I pointed out yesterday the Stock market internals are signaling an inflection point. On a short term basis, some internal indicators are suggesting the stock market is at a point I expect to see a more significant breakout in one direction or another. That may sound like a symmetrical statement, but it’s the result of a symmetrical point that I consider midfield. From here, I look for signals of which direction the momentum shifts.

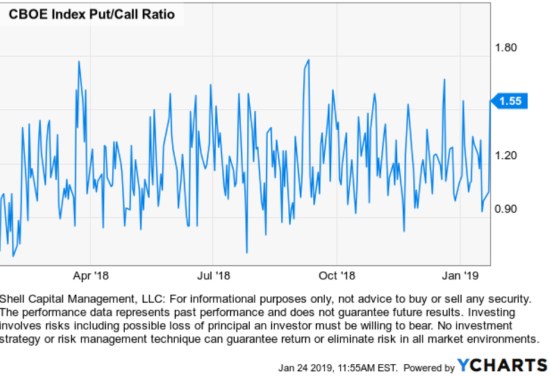

The asymmetry in the CBOE Index Put/Call Ratio suggests an increase in hedging yesterday. In the chart below, we see the Put/Call Ratio on Index options is at the high end of its range. I believe index options are used more for hedging by large institutions like hedge funds and pensions than for speculation by smaller individuals. I must not be the only one who recently hedged market risk.

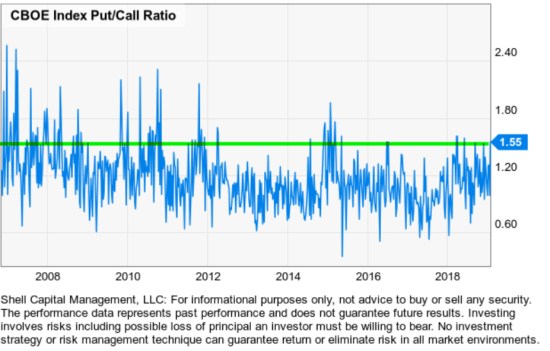

Looking back over the full history, we see the current asymmetry of 1.55 puts to calls is a level that shows the asymmetry is on the upper range. When it gets too extreme, it can signal an overly pessimistic position.

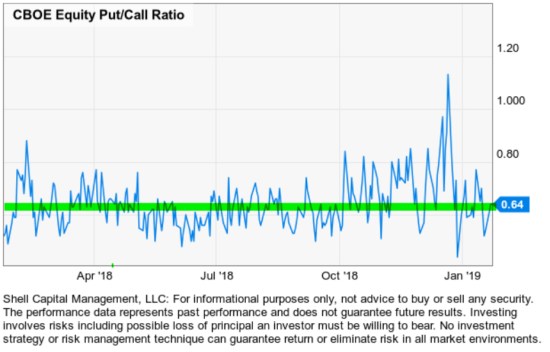

The CBOE Equity Put/Call Ratio which I believe is more of a measure of individual investor speculation remains at a normal level at this point. That is, we normally see the Equity Put/Call Ratio below 1 as it indicators more (speculative) call volume than put volume.

However, when the Equity Put/Call Ratio spiked up to an extreme in late December I thought it was a good indicator of panic. That turned out to be the case as it marked the low so far.

From here, I’m looking for signs of which direction the momentum is shifting. The CBOE Index Put/Call Ratio seems to suggest professional investors like me are more concerned about hedging against downside loss. They may be like me, setting on capital gains I prefer to hold (let the winners run!) so adding a hedge can help offset a loss of value. Yet, if we see a continuation up in the recent uptrend we simply take a smaller loss on the hedges that we can tax deduct.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

The observations shared on this website are for general information only and are not specific advice, research, or buy or sell recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. Use of this website is subject to its terms and conditions.

You must be logged in to post a comment.