– David Ricardo 1772 – 1823

Those words, today known as “The Golden Rule of Trading”, were printed in The great metropolis, Volume 2 By James Grant in 1838. To be sure what he specifically meant:

– David Ricardo 1772 – 1823

Those words, today known as “The Golden Rule of Trading”, were printed in The great metropolis, Volume 2 By James Grant in 1838. To be sure what he specifically meant:

Who would believe the government of world’s greatest country, the United States of America, would shut down? And, since it did today, who would expect the Dow Jones Industrial Average would be up 65 points at noon? Portfolio management requires preparation and dealing with unlikely events – those that may even seem impossible. And then, accepting the things we cannot change. With that in mind:

Impossibilities in the World

No matter how smart you are…

1) You can’t count your hair.

2) You can’t wash your eyes with soap.

3) You can’t breathe when your tongue is out.

Put your tongue back in your mouth, silly!

It’s a Beautiful Morning even when it’s not…

Portfolio Management is about buying and selling many different positions over time, not just one “pick”. I often say it’s like flipping 10 coins at the same time with each having a different payoff and profit or loss. It could be a completely random process (like flipping a coin), but if we can positively skew the payoffs (asymmetric payoffs) we end up with more profit than loss (asymmetric returns). And, as a portfolio manager I may flip that coin 100 or 500 times a year. The fact is: if the expectation for profit is positive we want to do it as often as possible.

Picking just one position is like flipping the coin just once. Its outcome may have an expected probability and payoff that is positive, but will be determined by how it all unfolds. We can never control the outcome at the point of entry. It’s the exit that always determines the outcome. We can say that same whether we are speaking of stocks, bonds, commodities, and currencies or buying and selling private businesses: if you actually knew for sure the outcome would be positive you would only need to do it once – but you don’t. So deciding what to buy is a small part of my complete portfolio management process. It’s what I do after I’m in a position that makes it “management”. To manage is to direct and control. If all you do is “buy” or “invest” in a position, you have no position “management”.

But when Trang Ho at INVESTOR’S BUSINESS DAILY®recently asked me “What ‘s the one position you would choose over the next several months and why”, I gave her the first position I thought of – and the most recent position I had taken. I primarily get positioned with the current direction of the trend and stay with it until it changes. That may be labeled “trend following”. I define the direction of the trend (up, down, sideways) and then get in that direction until it changes. Trends don’t last forever. There is a point when the probability becomes higher and higher of a reversal. I call that a “counter-trend”. I developed systems that define these directional trends more than a decade ago and have operated them for-profit since. What I can tell you from my experience, expertise, and empirical evidence is that stock market trends, like many other market trends, cycle up and down over time. So, portfolio management is a daily routine of position management that includes predefining risk at the point of entry, taking profits, and knowing when to exit to keep losses small. That exit, not the entry, determines the outcome.

You may consider these things as you read my recent interview in Investors Business Daily titled: Market Strategists: 5 Contrarian ETF Investing Ideas.

Read More At Investor’s Business Daily: http://news.investors.com/investing-etfs/090613-670234-contrarian-etf-investing-ideas-stock-market-strategists.htm#ixzz2gNp8bWUT

Source: ORACLE® Team USA

If things actually worked they way we are taught in school, all you need to do it get a “college degree” and you’ll be successful.

The reality is, learning the essentials like reading, writing, and arithmetic are basic requirements like eating, sleeping, and you know what.

To be great at something, we have to do a lot more than the basics.

You may consider that many of the greatest game-changers in America didn’t need anyone to tell them what to do next. They instead charted their own course and it was one that didn’t exist before.

Our society wants us to fit into the middle of the bell curve like the average person, but for some of us it’s a lot more fun to be an outlier,

Congratulations! To Larry Ellison and his ORACLE® Team USA for completing an improbable comeback to win Race 19 to successfully defend the 34th America’s Cup on Wednesday in San Francisco.

It’s a fine example of a game-changing asymmetry.

Before the huge win, Larry Ellison, who is co-founder and CEO of ORACLE®, was criticized for skipping a keynote address at a company conference to instead watch the comeback of his regatta team. It was a once in a lifetime moment only a few will ever experience by a man who has earned his freedom.

