Investor sentiment oscillates between the fear of missing out and the fear of losing money.

Investor enthusiasm typically follows the recent trend.

After prices fall, enthusiasm wains as investors fear losing more money.

After prices trend up, investors fear missing out.

Some may literally oscillate between these feelings intraday, daily, or weekly, depending on how closely they watch.

I also believe investors underreact and overreact to new information, such as the “news.”

An overreaction is when price trends become overbought or oversold, driven by positive or negative investor sentiment. It’s why we see price trends crash down or rise into bubbles.

Overreactions can drive prices up or down too far, too fast.

An underreaction is when investors initially underreact to new information, so the price trend drifts up or down over time, rather than an immediate gap up or down. This underreaction drives price trends!

All of this is why my focus is on the direction of price trends, along with volatility, investor sentiment, and multiple time frame momentum.

I’ve also recently pointed out the news isn’t necessary to cause, or driver, of daily price action or price trends (directional drifts), even though most people probably believe it is.

We see an excellent example lately with Coronavirus.

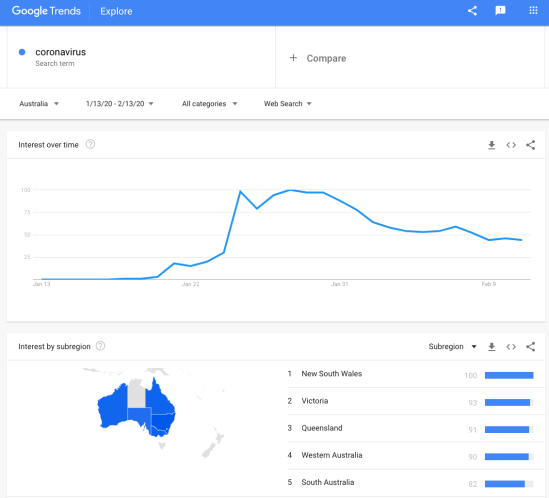

Below is the latest chart from Google Trends, showing an interest in Coronavirus over time. The numbers represent search interest relative to the highest point on the chart for the given region and time.

- A value of 100 is the peak popularity for the term.

- A value of 50 means that the term is half as popular.

- A score of 0 means there was not enough data for this term.

According to the data, it started January 19, 2019, and interest peaked January 28 at 100. Since then, interest in Coronavirus has trended down to a current level of 44, suggesting the term is less than half as popular as it was just three weeks ago.

It seems that news gets tiring, and people lose interest.

Or, maybe people initially overreact and spend a lot of time researching the topic, and then their enthusiasm drifts down from the peak. So perhaps they underreact later?

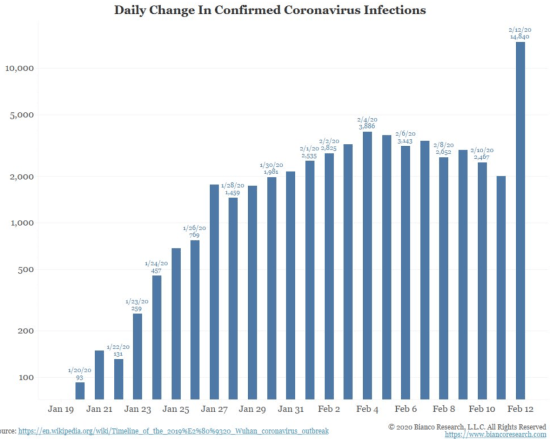

Or, maybe in the case of Coronavirus, the waning interest was helped by understated data?

Other global macro fund managers I know were relieved, but then a few of us noticed China had changed in their diagnostic criteria. We now see the spike in the above table.

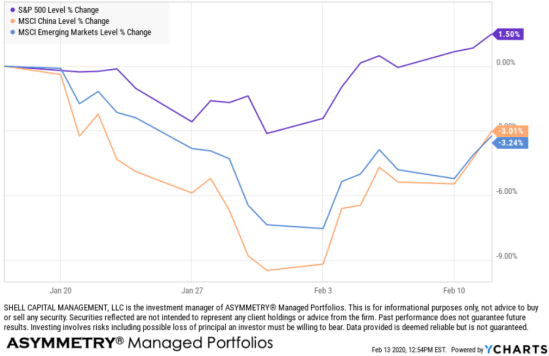

Yet, the U.S. stock market blows it off. Since the first talk of Coronavirus, the U.S. equity market declined about -3% but has gained 1.5% in total. The China MSCI Index, on the other hand, dropped -10% priced in U.S. Dollars and is down about -3%. The Emerging Markets Index, including China and other emerging countries, has trended a similar path.

It doesn’t seem to be a terrible reaction to me. Especially when we consider much of China is shut down as they attempt to stop the spread.

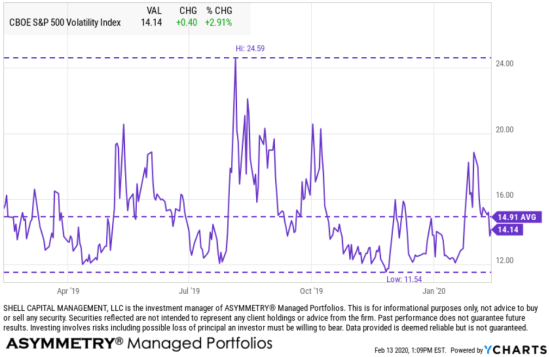

I believe the small decline we saw in the U.S. was just the market, doing what it does, as the U.S. stock index was extended on the upside, and volaltity was contracted. I was expecting to see some volatility expansion and a price drop based on the mathematics of momentum, velocity, and volatility. We saw it.

At this point, the trend is your friend until the end when it bends, but after that small correction, it seems we’ll soon find out if the upward momentum can continue. It comes at a time when there doesn’t seem to be an end in sight for the slowing and stopping the Coronavirus, so direct yourself accordingly. In the meantime, the headlines have turned much more cynical.

At the moment, the forward volatility expected by the options market as implied by the cost of options is just below its average over the past year. It’s far below the high of 24 when it spiked in August, and well above the low of 11.54 several weeks ago.

It will also be interesting to see if the interest in the term “Coronavirus” trends back up as the cases crow asymmetrically, or if it stays the same, or drifts down.

Either way, I believe there is a lot of asymmetric information going on here with China. Asymmetric information is a situation when one person or group has more or better information compared to another. It appears the Communist Party of China may be applying some strategic ambiguity in how they share their data. Another asymmetry is the illusion of asymmetric insight, a cognitive bias whereby people perceive their knowledge of others to surpass other people’s knowledge of them.

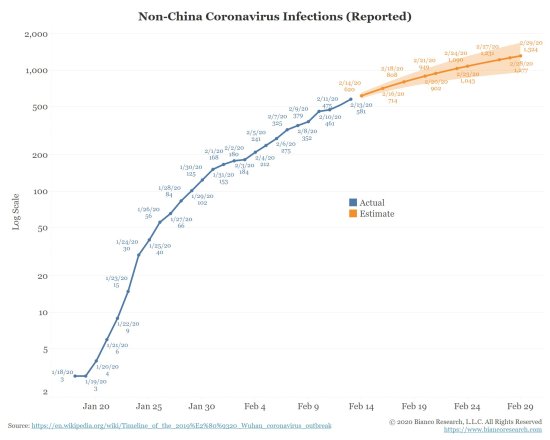

The below chart is the latest rest of world count with a trend line forecast through the end of the month.

I’m guessing we will find out soon if the market has underreacted to the news of rising confirmed cases and if investors then overreact on Monday after more data is released over the weekend.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor in Florida, Tennessee, and Texas focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.