People typically share their opinions based on their own personal observations of what they see and hear going on around them.

What we believe is always true, for us.

An advantage of a quant, or quantitative analyst, is the ability to study the data and trends to observe what is really doing on. Data science is an interdisciplinary field that uses scientific methods, processes, algorithms, and systems to extract knowledge and insights from structured and unstructured data. Then, we get to see how it compares to our own unique observations.

A friend of mine who happens to be a business broker helping people buy and sell businesses commented he thinks the next big recession will be caused by consumer debt. As we discussed it a few minutes, his opinion was based on his own observation that it seems the people around him are living “high on the hog” as we say it down South. In other words, people are taking on heavy debt and spending what they earn rather than saving and investing.

I can see why he may perceive it that way if your neighbors have a fleet of newly leased luxury cars in the driveway and seem to be taking vacations beyond what you believe they can afford. In some cases, if not many, it may be true their personal debt to income ratio may be maxed out. They may be buying cars, boats, and trips instead of saving and investing their excess earnings.

But, everything is relative.

Sometimes when things are good people want to take some extra chips and reward themselves. In fact, some of the greatest rainmakers I have known do this very thing. Many hard-charging producers of wealth also enjoy the rewards from their work.

Some of us get as much satisfaction from seeing our investment accounts grow from investing our excess earnings. Maybe we are more Introverts, so motivation comes from within, rather than impressing others. But that doesn’t mean we don’t enjoy the fruits of our labor. As everything is relative, we may be only eating a slice of an apple from a cart of dozens. But, for those who don’t have dozens of apples, it may seem more.

It’s an illusion of asymmetric insight, which is a cognitive bias whereby people perceive their knowledge of others to surpass other people’s knowledge of them.

Others are more extroverted and willing to spend all of their money in the present moment, rather than plan for the future. In this case, they may spend their earnings as fast as they get it, so there is no “excess” earnings to worry about. I suppose if you spend it all, you’ll have less stress about investing it, but you’ll be on the treadmill forever. While those who spend all of their earnings don’t have to concern themselves with the capital markets and investment management, they may not sleep well at night with all the uncertainty the lack of a secure future can bring. But, some of them may not think that far and not worry about it at all.

Consumer sentiment also has a role in how we all spend our money. When people are optimistic about the future, we are more willing to spend. There are infinite factors that drive sentiment, rational or not. For example, with a great credit score, you could get a car loan at 2% for years and such a low rate of cost to borrow may be more enticing to buy new cars. Even wealthy investors will take advantage of low rates since it doesn’t require withdrawing from investment funds and the borrowing cost is minimal. We can say the same for mortgage rates. The wealthiest of investors probably achieved it with some level of leverage. For example, business owners may use debt early on to grow their company and then when they sell it, it may either be debt-free or the net capital gain is much higher than it would have been without using the leverage to grow. Some use of debt or leverage can be good and it’s even essential in some areas such as real estate to maximum return on equity.

So, on the topic of debt, rates, savings, and such, here are some charts of the data.

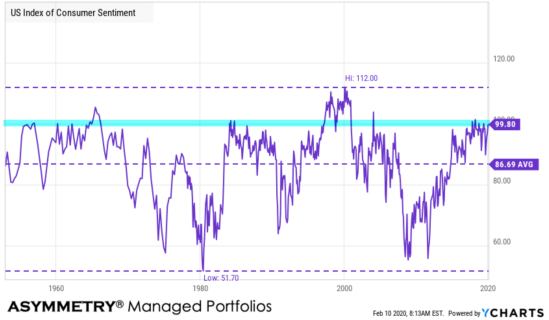

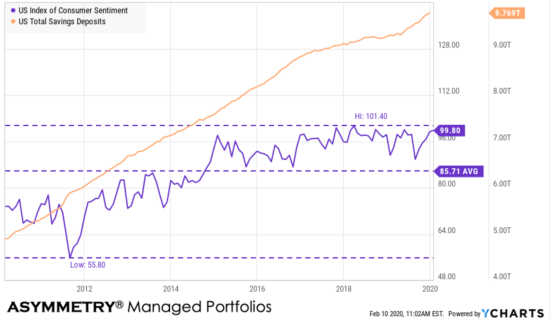

First, let’s look at consumer sentiment. The US Index of Consumer Sentiment from the University of Michigan tracks consumer sentiment in the US, based on surveys on random samples of US households. The index aids in measuring consumer sentiments in personal finances, business conditions, among other topics.

