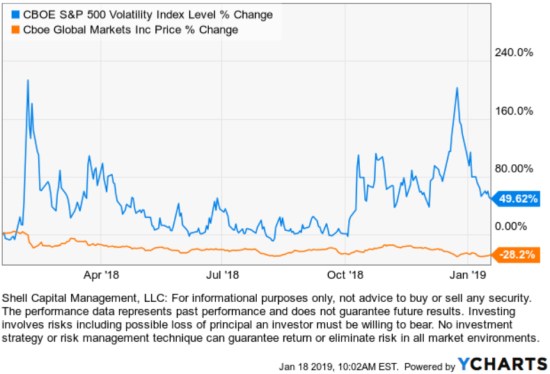

The CBOE VIX is settling down again after getting after it last year.

The VIX is designed to measure the 30-day expected volatility of the U.S. stock market, derived from real-time, mid-quote prices of S&P 500® Index call and put options.

The VIX Index is a measure of the market’s expectation of future volatility, so the market is pricing in less volatility from here.

VXV calculates based on a 3-month measure instead of VIX’s 1-month measure. The chart gives us an observation of term structure. Typically, we expect longer dated options like the 3-month to be higher than 1-month because they offer “insurance” for a more extended period. If the 1-month is higher than the 3-month, it means near term implied volatility has spiked, so the market is probably buying the protection of options. Right now the 1-month is lower than the 3-month, so the term structure is back to its normal contango.

By the way, anyone trading volatility or hedging with the VXX ETN should be aware that VXX is maturing on January 30th, 2019. Barclays has created a replacement with iPath® Series B S&P 500® VIX Short-Term FuturesTM ETN (VXXB).

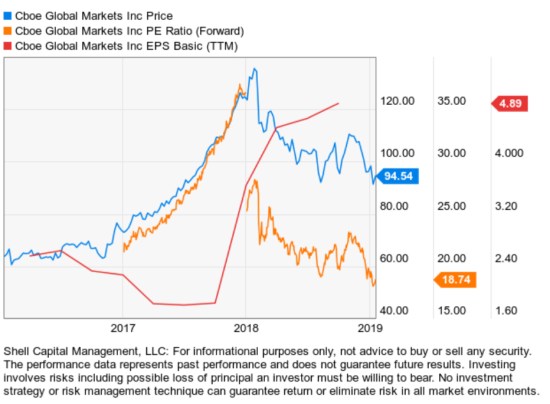

Speaking of CBOE, it will be interesting to see the outcome of the earnings report on February 8th and if the volatility last year improves their profitability. Blow is an interesting observation of the stock. The stock has declined -31% since its high last February. The orange line is the forward PE Ratio, with the stocks price over its earnings per share “predicted” by analysts. Keep in mind, analyst estimates are often wrong. Their expectations are no sure thing. The red line is the trailing 12 months earnings per share (EPS). The gap down in Forward P/E corresponding to the trailing twelve month EPS is an interesting observation.

The Forward P/E Ratio can signal analyst sentiment of a stock. If the forward P/E ratio is higher than the current P/E ratio, it indicates decreased expected earnings. A Forward P/E ratio less than the current P/E means expected increased earnings. Charting them below, it doesn’t appear the analyst are overly optimistic about the EPS report. But, what if they’re wrong?

We’ll soon learn if options and futures trading in VIX results in profits for CBOE in a volatility expansion. Over the past year, that hasn’t been the case, so maybe it’s time?

We’ll see.

Only time will tell if VIX implied volatility continues to contract and the CBOE stock trends up or down. But, if any company that should profit from directional movement up or down and a volatility expansion, it’s the CBOE. Analysts can get the CBOE stock wrong and the market can get the future volatility wrong,

Let’s see how it unfolds.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

The observations shared on this website are for general information only and are not specific advice, research, or buy or sell recommendations for any individual. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. Use of this website is subject to its terms and conditions.

Pingback: Feeling and Doing the Right Thing at the Right Time « ASYMMETRY® Observations