A hedge fund is really just a structure for running an investment program. It’s a business structure, usually a Limited Partnership, that operates like a business. It’s a “private investment partnership”. Its business is investing or trading. There are several good reasons for operating an investment program in a private investment partnership structure. For example, a global macro manager may have an edge constructing exposure to markets with options. Rather than risking money buying stock or a currency, we may gain a better risk/reward through a vertical spread. Many strategies are difficult to execute across multiple accounts, so they can’t effectively and efficiently be offered as separately managed accounts, so the LP structure is the better choice. And, even though some strategies can be implemented in a mutual fund, a mutual fund is far more expensive to operate and administer to make them available to the general public. So if a manager aims to only offer a strategy to a fewer number of investors, he ends up managing what is commonly called a “hedge fund”. There are all kinds of strategies operated in that format, so it’s really just industry jargon. The term “hedge fund” is just slang for a “private investment partnership that isn’t offered to everyone”. Beyond that, here is a great primer for hedge funds:

Interest Rate Trend

In Interest Rates are Trending Up, Bonds Investors Feeling the Pain we looked at the trend in interest rates and bond prices going back 15 years. For a more macro view of just how low interest rates are historically, below we view rates going back to 1962. It shows how low rates have been, but also gives historical precedent as to how high they could go…

source: dshort.com

How’s the market doing?

At lunch someone asked me “How’s the market doing this month?”

Which market? And, why does a month matter?

He probably meant the “stock market” because that’s what people know about, but there are many different markets and we can get long or short any of them.

source: FINVIZ

The role of shorting, firm size, and time on market anomalies

There are now more than 300 published papers providing evidence of the persistence of price trends (inertia/momentum). We point out the constant flow of new papers adding to the evidence of relative price strength as a market inefficiency (often called a market anomaly by academics). I call it velocity.

Abstract

We examine the role of shorting, firm size, and time on the profitability of size, value, and momentum strategies. We find that long positions make up almost all of size, 60% of value, and half of momentum profits. Shorting becomes less important for momentum and more important for value as firm size decreases. The value premium decreases with firm size and is weak among the largest stocks. Momentum profits, however, exhibit no reliable relation with size. These effects are robust over 86 years of US equity data and almost 40 years of data across four international equity markets and five asset classes. Variation over time and across markets of these effects is consistent with random chance. We find little evidence that size, value, and momentum returns are significantly affected by changes in trading costs or institutional and hedge fund ownership over time.

They find the momentum premium exists and is stable across all size groups and the entire 86-year period—it was persistent in all four 20-year periods examined, including the most recent two decades that followed the initial publication of the original momentum studies.

Source:

The role of shorting, firm size, and time on market anomalies Journal of Financial Economics, Volume 108, Issue 2, May 2013, Pages 275-301

Ronen Israel, Tobias J. Moskowitz

Interest Rates are Trending Up, Bonds Investors Feeling the Pain

First, we view 15 Year Chart of the 10 Year U.S. Treasury Note Yield (interest rate) (Symbol: $TNX). Keep in mind this chart reflects the rate of change in the interest rate, not the price trend. If we define a downtrend as “lower highs, lower lows” the 15 year trend for interest rates has been down. But since 2012, the trend has sharply turned up – though that isn’t the first time.

