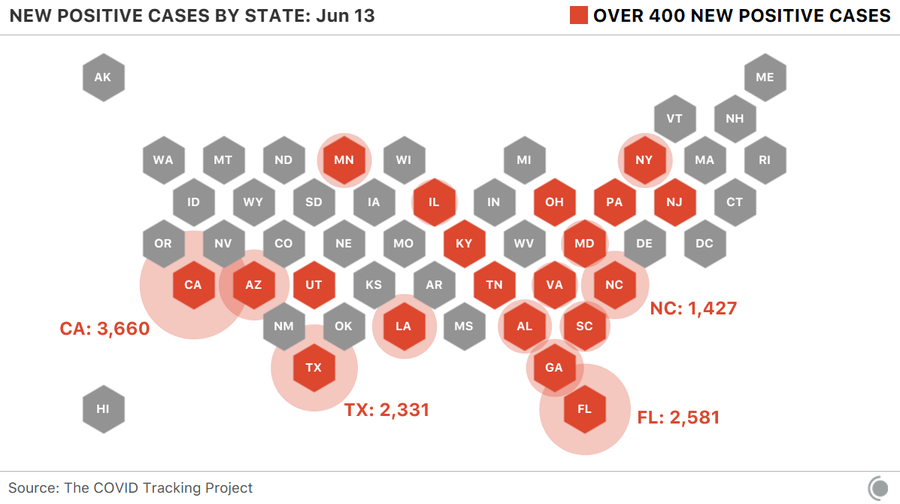

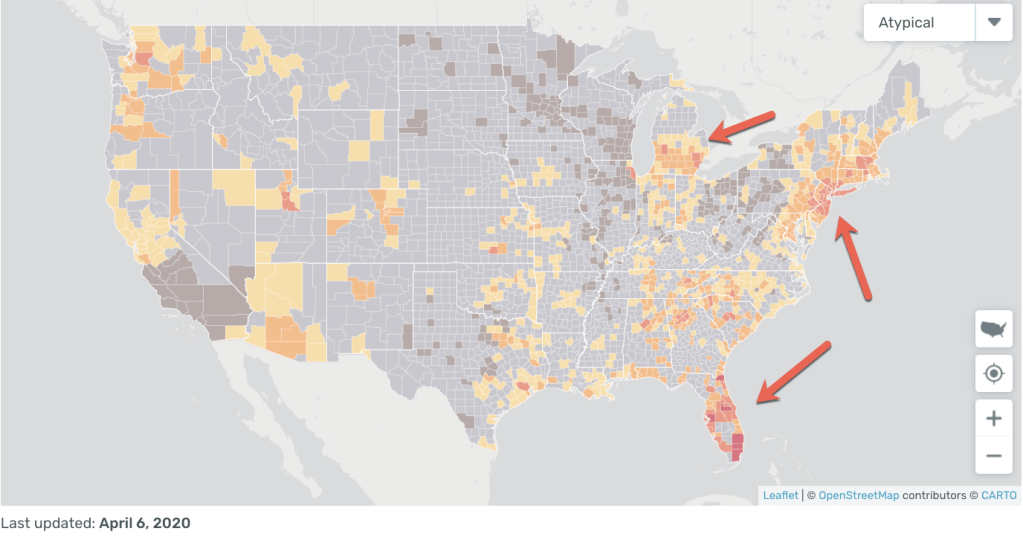

We saw 3 states report more than 2,000 cases yesterday: California, Florida, and Texas. A picture speaks a thousand words.

COVID HAS HIT THE NORTH MUCH HARDER THAN THE SOUTH

But the South is now seeing a surge in cases…

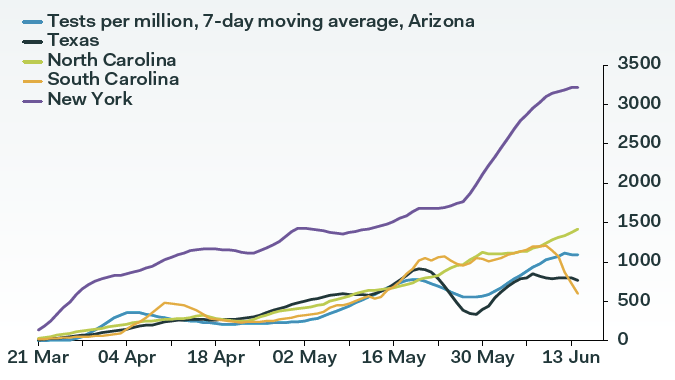

And it doesn’t seem to be an increase in testing.

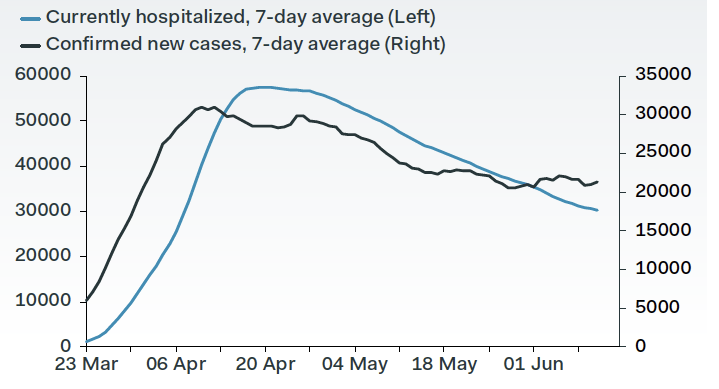

Can hospitalizations keep falling if cases are rising?

Because hospitalizations are rising rapidly in some Southern states.

I expect we’ll be hearing a lot about these new high breakouts in Arizona, Florida, Texas, and California. All of which, by the way, are the hottest and most humid states in the U.S., so much for the heat and humidity killing the virus.

What we have here is, a a notable uptrend across the South. I hope to see it fade, but based on what I’m seeing, it’s more likely to continue. Only time will tell.

If you are at risk, I recommend remaining cautious, wearing the dang mask, and treating this virus with respect.

Join 520 other subscribers

Speaking of the scientific method used for decision-making.

If you want to get as technical as possible, here’s some homework for the wannabe scientists and armchair mathematicians who really want to get into the maths of the matter. The virus has sparked a lot of important debates around the globe among though leaders. As researchers, we argue and debate our beliefs in hopes to gain new knowledge. One of the most heated public debates has been Taleb and Ioannidis.

The International Journal of Forecasting (IJF) is organizing a special section devoted to “Epidemics and forecasting with focus on COVID-19”. Based on their blog posts, John P. Ioannidis and Nassim N. Taleb will be given the opportunity to think of each other’s arguments about the COVID data and how to use it. Consequently, they will both be invited to write a full paper to better detail their views and why they think the opposite side’s views may not be adequate under the current circumstances. These opinion papers will then appear in the IJF, after scientific review by their peers. IJF should reserve the right to publish a closure based on this debate. This debate will not only allow us to better understand the points of view of the two great scientists but be also left as a guide for how to deal with future pandemics.

Nassim N. Taleb believes that all efforts and resources should be directed to halt its spread and reduce the number of infected and deaths without any concern about forecasting its future course as the uncertainty of doing so cannot be measured and the risks involved are highly asymmetric. See “On single point forecasts for fat tailed variable by Nassim Nicholas Taleb.”

John P. Ioannidis, on the other hand, claims that more reliable information is needed to make multiple billion-dollar decisions and that forecasting has failed us by being too pessimistic about the future growth of the pandemic and by exaggerating its negative effects. See “Forecasting for COVID-19 has failed”

Both of their observations are well worth a read.

In addition to the equity markets entering a higher risk level of a drawdown and volatility expansion, we now have a renewed risk of the scary COVID narrative driving more fear.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

“I still had much to learn, but I knew what to do. No more floundering, no more half-right methods. Tape reading was an important part of the game; so was beginning at the right time; so was sticking to your position. But my greatest discovery was that a man must study general conditions, to size them so as to be able to anticipate probabilities.” – Jesse Livermore, Reminiscences of a Stock Operator, by Edwin Lefèvre, first published in 1923.

