Most investors, individual and institutional, apply some kind of asset allocation method to a portfolio mix of cash, bonds, and stocks. The most diversified also invest internationally, so their portfolio is global. The most common method is strategic asset allocation, which allocates capital to funds that represent different parts of the stock and bond markets based on some prediction of future exected returns or historical returns along with variance. There isn’t much skill to it unless you can predict the future better than others.

That’s Global Asset Allocation and it’s especially what large institutional investors like pensions and endowments do.

Since around 2002, most financial advisors have adopted it as well. I say 2002 because that was when I remember even the large Wall Street brokers like J.P. Morgan and Merrill Lynch starting to teach their financial advisors to use Modern Portfolio Theory to create Global Asset Allocation portfolios. Although in many cases, these investment brokers and banks don’t necessarily allow their brokerage salespeople to create their own models, instead, they sell models the firm creates. After all, financial advisors at a brokerage firm or investment bank aren’t analysts or portfolio managers, their job is to sell the firms’ products and services. So, most individual investors who have a financial advisor at a large brokerage firm probably find themselves in some kind of Global Asset Allocation.

In The stock market has made little progress in the past two years which is a hostile condition for trend following I pointed out the U.S. equity market has made little progress in the past two years. I also showed a simple example of how and why it’s a hostile condition for trend following methods.

The past two years haven’t been any better for allocation to global stocks and bonds, no matter how you sliced it.

To illustrate this observation, we use the S&P Target Risk Index Series. Below is the chart of all four “target risk” allocations between global stocks, bonds, and cash.

An index isn’t a physical basket of securities, but a mathematical construct that describes the market. So, we can’t invest directly in an index. But we can invest in securities like ETFs that track indexes and which provide exposure to the markets they reflect. In the case of S&P Target Risk, BlackRock iShares has ETFs that aim to track each of the four indexes.

The S&P Target Risk series of indices comprises multi asset class indices that correspond to a particular risk level. They measure risk level based on exposure to cash and bonds (for lower expected risk) to stocks for higher risk and expected return. So, the four indices each measure the performance of specific allocations to equities and fixed income. Each index has varying levels of exposure to equities and fixed income and are intended to represent stock and bond allocations across a risk spectrum from conservative to aggressive.

Something unique about these indices is each index is composed of exchange traded funds (ETFs), rather than an index allocation to other mathematical indices.

Again, the indices represent stock-bond allocations across a risk spectrum from conservative to aggressive. The assigned risk level of the index (conservative, moderate, growth, and aggressive) depends on the allocation to fixed income.

S&P Target Risk Conservative Index. The index seeks to emphasize exposure to fixed income, in order to produce a current income stream and avoid excessive volatility of returns. Equities are included to protect long-term purchasing power.

S&P Target Risk Moderate Index. The index seeks to provide significant exposure to fixed income, while also providing increased opportunity for capital growth through equities.

S&P Target Risk Growth Index. The index seeks to provide increased exposure to equities, while also using some fixed income exposure to dampen risk.

S&P Target Risk Aggressive Index. The index seeks to emphasize exposure to equities, maximizing opportunities for long-term capital accumulation.

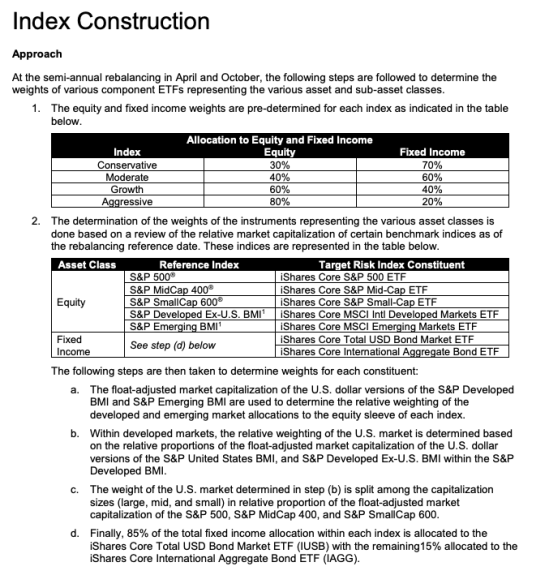

We can refer to Index Construction for details on each index’s allocation to equity and fixed income.

The short version is there is a 10% to 20% difference between the allocation between bonds and stocks.

So, how has Global Asset Allocation performed in this very volatile two years that’s had a hard time gaining enough momentum to stay at new highs?

S&P Target Risk Conservative Index. The index seeks to emphasize exposure to fixed income, in order to produce a current income stream and avoid excessive volatility of returns. Equities are included to protect long-term purchasing power.

Below is its return stream. Since it’s a relative return long-only fully exposed to the allocation all the time, I’m including the S&P 500 stock index just for reference. We can see the difference in the risk-reward profile for a conservative allocation. It’s bearly earned a gain the past two years at 2.29%.

For conservative investors, the downside avoidance was their main objective. We can see it in the % off high drawdown chart. At least for little return, it also experienced less downside, but at still had a drawdown of nearly -8%, so not exactly an asymmetric risk-reward over this short period.

Working our way toward more risk and expected return from a higher allocation of stocks, below is its return stream of the S&P Target Risk Moderate Index. The index seeks to provide significant exposure to fixed income, while also providing increased opportunity for capital growth through equities. Since it’s a relative return long-only fully exposed to the allocation all the time, I’m including the S&P 500 stock index just for reference. We can see the difference in the risk-reward profile.

The S&P Target Risk Moderate Index had more exposure to stocks than conservative, but it didn’t earn it a better return over the volatile period. However, with a drawdown of -10% compared to -20% for 100% stocks via the S&P 500, it’s “moderate” risk resulted in half the downside.

Continuing to work our way toward more risk and expected return from a higher allocation of stocks, below is its return stream of the S&P Target Risk Growth Index.

The S&P Target Risk Growth index seeks to provide increased exposure to equities, while also using some fixed income exposure to dampen risk. Here are the price trends.

The S&P Target Risk Growth allocation has earned 1.22% for a -13% drawdown.

S&P Target Risk Aggressive Index seeks to emphasize exposure to equities, maximizing opportunities for long-term capital accumulation.

The Aggressive allocation participated in the downside but not the upside.

Active management or tactical allocation isn’t the only method with “strategy risk” as sometimes asset allocation can get off track.

I don’t offer this kind of asset allocation that allocates capital to fixed buckets of stocks and bonds and then rebalances them periodically. As a tactical portfolio manager, instead of allocating to markets, I rotate between them based on asymmetric risk-reward. We don’t want to have too much exposure to falling markets and we prefer to focus on up trending markets. So, I prefer to limit my downside by predefining my risk and the upside takes care of itself as we let profits run. For me and our clients, our portfolio a replacement to this kind of asset allocation. Frankly, if I didn’t think I could achieve a better asymmetric risk-reward profile over full market cycles including drawdown control that we are better willing and able to tolerate, I wouldn’t bother doing what I do. If you can’t beat ’em, join ’em. But, from what I’ve seen so far, many investors in global asset allocation tapped out in the last bear market as both stocks and bonds experienced waterfall declines. Do you know what didn’t? cash and shorts.

To me, that’s tactical.

The bottom line is, all investments and investment strategies involve risk, including the potential loss of principal an investor must be willing to bear. Which one is right anyone is a function of their personal preferences toward someone actively making decisions or passively holding exposure to market risk, their risk tolerance for drawdowns, and their desire to pursue asymmetric risk-reward. None of it is a sure thing.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.