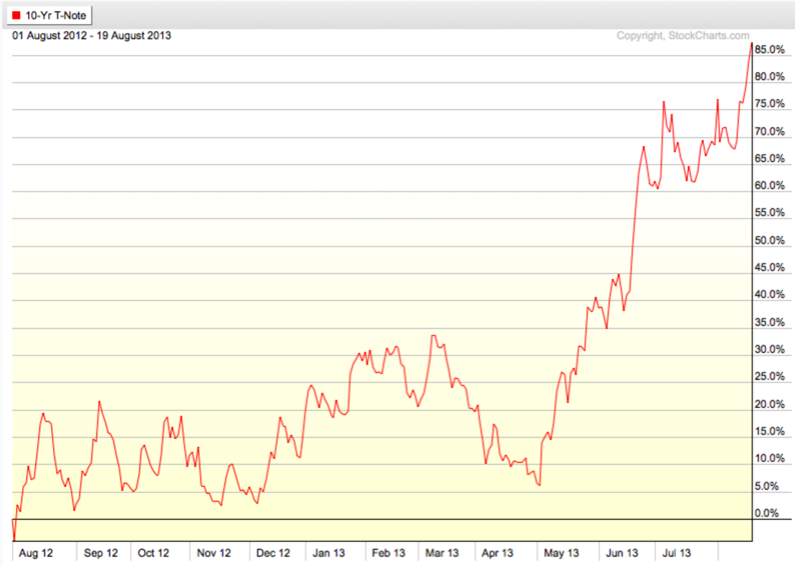

Next, we zoom in t0 view the magnitude of the interest rate on the 10 Year U.S. Treasury Note Yield since its low a year ago in August 2012. The interest rate on the 10 year treasury has gained 85%. The current yield is about 2.88%.

Next we look at the long term U.S. Treasury Bond Yield – the 30 year. Long terms rates have been in a downtrend the last 15 years, but have recently trended up sharply.

Understanding the implications of a reversal in the trend of interest rates is critical to a global macro fund manager. A large part of my global tactical decisions is identifying direction trend changes. and understanding how markets interact with each other. For example, we can see below how rising rates significantly impact the price value of bonds.

Below, we observe the total return (price trend + interest) of a wide range of different styles of bond ETFs.

- iShares Barclays 20+ Year Treasury Bond (TLT)

- iShares Core Total US Bond Market ETF (AGG)

- iShares S&P National AMT-Free Municipal Bond (MUB)

- iShares Barclays TIPS Bond (TIP)

Clearly, they have recently been in a downtrend with U.S. Government bonds down the most at -13.65% over the past year.

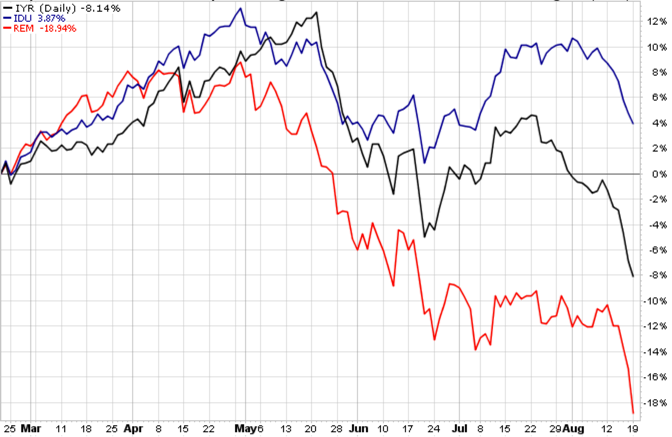

Finally, we observe some markets and sectors that are very sensitive to changes in interest rates.

- iShares Mortgage Real Estate (REM): provides exposure to U.S. residential and commercial mortgage real estate investment trusts (REITs), which trade like stocks and invest in real estate directly

- iShares U.S. Real Estate (IYR): exposure to U.S. real estate stocks and real estate investment trusts (REITs), which trade like stocks and invest in real estate directly.

- iShares U.S. Utilities: exposure to U.S. utilities stocks.

Eventually the Federal Reserve will stop their “Quantitative Easing” program of buying bonds. You know how supply and demand works: when demand dries up, price goes down…

Interest In Tactical Asset Allocation Grows Among ERISA Plans

According to a new white paper from The Center for Due Diligence “TACTICAL ASSET ALLOCATION & ERISA PLANS: Best Practices for Finding the Right Strategy for Plan Participants“:

Looking for ways to stabilize returns and manage downside risk, the interest in Tactical Asset Allocation (TAA) strategies has increased. This was initially driven by the 2008 financial crisis, where diversification of asset classes did not provide participants with downside protection. Fueled by concerns over a transitioning monetary policy and asset class repricing, today’s equity market valuations, changing interest rate environment and a better understanding of participant risk tolerance has further increased interest in TAA. This trend could impact the rosy projections for target-date funds and the market share held by the dominant providers.

Given today’s investment dynamics – heightened risk for equities as well as bonds – astute investment advisors are increasingly questioning the prudence of modern portfolio theory. The DOL’s recent Tips for ERISA Plan Fiduciaries may also have sparked the desire for more oversight through custom solutions.

