I’m not going to be surprised if we see a VIX volatility expansion this week along with the range of stock prices spreading out.

There are plenty of potential catalysts that could drive volatility and uncertainty higher for those who need a story driving it.

According to Bloomberg:

As Fed officials begin their discussions on Tuesday they will have some more data with which to assess the economy. Personal income, pending home sales and consumer confidence statistics are all due that morning. Then on Thursday, the ISM manufacturing report is expected to show industry is stabilizing and continuing to expand. Friday’s trade data will be pored over for evidence that the skirmish with China is having an effect. Also next week, the Treasury will say on Wednesday how much money it needs to borrow amid rising budget deficits.

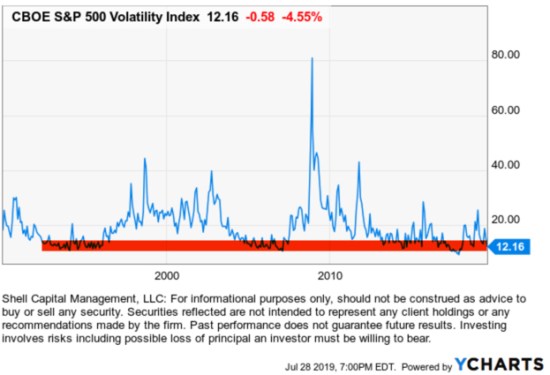

For me, the driver of a volatility expansion $VIX will just seem like a normal countertrend from a historically very low point. As vol has contracted into the 12’s it is at the low level of its cyclical range. This is when I start looking for a reversal.

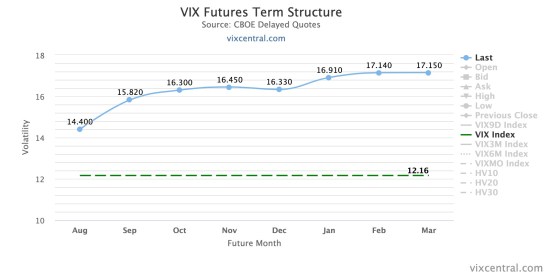

VIX futures are at a 9.86% contango, so the roll yield is a little steep. That is, the September VIX future is about 10% higher in price than the August VIX price. The difference in the price creates a roll yield those traders who are short VIX options or futures hope to earn.

Those of us more focused on the directional trend, especially countertrends, will be more alert to see volatility expand from here. The trouble is, the contango creates a headwind for the ETFs and ETNs we may want to enter long at some point. That’s because they may invest in both the front month and second month, so as they roll forward through time they are selling the lower-priced august to buy more of the higher-priced September. This negative roll yield is why the VIX based ETFs trend down over the long term. To trade them successfully, timing is important, but it’s also not so simple.

The next chart is the S&P 500 stock index with Bollinger Bands around the price trend set at two standard deviations from its 20 day moving average. While the VIX is an implied volatility index based on how the options market has priced options of the S&P 500 index stocks, these bands are measures of realized volatility. Actual volatility has also contracted recently.

Periods of low and contracting volatility are often followed by periods of higher and expanding volatility.

Let’s see how it goes…

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

Mike Shell and Shell Capital Management, LLC is a registered investment advisor and provides investment advice and portfolio management exclusively to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data is deemed reliable, but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. Use of this website is subject to its terms and conditions.

You must be logged in to post a comment.