The US stock market is now at risk of another decline

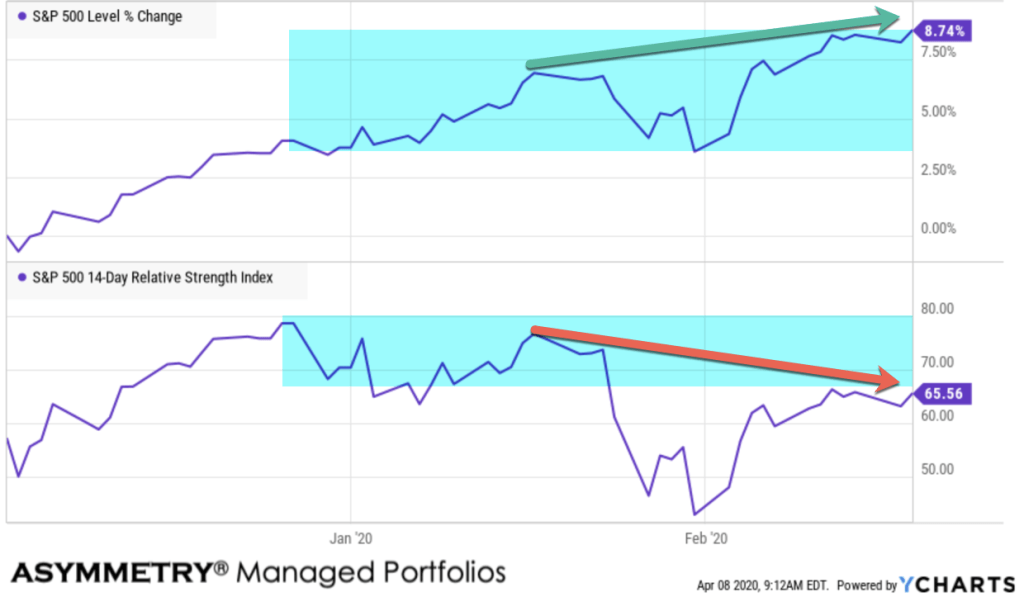

First, the relative strength of the S&P 500 has reached a level I consider overbought for the first time since the crash.

is a momentum oscillator that measures the speed and magnitude of directional price trends. The RSI oscillates between zero and 100, so it is range bound.I The RSI is defined as overbought when it reaches 70 or higher and oversold below 30.

