Ok, so this isn’t anything new. I just discussed it last week in “Investor sentiment signals greed is driving stocks as the U.S. stock market reaches short term risk of a pullback.” The sentiment indicators keep confirming the same signal: that investors are very optimistic about future gains.

It’s the kind of sentiment we often see before a decline.

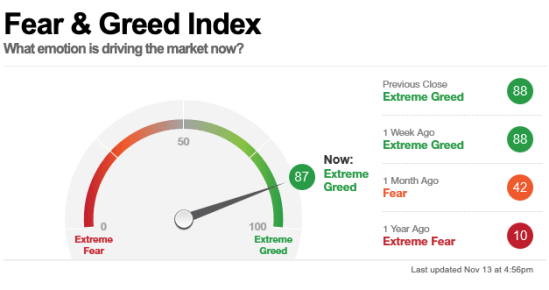

The Fear & Greed Index is a simple combination of seven different indicators that are considered investor behavior measures. It includes the Put/Call Ratio, the net new 52 week highs and lows, stock price breadth, market momentum, the yield spread between junk bonds and investment-grade, and market volatility. It’s a useful gauge to monitor against your own sentiment and behavior. The Fear & Greed gauge remains at a high level, signaling “Extreme Greed” and excessive optimism.

Just as the stock market cycles up and down over time, so does investor sentiment. In fact, I believe investor sentiment oscillating between fear and greed is what drives stocks in the short run.

We measure this investor behavior with these different indicators. For example, the number of stocks hitting 52-week highs exceeds the number hitting lows and is at the upper end of its range, indicating extreme greed. The S&P 500 is 4.90% above its 125-day average is another above the average than has been typical during the last two years and rapid increases like this often indicate extreme greed.

The Put/Call Ratio shows during the last five trading days, volume in put options has lagged volume in call options by 50.13% as investors make bullish bets in their portfolios. This is among the lowest levels of put buying seen during the last two years, indicating extreme greed on the part of investors.

Stocks have outperformed bonds by 4.50 percentage points during the last 20 trading days. According to the Fear & Greed Index, this is close to the strongest performance for stocks relative to bonds in the past two years and indicates investors are rotating into stocks from the relative safety of bonds.

Junk bond demand shows investors in low-quality junk bonds are accepting only 1.84% in additional yield over safer investment-grade corporate bonds. This spread is down from recent levels and indicates that investors are pursuing higher risk strategies.

Investors tend to feel the wrong feeling at the wrong time as they oscillate between the fear of missing out and the fear of losing money.

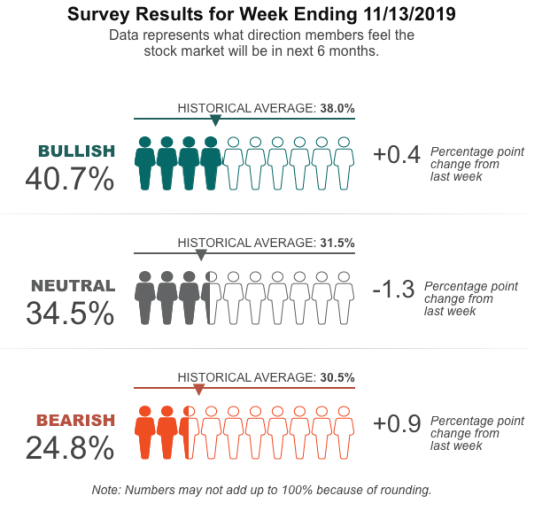

Another useful gauge I follow is the AAII Sentiment Survey. Since 1987, AAII members have been answering the same simple question each week. The results are compiled into the AAII Investor Sentiment Survey, which provides insight into the mood of individual investors. Today’s AAII Sentiment Survey shows Investors are optimistic again. Optimism is above 40% on back-to-back weeks for the first time since August 2018.

The investor misbehavior of thinking, feeling, and doing the wrong thing at the wrong time doesn’t just include individual investors, but also many professional investment managers.

‘Fear of missing out’ triggers huge fund manager shift from cash to stocks,

The latest Bank of America Merrill Lynch investment fund managers survey shows fund manager cash levels are lowest in six years and

“Investors are experiencing Fomo—the fear of missing out—which has prompted a wave of optimism and jump in exposure to equities and cyclicals,”

According to ‘Fear of missing out’ triggers huge fund manager shift from cash to stocks, Bank of America Merrill Lynch says:

The survey of 230 managers running $700 billion of assets found cash levels dropped 0.8 percentage points to 4.2%, the biggest monthly drop since Nov. 2016 and the lowest cash balance since June 2013.

Like individual investors, many investment managers also oscillate between the fear of missing out and the fear of losing money. This may be especially true for relative return mutual fund type active managers who aim to beat an index benchmark. If they are underperforming their index after an uptrend, they may feel the fear of missing out and increase their exposure. If they lose as much or more on the downside, they may tap out after the fact to avoid further losses.

An objective of absolute returns necessarily requires seeing, believing, and doing things differently as an independent thinker.

As investors seem to be taking on more risk, I see indications that stocks may be near a point of buying exhaustion. Keep in mind, these investor sentiment surveys are on a lag. It was probably this very optimism that pushed stocks to this higher level.

If there is enough enthusiasm left to keep driving prices higher, the uptrend will continue as long as optimism prevails. If instead these indicators and surveys are a signal of buying exhaustion, we’ll see prices fall at some point from here.

I focus on these extremes in investor sentiment.

So, it may be a good time to reduce or hedge off some risk.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.