Why invest in international markets? someone asked.

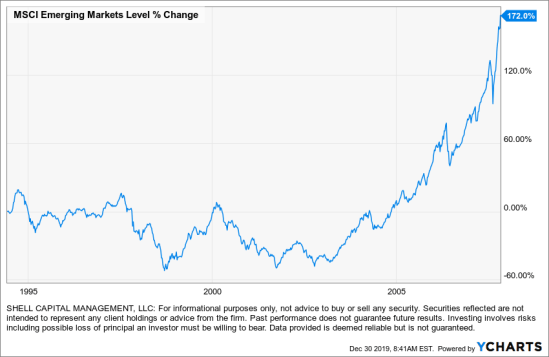

Go back to 2007 and it was more obvious. I remember just the opposite questioned posed then; why not invest it all in Emerging Markets? Of course, that was after this:

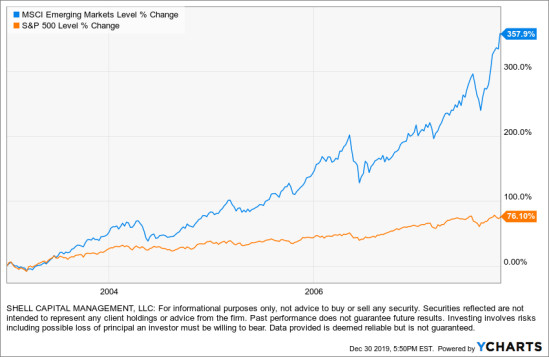

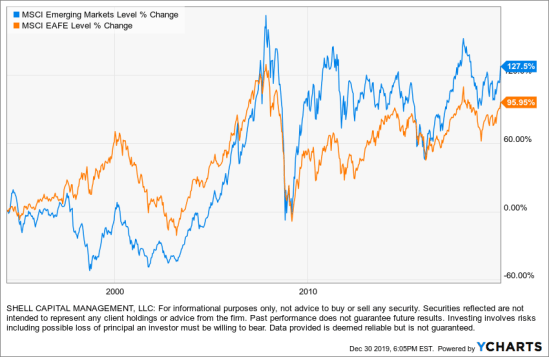

Emerging markets were the dominant trend from 2003 to 2007. As the chart shows, it wasn’t even close: 358% for the MSCI Emerging Markets Index vs. 76% for the S&P 500 U.S. stock index.

The MSCI Emerging Markets Index represents securities that are headquartered in emerging markets countries. An emerging market is considered a country that has not yet become developed because of economic characteristics. These countries tend to present a unique investment opportunity because of the nature of their growth potentials.

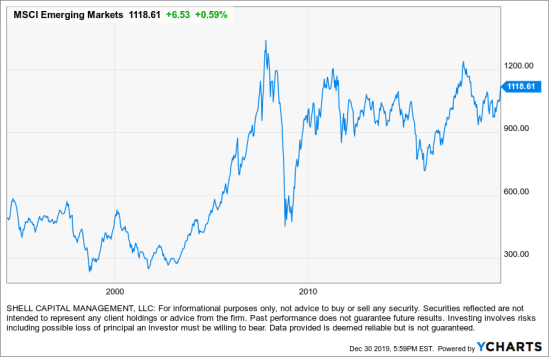

However, emerging countries aren’t without risk. MSCI Emerging Markets Index has had three notable drawdowns greater than 50% in 1998, 2001, and 2008.

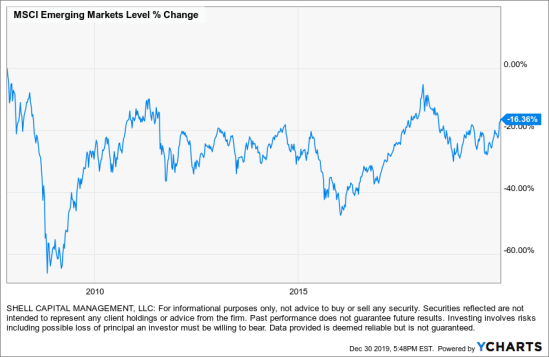

Back in 2007, when someone asked me “why not invest it all in Emerging Markets” I guessed it was likely the end. Even though the person was born in a foreign country and did business globally, the enthusiasm was a sign. Doing business around the world doesn’t make someone a global investment expert. As this investor did indeed invest their money in Emerging Markets as he confirmed when I saw him a few years later, the timing was terrible. In fact, based on the MSCI Emerging Markets Index chart since 2007 it sill is.

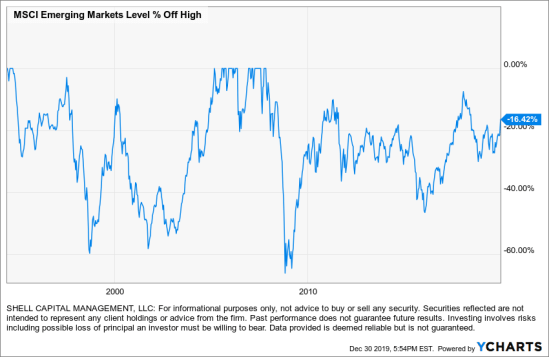

As we see the full history below, although international stock markets like Emerging Markets can have periods of drawdowns and otherwise non-trending times, there are still potentially profitable price trends that may be captured with a robust tactical method. I’ve avoided EM for a while now for obvious reasons.

Then, there are developed international markets. The MSCI EAFE Index tracks large-cap and mid-cap companies in developed countries around the world. The index primarily covers the Europe, Australasia, and the Far East regions. This index is used as an important international benchmark. The index has had large drawdowns in 2003 and 2009, which were largely due to recessionary periods. As you can see in the chart, the performance was similar to Emerging Markets. However, the gains on the upside weren’t as much.

You can probably see why investors aren’t talking about these international stocks the last several years. We won’t hear about it until after they trend up a lot and make headlines and magazine covers. I’m a global tactical manager, but I’ve avoided EM and DM for many years now for obvious reasons, unlike global asset allocation which invests in it all the time.

I’m unconstrained and tactical, so I shift between markets based on trends and countertrends, rather than allocating to them for constant exposure to the risk-reward.

The chart above doesn’t exhibit asymmetric risk-reward by itself, but my special weapons and tactics aim to extract it from what is there.

More recently, I’ve mostly focused in high dividend yield global stocks. But, there will come a time when this market are the place to be and when they do, I have 30 other countries outside the United States in my universe.

Have a question or comment? shoot me an email below:

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Any opinions expressed may change as subsequent conditions change. Do not make any investment decisions based on such information as it is subject to change. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect a position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.

You must be logged in to post a comment.