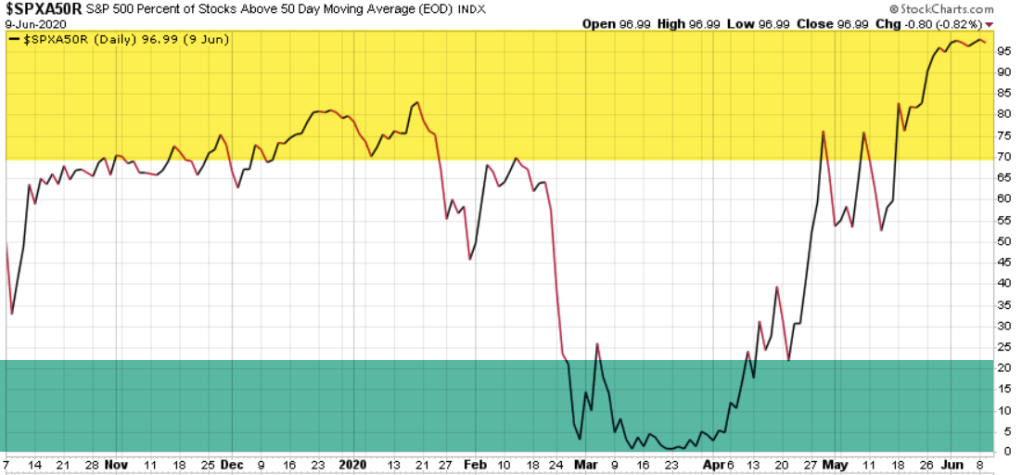

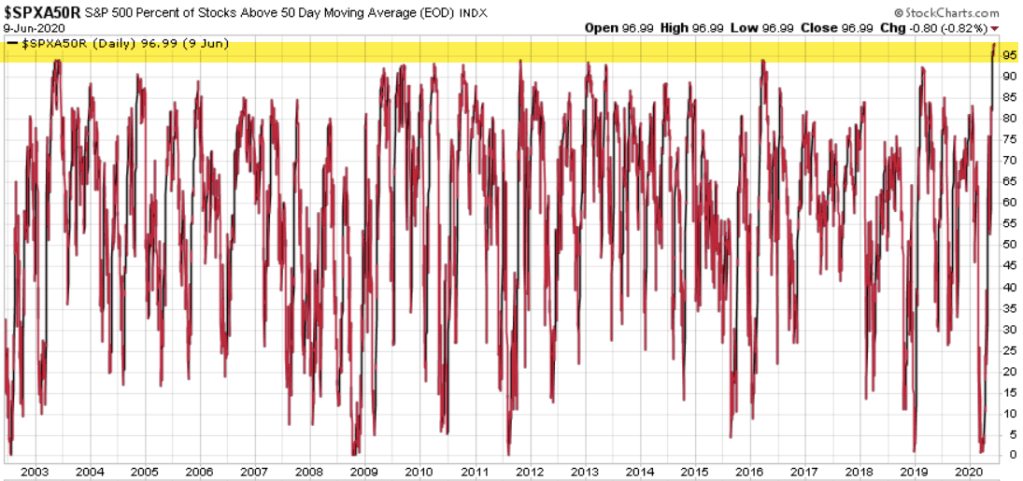

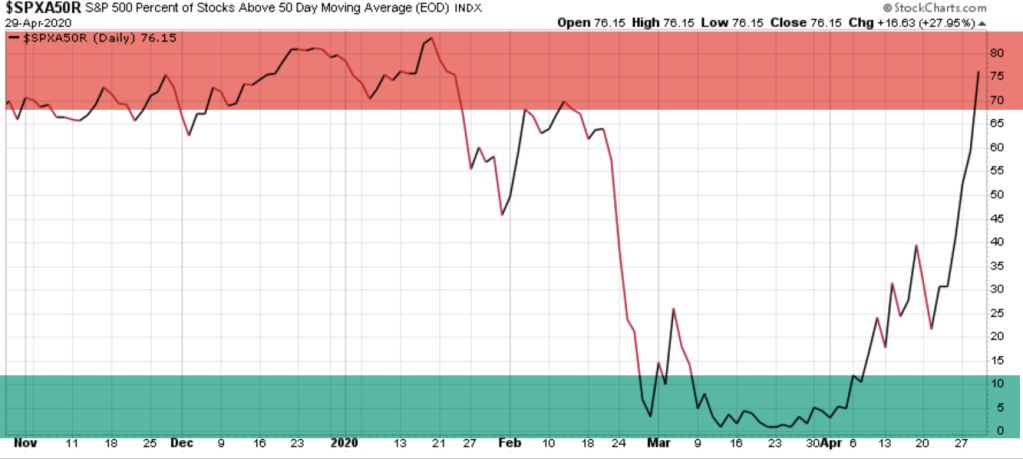

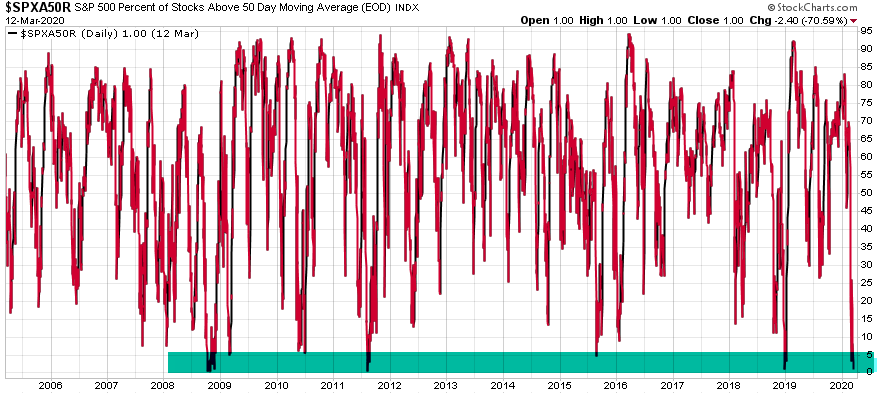

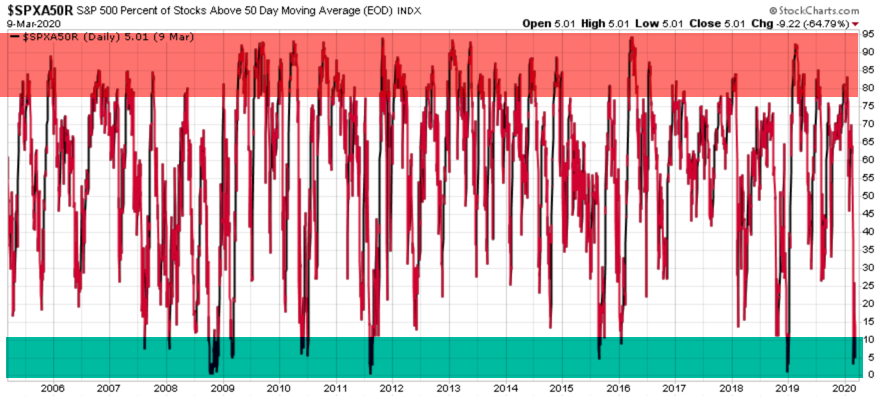

Another useful measure of market trend conditions is breath. The percent of S&P 500 stocks above their 50 day moving average shows us how many stocks are participating in the uptrend. Since June 1st, 97% of the stock are trending above their 50 day moving average, so they are in short term uptrends.

Strong breadth of participation is a good thing, until it reaches an extreme. A breath thrust as we saw begin the start in April was a good sign as the stock market was trending up, more and more stocks were entering uptrends. However, once all of the stocks are already in uptrends, we eventually have to wonder what is going to keep driving them higher.

Much of investment management is an understanding of what other market participants are likely to do next. When I see the percent of SPX stocks above their 50 day moving average at the highest level in twenty years, it simply tells us most of the stocks are in short term uptrends, but, the next direction for buying enthusiasm is going to be down.

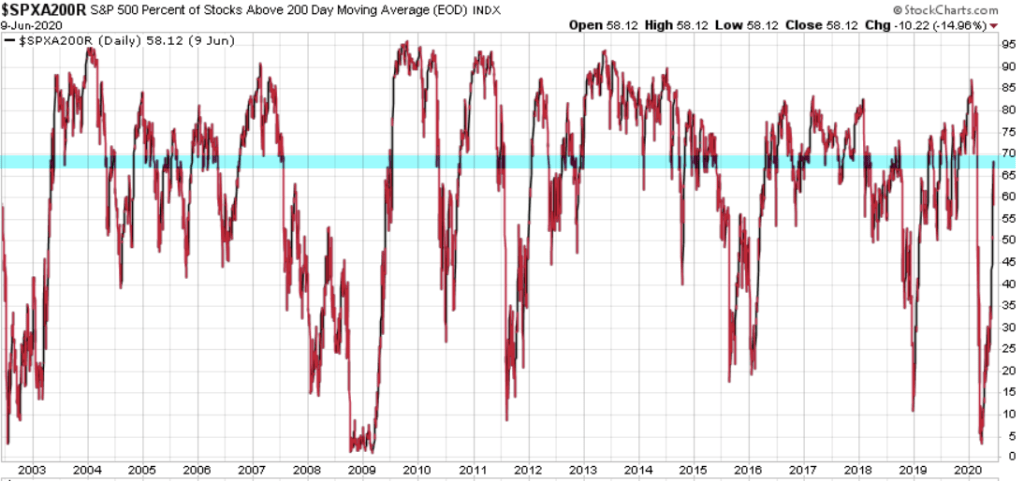

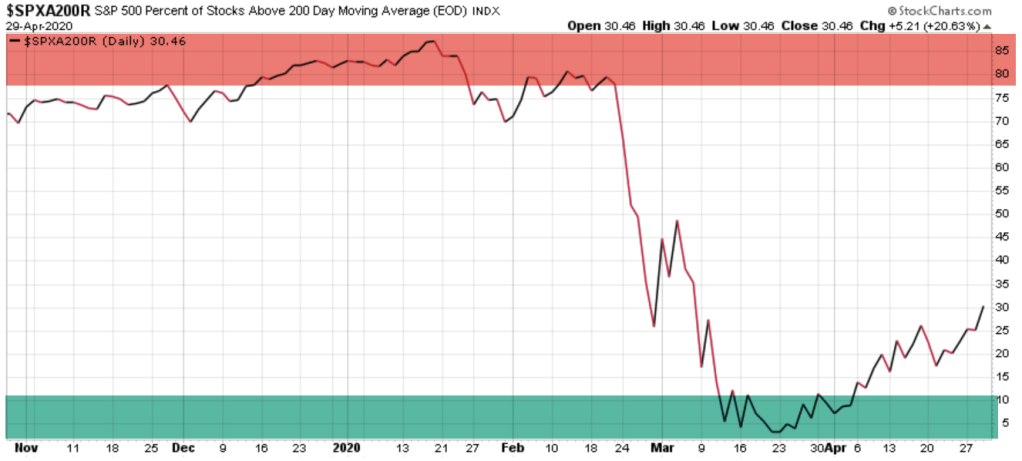

On a longer term time frame, which is the 200 day moving average, only about 60% of the S&P 500 stocks are in longer term uptrends, so there is plenty of room for continuation.

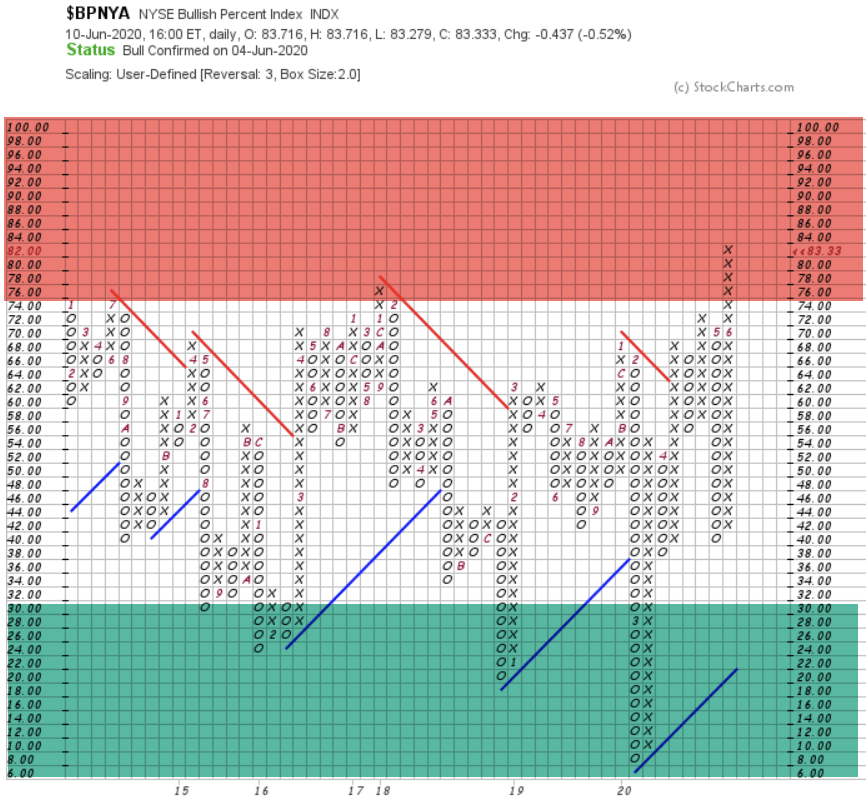

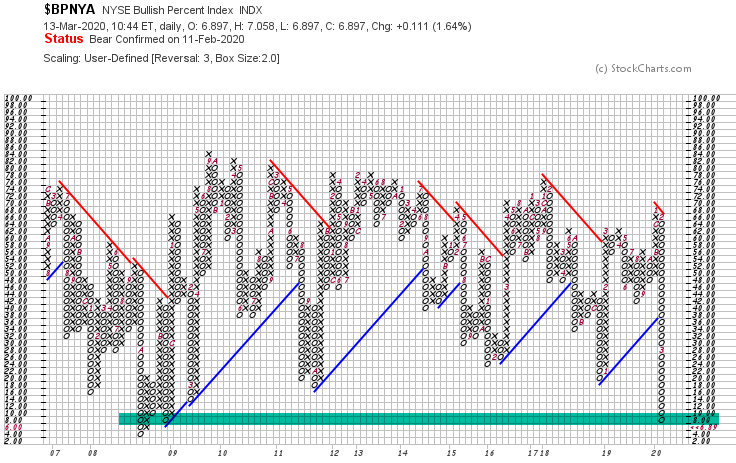

Next up is the good ole NYSE Bullish Percent.