Take out the 1999 euphoric period and consumer sentiment by this measure is about as high as it gets.

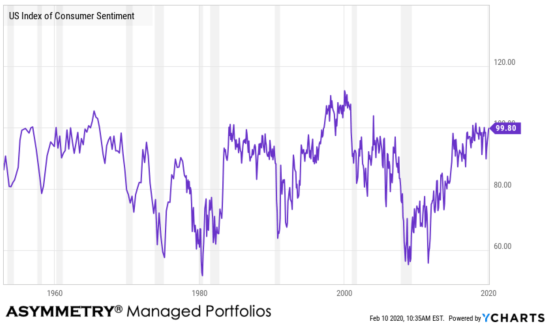

Historically, the index displays pessimism in consumers’ confidence during recessionary periods, and increased consumer confidence in expansionary periods. So, in the next chart, we highlight recessions in gray.

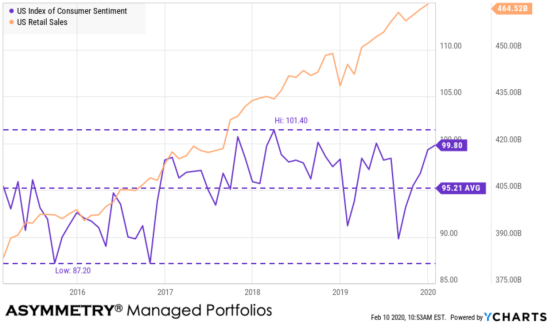

Does consumer spending match consumer sentiment?

As consumer sentiment is relatively high, spending as measured by US retail sales is at an all-time high. I note some divergence since around 2017 as sentiment has remained elevated but cycling up and down mostly above its average as retail sales trends up.

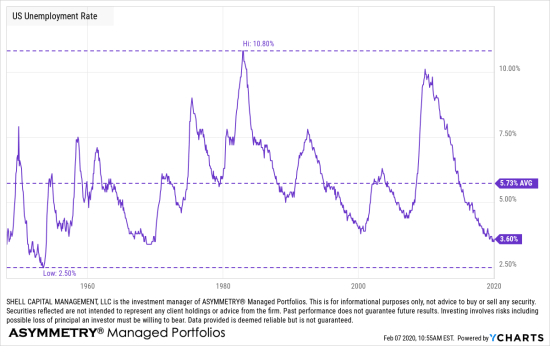

Employment and interest rates are a drive of these global macro trends. I observed in Employment, Coronavirus, it’s just the market, doing what it does… that unemployment is at historic lows. When most people who want to work are working that’s probably helping consumer sentiment. Gotta love such low unemployment! But, as a risk manager, we also use it as a reminder of situational awareness since nothing lasts forever.

What about the savings rate?

This is one of my favorite non-market global macro trend charts. Total savings is trending up.

Aside from employment, some other drivers of consumer sentiment are probably the trend and level of retail gas prices, auto loan rates, credit cards, home equity lines of credit, and mortgage rates. While we much prefer to see our fellow American’s use less debt, relatively low rates make borrowing more attractive. Again, some of the wealthiest families may even borrow at low rates and keep their capital invested. So, debt isn’t just borrowing because they can’t afford it otherwise.

