There is a lot of talk nowadays about “Smart Beta”. Smart beta refers to an investment style where the manager passively follows an index designed to take advantage of perceived systematic biases or inefficiencies in the market. Smart beta defines a set of investment strategies that emphasize the use of alternative index construction rules to traditional market capitalization based indices.

Low volatility or managed volatility, for example, is considered a version of “smart beta” because its weights the stocks (and therefore sector exposure) differently:

The PowerShares S&P 500® Low Volatility Portfolio (Fund) is based on the S&P 500®Low Volatility Index (Index). The Fund will invest at least 90% of its total assets in common stocks that comprise the Index. The Index is compiled, maintained and calculated by Standard & Poor’s and consists of the 100 stocks from the S&P 500® Index with the lowest realized volatility over the past 12 months. Volatility is a statistical measurement of the magnitude of up and down asset price fluctuations over time. The Fund and the Index are rebalanced and reconstituted quarterly in February, May, August and November.

I bolded the main difference between this index ETF and the traditional capitalization-weighted S&P 500. The S&P 500 everyone knows about weights is 500 stocks holdings based on market capitalization, so the largest stocks are the largest positions in the index.

The Low Volatility Portfolio is really a play on sector allocation. Because it creates its position size based on each stocks past 12 months volatility, it’s weighting will simply depend on what was less volatile the past year. And, it will look back to rebalance and reconstitute quarterly in February, May, August and November. So, you may consider what it really does is shifts the position size and sector weighting.

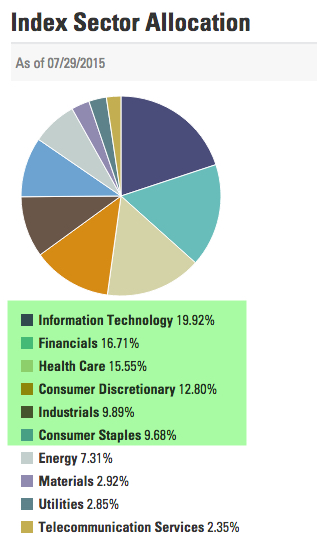

Below is the index sector allocation for the S&P 500 like what is used for SPDR® S&P 500® ETF so we can see which sectors have the largest position size.

Source: https://www.spdrs.com/product/fund.seam?ticker=spy

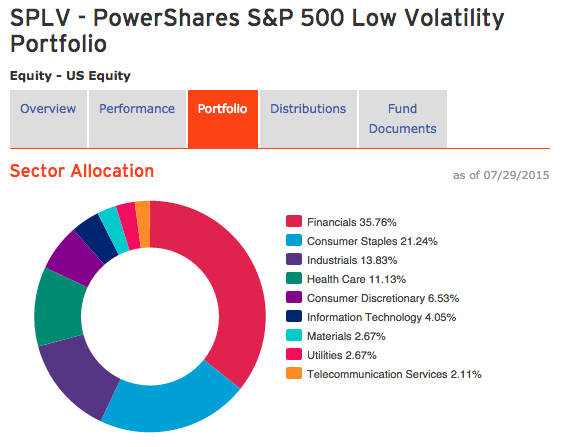

Now we observe the sector allocation of the PowerShares S&P 500 Low Volatility Portfolio. Notice is is heavily weighted in Financials (36%) and Consumer Staples (21%). That’s simply because those sectors stocks have demonstrated less realized volatility as measured by standard deviation over the past 12 months.

Source: https://www.invesco.com/portal/site/us/financial-professional/etfs/product-detail?productId=SPLV

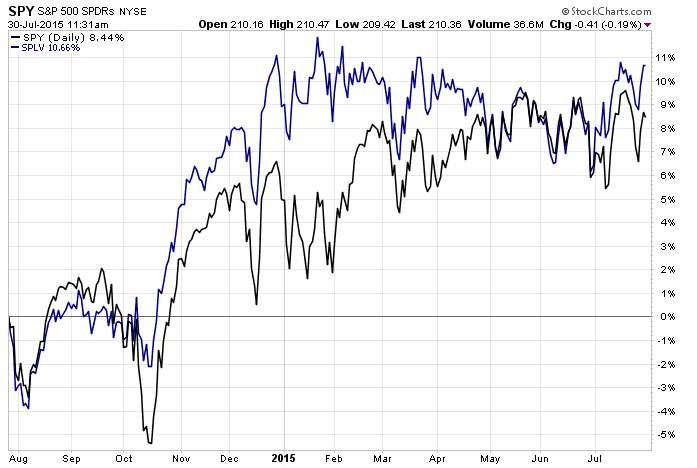

Now, let’s observe the difference in return streams. Below is a relative strength comparison of the two since inception of PowerShares S&P 500® Low Volatility Portfolio in May 2011. As you see, the low volatility index did have a smaller drawdown in 2011, but overall they’ve tracked the same most of the time. The real difference was the lower drawdown from the sector weighting helped reduce the loss in 2011 and that helped smooth out the returns for a few years. Since 2013 U.S. stock volatility declined, so that explains why the two indexes have trended more closely since.

Source: Shell Capital Management, LLC with http://www.stockcharts.com

Over the past year, there is a little more divergence at times as we see below.

Source: Shell Capital Management, LLC with http://www.stockcharts.com

You may consider that past realized volatility may not repeat into the future. In fact, it could reverse. But the real difference between these is the trailing realized volatility weighting changes the sector weighting. The sectors are the driver. Which sectors have the lowest 12 month historical volatility will determine the exposure to a volatility weighted index or fund. The risk to volatility weighting is the volatility of markets sometimes reach its lowest point at its peak in price as investors become more and more complacent and less indecisive, which is what causes a wider range in prices. I explained this in This is When MPT and VaR Get Asset Allocation and Risk Measurement Wrong.

Though the widening range of prices up and down gets our attention, it isn’t really volatility that investors want to manage so much as it is the downside loss of capital. I really manage volatility by actively increasing and decreasing exposure to loss.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Global Tactical.

Mike Shell and Shell Capital Management, LLC is a registered investment advisor and provides investment advice and portfolio management exclusively to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and are not specific advice, research, or buy or sell recommendations for any individual. For informational purposes only and should not be construed as advice to buy or sell any security. Securities reflected are not intended to represent any client holdings or any recommendations made by the firm. Investing involves risk including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information provided is deemed reliable, but is not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. Use of this website is subject to its terms and conditions.

You must be logged in to post a comment.