Are We Entering a Civil War? Or Entering the Phase That Precedes It?

The question keeps surfacing because something feels structurally different.

Not louder politics.

Not sharper rhetoric.

What people are sensing is a shift in how internal conflict is absorbed by the system.

Two independent, long-cycle frameworks help explain why this question is being asked now.

In The Changing World Order, Ray Dalio, founder of Bridgewater Associates, the world’s largest hedge fund, shows that escalating internal conflict is a recurring feature of late-stage debt and power cycles.

In The Fourth Turning Is Here, historians William Strauss and Neil Howe describe the same phase as a generational “Crisis” period—when existing institutions struggle to resolve new stresses.

Different lenses.

Same phase.

Civil Wars Don’t Start With Violence

History shows that civil wars are rarely the opening act.

They are the failure state—what happens after institutions lose the ability to mediate disagreement.

The conditions that tend to precede them include:

- Loss of trust in institutions

- Competing definitions of legitimacy

- Zero-sum political incentives

- Perceived unfairness in opportunity and outcomes

- A belief that the rules no longer apply evenly

These conditions can persist for years without open conflict.

But once they stack, the system becomes fragile.

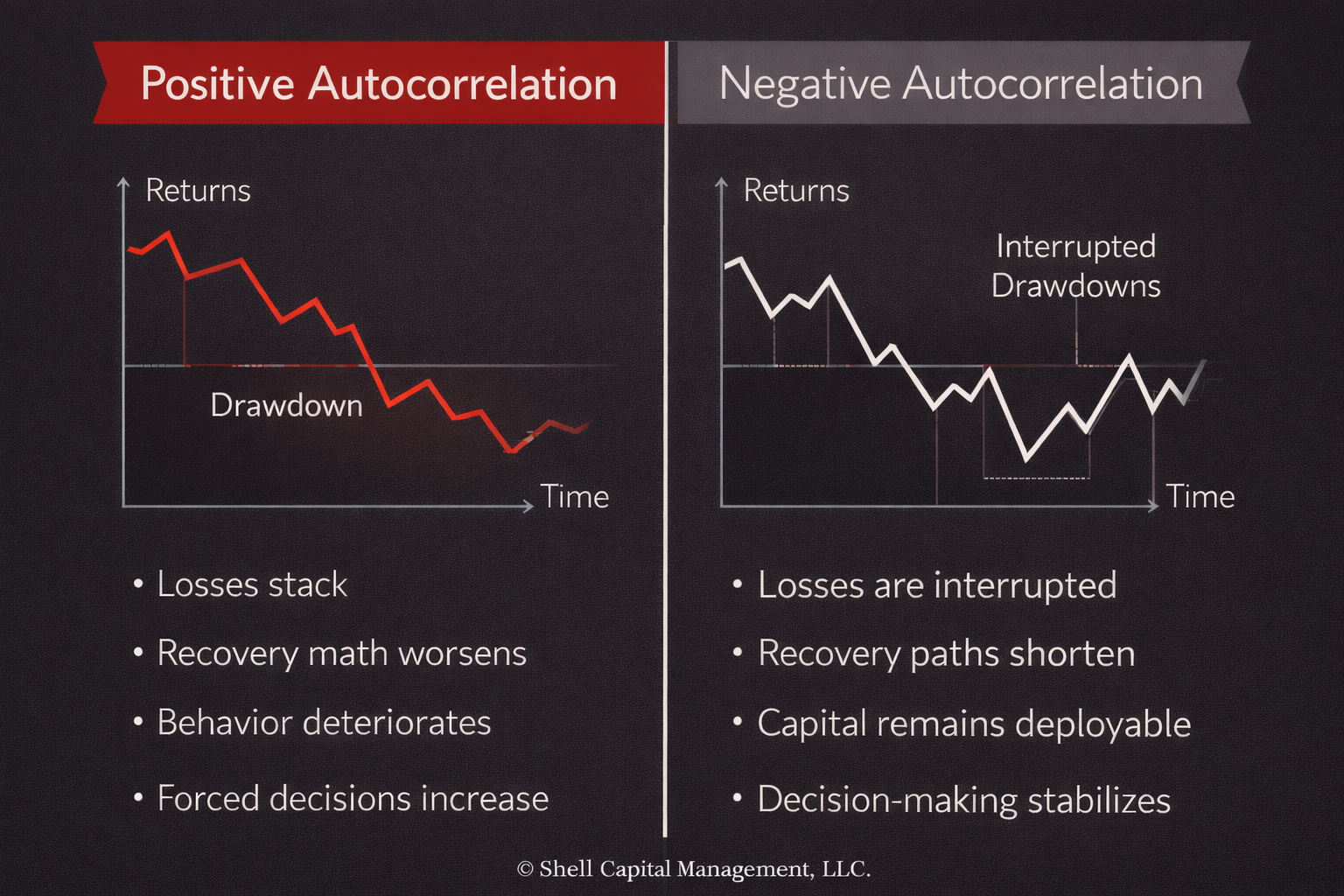

Escalating Conflict Is the Accelerator

Neither Dalio nor Strauss and Howe argues that internal conflict automatically leads to civil war.

