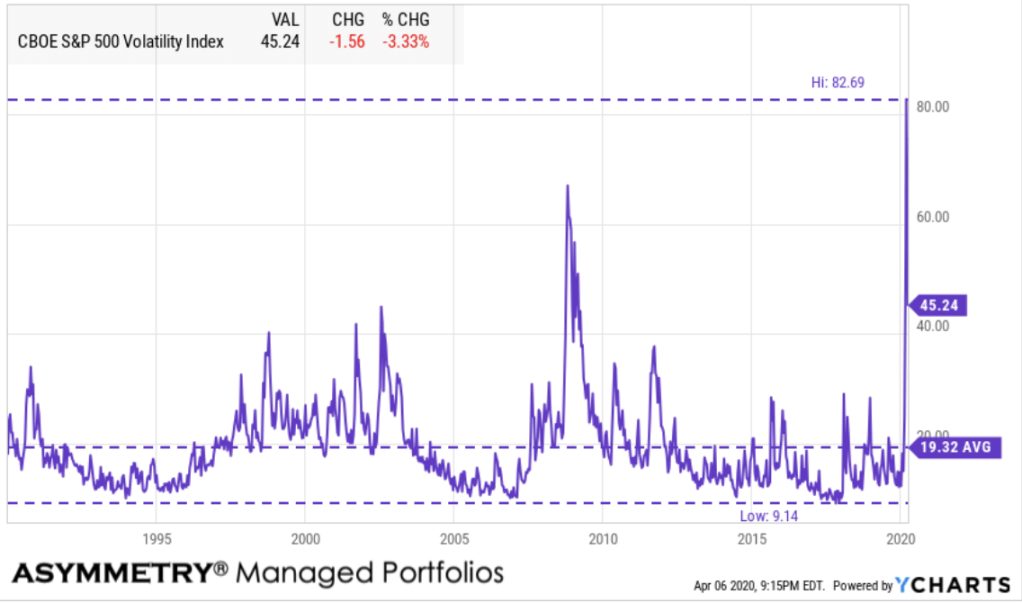

Prior to the volatility expansion that started a month ago, my mantra was:

Periods of low volatility are followed by volatility expansions.

The other side to it is:

Periods of high volatility are followed by volatility contractions.

Yes, indeed, after the CBOE S&P 500 Volatility Index (VIX) shattered it’s former all-time high when implied volatility spiked to 83, it is now settling down retracing about half of what it gained. For now, it’s a volatility contraction.

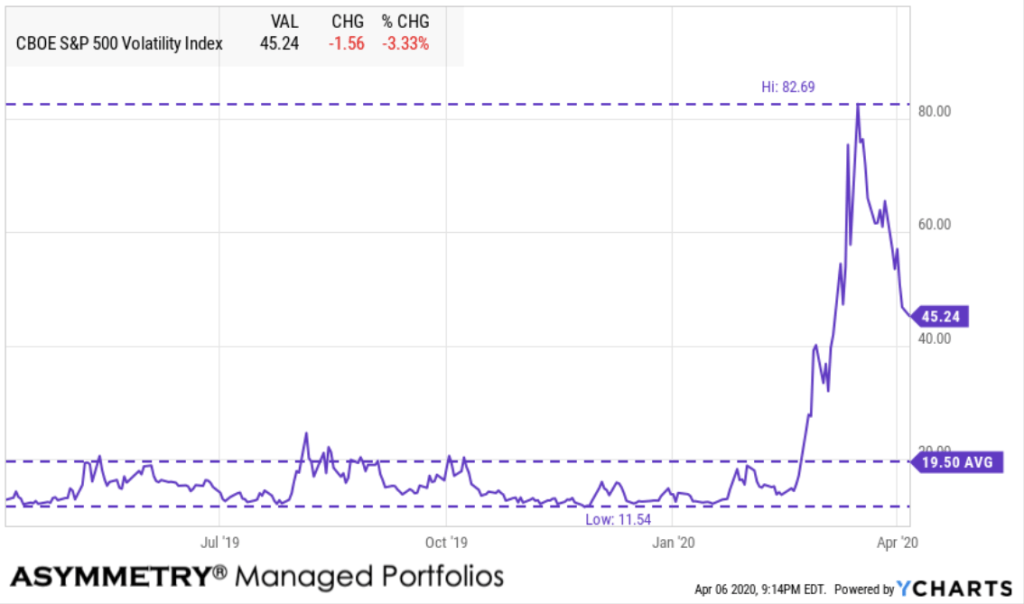

For a closer look, here is the trend zoomed in to the one year chart.

