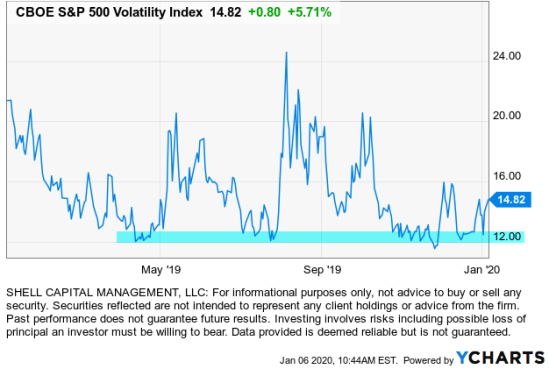

To no surprise, the CBOE S&P 500 Volatility Index that represents the market’s expectation of 30-day forward-looking volatility, is trending up.

So far, it isn’t much of a volatility expansion, but it’s elevated somewhat higher than it was. At around 15, the VIX is also well below its long term average of 18.23, although it hasn’t historically been drawn to the 18-20 level, anyway. The average is skewed by the spikes in volatility; volatility expansion.

VIX is at a current level of 14.82, an increase of 0.80 or 5.71%% from the previous market day.

Here are the 50 and 200-day moving average values for VIX.

As I shared over the weekend, and it was quoted in today’s MarketWatch article “U.S.-Iran tensions will spark increased volatility — here’s how to play stocks, fund manager says“:

“So, on a short-term basis, the stock indexes have had a nice uptrend since October, with low volatility, so we shouldn’t be surprised to see it reverse to a short-term downtrend and a volatility expansion.

“For those who were looking for a ‘catalyst’ to drive a volatility expansion, now they have it.”

I was referring to the U.S. conflict with Iran, of course.

The VIX index value is derived from the price inputs of the S&P 500 index options, it provides an indication of market risk and investors’ sentiments. VIX measures the implied ‘expected’ volatility of the US stock market. So, many market strategists use the VIX as a gauge for how fearful, uncertain, or how complacent the markets are. The VIX index tends to rise when the market drops and vice versa. During the 2008-2009 bear market, the VIX trended up as high as 80.86. Although the VIX cannot be invested in directly, securities like ETFs and derivatives based on it may provide the potential for an asymmetric hedge. For example, over the past year when the S&P 500 stock index was down -1% or more on the day, some of the ETFs based on long volatility spiked 10% or more. Volatility is difficult to time right, but when we do the payoff can be asymmetric. An asymmetric payoff is achieved when the risk-reward is asymmetric: maybe we risk 1% to achieve a payoff of 5%. Since long volatility has the potential for big spikes when volatility expands, it’s asymmetric payoff doesn’t require the tactical trader and risk manager to be as ‘right’ and accurate. So, the probability of winning can be lower, but the net pay off over time is an asymmetric risk-reward.

You can probably see why I pay attention to volatility and volatility expansions.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.