When asked to sum the Buddha’s teachings up in one phrase, Suzuki Roshi simply said,

“Everything changes.”

The universe is transient, in a constant state of flux. This impermanence, that things are constantly changing and evolving, is one of the few things we can be sure about. Whatever it is today, it will evolve and eventually change. I believed this, so I embraced change and uncertainty. That led me to deeply study rates of change, the magnitude of change, and the probability of change.

So when I speak about volatility, I am necessarily talking about “how much it has changed”. Volatility is the range of change. If there is no volatility, there is no change. If the range is very wide, the range of outcomes is wide.

In statistics, a standard deviation is a measure that is used to quantify this amount of range, variation, or dispersion of a set of data. In finance, it’s used to measure the range of prices. Many use it as a risk measure.

As of this month, I have been managing ASYMMETRY® Global Tactical for 10 years. Ten years is somewhat an arbitrary time frame, but it’s also a meaningful milestone given the range of change over this period. This past decade has been unique in that it included a range of change few have experienced or observed before. It’s really just change doing what it does.

What has changed over the past 10 years?

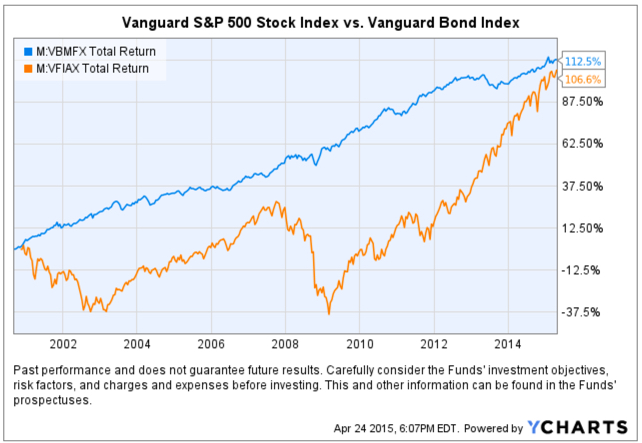

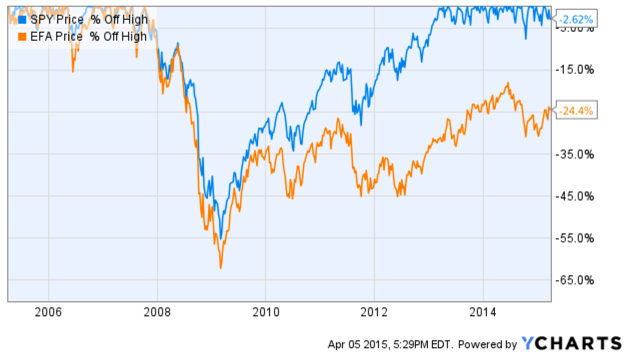

In A Tale of Two Conditions for U.S. and International Stocks: Before and After 2008 I pointed out the material change in the directional trends of the U.S. stock market vs. international stocks. Prior to 2008, the international stock market indexes were materially stronger trends than U.S. stocks. Since 2008, the U.S. stock market rate of change has been stronger than the global markets.

Another very significant change has been volatility. The change in volatility is critical to understand as I pointed out in This is When MPT and VaR Get Asset Allocation and Risk Measurement Wrong. Below, I will illustrate visually how volatility has changed and what it means today.

Historical standard deviation is commonly used in investment models as an input for volatility and is often considered a measure of ‘risk”. In some ways that is true, in other ways I disagree. When prices trade in a wide range up and down, it tends to get attention. Investors start to watch it closely. If a portfolio goes up 10% and then down -10% over a period of time, it gets the investors attention. If that portfolio declines -20%, then gains 10%, then declines -15%, they may have a reaction. We call the actual decline “drawdown”, but the widening range and how fast the values move up and down is called “volatility”.

