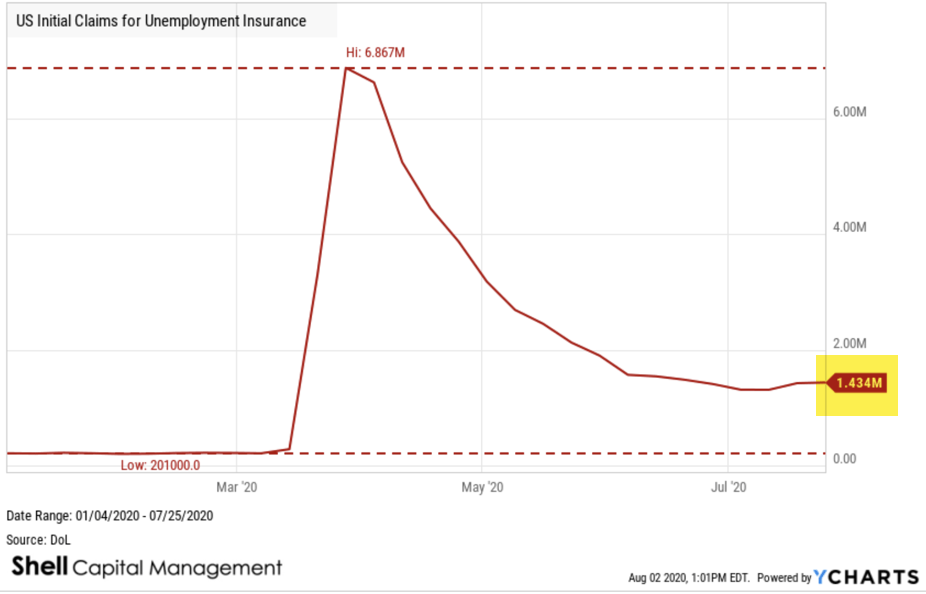

US Initial Jobless Claims, provided by the US Department of Labor, provides underlying data on how many new people have filed for unemployment benefits in the previous week.

We can gauge economic conditions with respect to employment.

As more new individuals file for unemployment benefits, fewer individuals in the economy have jobs.

For example, initial jobless claims have tended to reach a cycle peak at the end of recessionary periods. For example, near the end of the last recession, on March 21, 2009 there were 661,000 new filings.

US Initial Claims for Unemployment Insurance is at a current level of US Initial Claims for Unemployment Insurance is at a current level of 1.434 million, which is an increase 592.8% from one year ago.

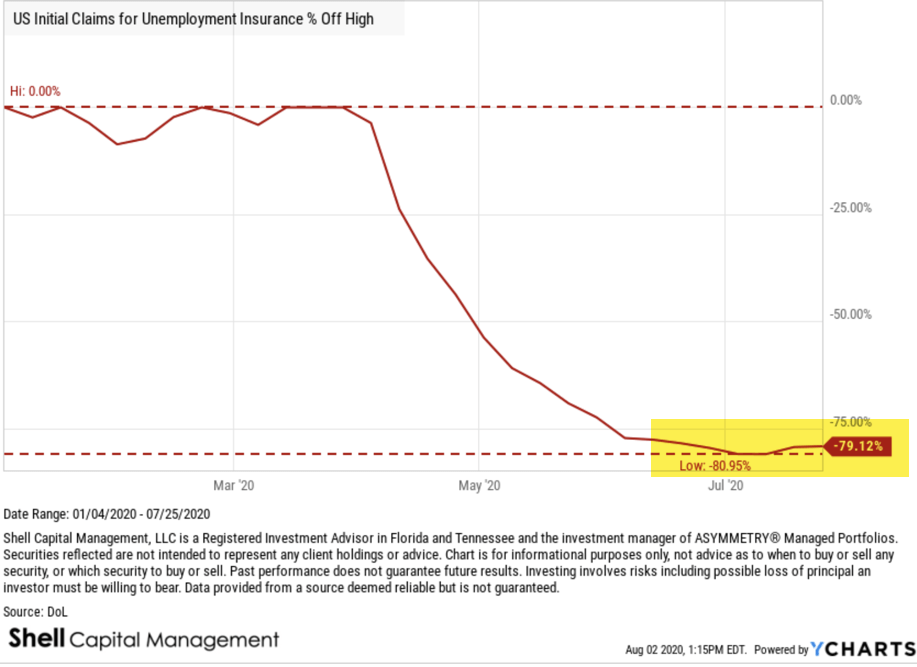

But, if it makes you feel any better, US Initial Claims for Unemployment Insurance are down -79% from its March 2020 high.

