People don’t usually invest all their money in equities, even though the stock market is mostly what we talk about. Large institutional investors like pensions and endowments don’t invest all their capital in the stock market, either. Instead, they invest in allocation to stocks and bonds globally diversified across world markets.

One of my favorite examples of the stock and bond part of this global asset allocation is the S&P Dow Jones Indices’ Target Risk index series.

S&P Dow Jones Indices’ Target Risk series comprises multi-asset class indices that correspond to a particular risk level. Each index is fully investable, with varying levels of exposure to equities and fixed income and are intended to represent stock and bond allocations across a risk spectrum from conservative to aggressive.

For example, after a positive year for stocks and bonds, most investors will pay more attention to the one that gained the most. After stocks outperform bonds, the best gains are naturally going to be the global allocation that held the most stock exposure.

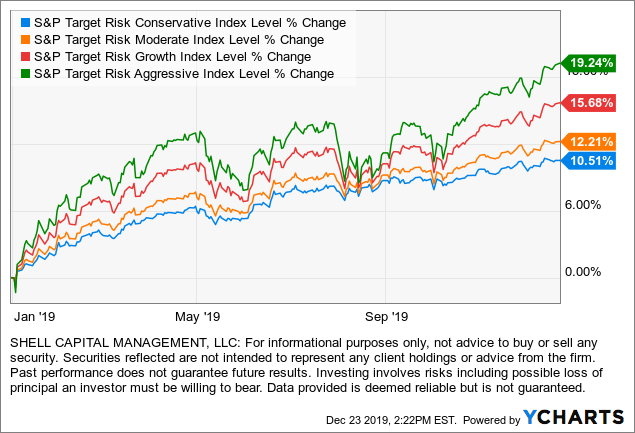

The S&P Target Risk Aggressive® Index is one of four multi-asset class indices that compose the S&P Target Risk Series. The S&P Target Risk Aggressive Index emphasizes exposure to equities, maximizing opportunities for long-term capital accumulation. It may include small allocations to fixed income to enhance portfolio efficiency. In a positive year like 2019, it was the clear winner on the upside. The aggressive allocation gained 19% so far in 2019. On the other end of the spectrum, even the conservative allocation gained 10%.

But, risk isn’t a knob.

Asset allocators don’t get to dial it up or down, and it always work out the way they want.

The reward isn’t a knob, either.

Just because a portfolio is dialed up with risk to “aggressive” doesn’t mean you get the reward from it.

That’s especially true in the short term. Had you believed risk and reward is a knob you turn to get what you want in January a year ago, you could have experienced the aggressive allocation resulted in the more aggressive loss.

The conservative model lost the least, but that isn’t a sure thing, either. In global asset allocation, conservative means more allocation to bonds for fixed income. If bonds fall and stocks rise, the conservative model could lose money and the more stock weighted aggressive could gain.

Diversification is often presented by advisors as a risk management strategy that mixes a wide variety of investments within a portfolio. But, diversification does not assure a profit or protect against loss. The outcome of asset allocation is driven by the exposure to stocks vs. bonds and their gain and loss.

That’s not what I do.

A global asset allocation of exposures that otherwise remain static is very different from dynamic exposures that change based on asymmetric risk-reward driving tactical decisions.

My outcome is decided by my tactical increase and decreases in exposure to risk-reward as I focus on asymmetric risk-reward. I believe there is a time for offense and a time for defense.

But, for everyone else, there’s global asset allocation. It’s what most people do. They allocate capital, I rotate capital. I rotate, rather than allocate.

If I were going to invest in static, long-only, fully invested all the time global asset allocation, it would look like these S&P Target Risk indexes. When it comes to a simple allocation of capital, who’s going to do it better than S&P? Many advisors are charging their clients 0.50% to 1% for a simple asset allocation like this. I personally believe the risk of a disaster is so high it makes the unmanaged risk imprudent, so we don’t offer fixed, long-only, fully invested all the time global asset allocation at Shell Capital. If we did, we’d probably manage billions because investors want “market returns” until they are big losses. We could also spend our time selling instead of analyzing. But we would constantly be apologizing for market behavior instead of embracing up and downtrends. In my opinion, it’s a difficult business model, but it’s still the easiest for financial advisors. They allocate to the funds, rebalance routinely, maybe do some tax-loss harvesting, and write a commentary about what the market did that lead to their results. Admittedly, it’s a lot easier than tactical portfolio management. When the market doesn’t do what they wanted, it’s the market’s fault. In 2008, they said let’s “hunker down.”

From my perspective, the investment advisory firms with the largest assets under management tend to be asset allocation firms. They advise clients to invest in global asset allocation models similar to these. Since they aren’t doing constant research and making tactical trading decisions, their time is freed up for the golf course, where they meet more and more clients.

Why do I think it’s a challenging advisory business model?

Global asset allocation doesn’t give me what I want, nor does it give our clients what they want. We want active risk management. We want a point in which we’ll reduce our exposure to loss and maybe even reverse it so as prices fall we profit from it. Sure, like global asset allocation, tactical portfolio management does not assure a profit or guarantee protection against a loss, either. But, like any other action in life vs. inaction, it’s an attempt, which to me, is better than no attempt at all.

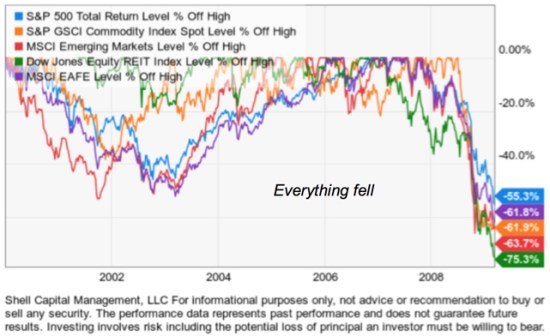

What I know is this: global markets can and do all fall together in times of crisis when investors who held their losses too long keep tapping out as prices fall.

Even the most respected global allocation funds participated in the waterfall decline enough to tap out most investors I know if they had invested in them – we didn’t.

I know some advisors and media have been criticizing the “hedge fund” side of the investment industry for years now because total returns haven’t been as high as the past. I don’t think passive indexing advisors have all that much to speak about themselves. Even the most aggressive index allocation that assumes no fees is a 26% gain in the past three years. That’s not an average gain, it’s a gain in capital.

More importantly, those numbers haven’t changed over the past 5 years. So, the past 5 years haven’t been so outstanding for anyone, especially factoring in the volatility.

In fact, it’s caused by volaltity. Volatility eats away at compounding capital positively.

Speaking of volatility, it’s the downside volatility we don’t like. Here are the historical drawdowns of these indexes since they launched in 2011.

If you look close, to get the return of global asset allocation, you’d have to hold through declines of -10% to -20% routinely. In a big bear market will be worse, which hasn’t happened since these indexes weRE made available.

That’s why I believe even a passive global asset allocation is a risky business and not an investment model I’m willing to offer. If people we know want global asset allocation, we show them a way to get it without us. We only offer what we believe is of value.

I can’t imagine what it would be like in 2011 when these global allocations were falling and all we can say is “Hopefully it stops falling?”

But, what if it doesn’t?

What if it keeps falling?

I believe everyone has a tap-out point. We can either determine it in advance or find out the hard way. The tap-out point will be tested over and over with global asset allocation.

But, 2019 wasn’t one of those years, so everyone has something to celebrate this year.

When the wind is blowing, we can let out the sail and enjoy the ride.

When the wind stops blowing, we have to row, not sail, or risk sinking.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.