When a market is rising, we can let out the sail and enjoy the ride, but when the wind stops, we row, not sail.

I started using this analogy in 2005 after reading my friend Ed Easterling’s book Unexpected Returns, which is a fine example of the distinction in mindset between tactical and dynamic risk management decisions vs. traditional (passive) asset allocation.

About sailing, he said:

Most investors, especially those with traditional stock and bond portfolios, profit when the market rises, and lose money when the market declines. They are at the mercy of the market, and their portfolios prosper or shrink as the market’s winds blow favorably or unfavorably. They are, in effect, simple sailors in market waters, getting blown wherever the wind takes them…

In sailing with a fixed sail, the boat moves because it grabs the wind; it grabs the environment and advances or retreats because of the environment. Relative return investing corresponds to this fixed-sail approach to sailing. When market winds are favorable, portfolios can increase in value rapidly. When the winds turn unfavorable, losses can accumulate quickly. Bull markets are the friends of relative return sailors, and catching the favorable bull market winds and continuing to ride them are the secrets to making money in a bull market.

About rowing, he said:

Rowing, as an action-based approach to boating, is analogous to the absolute return approach to investing. The progress of the boat occurs because of the action of the person doing the rowing. Similarly, in absolute return investing, the progress and profits of the portfolio derive from the activities of the investment manager, rather than from broad market movements.

Around 2005 I taught a course to portfolio managers via DWA Global Online University on presenting global tactical investment management and dynamic risk management to investors because it was challenging to get clients to understand why we row, not sail.

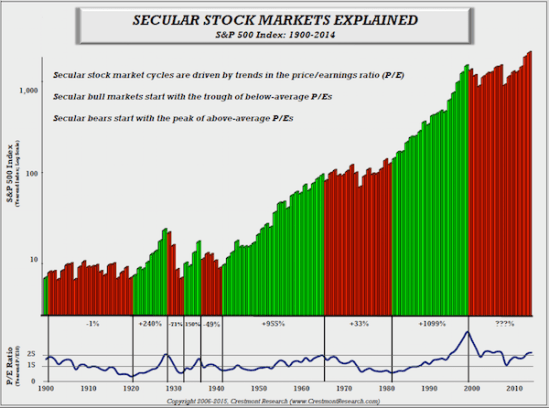

For example, we use a chart like this one to illustrate the secular bull and bear market periods are made up of several years of uptrends followed by several years of crushing downtrends.

It doesn’t matter if you gain 100% or 200% in an uptrend if you lose your gains in a -50% downtrend.

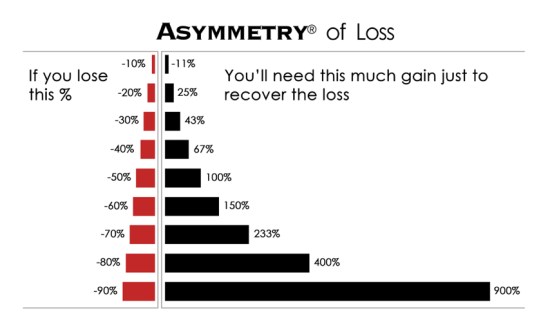

The foundation of my ASYMMETRY® Investment Program that focuses on asymmetric risk/reward is a deep understanding of the mathematics of loss. Most of the investment industry tells investors they should hold on through losses. However, I believe investors’ natural instinct to limit loss is mathematically correct.

As we show in more detail on ASYMMETRY® Managed Portfolios: As investors are loss averse, losses are also asymmetric. So, the natural instinct to avoid large losses is mathematically correct.

A -50% decline requires a gain of 100% just to get back to where it started.

For example, the more than -50% loss in U.S. stock indices from October 9, 2007, to March 9, 2009, wasn’t recovered until late 2013, nearly six years after it started.

The -50% loss took a 100% gain and six years to recover.

As losses increase, more gain is necessary to recover from a loss. The larger the loss, the harder it becomes to get back to the starting point before the loss. This asymmetry of loss is in direct conflict with investors’ objectives and provides us with a mathematical basis for active risk management and drawdown control.

This is why I row, not sail.

When a market is rising, we can let out the sail and enjoy the ride, but when the wind stops, I get out the oars and start rowing.

I prefer not to sink to the bottom.

The last bear market may be becoming a distant memory of investors, but those who forget the past are doomed to repeat it.

Don’t.

It doesn’t matter how much the return is if the downside is so high you tap out before it’s achieved.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.