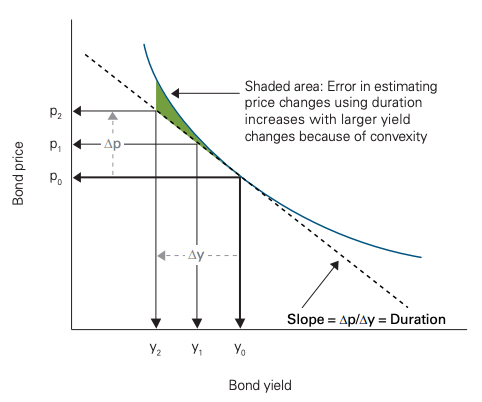

Convexity captures the asymmetry in the connection between bond prices and changes in interest rates.

Duration only captures one aspect of the relationship between bond prices and interest rate changes. For more significant interest rate trends, the correlation between the change in rates, and the change in bond prices is asymmetric.

The bond price decrease resulting from a substantial interest rate increase will typically be less than the price increase resulting from an interest rate decline of the same magnitude.

This asymmetry arises from the convex payoff pattern shown by the solid curved line in the chart below.

It plots the relationship between the yield of a bond and its price.

The dashed line estimates the consequence of a change in yield on the price of the bond.

This convex pattern also means a portion of the interest rate move continues uncaptured by duration.

Duration is a measure of interest rate risk and is mathematically derived from the slope of the dashed line.

The curved line represents convexity.

Convexity is a measure of the degree of the curve in the correlation between bond prices and bond yields.

Convexity captures the asymmetry.

You must be logged in to post a comment.