The NYSE Bullish Percent was the first breadth indicator. The NYSE Bullish Percent was developed by Abe Cohen, the founder of Investors Intelligence in 1955. Abe Cohen was an early pioneer of point & figure charting , which he believed provided the ideal building blocks for a market barometer. By recording stock prices, P&F charts effectively map out the relationship between demand (buyers) and supply (sellers). The advantage of P&F charts is the supply/demand asymmetries are clear cut and easy to identify:

If demand outstrips supply, a P&F buy signal is generated

If supply outstrips demand a P&F sell signal is generated.

The Bullish Percent, then, is a breadth indicator that shows the percentage of stocks on Point & Figure Buy Signals. As with other oscillators, the Bullish Percent Index is range bound and fluctuates between 0% and 100%. In its most basic form, the Bullish Percent Index favors the bulls when above 50% and the bears when below 50%. Bullish Percent is considered overbought and a higher risk zone when above 70% and oversold and a lower risk level when below 30%.

At the current reading of 83, it’s clearly in the “high risk” zone.

So, I wouldn’t be surprised to see this uptrend at least stall here, temporarily.

If we’re going to see a second leg down, this is where I believe it will start.

The Federal Reserve is fully committed to keeping this trend going, so we’ll see…

Risk management is essential for all investments because all investments have a risk of loss.

As a tactical decision to reduce our exposure to loss in response to the elevated risk levels I’m seeing, I sold to take profits on our remaining stock positions on Tuesday and invested in US Treasuries.

“But my greatest discovery was that a man must study general conditions, to size them so as to be able to anticipate probabilities. ”

– Jesse Livermore, Reminiscences of a Stock Operator, by Edwin Lefèvre, first published in 1923.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

