On Monday, I shared on Twitter:

Today’s jobs report is a mighty fine example of the market responding to positive rates and change and surprise.

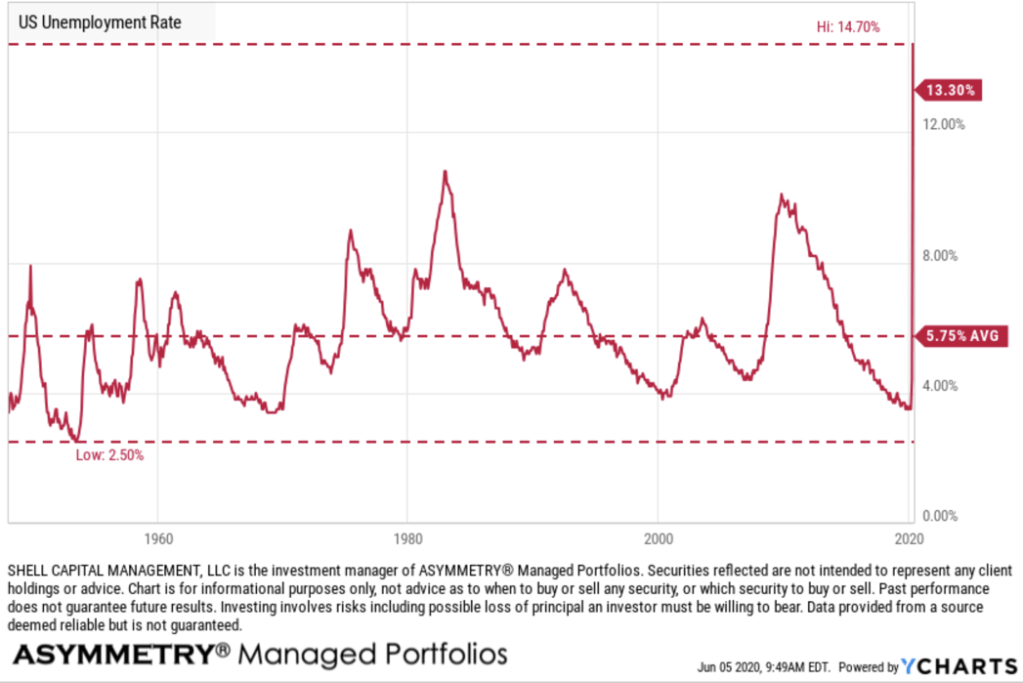

The US Unemployment Rate measures the percentage of total employees in the United States that are a part of the labor force, but are without a job.

It is one of the most widely followed indicators of the health of the US labor market and the US economy as a whole. Historically, the US Unemployment Rate reached as high as 10.80% in 1982 and 9.9% in November of 2009. Both of these times were notable recessionary periods.

That is, until COVID – 19 came along.

We saw a 14.7% unemployment rate in April in the United States of America. A stunning increase from such a low level in February of 3.5%. The unemployment rate had been declining, for example, it was 5.3% five years ago.

After today’s jobs report, the US Unemployment Rate is at 13.3%, compared to 14.7% last month and 3.6% last year. It’s still nearly three times higher than the long term average of 5.75%, but a lot better than Wall Street had expected.

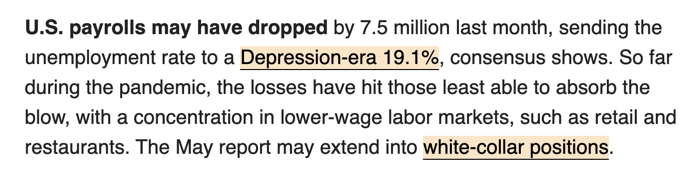

Wall Street expected a loss of 7.7 million jobs and a 19.8% unemployment rate today.

Bloomberg emailed sent out at 7AM this morning:

So, and Unemployment Rate at 13.3% is a huge positive surprise.

Some independent economist are already disputing the numbers.

In the last observation I shared last week, I said:

“And May’s unemployment number may be higher when it’s announced on June 5.

The stock market is said to be a discounting mechanism. The largest stock market investors who drive price trends don’t look back, they look forward.

It’s an auction market and operates on the proposition that investors and traders gaze into the future and discounts all known information about the present moment and expectations for what’s expected to happen next. So, when unexpected events happen, the market takes into account this new information very rapidly.

It certainly seems to be happening now.

Either the market is factoring in a quick recovery, or something else is driving it up.”

I think it’s safe to say the market has indeed gazed into the future and discounted a sharp recovery.

Yes, it certainly seems overly optimistic, but what is, is.

Notwithstanding a second wave of COVID-19 that hits even harder than the first, Wall Street seems to be pricing in the worst is behind for the U.S. economy.

What’s next?

It’s been a radical year. What else should we have expected out of 2020.

We’ve got to have some fun with it.

The US stock market will probably trend up today and reach an overbought level for the first time since January.

Remember: The market discounts the future, meaning it prices in future expectations. This discounting mechanism goes both ways.

The market is people. It’s large investors and small, but the largest investors drive the trends. It’s institutional investors managing money for others that are more advanced about gazing into the future.

Above all else, when it comes to forecasting or now casting a future trend, getting a grasp of what the majority of the market is thinking and doing is essential.

My guess is, the market has factored in the extremely aggressive response from the Federal Reserve and US Treasury to provide liquidity after it evaporated in March.

I know it’s very hard to go with the flow. Who would have believed this -37% decline would have recovered as much as it has so quickly?

No one.

But, it ain’t over till it’s over.

We have a new problem now.

The relative strength of stock indexes just tapped the overbought level, so the risk of a fall is now higher than it has been since this uptrend started.

Semper Gumby.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.