The Cboe Volatility Index VIX is back to its average of 15 over the past year, which implies volatility of 15% for the S%P 500 for the next 30 days based on options prices.

Indexes like the VIX may have no predictive ability as to market direction at this level, but options don’t lie. The options market is a two-sided market and two-sided markets provide some insight. Options can have predictive power at extremes, but in most cases, the speed is to the downside.

The Cboe VVIXSM Index is the volatility of VIX. The VVIX Index is an indicator of the expected volatility of the 30-day forward price of the VIX. This volatility drives nearby VIX option prices. Like the VIX, it’s also at its average level of the past year.

My next observation is the Cboe 3-Month Volatility Index (VIX3M). Once again, at its average.

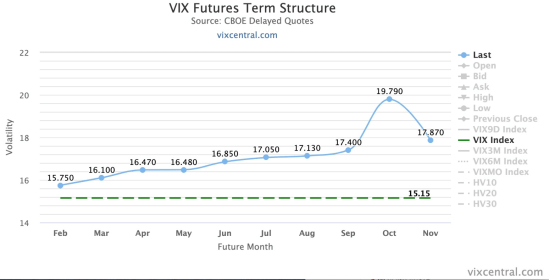

Next is the VIX Futures Term Structure. VIX futures reflect the market’s estimate of the value of the VIX Index on various expiration dates in the future. Monthly and weekly expirations are available and trade nearly 24 hours a day, five days a week. VIX futures provide market participants with a variety of opportunities to implement their view using volatility trading strategies, including risk management, alpha generation and portfolio diversification. All of these volatility trading strategies are reflected in the futures prices and the term structure shows it.

The upward-sloping VIX futures term structure is called contango and the current contango between the front month and next is 2.5%, which is small.

The upward-sloping VIX futures term structure as we see now suggests that short-term volatility is relatively low compared to its long-term level and investors/traders expect an increase in volatility in the future.

So, as the stock market is trying to regain its prior highs, volatile is trying to settle down for now. We’ll see if it can hold.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor in Florida, Tennessee, and Texas focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.