They argue something more precise:

Internal conflict accelerates whatever comes next.

As it escalates:

- Compromise becomes politically costly

- Decision-making degrades

- Rules lose legitimacy

- Power replaces process

The system still functions—but with less shock absorption.

That’s where asymmetry appears.

Why This Phase Feels Unstable

Late-cycle conflict is nonlinear.

- Stress builds quietly.

- Confidence erodes gradually.

- Then reactions become abrupt.

Small events provoke outsized responses.

Narratives harden.

Institutions lose the benefit of the doubt.

This doesn’t require violence to matter.

Markets, capital, and behavior reprice well before that.

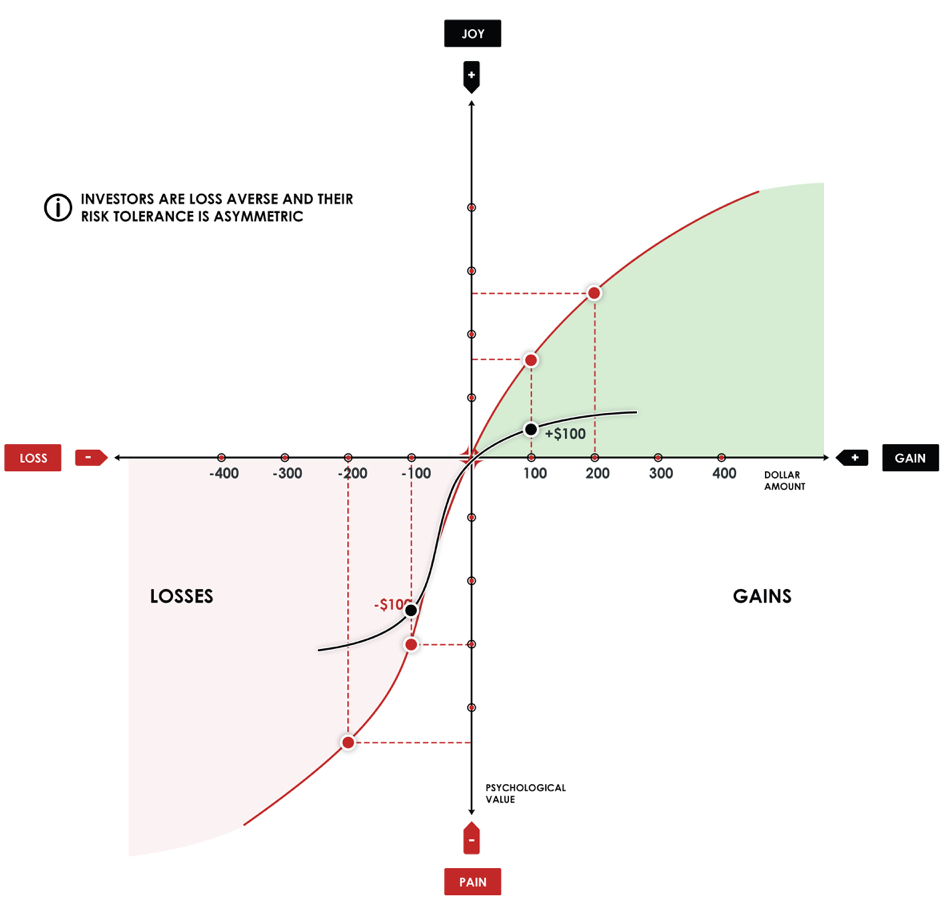

The Real Risk Isn’t Civil War

The real risk is assuming stability is guaranteed.

Dalio’s work shows how internal disorder weakens empires financially and institutionally.

The Fourth Turning shows how generational pressure forces confrontation and restructuring.

Together, they imply:

- Outcome distributions widen

- Policy paths become discontinuous

- Downside becomes heavier than models suggest

That’s negative asymmetry.

The ASYMMETRY® Perspective

This isn’t a prediction of civil war.

It’s a recognition of the phase.

Late-cycle systems don’t usually collapse overnight.

They lose resilience first.

They still operate.

Just with less margin for error.

Asymmetric risk management in this environment isn’t about forecasting the worst outcome.

It’s about designing exposure that survives multiple futures.

History doesn’t punish people for being cautious.

It punishes them for assuming the recent past is permanent.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

The observations shared in ASYMMETRY® Observations are for general informational purposes only and do not constitute investment advice or a recommendation to buy or sell any security. The content is not intended to provide a complete description of Shell Capital’s investment process or strategies and should not be relied upon in making investment decisions.