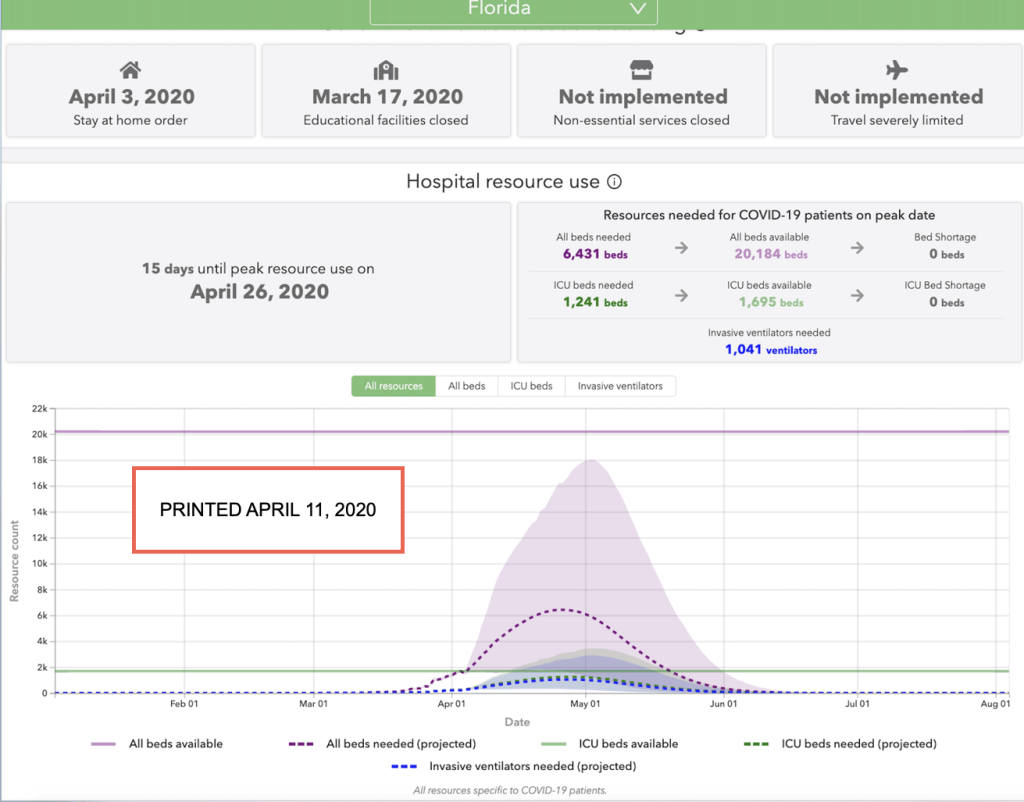

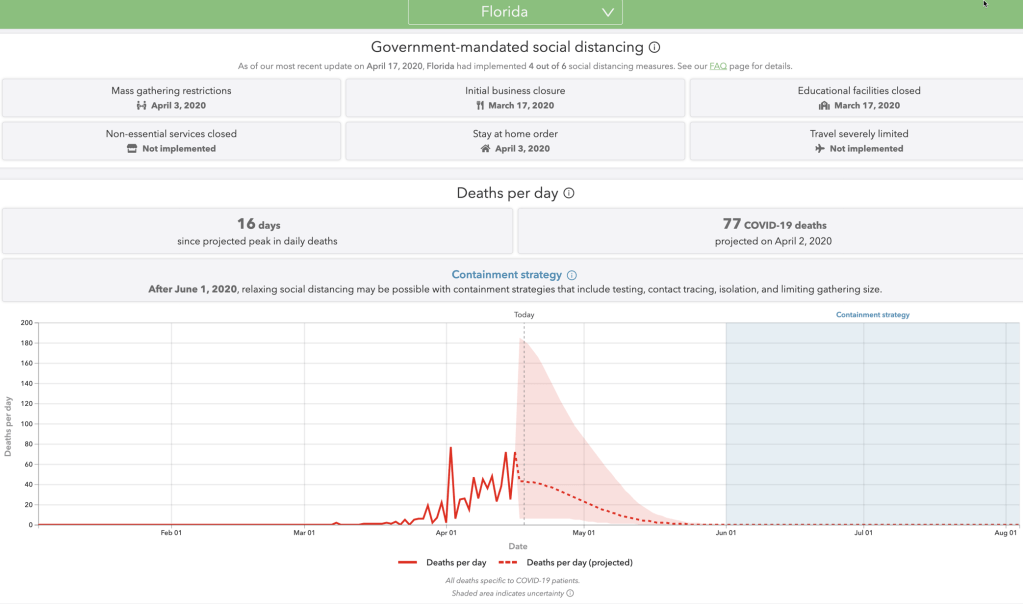

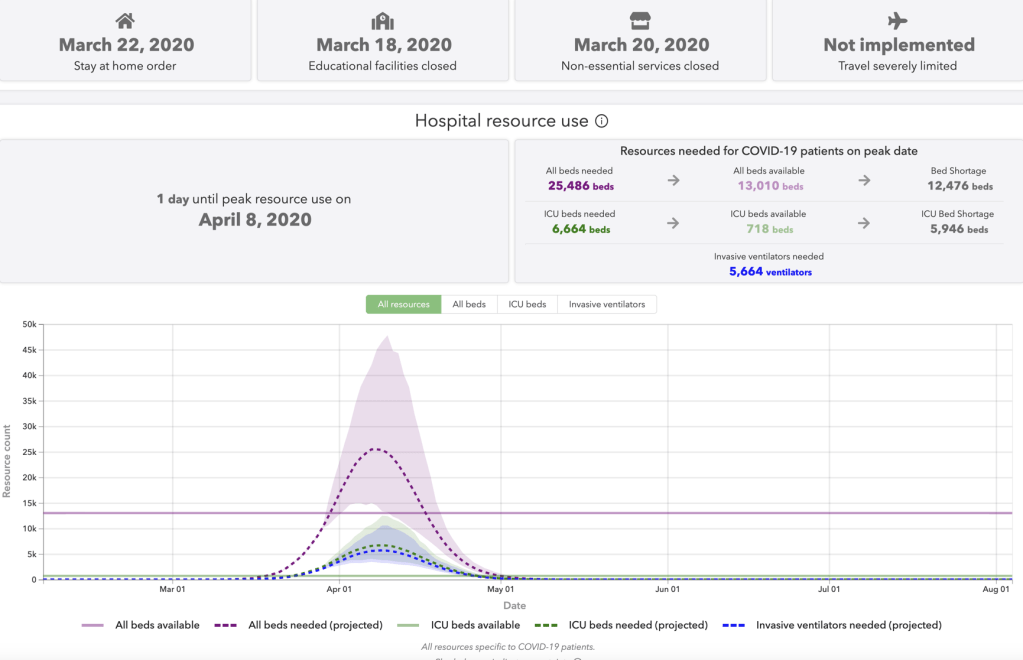

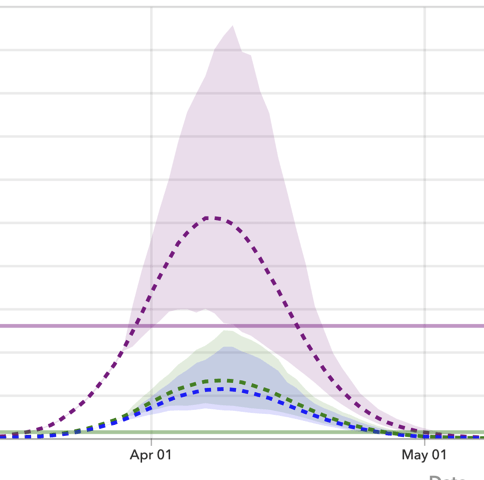

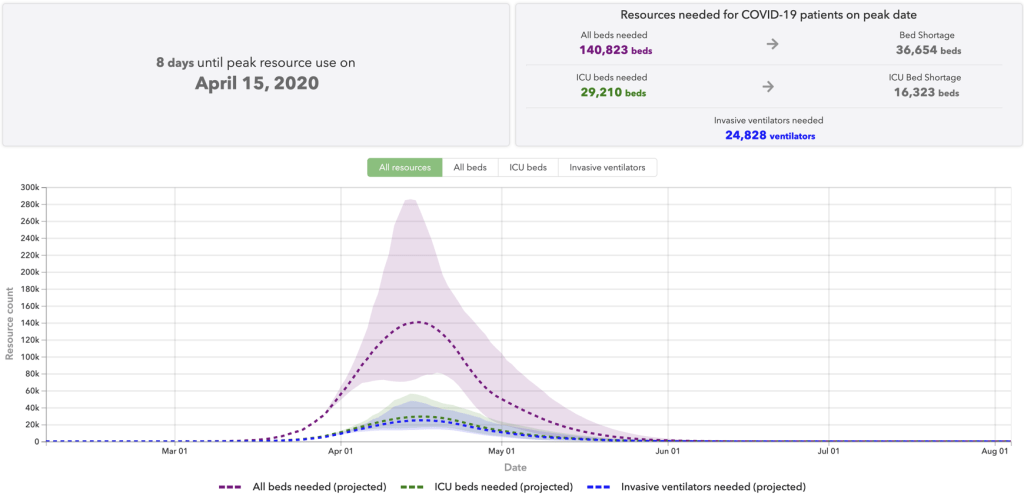

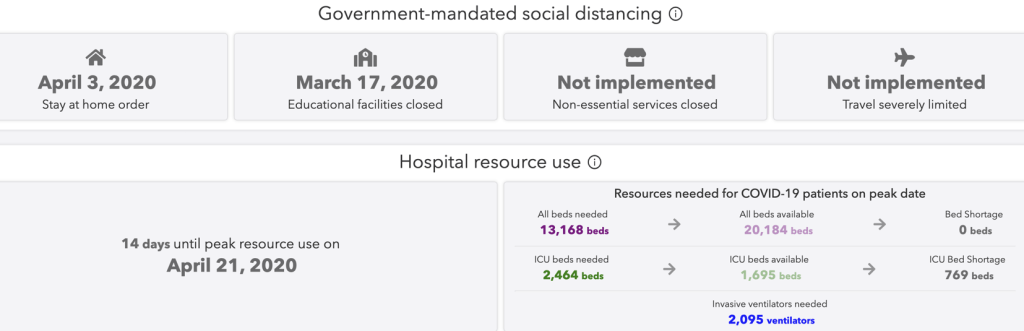

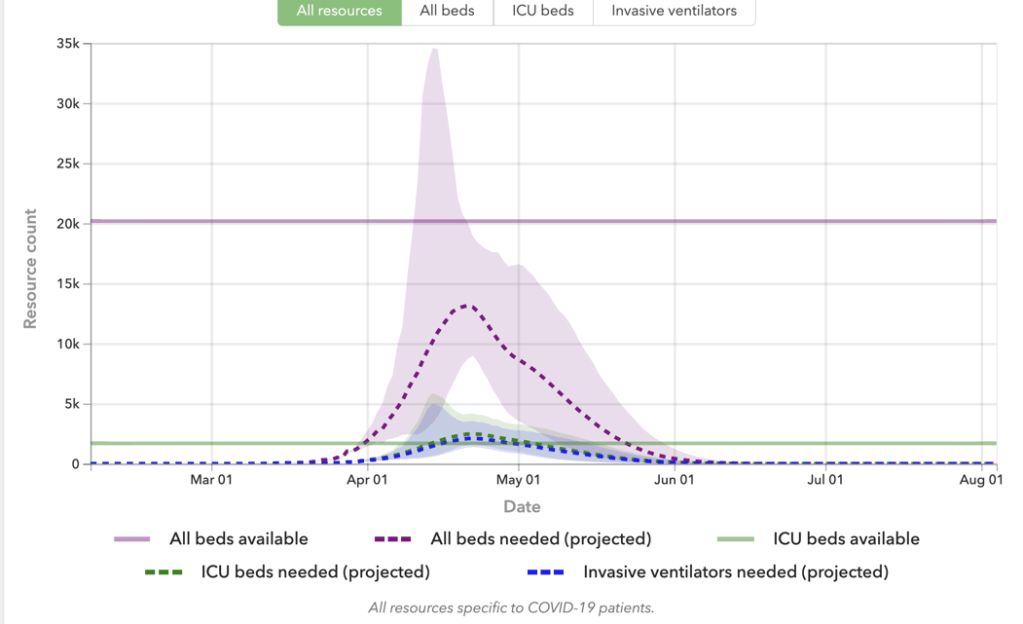

I’m sure there will be no shortage of criticism of the models attempting to predict things like hospital resource us such as the COVID-19 Projections from Institute for Health Metrics and Evaluation (IHME) that were widely used. The model had many assumptions, as any model would, and sometimes models get it wrong. Keep in mind, this model assumed social distancing, too, so it wasn’t a model misbehaving from our success in flattening the curve.

Below is an image I saved on April 11th, already showing Florida hospital resource use was improving.