While somewhat limited in application, many proprietary target date fund managers already use a tactical overlay. Until now, there was very little guidance for plan fiduciaries to help them understand the different types of core TAA strategies, let alone evaluate the suitability of a particular strategy for their individual plans.

Separating analytically disciplined TAA strategies from high risk “market timing” type strategies, the CFDD’s exclusive white paper on Tactical Asset Allocation & ERISA Plans will become an invaluable resource for plan sponsors, investment advisors and product manufacturers considering TAA strategies. It will also spearhead the need for tactical transparency and accountability.

TAA contemplates dynamic changes based on current conditions. In addition to requiring special skills and being more complex than traditional approaches, TAA managers may have different goals and trigger methodology. Offered in conjunction with the Wagner Law Group – one of the nation’s most prestigious ERISA law firms – the white paper provides a conceptual overview of legal standards, core fiduciary principles and QDIA applications that will benefit both the experienced and those considering tactical strategies for the first time.

In addition to providing the analytic framework for evaluation, the white paper includes a checklist of best practices and key considerations for plan fiduciaries considering TAA strategies. Moving beyond the marketing hype, the white paper empowers plan fiduciaries with the knowledge to understand/evaluate TAA strategies and ask the right questions. It also paints a realistic picture of the rewards, risks and limitations of these wide ranging strategies.

The Little Book of Hedge Funds by Anthony Scaramucci

I read The Little Book of Hedge Funds over a weekend. It’s an easy read and an excellent choice if you want to get a good overall understanding of hedge funds and the general industry of hedge fund management, selection, or absolute return strategies in general. It doesn’t get into detailed strategies, but instead a high level overview of the pursuit of asymmetric returns. My favorite part of the book was Anthony’s section on selection of hedge fund portfolio managers and how he defines “pedigree”. As he puts it (pp. 149-150):

“To make a long story short, the investment research and due diligence process is focused on determining or not a manager can: Generate attractive absolute and relative returns. Manage risk. Produce uncorrelated returns, with relatively attractive liquidity. Evolve as market conditions evolve. Perhaps most important, we have to understand how they will behave when the shit hits the fan in market debacles like LTCM, September 11th, the summer of 2002, 2008, the European financial crisis, and so on.”

He goes on to say he breaks the manager selection process into two categories. The first is Pedigree (pp. 150-151):

Pedigree:

“Pedigree is an all-encompassing term we use to assess whether a manager possesses the right experience and skill to execute a particular strategy in a particular market environment. Typically, an investor should strive to find a manager with many years of real “buy-side experience,” that is, the manager should have actually managed a reasonable amount of capital over a reasonable period of time. The exception to this rule is a new, cutting-edge manager who is implementing strategies that may not have existed three years ago. You would be surprised at how many hedge funds fail the basic “experience” test. For instance, if a manager’s only prior experience is that he was a fixed-income salesman, you could undoubtedly find someone with more relevant experience and skills. For whatever reason, a lot of hedge fund investors tend to be drawn like moths to a flame to big-name sell-side guys who come out and launch a new hedge fund. A general rule of thumb: Avoid these guys like the plague as history has shown that they tend to always fail. After all, managing capital for private investors is completely different from running market making/prop trading outfits. Pedigree also includes a manager’s temperament and qualitative judgment. Is he a loose cannon or thoughtful and deliberative? Has he experienced personal and professional setbacks in his career and how has he responded? Has he treated his investor capital with prudence or has he viewed it as a tool to make a name for himself and get rich quick? Answering these questions takes a lot of work. But, if you want to invest with a hedge fund manager you have to be willing to roll up your sleeves and analyze that manager’s pedigree.”

I thought his explanation of pedigree is outstanding. He points out that pedigree is more about a persons actual experience and skill as evidenced by track record rather than the things we would see on a resume like college alumni, GPA, and places they’ve worked. It shows Anthony Scaramucci is the real deal. That is especially true because Anthony himself is a Harvard MBA graduate and began his career at Goldman Sachs before staring his own firm. Getting in and out of Harvard’s MBA program and landing a job at Goldman is an accomplishment, but says nothing about ability to manage money. A portfolio managers pedigree is about executing with an edge and is evidenced by a track record.

