In October 2004, Jason Zweig interviewed Peter Bernstein for MONEY Magazine. The title was Peter Bernstein interview: He may know more about investing than anyone alive. Peter L. Bernstein was an early pioneer of tactical asset allocation thinking. He wrote about valuation-based asset allocation and being tactical in decisions rather than passive. He believed what I believe: we should take more risk when its likely to be rewarded and less risk when it is less likely to be rewarded. He published several books about it.

In the interview, Zweig asked:

“Is market timing [short-term trading back and forth among asset classes] really a good idea?”

Bernstein answered:

“For institutional investors, the policy portfolio [a rigid allocation like 60% stocks, 40% bonds] had become a way of passing the buck and avoiding decisions. The problem was that institutions had settled on a [mostly stock] asset allocation because in the long run, they concluded, that’s the only place to be. And I think the long run ain’t what it used to be. Stocks don’t have to do well in the future because they did well in the past. In fact, the opposite may be more likely.”

Source: http://money.cnn.com/2004/10/11/markets/benstein_bonus_0411/

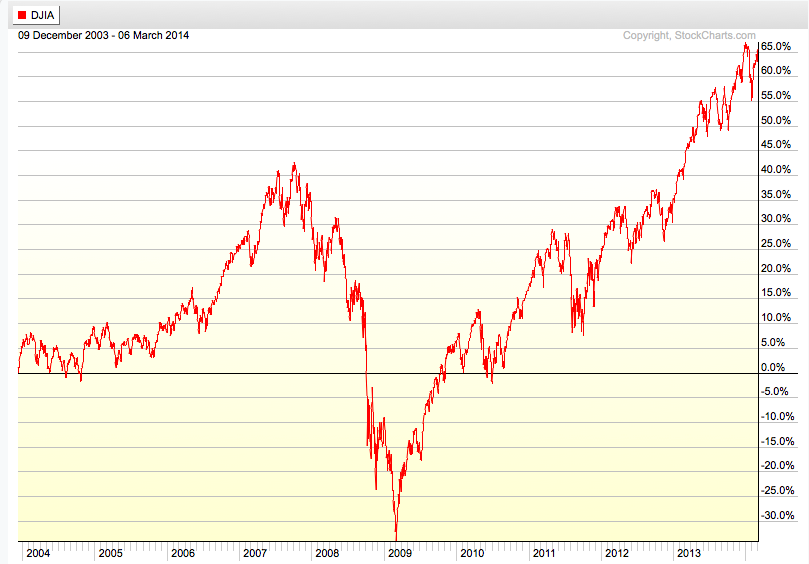

Based on the chart below, which shows the Dow Jones Industrial Average (a stock index that cannot not be invested in directly) since that interview in 2004, I’d say Bernstein was right. Over the next decade, the stock index went on to gain 65%, but it dropped nearly that much along the way. That doesn’t seem to be the kind of asymmetry® that investors are looking for. If you look at it close enough, you can probably see why it makes sense to take more risk at some points, less risk at others. Though, it’s probably at the opposite times most investors do. So, most will advise investors not to try to do it. Like most things in life, some do it much better than others and have active track records that reflect it.

You must be logged in to post a comment.