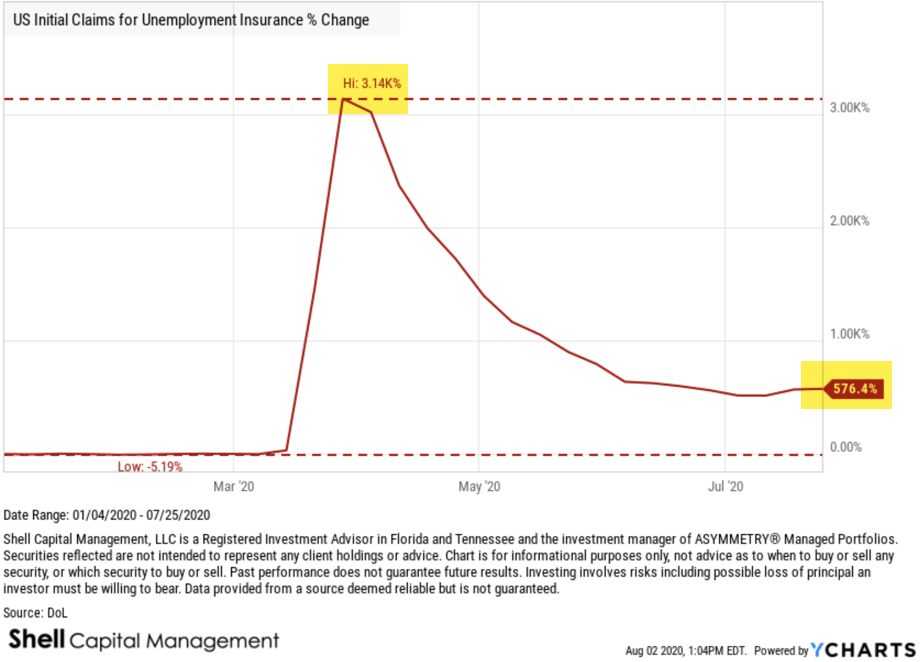

So, US Initial Claims for Unemployment Insurance is up 576% from the beginning of 2020, though it was up over 3,000% in March.