The Little Book of Hedge Funds description from Amazon:

The Little Book of Hedge Funds that’s big on explanations even the casual investor can use. An accessible overview of hedge funds, from their historical origin, to their perceived effect on the global economy, to why individual investors should understand how they work, The Little Book of Hedge Funds is essential reading for anyone seeking the tools and information needed to invest in this lucrative yet mysterious world. Authored by wealth management expert Anthony Scaramucci, and providing a comprehensive overview of this shadowy corner of high finance, the book is written in a straightforward and entertaining style. Packed with introspective commentary, highly applicable advice, and engaging anecdotes, this Little Book:

- Explains why the future of hedge funds lies in their ability to provide greater transparency and access in order to attract investors currently put off because they do not understand how they work

- Shows that hedge funds have grown in both size and importance in the investment community and why individual investors need to be aware of their activities

- Demystifies hedge fund myths, by analyzing the infamous 2 and 20 performance fee and addressing claims that there is an increased risk in investing in hedge funds

- Explores a variety of financial instruments—including leverage, short selling and hedging—that hedge funds use to reduce risk, enhance returns, and minimize correlation with equity and bond markets

Written to provide novice investors, experienced financiers, and financial institutions with the tools and information needed to invest in hedge funds, this book is a must read for anyone with outstanding questions about this key part of the twenty-first century economy.

The essence of investment management is the management of risks…

“The essence of investment management is the management of risks, not the management of returns.”

– Benjamin Graham

The problem is many portfolio managers believe they manage risk through their investment selection. That is, they believe their rotation from one seemingly risky position to another they believe is less risk is a reduction of risk. But, risk is the exposure to the chance of a loss. The exposure is still there. Only the perception has changed: they just believe their risk is less. For example, for the last thirty years, the primary price trend for bonds has been up because interest rates have been falling. If a portfolio manager shifts from stocks to bonds when stocks are falling, bonds were often rising. It appears that trend may be changing. Portfolio managers who have relied on bonds as their safe haven may rotate out of stocks into bonds and then their bonds lose money too. That’s not risk management.

They don’t know in advance if the position they rotate to will actually result in a lower possibility of loss. Prior to 2008, American International Group (AIG) carried the highest rating for an insurance company. What if you rotated to AIG? Or to any of the other banks. Many investors believed those banks were great values as their prices were falling. They just fell more. It has taken them a long time to recover some of their losses. Just like tech and telecom stocks in 2000.

All risks cannot be hedged away if you pursue a gain. If you leave no chance at all for a potential profit, you earn nothing for that certainty. Risk is exposure to an unknown outcome that could result in a loss. If there is no exposure or uncertainty, there is no risk. The only way to manage risk is to increase and decrease the exposure to loss. That means buying and selling or hedging. When you hear someone speaking otherwise, they are not speaking of active risk management. For example, asset allocation and Modern Portfolio Theory is not active risk management. The exposure to loss remains. They just shift their risk to more things. But they can all fall together, as they do in real bear markets.

It’s required to accomplish what the family office Chief Investment Officer said in “What a family office looks for in a hedge fund portfolio manager” when he said:

“I like analogies. And one of the analogies in 2008 brings to me it’s like a sailor setting his course on a sea. He’s got a great sonar system, he’s got great maps and charts and he’s perhaps got a great GPS so he knows exactly where he is. He knows what’s ahead of him in the ocean but his heads down and he’s not seeing these awesomely black storm clouds building up on the horizon are about to come over top of him. Some of those managers we did not stay with. Managers who saw that, who changed course, trimmed their exposure, or sailed to safer territory. One, they survived; they truly preserved capital in difficult times and my benchmark for preserving capital is you had less than a double-digit loss in 08, you get to claim you preserved capital. I’ve heard people who’ve lost as much as 25% of investor capital argue that they preserved capital… but I don’t believe you can claim that. Understanding how a manager managed and was nimble during a period of time it gives me great comfort, a higher level of comfort, on what a manager may do in the next difficult period. So again it’s a it’s a very qualitative sort of trying to come to an understanding of what happened… and then make our best guess what we anticipate may happen next time.”

I made bold the relevant points.

