A theory is a generalized explanation of how things work. For example, I apply a scientific process for quantitative investment research and that quantitative research can either be data-driven or theory-driven. Theory-driven research starts with a theory about how I something works or if a thing will work (or not). For example, we may theorize that buying a stock, ETF, commodity, or currency that is rising over the past six months may continue to rise and result in higher profits than buying securities that are falling. The is a belief in momentum and intertia. At that point, it’s just a theory – a belief. Theories aren’t necessarily true. But if you believe it, it’s probably true for you. A data-driven approach starts with testing all kinds of systems and methods to determine what works and what doesn’t and it doesn’t start with a theory, but instead a study of the data. Most of testing I’ve done was data-driven because I was trying to create a certain result through the process of buying and selling. I really don’t believe I need a good story to back it: if it works it works and proving that mathematically is good enough. As it turns out, doing original research without the biases of beliefs and theories may have been an edge. Of course, we can confirm, prove, or disprove our theories through data studies. People prefer a good story behind a good system. To have that illusion of some firm foundation behind why something works is probably better than not having one. I digress. I was thinking of that as I read over the below paper on options pricing theory. You see, the theories of how options are priced is a theory- a general explanation of why the premium is what it is. Option pricing is one the most researched theories. I thought the following paper titled “Option Pricing Asymmetry” was interesting. It doesn’t surprise me there is some asymmetry in options pricing.

Option Pricing Asymmetry by Dallas Brozik, Marshall University

Introduction:

“Option pricing is one of the most researched areas of finance. Several different option pricing models have been developed, each with its own strengths and weaknesses. One characteristic of these models is that call options and put options are treated as opposites by the pricing model. While such a result might be intuitively appealing, there is no a priori reason to believe that market participants price these contracts in an identical but opposite manner. Option prices reflect the behavior of the market participants, and if there is a significant difference between the behavior of the buyers/sellers of call options and the buyers/sellers of put options, then any option pricing model will need to reflect this difference in the pricing of the different contracts.”

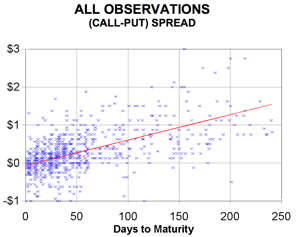

“The markets for call options and put options may be similar, but they are not identical. The pricing models for calls and puts are not mirror images. This lack of symmetry between call and put pricing implies that hypothesized relationships like put/call parity may be inaccurate and that models based on these hypothesized relationships will need to be revisited. One aspect of the difference appears to be that call and put options do not value time in the same way. In addition to any cost of capital assumed by the underlying pricing model, there is an additional time factor that causes the spread between call and put option prices to increase with time. No mechanism is suggested for this difference, but it is there. This is an area for future research.”

You must be logged in to post a comment.