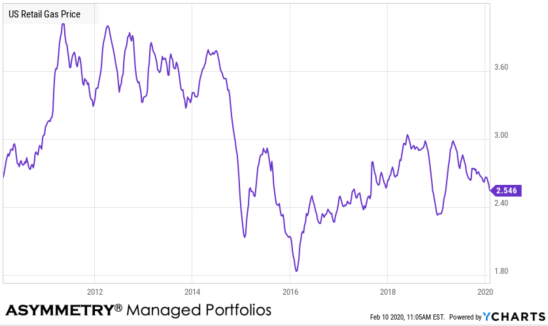

The US Retail Gas Price is the average price that retail consumers pay per gallon, for all grades and formulations. Retail gas prices are important to view in regards to how the energy industry is performing. Additionally, retail gas prices can give a good overview of how much discretionary income consumers might have to spend.

We’ve enjoyed some relatively low gas prices for the past five out of ten years. You may have noticed it at the pump or observed the lack of gas price headlines.

I first showed the more recent period to point out we tend to have recency bias, as we weight the most recent experience the most. It’s a “what have you done for me lately” kind of mindset.

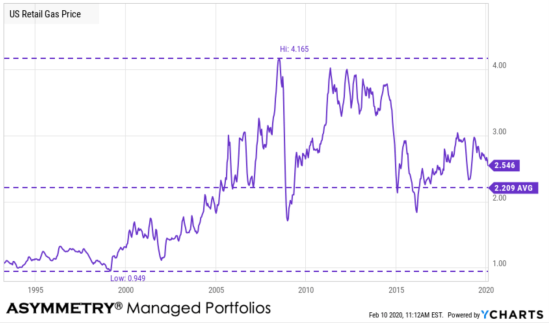

Next up is the longer-term trend in retail gas prices. I marked the high and low along with the average gas price going back to 1990.

While the retail gas price has been elevated above average, it’s far from the highest levels of the past.

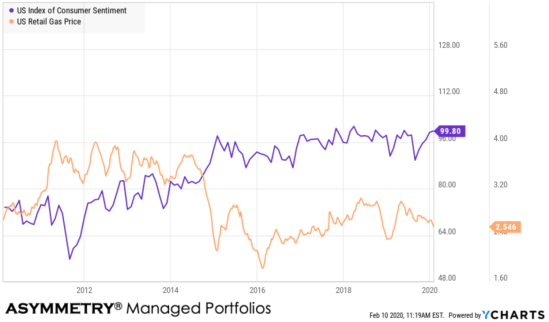

Is there really causation here between the price of gas and consumer sentiment?

There has been a negative correlation between the price of gas and consumer sentiment, so yes. I’ll say they are related the past decade in that a down-trending gas price helped drive up consumer sentiment.

I’m going to save some interest rates for another observation, so next up is my favorite chart.

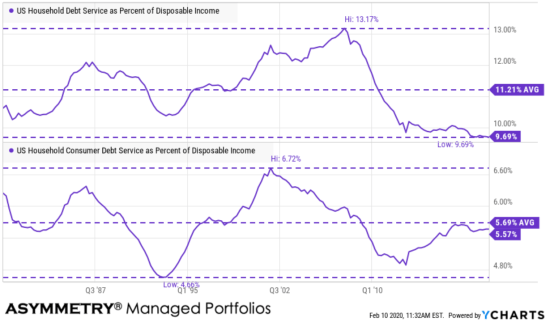

The Federal Reserve Board’s Household Debt Service and Financial Obligations Ratios convey how much of US household income is being spent on repaying debts and mortgages. It includes data specific to renters and homeowners. The homeowner data includes income spent on automobile lease payments, property taxes, and homeowner’s insurance.

US Household Debt Service as Percent of Disposable Income and US Household Consumer Debt Service as a Percent of Disposable Income are both at relatively low levels. Debt service is about as low as it’s been. Consumer debt service is below average.

So, in the big picture, my friend is wrong. The consumer debt situation is better than it may seem. By and large, this trend tells us our fellow American’s aren’t nearly as in debt as they were 10 to 15 years ago and overall, have less debt to disposable income than they’ve had in decades.

So, hopefully, in the next recession, American’s won’t have such a difficult time from being upside down drowning in their debt.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor in Florida, Tennessee, and Texas focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.