If you are like-minded and believe what we believe, contact us.

Option Pricing Asymmetry: The Lack of Symmetry

A theory is a generalized explanation of how things work. For example, I apply a scientific process for quantitative investment research and that quantitative research can either be data-driven or theory-driven. Theory-driven research starts with a theory about how I something works or if a thing will work (or not). For example, we may theorize that buying a stock, ETF, commodity, or currency that is rising over the past six months may continue to rise and result in higher profits than buying securities that are falling. The is a belief in momentum and intertia. At that point, it’s just a theory – a belief. Theories aren’t necessarily true. But if you believe it, it’s probably true for you. A data-driven approach starts with testing all kinds of systems and methods to determine what works and what doesn’t and it doesn’t start with a theory, but instead a study of the data. Most of testing I’ve done was data-driven because I was trying to create a certain result through the process of buying and selling. I really don’t believe I need a good story to back it: if it works it works and proving that mathematically is good enough. As it turns out, doing original research without the biases of beliefs and theories may have been an edge. Of course, we can confirm, prove, or disprove our theories through data studies. People prefer a good story behind a good system. To have that illusion of some firm foundation behind why something works is probably better than not having one. I digress. I was thinking of that as I read over the below paper on options pricing theory. You see, the theories of how options are priced is a theory- a general explanation of why the premium is what it is. Option pricing is one the most researched theories. I thought the following paper titled “Option Pricing Asymmetry” was interesting. It doesn’t surprise me there is some asymmetry in options pricing.

Option Pricing Asymmetry by Dallas Brozik, Marshall University

Introduction:

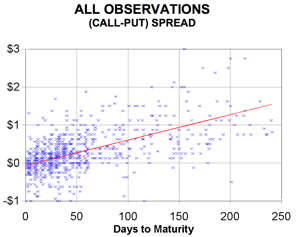

“Option pricing is one of the most researched areas of finance. Several different option pricing models have been developed, each with its own strengths and weaknesses. One characteristic of these models is that call options and put options are treated as opposites by the pricing model. While such a result might be intuitively appealing, there is no a priori reason to believe that market participants price these contracts in an identical but opposite manner. Option prices reflect the behavior of the market participants, and if there is a significant difference between the behavior of the buyers/sellers of call options and the buyers/sellers of put options, then any option pricing model will need to reflect this difference in the pricing of the different contracts.”

In summary, he finds that:

“The markets for call options and put options may be similar, but they are not identical. The pricing models for calls and puts are not mirror images. This lack of symmetry between call and put pricing implies that hypothesized relationships like put/call parity may be inaccurate and that models based on these hypothesized relationships will need to be revisited. One aspect of the difference appears to be that call and put options do not value time in the same way. In addition to any cost of capital assumed by the underlying pricing model, there is an additional time factor that causes the spread between call and put option prices to increase with time. No mechanism is suggested for this difference, but it is there. This is an area for future research.”

Source: Option Pricing Asymmetry (click to read the full paper)

How a Family Office Selects an Investment Manager

The topic of selecting an investment manager is an important one. Many investors, including professional financial planners and advisors admit they have little skill at selecting asset managers. In fact, some admit they do such a poor job at it they don’t even try. But if you understand the value in alternative investment strategies from private equity to absolute return focused investment programs, then you need to know what to look for in an investment manager. These alternative investment strategies are most often offered privately in a private hedge fund format and sometimes offered as a separate managed account (SMA). Whether you are a private individual investor, an allocator for a family office or institution, or a portfolio manager, the video below is an outstanding example of how a sophisticated investor analyzes a money manager. It’s an interview with the Chief Investment Officer of a family office. He explains why a family who sold a large business may be interested in alternative investments or alternative investment strategies rather than conventional public investments and investment programs like mutual funds. His family office has allocated 80% to alternative investment managers (like hedge funds and the Asymmetry Investment Program™). He offers some insight about:

- Why family offices (and other wealthy investors) are attracted to alternative investment strategies commonly offered as a private hedge fund.

- What they specifically look for in selecting a portfolio manager.

- How allocators filter managers post crisis: What exactly did you do in 2008?

- Are they looking at younger emerging hedge fund/money managers?