It’s a fine example of knowing when to get off the treadmill…

And, if you know the story, this unlikely outcome came from an unlikely team to start with. The combination of a billionaire CEO and a car radiator mechanic. The story is in The Billionaire and the Mechanic by Julian Guthrie. (I’ve been listening to the Audible version). It’s about how an unlikely duo won the sport’s oldest trophy – before this one. From Amazon:

“The America’s Cup, first awarded in 1851, is the oldest trophy in international sports, and one of the most hotly contested. In 2000, Larry Ellison, co-founder and billionaire CEO of Oracle Corporation, decided to run for the coveted prize and found an unlikely partner in Norbert Bajurin, a car radiator mechanic who had recently been named Commodore of the blue collar Golden Gate Yacht Club.

Julian Guthrie’s The Billionaire and the Mechanic tells the incredible story of the partnership between Larry and Norbert, their unsuccessful runs for the Cup in 2003 and 2007, and their victory in 2010. With unparalleled access to Ellison and his team, Guthrie takes readers inside the design and building process of these astonishing boats, and the management of the passionate athletes who race them. She traces the bitter rivalries between Oracle and their competitors, including Swiss billionaire Ernesto Bertarelli’s Team Alinghi, and throws readers into exhilarating races from Australia and New Zealand to Valencia, Spain.

With new television coverage and huge media, the America’s Cup is poised to be bigger than ever, and The Billionaire and the Mechanic is a must-read for anyone interested in the race or this remarkable story.”

The “red pill” and “blue pill” refer to a choice between the willingness to learn a potentially unsettling or life-changing truth by taking the red pill or remaining in contented ignorance with the blue pill. It refers to a scene in the 1999 film The Matrix.

I have been talking to a financial planner recently who is struggling between the red pill and the blue pill.

On the one hand, the poor performance of stock and bond indexes over the past decade or so, particularly the losses in bear markets, led him to study long-term market cycles.

An understanding that markets don’t always go up over long periods is the reality of the red pill.

On the other hand, much of the investment industry still believes in getting “market returns” and that a simple plan of “asset allocation” and occasional re-balancing is prudent enough, so a financial planner can choose to keep his practice simple by continuing that plan.

Some investment advisers even consider re-balancing and an occasional change “tactical”.

It isn’t.

The blue pill and the red pill are opposites, representing the choice between the blissful ignorance of illusion (blue) and embracing the painful truth of reality (red).

On the one hand, after understanding the trends of global markets based on simply looking at their history, he realizes the probable outcome of stocks and bonds based on trends I discuss in The S&P 500 Stock Index at Inflection Points and 133 Years of Long Term Interest Rates. Though price trends can continue far more than you expect, the stock and bond markets are at a point where their trends could reverse. The financial planner realizes if he takes the red pill of reality, he’ll have to embrace these facts and do something rather than sit there. He’ll have to change his long-held beliefs that markets are efficient and the best you can do is allocate to them. He’ll have to do extra assignments and homework to find alternative investment managers whose track record suggests they may have the experience and expertise to operate through challenging market conditions.

On the other hand, changing one’s beliefs and taking a different approach can be extra work and have risks. If he continues the static asset allocation to stocks and bonds he’s always done, he says he won’t be doing something so different from the majority of advisers. He knows his career and his life will be easier. When the markets go up, his clients make market returns (minus his fees). When the markets go down, other people are losing money too, and he certainly can’t control what the market does, so: it’s the market. I can see how this is an enticing business model, especially for a busy person who has a life outside the office. That’s probably why it’s so popular.

A similar theme of duality happens in the movie The Matrix.

Morpheus offers Neo either a blue pill (to forget about The Matrix and continue to live in the world of illusion) or a red pill (to enter the sometimes painful world of reality).

Duality is something consisting of two parts: a thing that has two states that may be complementary or opposed to each other. We all get to choose what we believe and our choices shape the world we individually live in.

