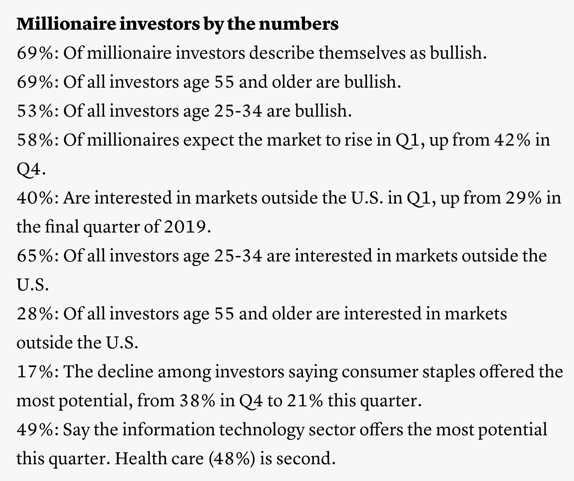

Investors, including millionaires and fund managers, are really bullish.

According to E-Trade Financial:

“In Q4 of last year, even as stocks gained, millionaires were cautious and possibly worried about a repeat of the plunge in the fourth quarter of 2018. Now 76% of these wealthy investors grade the U.S. economy highly, and there has been a 16% increase in investors who expect the market to rise by as much as 5% this quarter, according to an E-Trade Financial quarterly survey provided exclusively to CNBC.”

Then, Bank of America Merrill Lynch’s regular survey of global fund managers:

“The FOMO — fear of missing out — market did not come out of nowhere.

Last November, Bank of America Merrill Lynch’s regular survey of global fund managers found that global fund managers’ cash levels posted their largest decline since President Donald Trump’s 2016 election as investors rushed to take on risk.”

After reading that, I thought: With everyone so bullish, what could go wrong?

Place tongue in cheek image here.

Following up with my reaction over the weekend to Barron’s cover in Now, THIS is what a stock market top looks like!, I finally got around to reading the article “Ready or Not, Here Comes Dow 30,000.”

Barron’s said:

“Investors are responding to a set of conditions- low interest rates, muted inflation, and massive cash returns from U.S. companies – that make putting money into stocks the rational thing they can do.”

So, the reach for yield drives the stock market because:

“Some 80% of companies in the index cash-return yields higher than treasuries.”

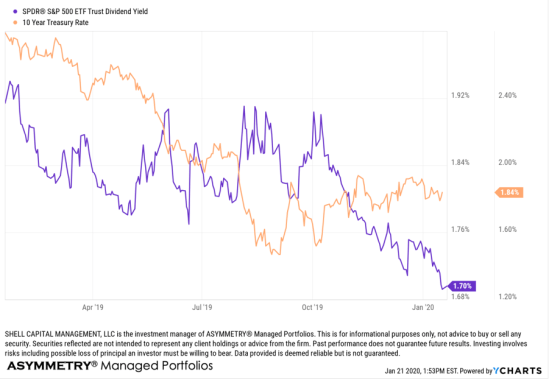

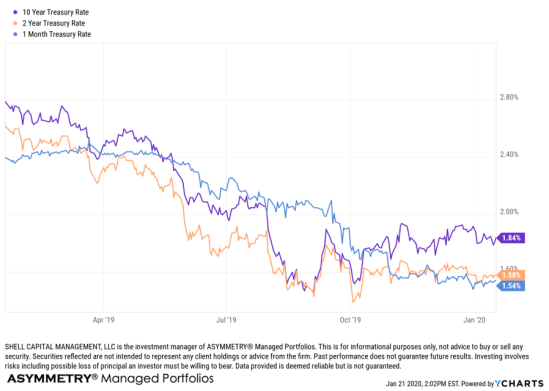

Below I compare the S&P 500 stock index ETF dividend yield to the 10 year Treasury rate. By this measure, the 10 year is 1.84%, which is 0.14% more than the SPY.

However, since the Treasury yield curve is relatively flat, the one-month Treasury is 1.54%, so there isn’t much of a spread or premium between the interest rate earned for just one month over 10 years.

Moving on to “What Can Go Wrong” they say rising bond yields are a risk to equities.

Of course, rising prices (inflation) is a driver of rising bond yields.

So, inflation may be the driver of a longer-term downtrend in stocks if these markets interact this way.

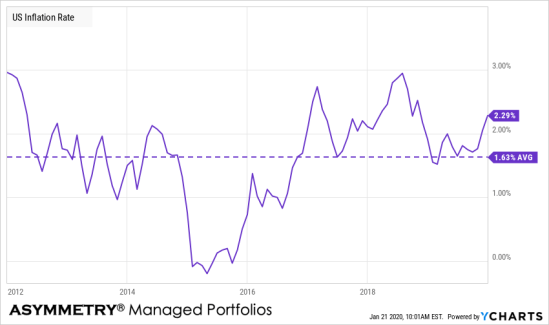

Since 2012, the Federal Reserve has targeted a 2% inflation rate for the US economy and may make changes to monetary policy if inflation is not within that range. So far, the FED has been successful ‘on average’, but there have been some uptrends in inflation.

Next, I added the high and low inflation rate since 2012 and highlight above 2% in yellow.

By and large, inflation cycles within a range. With the current inflation rate at 2.29%, which is a little higher than the Fed 2% target, I suppose global macro traders should pay attention to the trend and rate of change of inflation.

What could go wrong?

There are always many things that can cause a market to fall. We’ve got a U.S. Presidential election this year, an impeachment, now a new virus.

A quick glance at headlines shows:

BREAKING NEWS

CDC expected to announce first US case of deadly Wuhan coronavirus

So, there are always many things that could go wrong and be regarded as a catalyst for falling prices, but I focus on the direction of the price trend, momentum, volatility, and sentiment as my guide.

The direction of the price trend is always the final arbiter.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor in Florida, Tennessee, and Texas focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.