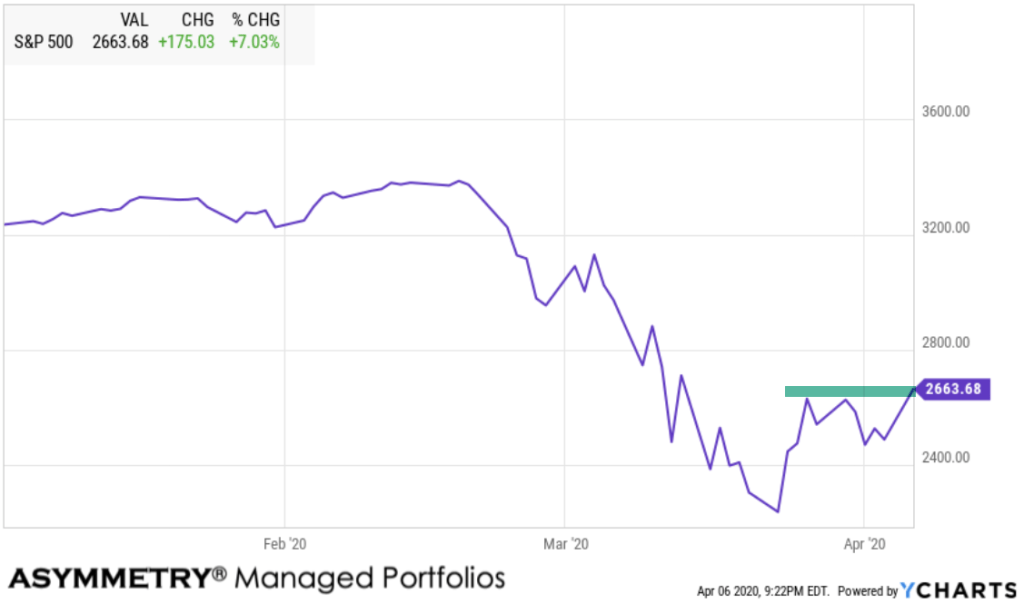

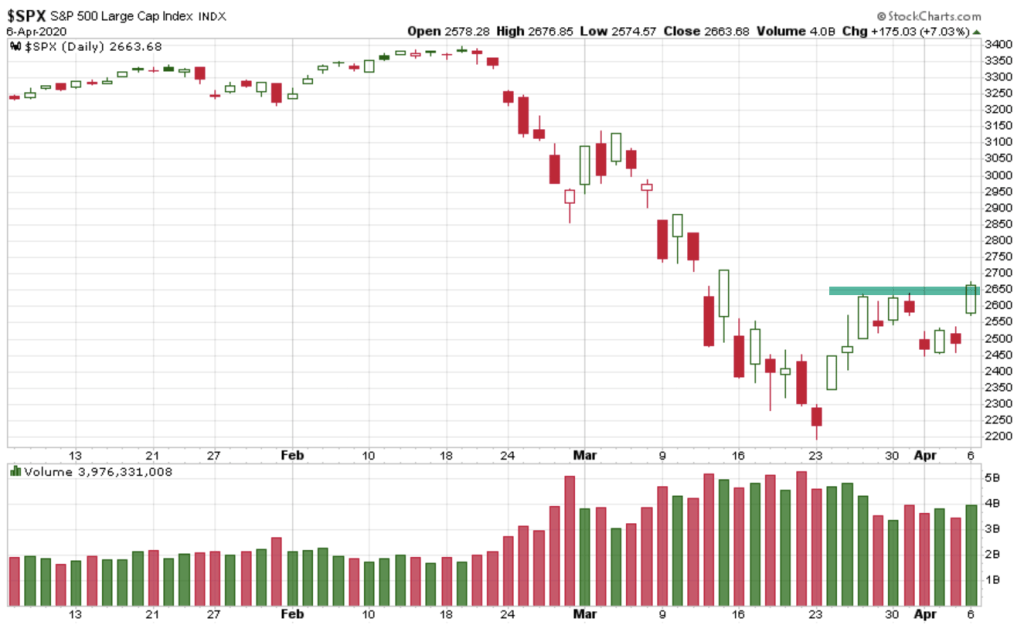

The stock market as measured by the S&P 500 made a solid advance today by any measure. According to Walter Deemer, today was a 90.3% upside day with 2732 advances and 276 declines. So far, March 23rd was the lowest point and the stock market is trying to recover some of the losses. The day after the low was March 24 was a 93.9% upside day with 2791 up and 244 down, which was even stronger. So, the advance off the low is showing some thrust, but only time will tell if it can continue, or if this is just an oversold bounce.