I can’t say that I can totally relate to the financial adviser because it is my nature to be more tactical and active in decision-making. I believe we should actively pursue what we want. And, I believe what we want from the markets is in there, I just have to extract it from the parts we don’t want. I once explained my investment strategy to a lifelong friend and he replied “you have always been tactical” and reminded me of my background. Though it’s different from me, I can truly appreciate the struggle advisers and investors face choosing between the red or blue pill. Investors and advisers like “market returns” when they are positive, which is what we experience most of the time. It’s when those markets decline that they don’t want what the market dishes out. The markets don’t spend as much time in declines. I pointed out in The Real Length of the Average Bull Market the average upward trend for stocks (bull market) lasts 39 months while the average decline ( bear market) is about 17 months. Investors eventually forget and become complacent about the time they need a reminder. Though the stock markets trend up about 3 times longer than they trend down, it’s the magnitude of the losses that cause long-term investors a problem. For example, the bull market from 2003 through October 2007 gained over 105% but the -56% decline afterward wiped out those gains. You can see that picture in The S&P 500 Stock Index at Inflection Points.

The risk for the financial adviser who has historically focused on “market returns” is that a new strategy for them that applies some type of active risk management is likely to be uncorrelated and maybe even disconnected at times from “market returns”. For example, I discussed that in Understanding Hedge Fund Index Performance. Investors who are used to “market returns” but need a more absolute return strategy with risk management may require behavior modification. If they want an investment program that compounds capital positively by avoiding large losses and capturing some gains along the way they have to be able to stick with it. That requires the adviser to spend more time educating his or her investors about the reality of the red pill. Kind of like I am doing now. Some people have more difficulty doing something different, so they need more help. Others are better able to see the big picture. Some financial advisers would rather deal with explaining the losses when markets decline. For them, it can be as simple as forwarding clients some articles about the market going down with a message something like “We’re all in this together – let’s just hunker down”. That doesn’t require a great deal of independent thinking or doing.

While most individual investors probably do lose money when the stock and bond markets do, that isn’t necessarily the case for those who direct and control downside risk.

It isn’t enough to have a good investment program with a strong performance history.

Just as important is the ability to help investors modify their beliefs and behavior.

That’s the reality of the red pill.

By definition, active is more work than passive. Investors and advisers alike get to choose which pill they take: the blissful ignorance of illusion (blue) and embracing the painful truth of reality (red).

I believe in individual liberty and personal responsibility, so the choice is your own.

My thoughts on the subject are directional – I am the red pill.

Morpheus: “You have to understand, most of these people are not ready to be unplugged. And many of them are so inured, so hopelessly dependent on the system, that they will fight to protect it.”

“Unfortunately, no one can be told what the Matrix is.

You have to see it for yourself.”

Like The Matrix, this is going to be a sequel.

To be continued…

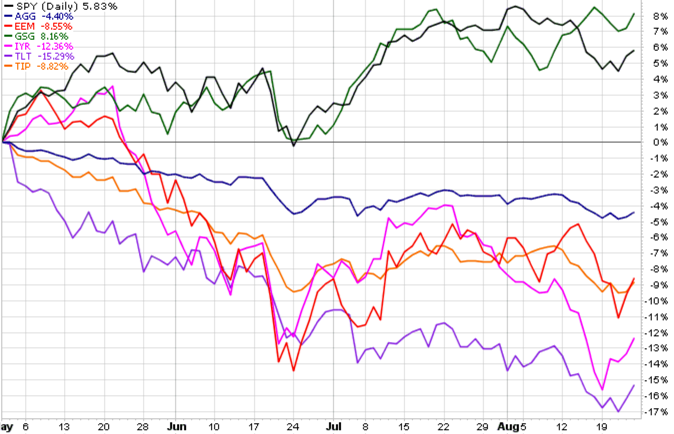

Since May, we observe that global market indexes have diverged. While some markets are still trending up, others are trending down. Prior to 2013, many markets were generally trending together. The current U.S stock bull market is now 52 months old from from its March 2009 bear market low. If history is a guide, it’s closer to the end (read: The S&P 500 Stock Index at Inflection Points). One of the things we see near the end of a major trend change is some world markets start to reverse down. For example, going in to 2008 it was Financials and REITs (real estate). As we see in the chart, U.S. stocks are still trending up for now, but emerging markets and all categories of bonds and Real Estate Investment Trusts (REITs) are weak. Rising interest rates = falling bond prices and falling interest rate sensitive markets like REITs. The diversification of global asset allocation over this period has actually resulted in more downside risk rather than reducing it. Bonds have been in a rising trend for the past 30 years, so when stocks drop -50% exposure to bonds haves helped to offset the losses for asset allocators who mix stocks and bonds. If bonds are changing to a downtrend as it appears they are, bonds may not be a crutch in the next bear market. In fact, they may inflate losses.

