The demand for retirement expertise is strong and getting stronger. In my career over more than two decades, I’m not only observing an aging client base but also a noticeable increase in the number of people over fifty looking for income from their investments.

I don’t always call it “retirement” as it’s really “freedom.”

I don’t necessarily call it “financial freedom” because freedom is freedom, and it’s hard to have it without the financial part squared away.

As my wife Christi and I are rapidly approaching 50 ourselves with seemingly more momentum we’re noticing we are around more and more friends who are looking forward to the shift from “working for a living” to their money working for them.

I call it “getting off the treadmill,” and not everyone wants to get off the treadmill, but when you are ready to, you need a plan.

We create plans for getting off the treadmill and more importantly, staying off it.

But that isn’t my topic today. Today we have a simple topic relative to retirement income portfolio management. That’s what most call it. I just think of it as replacing earned income from working or running a business with passive income from not having to physically “do” things to get money income.

As an active investment manager, I’m not otherwise a fan of anything passive. There is nothing about what I’m going to share here that is passive for me, but it is for investors who want to get a check and go enjoy doing whatever it is they want to do with their time.

Here we go.

The word “correlation” is a statistical term that is grossly overused in the investment industry, but there may be no better true example than the negative correlation between price and yield (or interest rate.)

When the price of a stock or bond that is paying dividend or interest FALLS, its yield from that starting point RISES.

Conversely, when the price of a stock or bond that is paying dividend or interest RISES, it’s yield FALLS from that starting point.

It’s an inverse correlation and the one time when I switch from a trend-following strategy to a countertrend strategy.

If I want high income, I necessarily aim to buy low and sell high through the trend cycles.

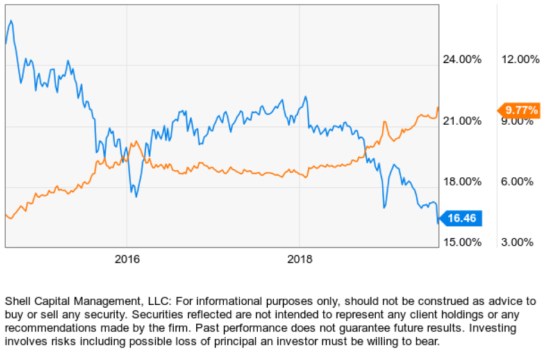

I’ll share a very straightforward example, but I’ve removed the name of the fund. This ETF is one I actually own and since my mission here isn’t to make recommendations to people I don’t know or promote a position I have in my ASYMMETRY® High Income Yield portfolio, we’ll just leave off the name. Instead, let’s focus on the price and yield trends.

One advantage of falling stock prices is as price falls, the dividend yield rises from that new price. In the example below, the blue line is the price trend over the past five years. The orange line is its dividend yield. You can see when the price declines, the yield from that staring point rises.

If we buy it after it falls, our yield percentage is based on what price we buy it. Of course, that’s assuming all its holdings continue to pay their dividends/interest. This isn’t risk-free, so I add some risk management techniques to the overall strategy.

The bottom line is, when we look at the blue line above, that’s the price, and it has declined to the lowest point in five years. However, the orange line, which is the dividend yield on this ETF is at an all-time high.

If it’s high income we want from our savings, we want to buy after the price falls, then may sell, or hedge, to reduce exposure after the price trends up to an extreme.

When we buy high yielding assets at lower prices, the dividend payment is higher from that starting point as long as the companies we invest in keep paying their dividends. In this example, this one ETF alone invests in over 100 of the highest dividend-yielding equity securities around the world.

One of the primary risks of high dividend-yielding securities is rising interest rates. Over more than a decade, we’ve seen the central banks drive interest rates from one extreme to another. As the chart of the Prime Rate shows, they lowered rates from 8% in 2007 all the way to 3.25% and kept it at that historically extreme low level. Starting in 2016, the Federal Reserve started raising interest rates. By last year, the Prime Rate had reached 5.5%. The Fed recently lowered the rate to 5.25%.

Economic data now suggests the Fed may continue to lower interest rates.

So, instead of a rising interest rate environment, we may see a falling interest rate environment.

The bad news is; if the Fed keeps lowering rates, historically, the Fed has lowered rates to ward off recession or when it sees substantial risks of a downturn.

The good news is, these falling prices are creating an opportunity for investors who want to build a high-income portfolio through dividend yield and interest.

Of course, if that sounds like you, you don’t want to wait until it happens to get started. If you look closely at the chart again, there are seasons and cycles to increase and decrease exposure.

What we are seeing now is a new opportunity to add exposure.

I’m not saying to randomly go pick high yielding dividend stocks or ETFs. Like any investment, it isn’t risk-free. Investing always involves risk, including the possible loss of principal. High yielding stocks are often speculative, high-risk investments. So, portfolio management requires actively managing the risk along with diversification. Some high dividend companies can be paying out more than they can support and may reduce their dividends or stop paying dividends at any time, which could have a material adverse effect on the stock price of these companies and the Fund’s performance. International investments additionally involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles, or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume.

The bottom line is; there is no free lunch. If we want the potential for return, we have to be willing to take the risks we are willing to take, and tactically manage or hedge the risks we want to limit.

As with most things in life, timing is everything. We don’t have to get the timing perfect, just good enough to result in asymmetric risk/reward.

Right now, I see interesting asymmetric risk/reward setups in some of these securities we use to build our high-income portfolio. That is, the potential for future capital gain from price appreciation and high income from the dividend yield seems more elevated than the downside risk.

Of course, if I predetermine my downside risk as I do, I can skew the payoff asymmetrically.

For example, in the case above, this fund of 100 stocks is yielding about 10% from this price. If I invest in it today, the future expected return from the dividends alone would be approximately 10% a year from now, and it pays monthly. You can probably see how attractive that sounds to someone who wants to live off their capital. Let’s see a simple example of the possibility of asymmetry.

Price Falls: As its price has already fallen sharply and its yield has increased to nearly 10%, I may believe it won’t drop a lot more. However, even though it may be oversold, I could predetermine an exit of only -5% below the current price. If it falls -5% after I buy it, I could sell it and take the loss and move on. But, these positions are unique. It isn’t just about the price trend. As price falls, its income-generating potential is increasing. So, a falling price actually increases the future asymmetric risk/reward payoff potential.

Price Stays the Same: If the price stays the same for a year, we will earn about 10% from the dividends. If I only risked 5% on the position and it trended up instead of down and stayed the same for a year, our asymmetric risk/reward is 2:1. I risked 5% to earn 10%.

Price Trends Up: The best outcome is I buy it, and the price goes up, and we also earn the 10% income from the yield. If the price gained 10% and the yield paid 10%, the total return would be 20%. If I risked 5% to earn 20%, the asymmetric payoff is 4:1.

You can probably see why I call this strategy ASYMMETRY® High Income Yield.

Questions? feel free to email me.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

Mike Shell and Shell Capital Management, LLC is a registered investment advisor and provides investment advice and portfolio management exclusively to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data is deemed reliable, but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. Use of this website is subject to its terms and conditions.

You must be logged in to post a comment.