Getting more technical with the charting, the candlesticks show some bullish patterns. However, the S&P 500 has already reached the mid way point in my momentum measures were I expect if it’s going to stall, this is where it happens.

Many people believe the news headlines drive stocks prices, but today is yet another example that it isn’t necessarily that case. The news was bad today, with headlines like “U.S. Death Toll From Coronavirus Tops 10,000” and “U.K. Prime Minister Boris Johnson Moved to Intensive Care” and then “Virus Puts a Prison Under Siege.”

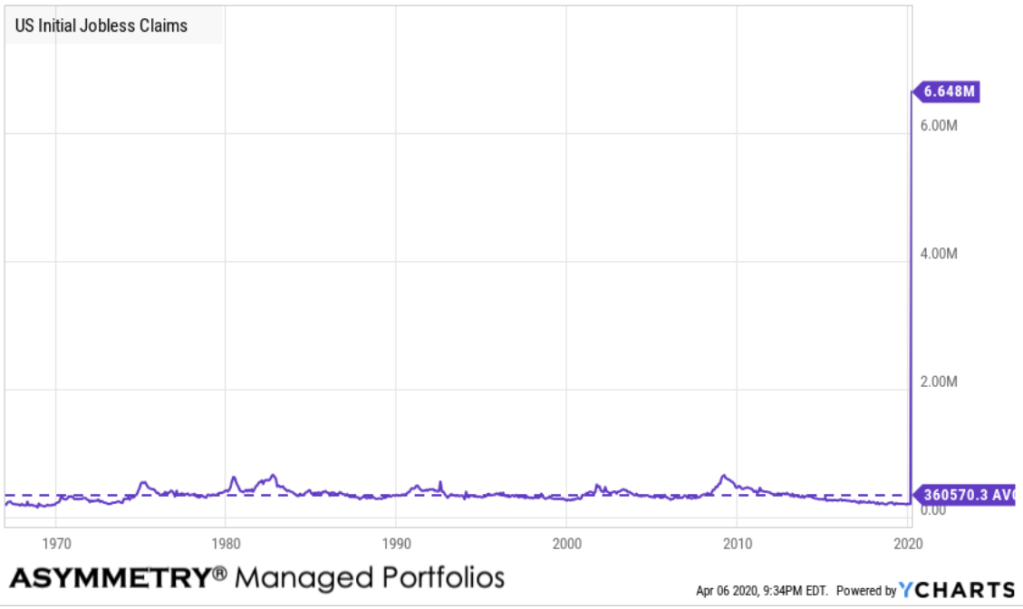

US Initial Jobless Claims last week was off the charts. Provided by the US Department of Labor, US Initial Jobless Claim provides underlying data on how many new people have filed for unemployment benefits in the previous week. Given this, one can gauge market conditions in the US economy with respect to employment; as more new individuals file for unemployment benefits, fewer individuals in the economy have jobs. Historically, initial jobless claims tended to reach peaks towards the end of recessionary periods such as on March 21, 2009, with a value of 661,000 new filings.

US Initial Jobless Claims is at a current level of 6.648M, an increase of 3.341M or 101.0% from last week. This is an increase of 6.436M or 3,004% from last year and is higher than the long term average of 353698.

If there was anything we learned from the last 11 years is the truth behind the axiom “don’t fight the Fed.” Fed intervention and the passage of a record-breaking $2.3 trillion US fiscal stimulus has supported fragile consolidation across many markets, including Treasuries, agency mortgage-backed securities and money markets.

A global recession is now imminent.

They won’t call it for another year or two, but I will now. We’ll see negative GDP growth across the world, although it may well recover as sharply as it fell. Once restaurants, etc. finally open back up, they will be in high demand. So, if restaurants can hang in there, there will be brighter days ahead. Right now, we just don’t know how long it may take.

As for the Coronavirus and data, we’ve discovered many issues with the data being reported by states. I’ve been monitoring it waiting for some improvements before sharing any more quantitative analysis.

This ain’t my first rodeo riding a bucking bear. I operated successfully through the 2008-09 bear market as well as the 2000-03 bear market. Both of them included ugly recessions with people losing their jobs, etc.

This one will be worse. But, again, there’s also a good chance the recovery is just as stunning as the waterfall decline.

So, stay tuned.

Periods of high volatility are often followed by volatility contractions and that’s what we’re seeing now. However, it is highly likely we won’t be seeing a VIX at 12 anytime soon as I expect elevated implied volatility for a long time, driven by demand for hedging with options. It’s likely to be similar to post 1987 when the risk of a price shock remains price into options.

I’ve got a lot more to share, but timing is everything.

Don’t miss out, we’ll automatically send you an email of new ASYMMETRY® Observations by entering your email below.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.