If you aren’t familiar with the index symbols for the markets in the table in the top left:

If you have any questions or comments, contact me.

First, we view 15 Year Chart of the 10 Year U.S. Treasury Note Yield (interest rate) (Symbol: $TNX). Keep in mind this chart reflects the rate of change in the interest rate, not the price trend. If we define a downtrend as “lower highs, lower lows” the 15 year trend for interest rates has been down. But since 2012, the trend has sharply turned up – though that isn’t the first time.

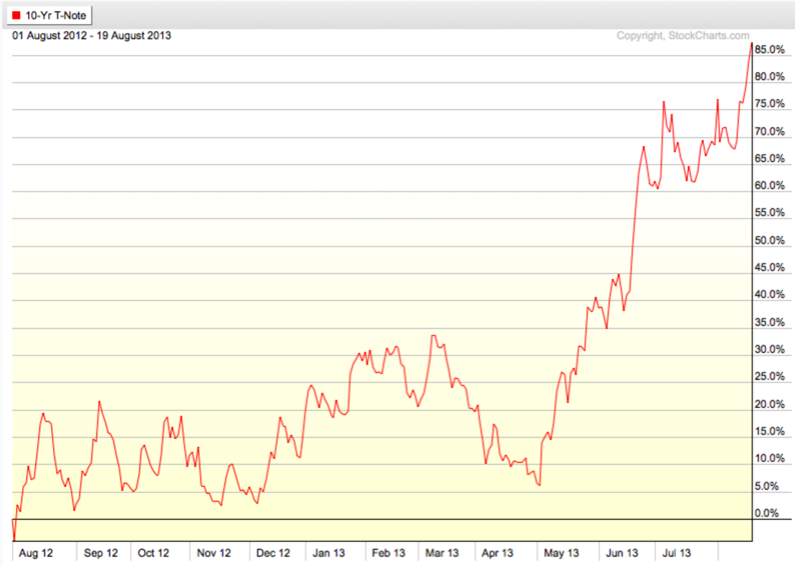

Next, we zoom in t0 view the magnitude of the interest rate on the 10 Year U.S. Treasury Note Yield since its low a year ago in August 2012. The interest rate on the 10 year treasury has gained 85%. The current yield is about 2.88%.

Next we look at the long term U.S. Treasury Bond Yield – the 30 year. Long terms rates have been in a downtrend the last 15 years, but have recently trended up sharply.

Understanding the implications of a reversal in the trend of interest rates is critical to a global macro fund manager. A large part of my global tactical decisions is identifying direction trend changes. and understanding how markets interact with each other. For example, we can see below how rising rates significantly impact the price value of bonds.

Below, we observe the total return (price trend + interest) of a wide range of different styles of bond ETFs.

Clearly, they have recently been in a downtrend with U.S. Government bonds down the most at -13.65% over the past year.

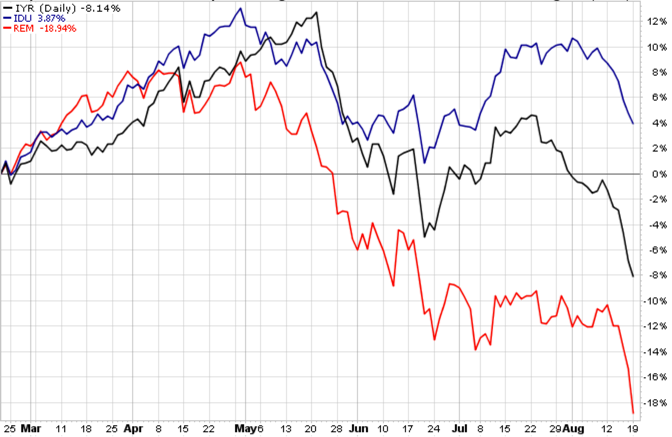

Finally, we observe some markets and sectors that are very sensitive to changes in interest rates.

Eventually the Federal Reserve will stop their “Quantitative Easing” program of buying bonds. You know how supply and demand works: when demand dries up, price goes down…

You must be logged in to post a comment.