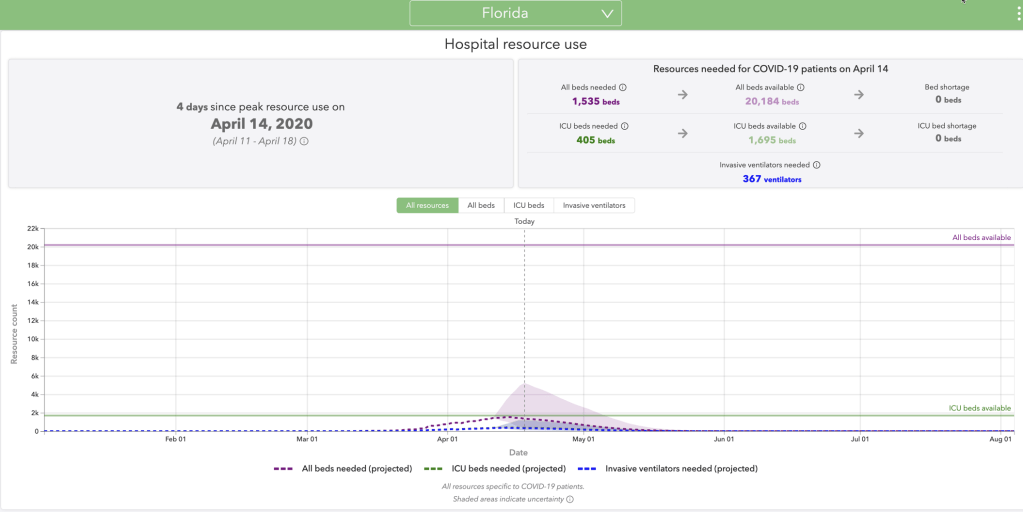

Here it is today. Their educated guesses overestimated resource use, though it wasn’t a big surprised to me, since I paid attention to the wide range of possibilities they illustrated.

How inaccurate were they?

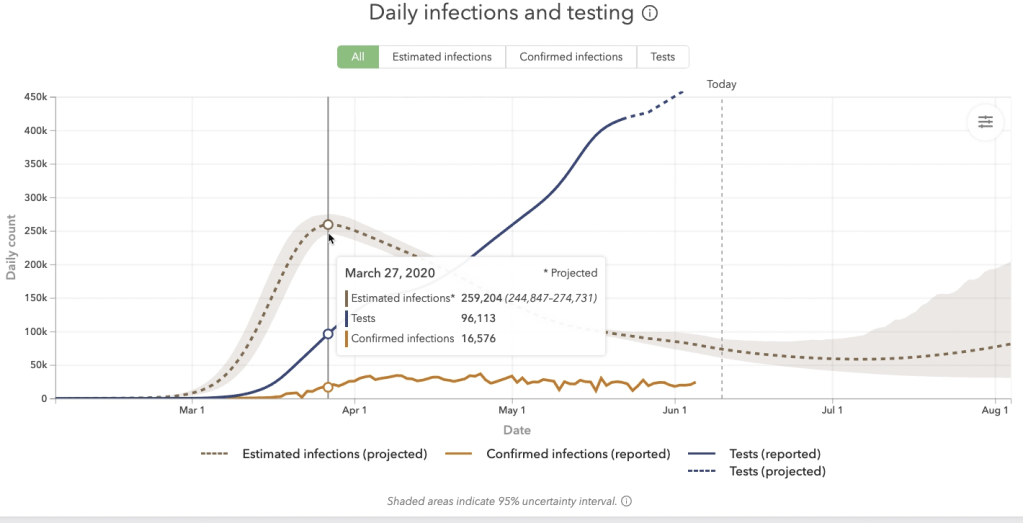

On March 27, 2020 the projected infections was 259, 204, but the confirmed infections was 16,576.

The brown line at the bottom is the confirmed infections, the higher line is their projections.

COVID – 19 isn’t over.

It’s still spreading, but not nearly as they predicted.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

Today’s jobs report is a mighty fine example of the market responding to positive rates and change and surprise.

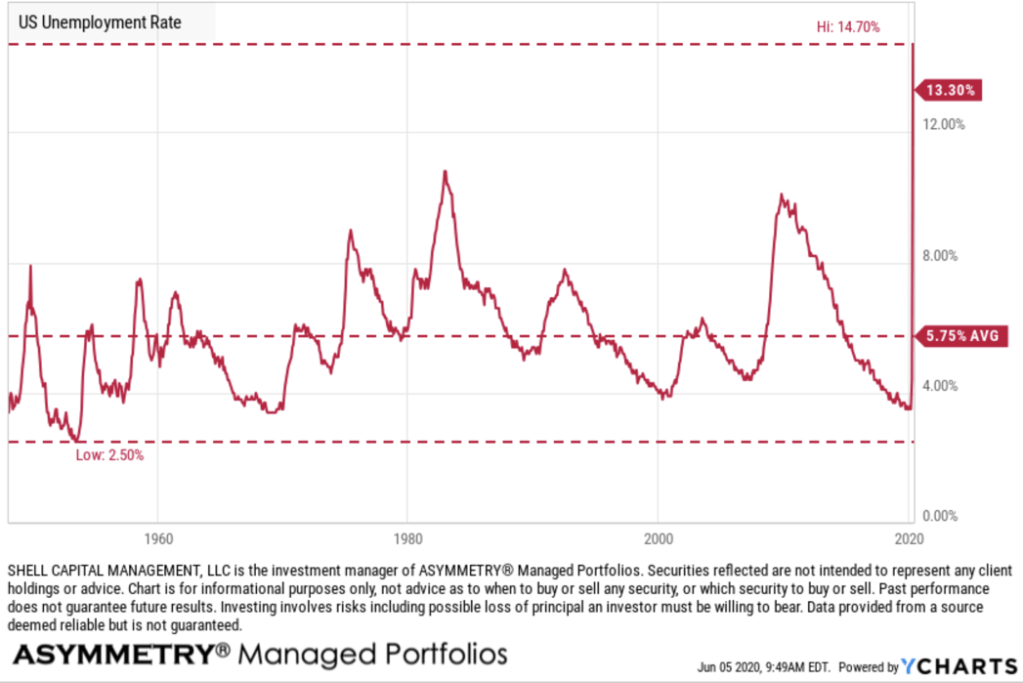

The US Unemployment Rate measures the percentage of total employees in the United States that are a part of the labor force, but are without a job.

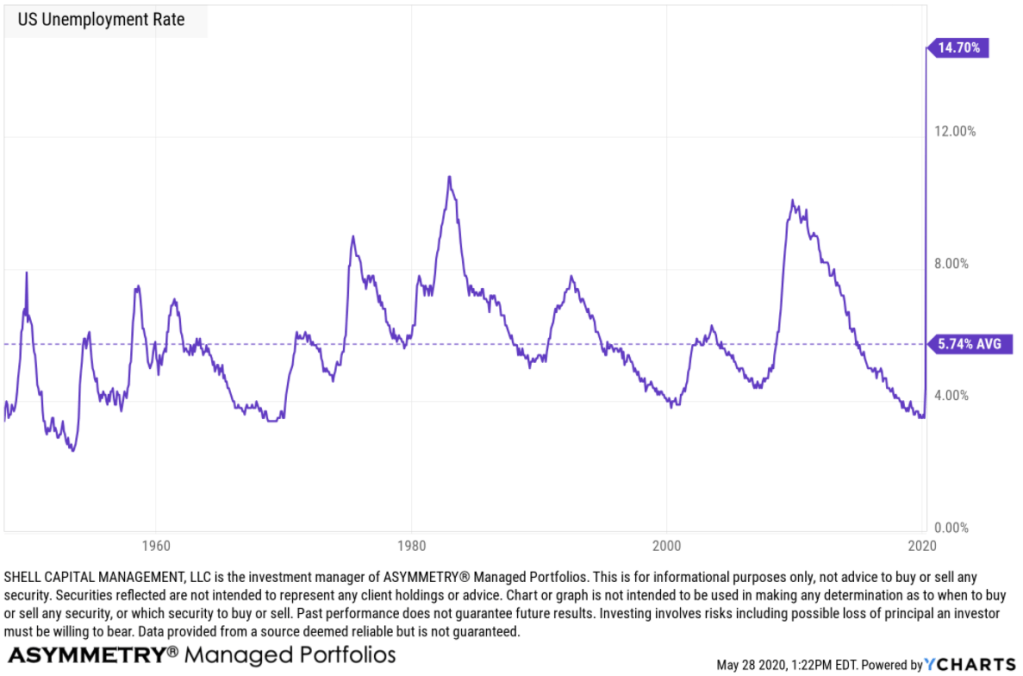

It is one of the most widely followed indicators of the health of the US labor market and the US economy as a whole. Historically, the US Unemployment Rate reached as high as 10.80% in 1982 and 9.9% in November of 2009. Both of these times were notable recessionary periods.