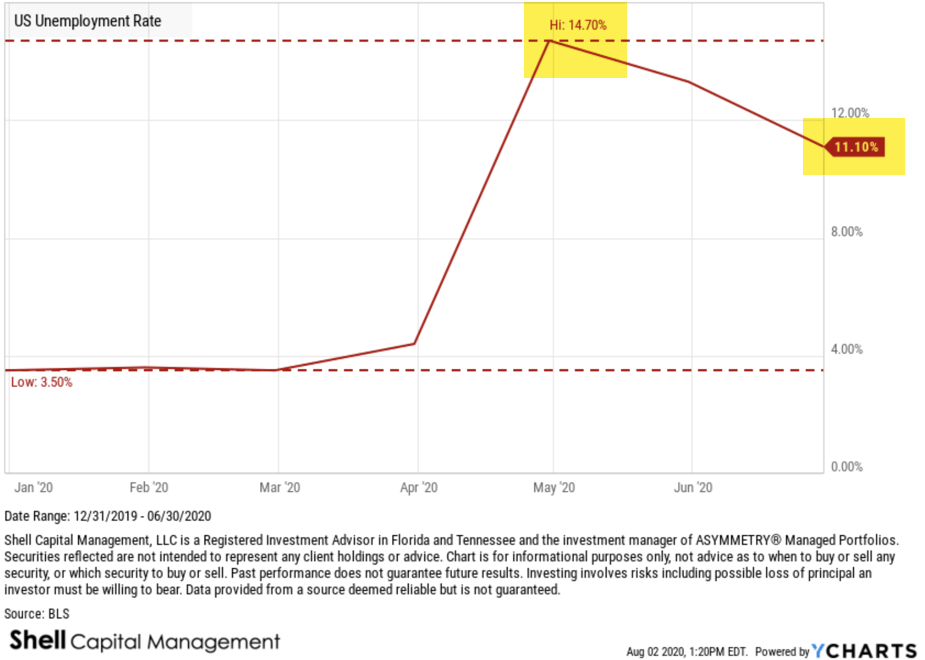

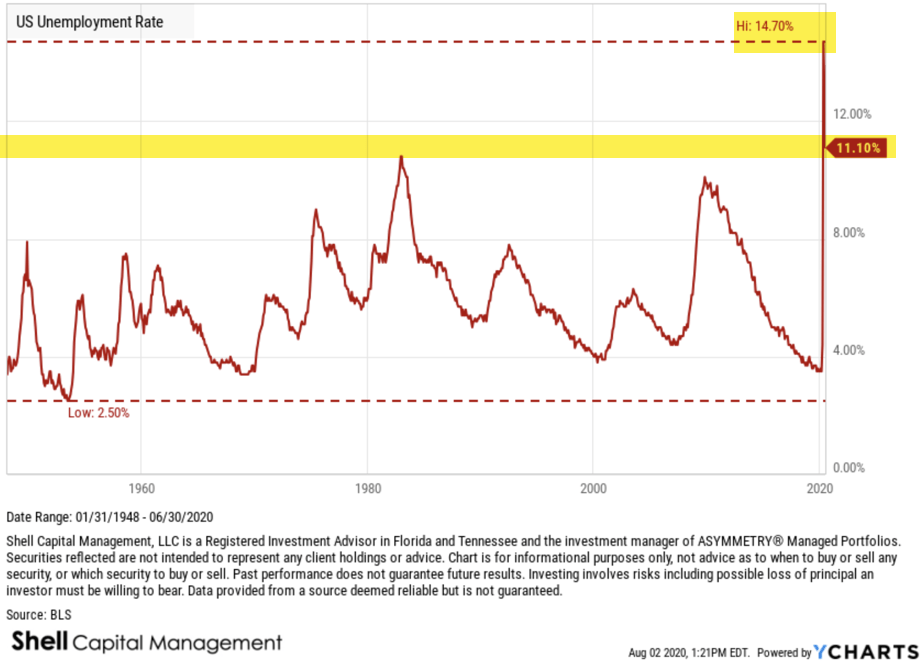

The US Unemployment Rate measures the percentage of total employees in the United States that are a part of the labor force, but are without a job.

The US Unemployment Rate is one of the most widely followed indicators of the health of the US labor market and the US economy as a whole.

Historically, the US Unemployment Rate has reached as high as 10.80% in 1982 and 9.9% in November of 2009.

Both periods were significant recessionary periods.

US Unemployment Rate is at 11.10%, compared to 13.30% last month and 3.70% last year. It is much higher than the long term average of 5.75%.

The US Unemployment Rate at 14.7% was by far the highest it has been in 72 years according the the Bureau of Labor Statistics.

At 11.10% the US Unemployment Rate is still higher than the prior peak in 1982.

I know most people were shocked by this spike in unemployment, and of course, much of it was driven by the Coronavirus pandemic, but it’s also just the market, doing what it does.

For example, I shared in an observation here on December 29, 2019 in “Asymmetry in yield spreads, inverted yield curve warning shot, and unemployment” when I shared the following in regard to what was then an extremely low unemployment rate.

“The yield curve inversion doesn’t automatically mean a recession is in the near future.

Employment is essential, too. The U.S. Unemployment Rate is about as low as it’s ever been.”

“As with all cycles, it isn’t the extremely low level of the cycle we should focus on, but what’s more likely to happen next. It should be no surprise that low unemployment precedes recessions.”

But, I’ll close this observation with the same one I did this one last December.

For me, the directional trend of the stock market will be my primary guide for the economy but I monitor many trends for situational awareness of what is going on.

I hope all is well with all of you and you are avoiding COVID-19 like the plague.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.