On how they select hedge funds: (begins around 4:07/9:57)

“We are looking for opportunities with managers were we can get comfortable as to their strategy and what will generate returns for them and what the risks might be? We haven’t been very active with emerging or start-up managers. I think a lot of that has to do with where we are in terms of time.

2008 was an awesome and an awful market experience it’s helpful to look at managers who actually were in existence during that period of time to gain some understanding of how they manage their portfolios are the most difficult. Someone doesn’t have a 08 track record is much harder to get a sense of how they’re going to do a difficult markets. 09 was a pretty easy market to make money if you were long.”

How are you evaluating the 2008 period what are you looking at specifically, the drawdown?

“We obviously start with performance but I also want to see exposure in the portfolio. How did the manager navigate those markets? Did he keep his portfolio fully invested in a market environment for his strategy was not allowing it to make money was actually causing losses? Did he trim exposure? When did he put exposure back into the market place? is something that we look at it. It’s really it’s a number of different factors we try and I can understand how the manager managed during that period of time and try to gain some insight on his style. Conviction doesn’t automatically mean that you stay fully invested at all times. Although we certainly saw a number of managers who waited FAR too long to trim their exposure. So, it’s a combination of all those factors we try and consider. But I would say one of the things that are most important to me is trying to follow a managers gross and net exposures during that period trying to understand. That leads to conversations of what the manager was thinking at the time.”

He goes on to say:

“I like analogies. And one of the analogies in 2008 brings to me it’s like a sailor setting his course on a sea. He’s got a great sonar system, he’s got great maps and charts and he’s perhaps got a great GPS so he knows exactly where he is. He knows what’s ahead of him in the ocean but his heads down and he’s not seeing these awesomely black storm clouds building up on the horizon are about to come over top of him. Some of those managers we did not stay with. Managers who saw that, who changed course, trimmed their exposure, or sailed to safer territory. One, they survived; they truly preserved capital in difficult times and my benchmark for preserving capital is you had less than a double-digit loss in 08, you get to claim you preserved capital. I’ve heard people who’ve lost as much is 25% of investor capital argue that they preserved capital… but I don’t believe you can claim that. Understanding how a manager managed and was nimble during a period of time it gives me great comfort, a higher level of comfort, on what a manager may do in the next difficult period. So again it’s a it’s a very qualitative sort of trying to come to an understanding of what happened… and then make our best guess what we anticipate may happen next time.”

I can tell you he’s spot on. Those whose jobs are that of the asset allocator, who allocates capital to investment programs, often rely too much on Modern Portfolio Theory statistics and not enough on looking very closely under the hood. As a quantitative trading system developer and operator, we are focusing on far different things and I can tell you: it’s the things that matter. It’s critical that the investor or allocator take a close look at the downside: how was their drawdown from peak to trough? What were the actual holdings during that time? Like he said: do they stay in the market even when it’s not working for them? Or, do they reduce their exposure to the possibility of loss (risk management) by selling positions or dynamic hedging?

I very much agree with his comments about experience. Today there are many people selling hypothetical backtests who have no real experience executing during difficult conditions. After such a radical waterfall occurred in 2008 – 2009, more investors and professionals have now figured out the state of the market. In a secular bear market, such waterfalls occur and it can happen again. After the fact, many investment professionals have scrambled to come up with solutions and naturally they’ll be attracted to what actually worked in the past: like some forms of Global Tactical Asset Allocation, Trend Following, and other so-called “alternative” investment strategies like we run. We now have new people interested in active portfolio management that seek an absolute return, rather than a relative return. But like he said: they lack the actual experience. You really don’t know how they’ll react in the heat of the battle. But you can be assured of this: back-testing a system is one thing, and executing is another.

Click below to view:

Family Office Management, Investment Management, Hedge Funds, Absolute Returns, Active Risk Management

www.AsymmetryObservations.com

![]()

After a year hiatus, I am pleased to introduce my new blog. My prior site, Asymmetric Investment Returns, had an average readership of over 4,000 a day. ASYMMETRY® Observations is my observations about alternative investment strategies and global trend observations aimed at creating asymmetric returns; more of the profits we want, less of the downside we prefer to avoid. http://www.AsymmetryObservations.com

{kind=link}

You must be logged in to post a comment.