That is, until COVID – 19 came along.

We saw a 14.7% unemployment rate in April in the United States of America. A stunning increase from such a low level in February of 3.5%. The unemployment rate had been declining, for example, it was 5.3% five years ago.

After today’s jobs report, the US Unemployment Rate is at 13.3%, compared to 14.7% last month and 3.6% last year. It’s still nearly three times higher than the long term average of 5.75%, but a lot better than Wall Street had expected.

Wall Street expected a loss of 7.7 million jobs and a 19.8% unemployment rate today.

Bloomberg emailed sent out at 7AM this morning:

So, and Unemployment Rate at 13.3% is a huge positive surprise.

Some independent economist are already disputing the numbers.

The jobs report, as an aside, was again skewed by reporting irregularities. Not just that, the payroll pop seems to reflect businesses re-hiring so as to get the PPP loans switched to grants. So put away that champagne!

“And May’s unemployment number may be higher when it’s announced on June 5.

The stock market is said to be a discounting mechanism. The largest stock market investors who drive price trends don’t look back, they look forward.

It’s an auction market and operates on the proposition that investors and traders gaze into the future and discounts all known information about the present moment and expectations for what’s expected to happen next. So, when unexpected events happen, the market takes into account this new information very rapidly.

It certainly seems to be happening now.

Either the market is factoring in a quick recovery, or something else is driving it up.”

I think it’s safe to say the market has indeed gazed into the future and discounted a sharp recovery.

Yes, it certainly seems overly optimistic, but what is, is.

Notwithstanding a second wave of COVID-19 that hits even harder than the first, Wall Street seems to be pricing in the worst is behind for the U.S. economy.

What’s next?

It’s been a radical year. What else should we have expected out of 2020.

We’ve got to have some fun with it.

Did we skip the murder hornets? it feels like we skipped the murder hornets. 🧐 🐝

The US stock market will probably trend up today and reach an overbought level for the first time since January.

Remember: The market discounts the future, meaning it prices in future expectations. This discounting mechanism goes both ways.

The market is people. It’s large investors and small, but the largest investors drive the trends. It’s institutional investors managing money for others that are more advanced about gazing into the future.

Above all else, when it comes to forecasting or now casting a future trend, getting a grasp of what the majority of the market is thinking and doing is essential.

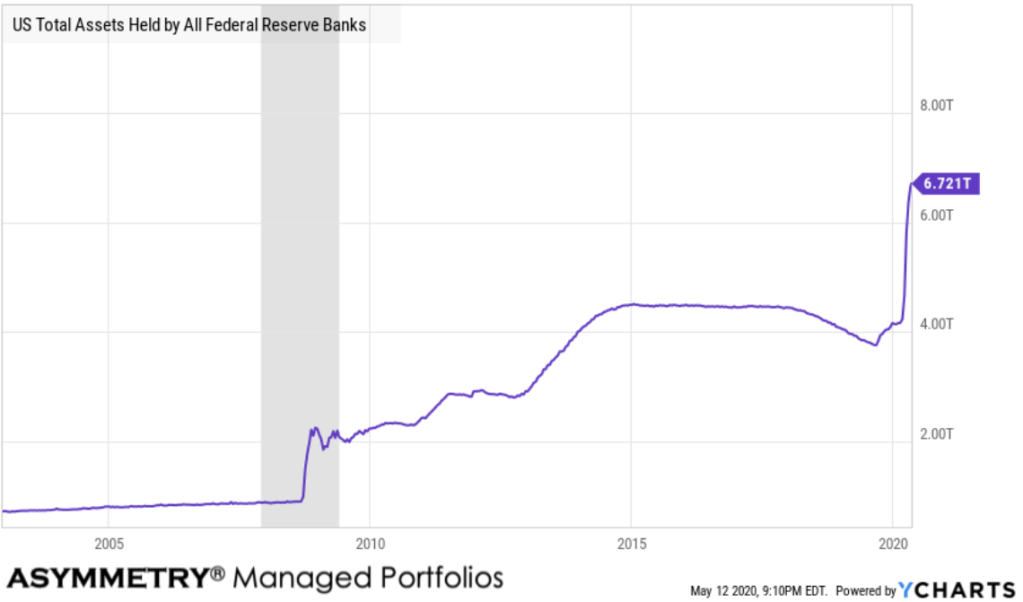

My guess is, the market has factored in the extremely aggressive response from the Federal Reserve and US Treasury to provide liquidity after it evaporated in March.

I know it’s very hard to go with the flow. Who would have believed this -37% decline would have recovered as much as it has so quickly?

No one.

But, it ain’t over till it’s over.

We have a new problem now.

The relative strength of stock indexes just tapped the overbought level, so the risk of a fall is now higher than it has been since this uptrend started.

Semper Gumby.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

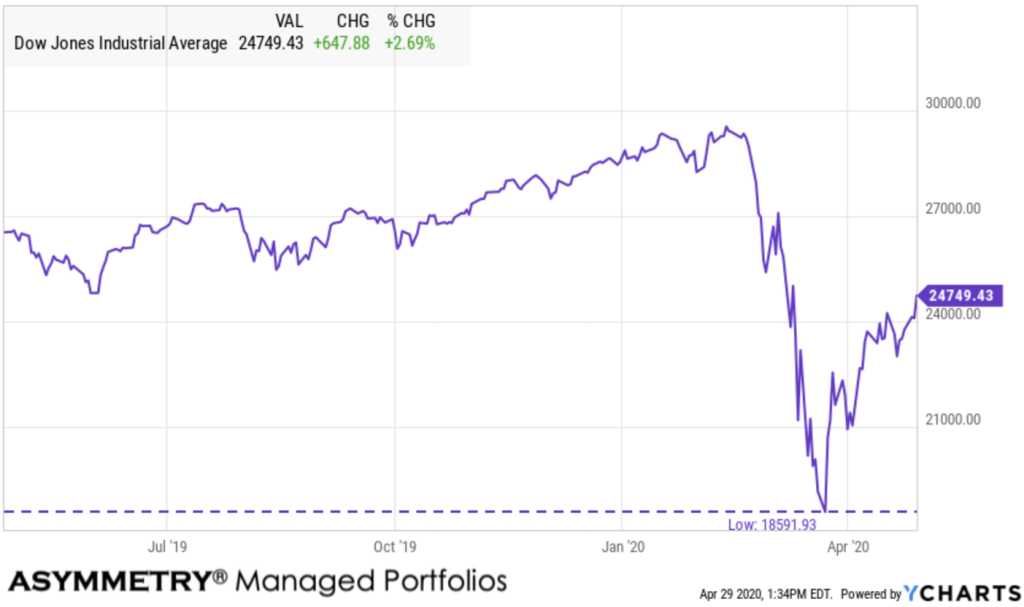

As the U.S. unemployment rate in April 2020 was 14.7%, the highest since the Great Depression, the U.S. stock market is trending up.

And May’s unemployment number may be higher when it’s announced on June 5.

The stock market is said to be a discounting mechanism. The largest stock market investors who drive price trends don’t look back, they look forward.

It’s an auction market and operates on the proposition that investors and traders gaze into the future and discounts all known information about the present moment and expectations for what’s expected to happen next. So, when unexpected events happen, the market takes into account this new information very rapidly.

It certainly seems to be happening now.

Either the market is factoring in a quick recovery, or something else is driving it up.

The Efficient Markets Hypothesis (EMH) is based on the theory that the stock market is a very efficient discounting system, so it factors in expectations of the future. The Efficient Markets Hypothesis suggests the stock market generally moves in the same direction as the economy.

Yeah, I know. If there ever was a time that sounds silly it’s now. Well, and every other market crash and bubble. I’ve seen my fair share of those in the past two decades.

One of the most interesting paradoxes in investment management is the market discounts everything is also the first premise of Technical Analysis.

The three premises on which the technical approach is based:

Market action discounts everything.

Prices move in trends.

History repeats itself.

