I love music, so it plays in the background in my office, instead of financial news. Sure, I have Bloomberg playing on a TV, but with the volume down. I rarely turn it up, unless someone I know is speaking of something I’m interested in. My day is filled with music, a wide range of music, so when I thought “delight” and typed out “permabear delight,” I heard three different songs.

A permabear is an investment manager or investor who is always negative about the future direction of the markets and the economy in general, no matter what. The parts of the word help us understand its meaning: “Perma,” which means permanent and “bear,” which is someone who believes the market will fall (a “bear” market.)

I’ve never been called a permabear in my 20+ year investment management career. But recently, a new follower asked if I am a permabear. It’s understandable because all he’d read was the past few months of my observations, and I have indeed been increasingly bearish. I got utterly bearish late January as my tactical trading signals, risk management, and drawdown control systems guided me to remove our stock market exposure to zero. The signals from my signals drive any “feeling” of bearishness I may have. Additional factors are extreme investor bullishness, implied volatility at extremes, and people wanting to get more aggressive. This is the part I often share here, hoping to help people observe how they feel the wrong feeling at the wrong time, and by doing so, they may eventually learn to feel the right feeling at the right time.

I tend to feel the right feeling at the right time. It’s something I’ve intentionally worked on, daily, for over two decades now, and with repetition comes increased skill and experience. For long term readers of my observations, I hope you’ve observed that. For our investment management clients, they’ve seen it in action in real-time. So, I become increasingly bearish as my quantitative systems signal risk levels are elevated. But, I also become bullish when the algorithms signal a price trend and volatility may have moved too far, too fast. When price trends move too far, too fast, I consider it an overreaction to information. I’ve discussed it a few times lately, especially regarding the coronavirus outbreak. I believe we witnessed an initial underreaction to how investors may eventually react, and then what appears to be an overreaction. At least in the short term.

So, now, I’m far from a permabear myself. I have investment manager friends who are permabears, and their performance reflects it. I also have friends who are permabears and have been unable to invest their money outside an FDIC insured bank account. That has been a big risk to them over the decades, but they may not know it, but to each their own. Banks need CD savers so they can lend the money out to borrowers at higher rates. It all seems to work out as everyone gets what they want.

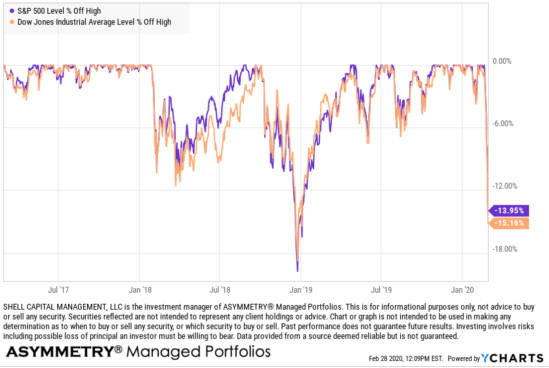

At this point, the widely followed stock indexes have declined sharply with speed. The S&P 500 is down -14% from its recent all-time high, and the Dow is down over -15%. The chart below is the % off high to put these drawdowns into context. It still isn’t as deep as late 2018, but it is now very close and happened much faster.

While this may be a buying opportunity for those of us who had cash to increase exposure at these lower prices, it’s always possible it could trend lower. What seems more likely at this point is prices get low enough to attract buying enthusiasm, and if it’s enough, it reverses this waterfall decline, at least temporarily. After that, this may well be the bigging of the next big bear market. It’s a process, not an event, although this decline does look much more like an event than usual since it was so far, so fast.

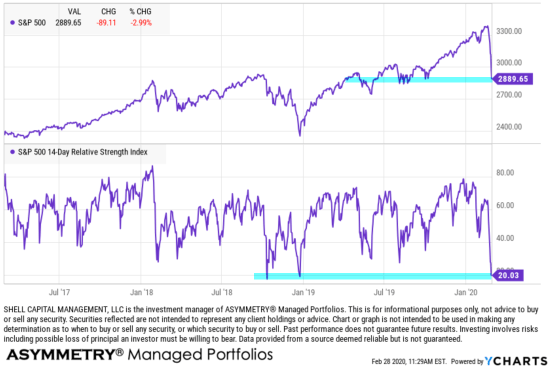

I’ve now become short term bullish on the stock market. My systems which have been quantified and scientifically tested for robustness are now signaling prices are now at a level we consider oversold and a countertrend back up, at least retracing some of the recent waterfall declines that appear to be an overreaction. For example, below is the current chart of the S&P 500, which is down another -3% today. Below the price trend is a simple 14-day measure of relative strength, a momentum indicator measuring the magnitude of recent price changes to evaluate overbought or oversold conditions. Today it has reached 20, which is the point I consider oversold. In fact, it’s now as low as it was during the late 2018 -19% waterfall decline.

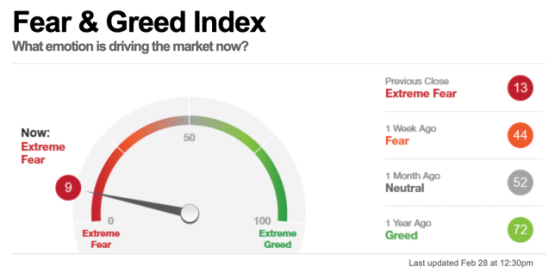

Of course, after prices fall, so does investor enthusiasm to invest in stocks. It is no surprise to see the Fear & Greed Index made up of seven different sentiment measures reach the “Extreme Fear” level.

Warren Buffett said when it comes to investing in stocks, it is smart to be “Fearful when others are greedy and greedy when others are fearful.” Although I do a lot more tactical strategies that he does, at these extremes we have something in common.

Warren Buffett said when it comes to investing in stocks, it is smart to be “Fearful when others are greedy and greedy when others are fearful.” Although I do a lot more tactical strategies that he does, at these extremes we have something in common.

We don’t invest our grocery money in stocks, but this may eventually prove to be a positive asymmetric risk-reward opportunity when risk is defined with a predetermined exit (stop loss) or positions structured in a way that define or limit downside risk.

A permabear, on the other hand, are maybe singing “Don’t go chasing waterfalls” by TLC, I’m hearing a diversified genre of some Rapper’s Delight by The Sugar Hill Gang, Afternoon Delight by Starland Vocal Band, and Dixieland Delight by Alabama if you want to follow along.

I’m about to take the longest trip to Florida to Tennessee of my life. I hope you have a great weekend. As always, next week will be fascinating. Investors will either fear losing more money or fear missing out if they tapped out at low prices. I have bypassed both in our managed portfolios as we avoided the waterfall decline, so we’re in a position of strength to increase exposure to risk and reward. If you sell higher, you can buy lower. At this point, we can tolerate some downside from any new exposure from here as we know its mathematically becoming less likely, and we are now positioned to not have any fear of missing out if the trend reverses up.

I hope this helps!

Have questions? Need help? Contact us here.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor in Florida, Tennessee, and Texas. Shell Capital is focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. I observe the charts and graphs to visually see what is going on with price trends and volatility, it is not intended to be used in making any determination as to when to buy or sell any security, or which security to buy or sell. Instead, these are observations of the data as a visual representation of what is going on with the trend and its volatility for situational awareness. I do not necessarily make any buy or sell decisions based on it. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.