A fellow portfolio manager I know was telling me about a sharp price drop in one of his positions that was enough to wipe out the 40% gain he had in the stock. Of course, he had previously told me he had a quick 40% gain in the stock, too. That may have been his signal to sell. Biogen, Inc (BIIB) recently declined about -30% in about three days. Easy come, easy go. Below is a price chart over the past year.

Source: Shell Capital Management, LLC created with http://www.stockcharts.com

Occasionally investors or advisors will ask: “Why trade index ETFs instead of individual stocks?“. An exchange-traded fund (ETF) is an investment fund traded on stock exchanges, much like stocks. Until ETFs came along the past decade or so, gaining exposure to sectors, countries, bond markets, commodities, and currencies wasn’t so easy. It has taken some time for portfolio managers to adapt to using them, but ETFs are easily tradable on an exchange like stocks. Prior to ETFs, those few of us who applied “Sector Rotation” or “Asset Class Rotation” or any kind of tactical shifts between markets did so with much more expensive mutual funds. ETFs have provided us with low cost, transparent, and tax efficient exposure to a very global universe of stocks, bonds, commodities, currencies, and even alternatives like REITs, private equity, MLP’s, volatility, or inverse (short). Prior to ETFs we would have had to get these exposures with futures or options. I saw the potential of ETFs early, so I developed risk management and trend systems that I’ve applied to ETFs that I would have previously applied to futures.

On the one hand, someone who thinks they are a good stock picker are enticed to want to get more granular into a sector and find what they believe is the “best” stock. In some ways, that seems to make sense if we can weed out the bad ones and only hold the good ones. It really isn’t so simple. I view everything a reward/risk ratio, which I call asymmetric payoffs. There is a tradeoff between the reward/risk of getting more detailed and focused in the exposure vs. having at least some diversification, such as exposure to the whole sector instead of just the stock.

Market Risk, Sector Risk, and Stock Risk

In the big picture, we can break exposures into three simple risks (and those risks can be explored with even more detail). We’ll start with the broad risk and get more detailed. Academic theories break down the risk between “market risk” that can’t be diversified away and “single stock” and sector risk that may be diversified away.

Market Risk: In finance and economics, systematic risk (in economics often called aggregate risk or undiversifiable risk) is vulnerable to events which affect aggregate outcomes such as broad market declines, total economy-wide resource holdings, or aggregate income. Market risk is the risk that comes from the whole market itself. For example, when the stock market index falls -10% most stocks have declined more or less.

Stock and Sector Risk: Unsystematic risk, also known as “specific risk,” “diversifiable risk“, is the type of uncertainty that comes with the company or industry itself. Unsystematic risk can be reduced through diversification. If we hold an index of 50 Biotech stocks in an index ETF its potential and magnitude of a large gap down in price is less than an individual stock.

You can probably see how holding a single stock like Biogen has its own individual risks as a single company such as its own earnings reports, results of its drug trials, etc. A biotech stock is especially interesting to use as an example because investing in biotechnology comes with a unique host of risks. In most cases, these companies can live or die based on results of drug trials and the demand for their existing drugs. In fact, the reason Biogen declined so much is they reported disappointing second-quarter results and lowered its guidance for the full year, largely because of lower demand for one of their drugs in the United States and a weaker pricing environment in Europe. That is a risk that is specific to the uncertainty of the company itself. It’s an unsystematic risk and a selection risk that can be reduced through diversification. We don’t have to hold exposure to just one stock.

With index ETFs, we can gain systematic exposure to an industry like biotech or a sector like healthcare or a broader stock market exposure like the S&P 500. The nice thing about an index ETF is we get exposure to a basket of stocks, bond, commodities, or currencies and we know what we’re getting since they disclose their holdings on a daily basis.

ETFs are flexible and easy to trade. We can buy and sell them like stocks, typically through a brokerage account. We can also employ traditional stock trading techniques; including stop orders, limit orders, margin purchases, and short sales using ETFs. They are listed on major US Stock Exchanges.