That both the Efficient Markets Hypothesis and Technical Analysis is based on the belief the market discounts everything known and expected about the future is logically self-contradictory, because EMH doesn’t believe prices move in trends. EMH certainly doesn’t believe Technical Analysis, including trend identification systems for trend following and pattern recognition, is useful. Yet, trend systems and pattern recognition are some of the very strategies that I’ve seen to achieve asymmetric risk-reward.

I consider most trend identification systems to be pattern recognition. Pattern recognition is the systematic recognition of patterns in data. For example, the first action in trading breakouts is to identify current price trend patterns along with potential support and resistance levels in order to signal entry and exit points.

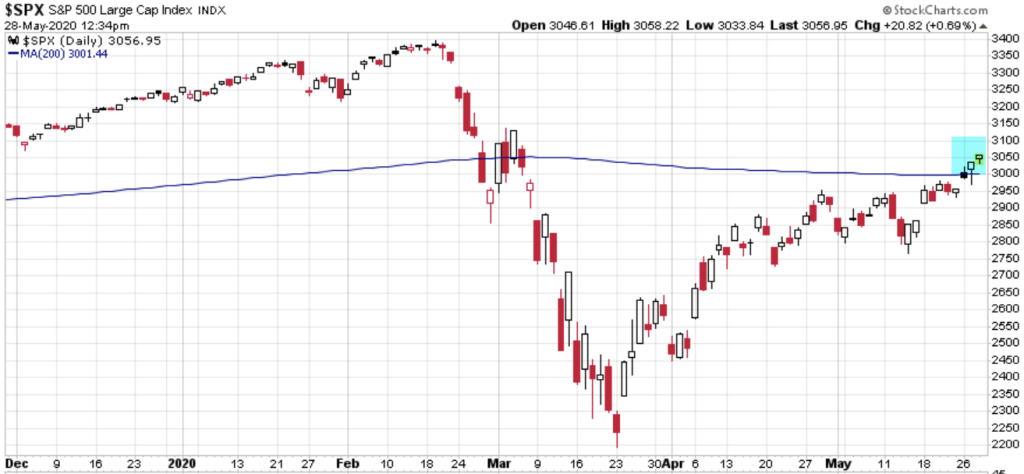

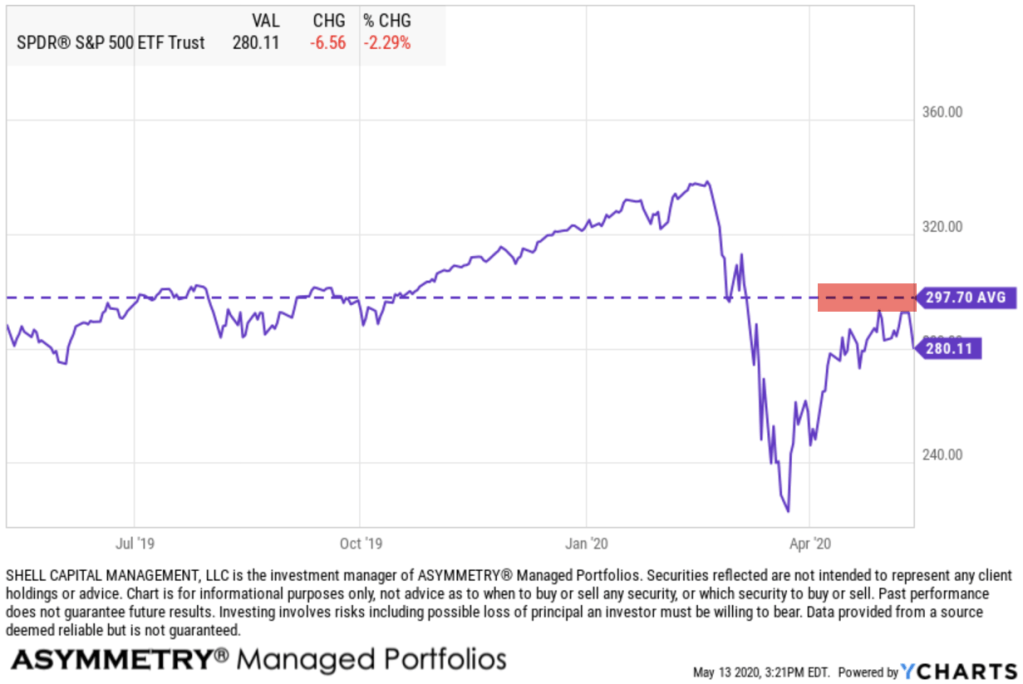

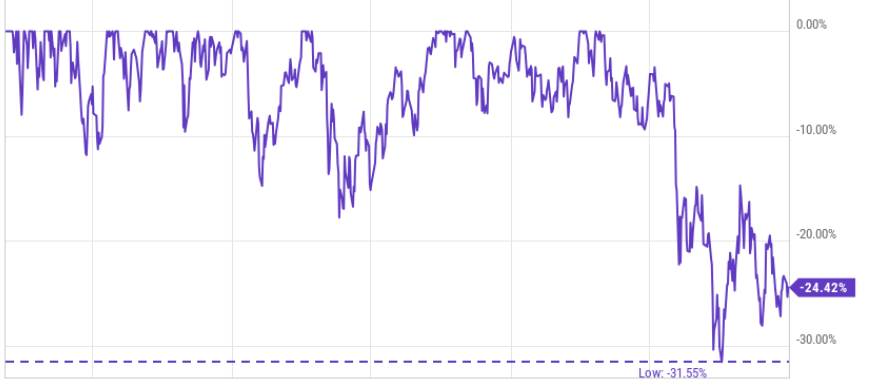

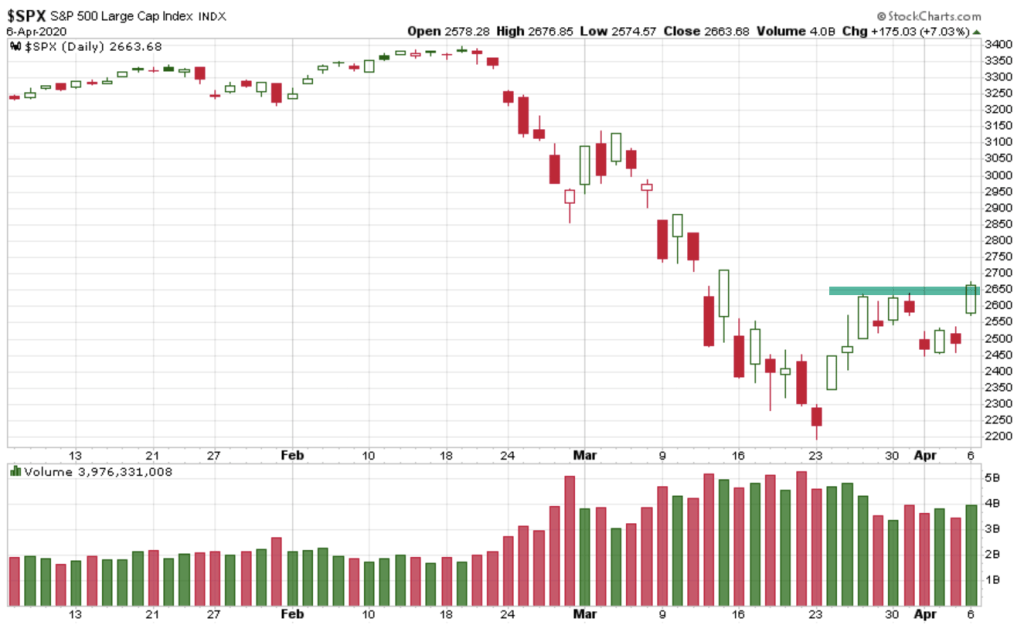

So, here we are. The S&P 500 is now trading above its 200 day moving average again after trending below it on February 27th.

It has been shocking to most that the stock index is now only down about -10% from its February high after a -36% waterfall decline over just 23 trading sessions.

It the fastest waterfall we’ve seen of this magnitude, so maybe we shouldn’t be surprised to see it swing back up to recover 2/3rds of the decline.

But no, it’s not a surprise. I tactically traded through the last two most radical bear markets since the Great Depression and they both included many swings up and down along the way.

The swings are the danger.