Securities, charts, indicators, formulas, or examples referenced are illustrative in nature and are not intended to represent actual client holdings or recommendations. Past performance is not indicative of future results. Investing involves risk, including the potential loss of principal.

Any opinions expressed are subject to change without notice as market conditions evolve. All information is believed to be reliable but is not guaranteed and should be independently verified. Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement.

This material is not intended as an offer or solicitation for advisory services in any jurisdiction where such offer or solicitation would be unlawful.

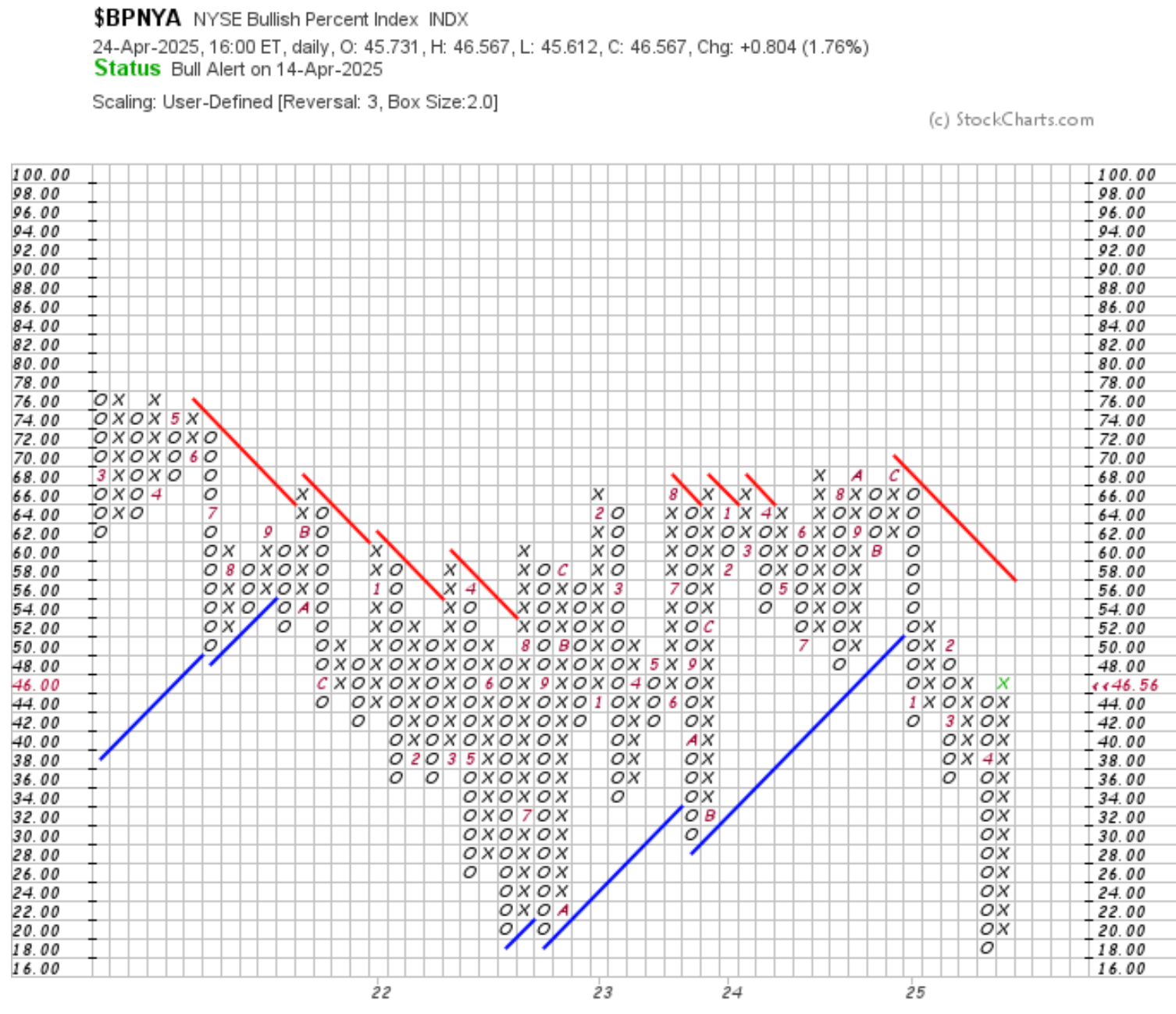

In the sector snapshot, seven sectors have zero percent of their stocks trading above the 5-day and 20-day moving averages. Technology, Energy, Materials, Industrials, and Communication Services are effectively in a state of internal collapse. Even Consumer Discretionary and Financials show only marginally better participation.

In the sector snapshot, seven sectors have zero percent of their stocks trading above the 5-day and 20-day moving averages. Technology, Energy, Materials, Industrials, and Communication Services are effectively in a state of internal collapse. Even Consumer Discretionary and Financials show only marginally better participation.