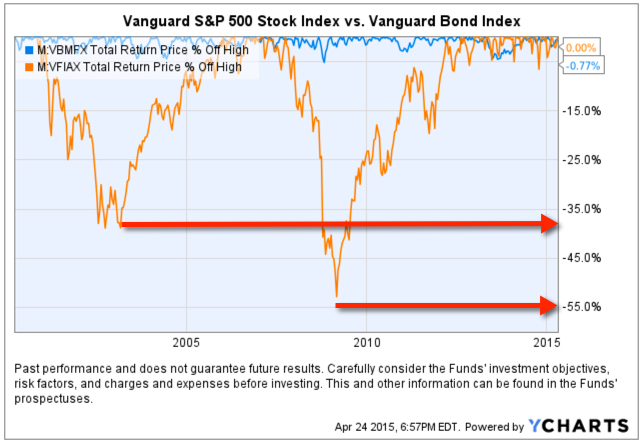

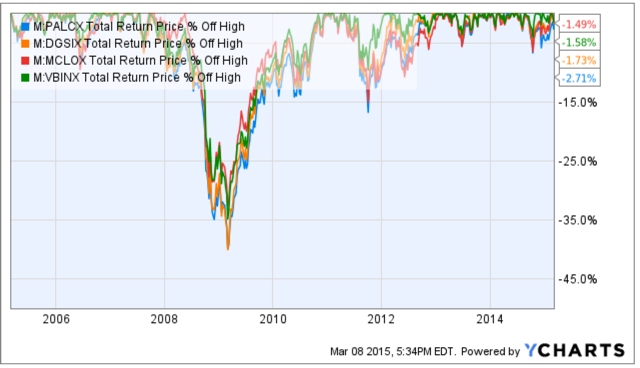

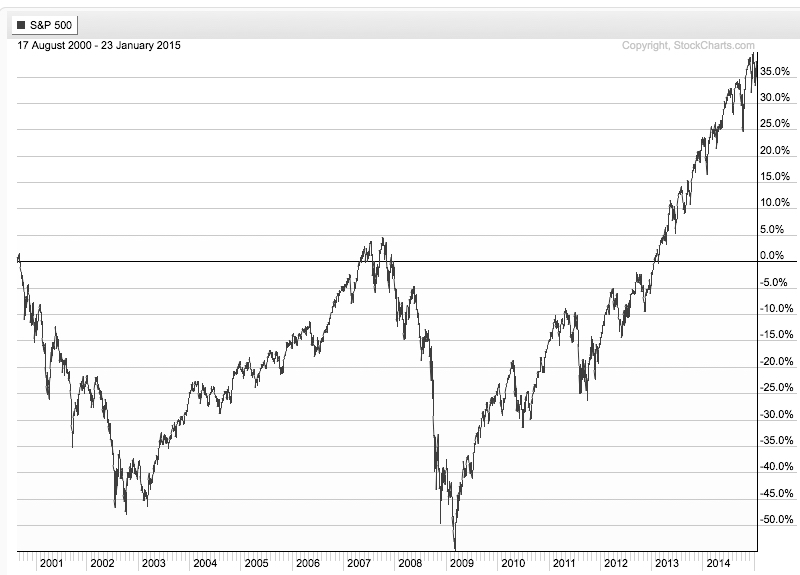

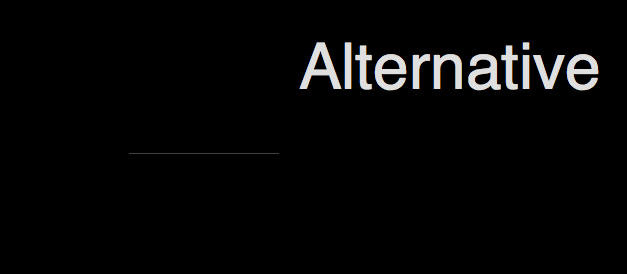

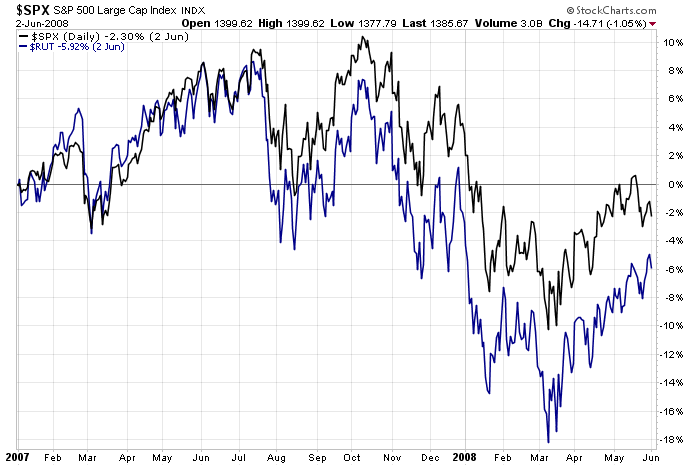

The chart below is the S&P 500 stock index (blue line) and the historical volatility as measured by standard deviation with a 1 year look-back. As you can see, historical volatility as measured by standard deviation tends to decline after the price trend rises such as 2005 to late 2007 and again starting in 2013 to now. We can also observe it increasing significantly after the stock index declined. Historical volatility stayed very high after 2008 and observing from a 1 year look-back, it remained very high until late 2013. Investors dislike volatility because it’s more difficult to hold on to a trend when its range up and down is high. If investors don’t like volatility, then you can see why they had such a hard time holding stock positions for several years.

Clearly, investors who don’t like volatility had a very difficult time holding the stock market up until recently. The past decade has shown us material changes in volatility from the low and decreasing period pre-2008 to the extreme high volatility up until late 2013. Some investors may now even be thinking of getting “more aggressive”, now that the wide price swings have become a distant memory. But you may consider that low volatility is a sign of less indecision. After prices trend up for years, investors become more complacent and therefore volatility declines. Just as we saw in 2007, we shouldn’t be surprised to see volatility very low at the price peak.

You can probably see how this is a real problem. On the one hand, if we want investors to be able to handle the volatility of a investment program, the risk and volatility necessarily needs to be managed so they don’t experience it. An active risk management system with an absolute return objective like I operate wants to have less exposure during highly volatile periods investors prefer to avoid. Yet, you may see how many investors who apply conventional asset allocation and risk measures, like Modern Portfolio Theory and Value at Risk that use standard deviation as an input, are likely to have models that get them more exposure at the peaks and less exposure at the lows. That is, at the peaks their models expected return is at its highest and its expected variance is at its lowest. After a major decline in price just the opposite is true: their expected return based on the historical return is at its lowest and expected variation is the highest.

The past 10 years was a very challenging period anyway we slice it. But an investment program like ASYMMETRY® Global Tactical that avoided large drawdowns as well as avoided such radical swings, allowed investors to stick with the program and compound capital positively rather than panic out or deal with large losses and drawdowns.

The Greek philosopher Heraclitus famously said, “No same man could walk through the same river twice, as the man and the river have since changed.” I think we can be sure about only one thing: the next price trend and volatility will be different, so I embrace it and am prepared for however it unfolds.

{kind=link}

{kind=link}

You must be logged in to post a comment.