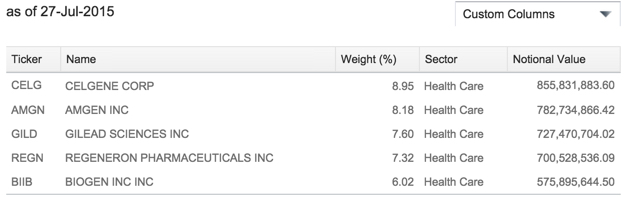

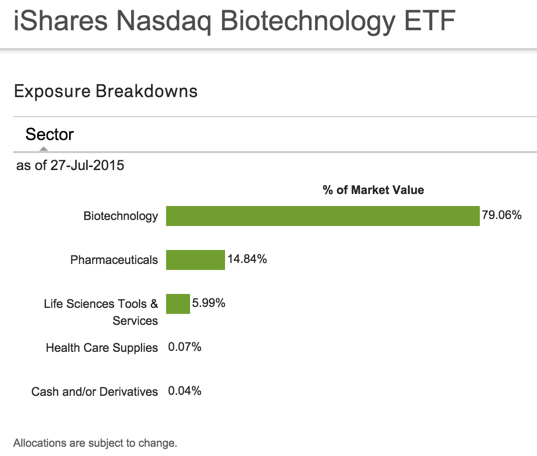

The iShares Nasdaq Biotechnology ETF objective seeks to track the investment results of an index composed of biotechnology and pharmaceutical equities listed on the NASDAQ. It holds 145 different biotech stocks and is market-cap-weighted, so its exposure is more focused on the larger companies. It therefore has two potential disadvantages: it has less exposure to smaller and possibly faster growing biotech stocks and it only holds those stocks listed on the NASDAQ, so it misses some of the companies that may have moved to the NYSE. According to iShares we can see that Biogen (BIIB) is one of the top 5 holdings in the index ETF.

Source: http://www.ishares.com/us/products/239699/ishares-nasdaq-biotechnology-etf

Source: http://www.ishares.com/us/products/239699/ishares-nasdaq-biotechnology-etf

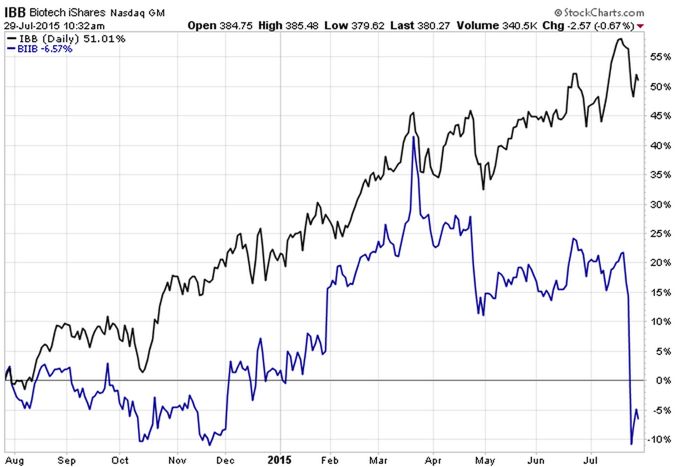

Below is a price chart of the popular iShares Nasdaq Biotech ETF (IBB: the black line) compared to the individual stock Biogen (BIIB: the blue line). Clearly, the more diversified biotech index has demonstrated a more profitable and smoother trend over the past year. And, notice it didn’t experience the recent -30% drop that wiped out Biogen’s price gain. Though some portfolio managers may perceive we can earn more return with individual stocks, clearly that isn’t always the case. Sometimes getting more granular in exposures can instead lead to worse and more volatile outcomes.

Source: Shell Capital Management, LLC created with http://www.stockcharts.com

The nice thing about index ETFs is we have a wide range of them from which to research and choose to add to our investable universe. For example, when I observe the directional price trend in biotech is strong, I can then look at all of the other biotech index ETFs to determine which would give me the exposure I want to participate in the trend.

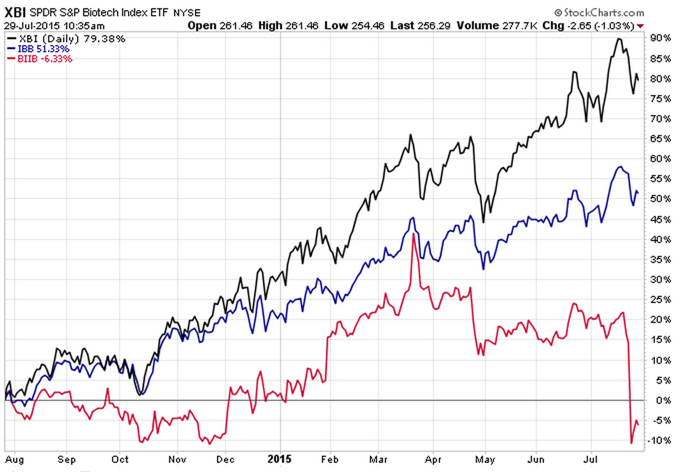

Since we’ve observed with Biogen the magnitude of the potential individual risk of a single biotech stock, that also suggests we may not even prefer to have too much overweight in any one stock within an index. Below I have added to the previous chart the SPDR® S&P® Biotech ETF (XBI: the black line) which has about 105 holdings, but the positions are equally-weighted which tilts it toward the smaller companies, not just larger companies. As you can see by the black line below, over the past year, that equal weighting tilt has resulted in even better relative strength. However, it also had a wider range (volatility) at some points. Though it doesn’t always work out this way, you are probably beginning to see how different exposures create unique return streams and risk/reward profiles.

Source: Shell Capital Management, LLC created with http://www.stockcharts.com

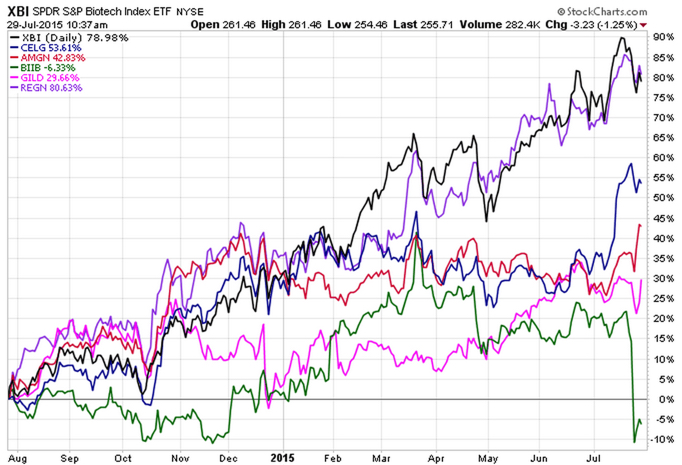

In fact, those who have favored “stock picking” may be fascinated to see the equal-weighted SPDR® S&P® Biotech ETF (XBI: the black line) has actually performed as good as the best stock of the top 5 largest biotech stocks in the iShares Nasdaq Biotech ETF.

Source: Shell Capital Management, LLC created with http://www.stockcharts.com

Biotech indexes aren’t just pure biotech industry exposure. They also have exposures to the healthcare sector. For example, iShares Nasdaq Biotech shows about 80% in biotechnology and 20% in sectors categorized in other healthcare industries.

Source: www.ishares.com

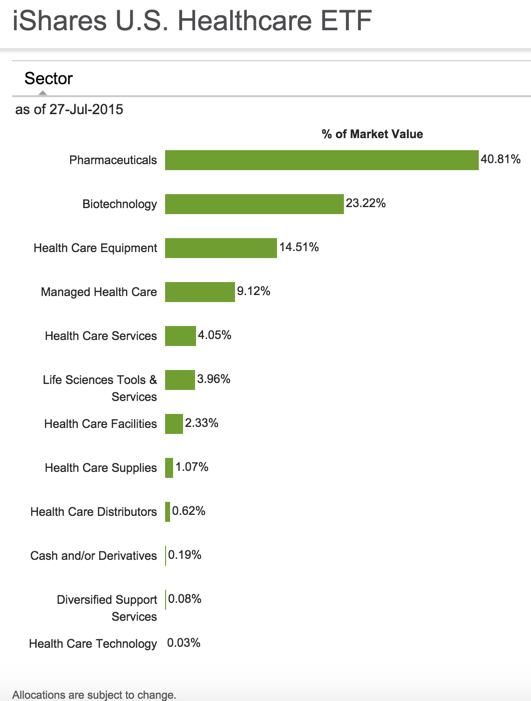

The brings me to another point I want to make. The broader healthcare sector also includes some biotech. For example, the iShares U.S. Healthcare ETF is one of the most traded and includes 23.22% in biotech.

Source: https://www.ishares.com/us/products/239511/IYH?referrer=tickerSearch

It’s always easy to draw charts and look at price trends retroactively in hindsight. If we only knew in advance how trends would play out in the future we could just hold only the very best. In the real world, we can only identify trends based on probability and by definition, that is never a sure thing. Only a very few of us really know what that means and have real experience and a good track record of actually doing it.

I have my own ways I aim to identify potentially profitable directional trends and my methods necessarily needs to have some level of predictive ability or I wouldn’t bother. However, in real world portfolio management, it’s the exit and risk control, not the entry, the ultimately determines the outcome. Since I focus on the exposure to risk at the individual position level and across the portfolio, it doesn’t matter so much to me how I get the exposure. But, by applying my methods to more diversified index ETFs across global markets instead of just U.S. stocks I have fewer individual downside surprises. I believe I take asset management to a new level by dynamically adapting to evolving markets. For example, they say individual selection risk can be diversified away by holding a group of holdings so I can efficiently achieve that through one ETF. However, that still leaves the sector risk of the ETF, so it requires risk management of that ETF position. They say systematic market risk can’t be diversified away, so most investors risk that is left is market risk. I manage both market risk and position risk through my risk control systems and exits. For me, risk tolerance is enforced through my exits and risk control systems.

The performance quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance quoted, and numbers may reflect small variances due to rounding. Standardized performance and performance data current to the most recent month end may be obtained by clicking the “Returns” tab above.

{kind=link}

{kind=link}

You must be logged in to post a comment.